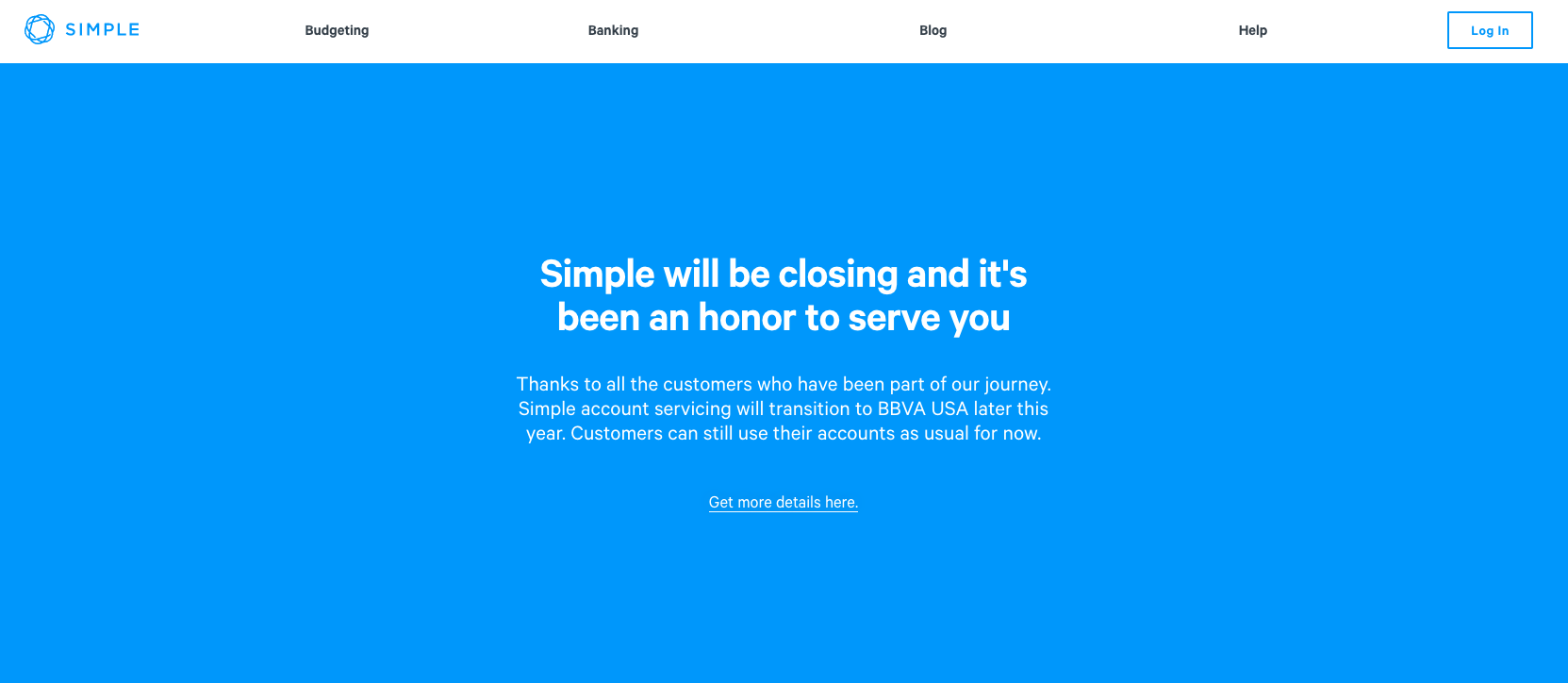

You’ve likely heard that BBVA has decided to shutter Simple, its in-house challenger bank. Yesterday, the company sent an email to accountholders stating, “BBVA USA has made the strategic decision to close Simple.”

The reactions across fintech are mixed– some say they’re not surprised, and others have expressed more nostalgia than anything.

Those who aren’t surprised cite PNC’s recent acquisition agreement with BBVA. The two may have been trying to streamline their businesses in order to minimize duplication of market coverage and services. There’s also the fact that competition in the challenger bank space is hotter than ever, and it doesn’t make sense for BBVA (or PNC, for that matter) to try to keep up with the marketing spend that others such as Chime have shelled out to acquire customers.

Since this is a eulogy, however, I’ll focus on the nostalgia. Simple was founded in 2009 as BankSimple and quickly became one of the top pioneers in the challenger banking space. I like to think of Simple as the grandfather of challenger banks (perhaps the grandmother is Moven, which closed its B2C model last year).

Simple was ahead of its time in focusing on the millennial client base that is untrusting of banks and prefers a straightforward, transparent approach. The bank also offered features that were unique at the time, such as geolocation via an integration with Google maps for every transaction, instant purchase notifications, and a “safe to spend” balance that indicated the user’s discretionary spending balance.

The bank’s young, Portland, Oregon-based staff were consistently quirky and upbeat on customer service phone calls. Simple maintained this culture even after BBVA acquired it in 2014.

Does anyone remember Simple’s catchphrase when it launched? “We don’t suck.” Hopefully the new generation of challenger banks will keep this mantra in mind as they work on creating the new wave of consumer-first banking technology.

As for what’s next, Simple’s email to clients went on to detail what to expect, stating, “In the future, your Simple account will become exclusively serviced by BBVA USA, but until then you can continue to access your account and your money through the Simple app or online at simple.com. You will receive additional information in the near future about the transition of your account servicing to BBVA USA.”

So long, Simple, you will be missed.

Seven months after

Seven months after

{kind=link}