This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

The US Treasury tapped Robinhood and BNY to power and manage Trump Accounts, the new government-backed, tax-deferred investment program for children seeded with $1,000 at birth.

The platform will be fully white-labeled and operated by the Treasury, with Robinhood providing the technology, UX, education, and customer support behind the scenes.

The deal marks a strategic shift for Robinhood from consumer brokerage to infrastructure provider.

The United States Treasury Department announced today that digital stock brokerage app Robinhood will build the brokerage platform and serve as the initial trustee for Trump Accounts, the new custodial-style Individual Retirement Accounts for children under 18.

The department selected BNY as the financial agent for the Trump Account program. BNY will be responsible for managing the initial accounts and has selected Robinhood to help develop the new Trump Accounts app. The new standalone Trump Accounts app will be fully white-labeled with no Robinhood branding and will offer an intuitive user interface and user experience that will help families to view and manage their Trump Accounts.

Along with building the front-end experience, Robinhood will also create educational resources and manage customer support for Trump Accounts.

“We are proud to power Trump Accounts with Robinhood’s technology and to work alongside a historic and trusted institution like BNY,” said Robinhood Markets CEO Vlad Tenev. “Our task is clear: to provide the next generation of Americans with a world-class, intuitive platform to jumpstart their financial future.”

Trump Accounts launch on July 4 and will serve as tax-deferred investing accounts for children. Babies born between 2025 and 2028 receive a one-time $1,000 deposit from the Treasury to seed their retirement. Currently, more than four million children have been signed up for a Trump Account. As part of its efforts, Robinhood said it plans to match the Treasury’s $1,000 contribution to Trump Accounts for eligible children of its employees.

Once the app is built, the US Treasury will retain control over the app and the operations for all accounts. The Treasury did not disclose any financial details around the agreement.

“We continue to believe that the American stock market remains the greatest wealth creation vehicle of our time,” the company said in a statement. “…by providing young Americans with a dedicated platform to engage with the markets early, Trump Accounts will help millions of citizens maximize the power of compounding and build a lasting financial legacy.”

The move positions Robinhood as an infrastructure provider. By powering a federally backed investing program at scale, the company is moving beyond consumer brokerage and into the realm of embedded financial services.

Even without branding, this partnership gives Robinhood access to one of the largest distribution channels in retail investing and demonstrates its ability to operate as a trusted backend provider for government-led initiatives. While Robinhood still values owning the customer relationship, it is now expanding its scope to own the rails, as well.

ASN Bank has forged a strategic technology partnership with core banking platform provider Ohpen.

Ohpen will deliver an integrated SaaS platform that provides mortgage origination, servicing, and credit management.

Founded in 2009, Ohpen made its Finovate debut at FinovateFall 2012 in New York. Matthijs Aler is CEO.

Netherlands-based ASN Bank announced a strategic technology partnership with cloud-native core banking platform Ohpen. The partnership will support the financial institution’s efforts to standardize and modernize its IT architecture, providing ASN Bank with a fully integrated SaaS platform that covers mortgage origination, servicing, and credit management. Ohpen’s platform will enable ASN Bank to transition away from legacy infrastructure that has limited the institution’s ability to implement new products and services, and hampered reporting transparency as well as operational efficiency. Beyond a simple technology upgrade, the partnership supports ASN Bank’s “Simplify and Grow” strategy to establish new foundations for its integral processes and systems.

“Modernizing our mortgage operations unlocks an effective performance in our ability to serve customers via our franchisees and intermediaries as key distribution partners for mortgages,” ASN Bank Director of Lending Bianca de Bruijn-van der Gaag said. “Simplifying and standardizing our end-to-end processes means we can organize our business operations more effectively and efficiently. For our customers and distribution partners, this will lead to enhanced customer experience in document handling and accelerated processing time.”

