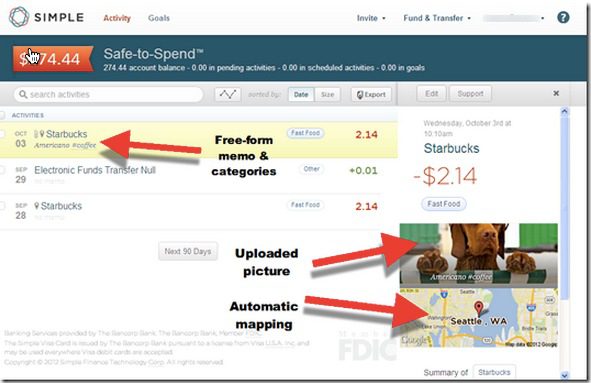

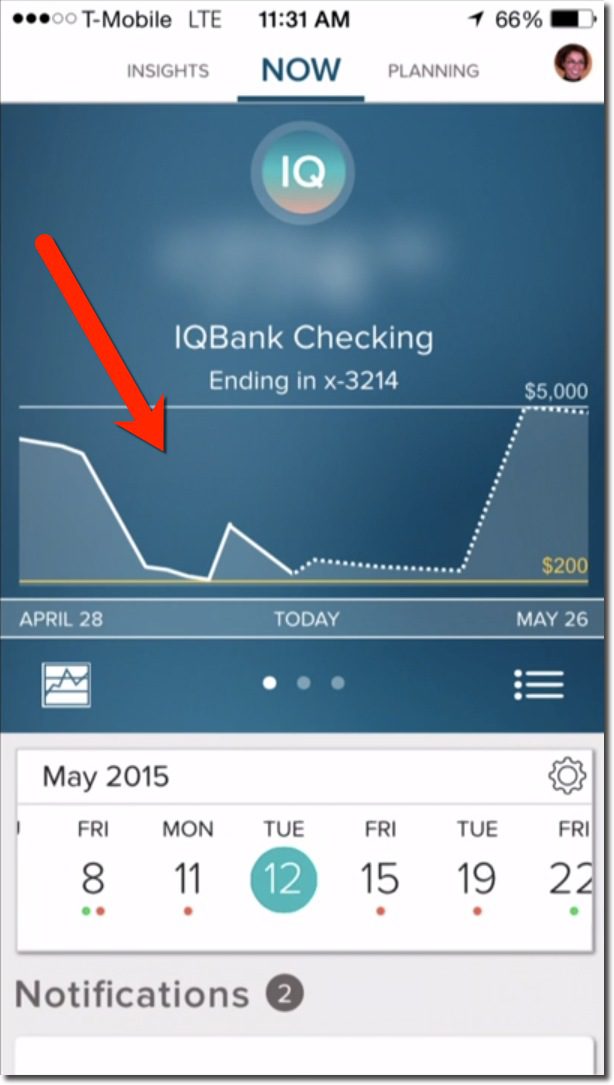

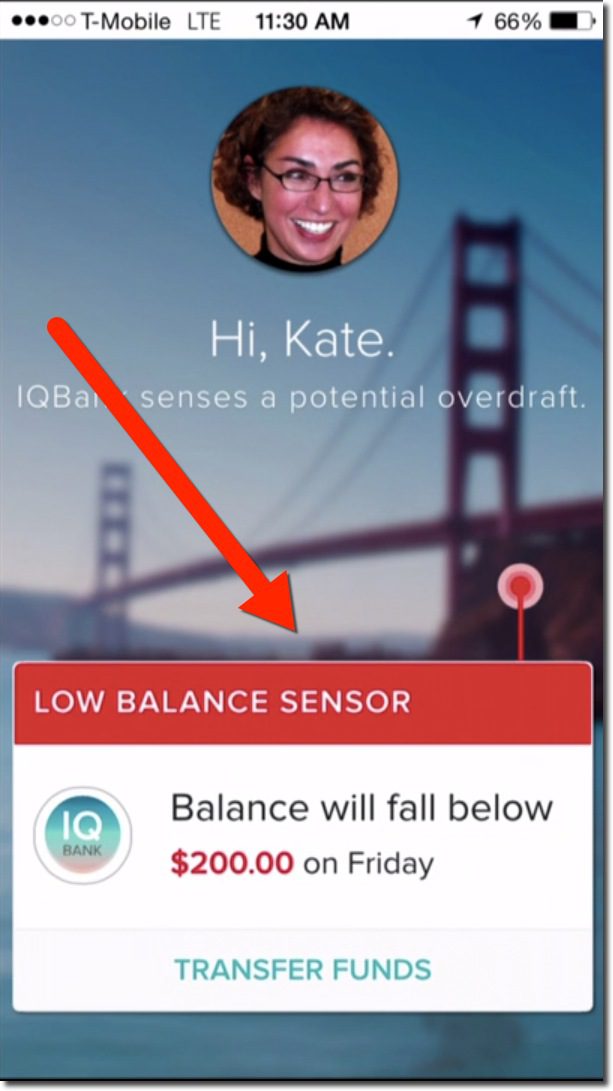

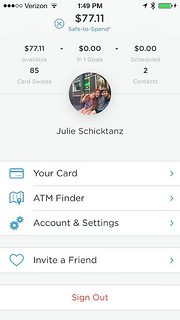

Definition: Neo-Bank

Delivering banking services without touching the funds

————————-

This morning, Celent’s Stephen Greer published a post called, The Challenges of the New Neo-Bank, wherein he states:

In recent months, the neo-bank model (e.g., Simple, Moven, GoBank) has hit a few stumbling blocks that call into question the promise of the digital-only model…

Stephen lays out four scenarios for the future of neo-banks:

1. Neo-banks are acquired and assimilated into larger financial brands

2. Larger brands start their own digital “neo-bank-like” brands

3. Neo-banking fails to become a viable business model, but nevertheless influences the industry

4. Neo-banking becomes the dominant method of accessing underlying accounts held at traditional banks

My thoughts: We already see #1 and #2 happening, so the question comes down to whether we are headed long-term towards #3 or #4. Like most analysts, I’m firmly in the “it depends” camp. But I’ll go out on a limb a bit. I believe we will see dozens, if not hundreds, of neo-banks launch in the next few years. Here’s why:

1. Simple’s $100-million exit to BBVA

1. Simple’s $100-million exit to BBVA

I’m not sure how much equity the founders held at the end, but it must have been a multi-million dollar payday for five-plus years of hard work. While that’s not enough to make the cover of Forbes, it’s a huge win for most entrepreneurs.

2. Marketplace lending provides a path to profitability

The problem with the neo-bank model in an era of low deposit rates and shrinking interchange, is that those traditional income sources are not enough to pay competent developers, execs and customer service folk. With consumers loath to pay fees, most startups end up forced into the ad-supported model, which strains their credibility with customers.