Ohpen’s core banking platform powers lending, mortgages, savings, investment, and pension products. The Amsterdam-based fintech enables banks and other financial services providers to modernize their banking infrastructure, streamline operations, and create end-to-end digital banking experiences for customers. The company will provide ASN Bank with a highly configurable origination engine, automated servicing workflows, and integrated credit management built on a unified data model. The solution offers higher levels of straight-through processing and a single source of data truth across the mortgage lifecycle. ASN Bank will also benefit from a solution that not only evolves without requiring major structural changes, but also helps the institution meet both current and future regulatory mandates.

“This is about more than replacing legacy infrastructure,” Ohpen Director Jan Lamber Voortman said. “It is about giving ASN Bank the agility, transparency, and operational efficiency required for the next decade. Cloud-native architecture, configurable product design, and unified data are no longer differentiators. They are foundations.”

Full implementation of the new technology is expected to be completed by the end of 2027. The process will also include structured change management and internal ambassadors across underwriting and servicing teams to ensure successful cultural and technical adoption.

Headquartered in Amsterdam, Ohpen made its Finovate debut at FinovateFall 2012. The company has more than €100 billion in assets under management on its platform, and includes De Volksbank, Nationale-Nederlanden, and BNP Paribas Personal Finance among its customers. Matthijs Aler is Ohpen’s CEO.

The Finovate Awards are back, which means nominations for 2026 are officially open! Each year, the Finovate Awards recognize the companies, financial institutions, and individuals pushing the boundaries of financial services. The program highlights the newest tools, solutions, and ideas shaping how money moves, grows, and is managed.

Today, we’re unveiling the full list of 31 award categories for 2026, including several new additions.

Whether you’re building, partnering, or leading in fintech, there’s a category designed to recognize your impact. Check out the full list below:

Awards for Banks and Financial Institutions

These categories spotlight banks and financial institutions delivering standout innovation and customer value:

Best Anti-Fraud/AML Solution

Best Banking as a Service Provider

Best Consumer Lending Solution

Best Customer Experience Solution

Best Digital Bank

Best Financial Mobile App

Best Marketing/Customer Acquisition Solution

Best Wealth Management Solution

Excellence in Open Banking/Open Finance

Top Fintech VC

Why it matters: In today’s era of increasing competition and elevated customer expectations, banks must now compete on experience, infrastructure, and ecosystem participation. These categories recognize institutions that are evolving beyond traditional models to meet modern expectations.

Awards for Banks, FIs, and Fintechs

These categories highlight collaboration, infrastructure, and breakthrough innovation across the ecosystem:

Best Consumer-Facing Payments Solution

Best Corporate Payments Solution

Best Cryptocurrency Application for FIs

Best Enterprise Payments Solution

Best Fintech Partnership

Best Generative AI Solution

Best ID Management/KYC Solution

Best Insurtech Solution

Best RegTech Solution

Best SMB/SME Banking Solution

Excellence in Financial Inclusion

Excellence in Sustainability

Most Impactful AI-Based Solution

Excellence in Stablecoins, Tokenized Deposits, or Tokenized Assets

Excellence in Risk Management

Why it matters: AI is moving from pilot and into production, tokenization is altering infrastructure, and partnerships are becoming the default path to innovation. These categories show the industry’s shift from standalone tools to a more connected financial ecosystem.

Awards for Fintechs and Technology Firms

These categories focus on the builders powering the next generation of financial services:

Best Alternative Investments Solution

Best Back-Office/Core Services Solution

Best Embedded Finance Solution

Top Emerging Fintech Company

Why it matters: The most important fintech innovations today are often invisible to the end user because they are embedded into workflows, infrastructure, and platforms. These awards recognize the companies building the infrastructure behind modern finance.

Awards for Individuals

These categories celebrate the people driving the industry forward:

Executive of the Year

Innovator of the Year

Why it matters: Behind every breakthrough product or platform is leadership and vision. These awards recognize the individuals shaping the direction of fintech.

Submit Your Nomination

If you’re building, scaling, or leading in fintech, now is the time to put your work forward. Submit your nomination today and save when you apply before the early-bird deadline of April 24, 2026.

The Finovate Awards are designed to spotlight what’s new and what’s working. And in 2026, when the industry is moving from experimentation to execution using a range of new technologies, we’re excited to help differentiate between the solutions that show promise and the ones delivering real, measurable impact.

Welcome to Q2! We’re looking forward to first-looks at how fintechs are faring in 2026, especially with regard to investment trends. For now, we’re seeing new C-suite leadership in digital banking, partnerships in insurtech, and a new fintech that is leveraging stablecoins for cross-border payments. Be sure to check back here at Finovate’s Fintech Rundown in the days to come for the latest fintech news headlines.

Derivative Pathdelivers FX payments solution powered by Wells Fargo’s FX Payment Solutions and connected through Jack Henry’s Treasury Management platform.

ASN Bank chooses core banking platform provider Ohpen as its new strategic technology partner to enhance its mortgage operations.

Fraud prevention

Marqetaenhances its Real-Time Decisioning (RTD) offering with an AI-powered risk score that analyzes transaction risk levels.

Finovate Best of Show winner 1Kosmosannounces that its platform has secured Department of War (DoW) Impact Level 4 (IL4) authorization.

iDenfy and 5 Star Jets team up to integrate identity verification and AML screening into the aviation company’s payment verification process for both fiat and cryptocurrencies.

SoFi is entering commercial banking with a 24/7 model that combines fiat accounts, crypto rails, and its own tokenized deposit, SoFiUSD, to enable real-time money movement.

The company is taking a “stablecoin sandwich” approach, converting fiat to SoFiUSD and back again to enable instant settlement while keeping deposits on its balance sheet.

SoFi is positioning itself between banks and fintechs, aiming to deliver the speed of crypto-native players and the trust of a regulated bank in a single platform.

Lending and wealth management fintech SoFi is joining the commercial banking world with the launch of SoFi Big Business Banking, its new set of enterprise banking tools. The new offering comes with both fiat and crypto-native infrastructure that allows for 24/7 money movement.

The launch comes as part of SoFi’s new focus on integrating into the blockchain. Most recently, the company launched its own tokenized deposit, SoFiUSD, to settle its crypto trading business, offer faster settlement around the clock, power international remittances, and more.

“To be competitive businesses today must operate in a global, always-on environment 24 hours a day, 7 days a week, while legacy banks typically still operate 9 to 5, Monday to Friday,” said SoFi CEO Anthony Noto. “SoFi Big Business Banking is changing that by combining the strength and regulatory foundation of a nationally chartered bank with the speed, scale, and flexibility companies need to move and manage money or digital assets in real time.”

SoFi’s new business offering will help companies make payments, access funds, and operate in real time with a fully chartered bank. At launch, SoFi’s Big Business Banking comes with deposit accounts, fiat, crypto, and SoFiUSD payments. By leveraging digital currencies, SoFi is enabling businesses to transact outside of traditional banking hours. The company is taking the “stablecoin sandwich” approach, allowing businesses to convert from fiat to SoFiUSD, then back to fiat, enabling real-time settlement without relying on external rails, while ensuring deposits remain on SoFi’s balance sheet.

By combining fiat accounts, payments, and digital asset infrastructure into a single regulated platform, SoFi is positioning itself as the bank for a world where money moves 24/7 and across formats. While fintechs like Ramp are building the operating systems for how companies spend money, SoFi is making a play to own where that money lives—and increasingly, how it moves between traditional and on-chain systems.

SoFi’s Big Business Banking is already live. Initial clients include Cumberland, Bullish, BitGo, B2C2, Fireblocks, Wintermute, Galaxy, Jupiter, Mesh Payments, and Mastercard.

Competition in the business banking space has been steadily rising for the past six years, and the use of blockchain rails is intensifying the pressure. Banks are piloting tokenized deposits and blockchain-based settlement, while payments firms like Stripe and Checkout.com are adding stablecoin capabilities to support faster global commerce. Crypto-native players, such as Circle and Coinbase, continue to offer 24/7 settlement outside the banking system entirely. SoFi is attempting to bring these models into a single offering that delivers the speed of stablecoins with the trust of a regulated bank. And because it has its own stablecoin, it doesn’t rely on external infrastructure.