But with the growing popularity, and proven profit potential, of marketplace lending (aka P2P lending), neo-banks can partner with or build their own loan platforms to profitably put those deposits to work (sounds less “neo” and more “banking” doesn’t it?). So I envision the day where neo-banks allow you to store your funds in the prepaid account for no interest, or put it to work in a lending marketplace to earn a few percentage points on the funds, with the neo-bank pocketing a bit of the spread.

3. Third-party financial watchdogs become trusted services

Another advantage of being an independent neo-bank is that it’s easier to become an unbiased watchdog over all things financial. The neo-bank can track all your accounts (Mint/Yodlee), find areas where you are overpaying or have potentially been defrauded (BillGuard), monitor your credit score (Credit Karma) and even analyze the effectiveness of your 401k (Brightscope).

Right now, it’s still almost impossible for third-party startups to get to scale because customers just don’t trust them. But that will slowly change as the newcomers gain brand recognition (for example, Intuit’s Quicken, Quickbooks, and TurboTax brands).

4. It’s much, much harder to launch a real bank

Ten years ago, we were seeing about 10 new banks launched every month. Due to all the failures brought on by the Great Recession (and I would argue, way too much deposit insurance), there has only been one new bank launched in the past three years (through end of 2013). So, if you want to get a banking business started, you have little choice but to go with a non-bank model.

—————

Comments? Give me a shout @netbanker

Picture credit: Article from NY Times, 20 Feb 2014 (link); sign in background from Simple HQ