As the push into AI continues, many banks are still struggling to modernize their digital foundations without simply recreating their existing platforms. For institutions operating across multiple markets, that challenge becomes even more complex, as firms need to balance local autonomy with the need for standardization, speed, and scalability.

In a recent conversation with Vanja Tokic of Raiffeisen Bank International, Tokic explained that the real work of transformation is happening in how banks rethink processes, align teams, and prepare their data and systems for what comes next. He also talked about what it takes to actually get started.

“There is still a lot of overhype on the GenAI topic. Banks and people in general are underestimating what it takes to put those things into real processes, into real production… It looks really simple when you start prompting, but when you actually have to do it in a regulated environment, then it’s really difficult to get it done.”

Tokic serves as Head of Digital Channels and Conversational AI and previously led retail digital transformation strategy at Raiffeisen Bank International. With more than two decades of experience in digital banking, he focuses on translating high-level strategy into execution by aligning teams across markets, driving adoption of reusable platforms, and building what he describes as a “digital bank with a human touch.”

Raiffeisen Bank International is an Austria-based banking group that operates across Central and Eastern Europe, serving millions of customers through a network of subsidiary banks. The organization functions as both a central institution for the Raiffeisen Banking Group and a holding company for its international operations, offering retail and corporate banking services across the region.

For financial institutions, growth involves deepening relationships with existing customers. At a time when switching financial institutions comes at a low cost and fintechs offer many of the same benefits as traditional banks, customer engagement and financial wellness have become strategic priorities.

For traditional financial institutions whose offerings can seem static, providing personalized experiences that help customers save smarter, build better financial habits, and feel more in control of their financial lives can help retain and win over clients. The banks that succeed will be those that can embed themselves into customers’ day-to-day financial decisions.

At FinovateSpring 2026, five companies are focused on helping banks do exactly that. From savings and financial wellness tools to engagement platforms and next-generation consumer experiences, these solutions are designed to drive loyalty, increase product adoption, and deliver measurable value to both customers and institutions.

Business HYS by Plinqit helps banks compete for deposits while giving small and medium-sized businesses (SMBs) more effective ways to manage their cash. The platform is designed to drive deposit growth by offering high-yield savings experiences tailored to business customers, an area where many traditional banks have struggled to differentiate.

Headquartered in Ann Arbor, Michigan and founded in 2015, Plinqit enables financial institutions to attract and retain SMB deposits without overhauling their existing infrastructure which ultimately helps level the playing field to compete against larger competitors and digital-first challengers.

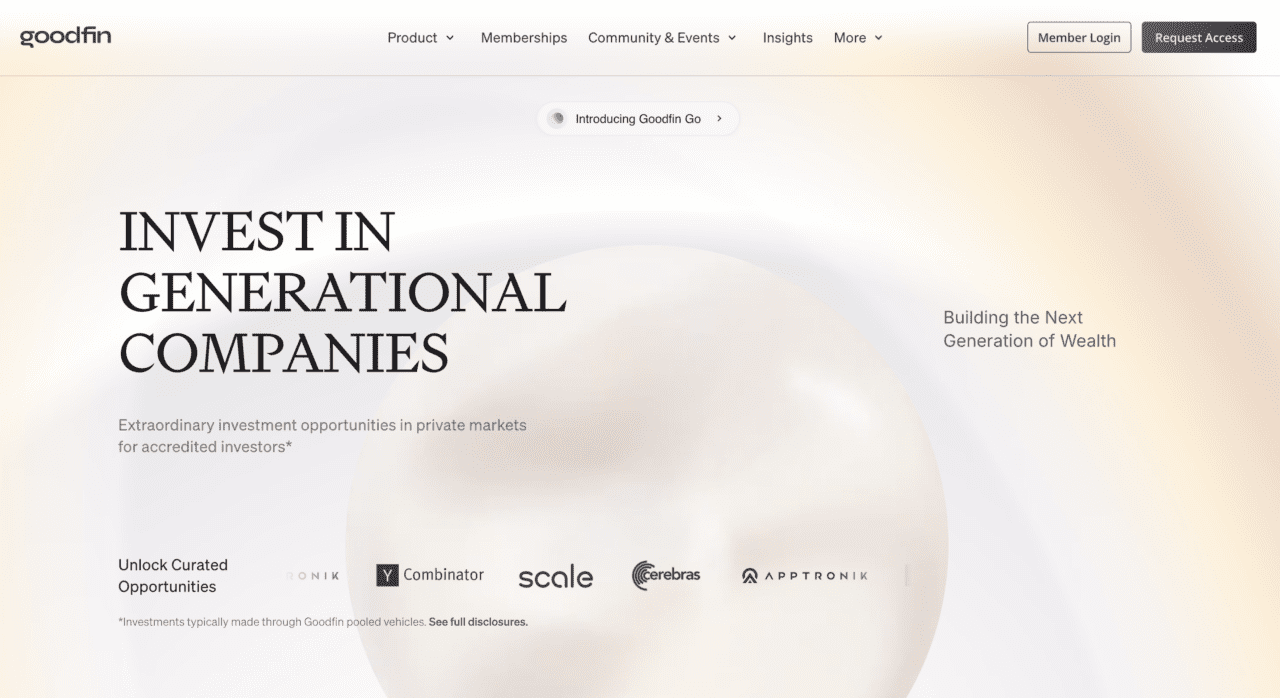

Goodfin is expanding access to alternative investments by opening institutional-grade opportunities to a broader range of investors. Its platform is designed to help financial institutions and fintechs offer differentiated wealth-building tools such as private equity, venture capital, and pre-IPO deals that go beyond traditional stocks and bonds.

Founded in 2022 and headquartered in San Francisco, Goodfin enables banks to meet growing customer demand for access to alternative assets, while positioning themselves as gateways to more sophisticated investment opportunities.

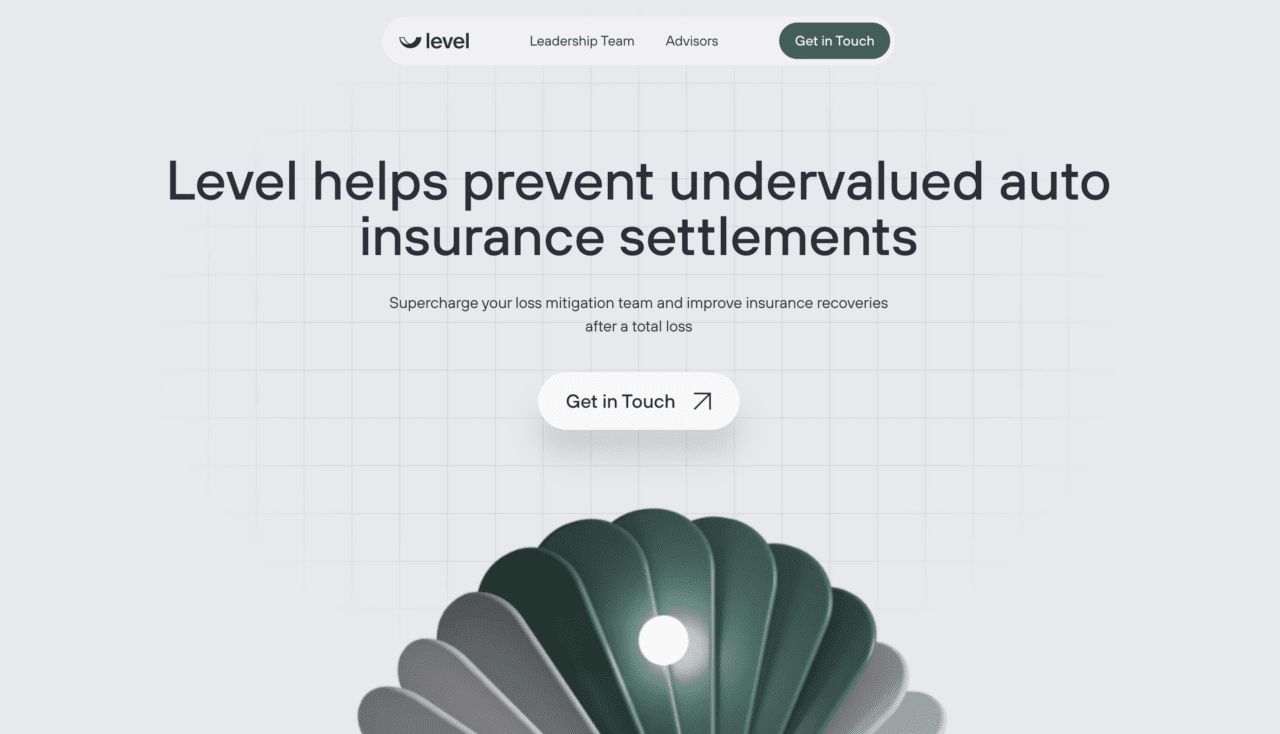

Level helps auto lenders reduce losses by identifying and recovering missed value in total loss insurance claims. Its AI-powered claims management platform centralizes workflows into a single portal, enabling lenders to detect undervalued claims and dispute them at scale.

Backed by licensed claims experts, Level combines automation with human oversight to increase recoveries, reduce deficiency balances, and accelerate time to payment. Headquartered in New York and founded in 2023, the company offers banks, credit unions, and lenders a way to improve operational efficiency while directly impacting the bottom line.

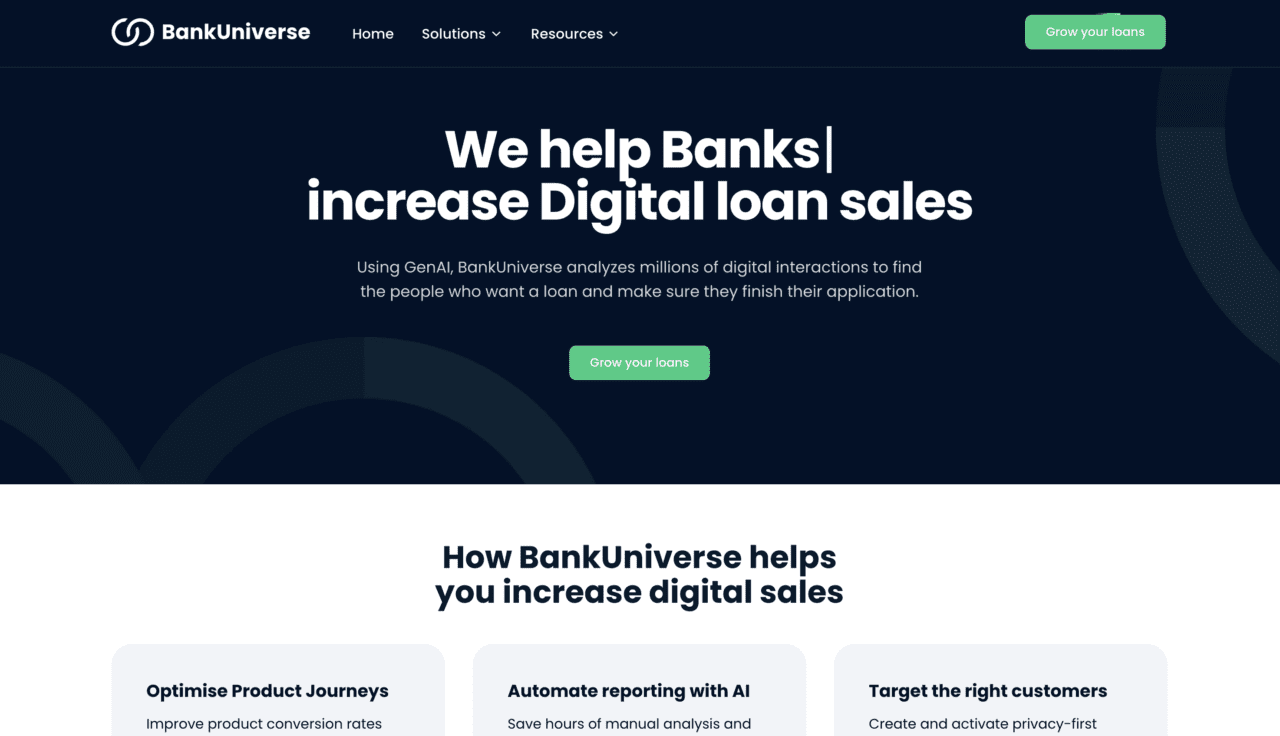

BankUniverse delivers a privacy-first intent engine that helps financial institutions identify and convert high-value prospects without relying on sensitive personal data. By analyzing user intent signals rather than personal identifiers, the platform enables banks to drive digital sales while maintaining strong data privacy standards.

Founded in 2024 and headquartered in Greece, BankUniverse helps institutions increase conversion rates while navigating growing regulatory and consumer expectations around data protection.

Bluum Finance provides a unified platform for embedded investing, combining brokerage, custody, and reporting into a single API. Its infrastructure allows financial institutions and fintechs to launch fully compliant investment offerings quickly, without the complexity and cost typically associated with building these capabilities in-house.

Founded in 2025 and headquartered in Los Angeles, Bluum enhances its offering with AI-powered advisory tools that deliver personalized investment experiences. The platform is built for a wide range of providers looking to bring investing into their existing customer journeys.

Why banks should care

Financial wellness and engagement are quickly becoming primary drivers of growth instead of nice-to-have features. Banks are under pressure to increase deposits, deepen relationships, and create new revenue streams while competing with fintechs that are often more agile and user-focused. Platforms that help customers save more effectively, access new investment opportunities, or receive more personalized financial guidance can translate directly into higher balances, stronger loyalty, and increased product usage.

At the same time, these tools enable banks to expand their role in customers’ financial lives without significantly increasing operational complexity. Whether it’s embedding investing capabilities, improving digital acquisition, or unlocking overlooked sources of value in existing portfolios, financial wellness platforms offer a practical way for institutions to drive both customer outcomes and business performance.

Qover, a Belgian fintech that specializes in “Insurance-as-a-Service,” has raised $12 million in a capital extension from CIBC Innovation Banking. The company, which made its Finovate debut at FinovateEurope 2018, reported that its total funding now tops $100 million.

The investment comes as the embedded insurance orchestration firm marks its 10th anniversary of serving customers throughout Europe. At a time when the international embedded insurance market is expected to grow from $176 billion in 2026 to more than $1.46 trillion by 2034, Qover currently protects 15 million customers via its insurtech platform and expects to reach 55 million users by the end of this year.

“We started with a simple conviction: insurance could be simpler and truly accessible across borders,” Qover CEO and Co-Founder Quentin Colmant said. “Ten years and 15 million users later, that conviction has become a platform, and with AI now accelerating what’s possible, we are more ambitious than ever. Our goal is to protect 100 million people by 2030, building the infrastructure that makes a global safety net real.”

Qover said that the funding from CIBC will support the company’s continued investment in its orchestration platform, AI capabilities, and operational infrastructure.

Qover’s API-first platform orchestrates embedded insurance for businesses and insurers across Europe. Adaptable to any product, partner, country, or risk carrier, Qover’s platform gives institutions greater control with less complexity, covering the full insurance lifecycle, from design to claims. Organizations using the platform benefit from a configurable setup that enables them to tailor the solution to their needs, as well as a modular approach that allows users to select from different platform modules and how they are implemented.

“The next decade of insurance will be defined by the companies that can operate at scale without sacrificing precision,” Qover General Counsel Caroline Hanotiau said. “AI gives us the opportunity to make compliance by design the standard, not the exception, allowing us to expand into more products and more regions with the confidence that we are always operating at the highest level. That’s how Qover will grow responsibly and at the scale our vision demands.”

Founded in 2016, Qover made its Finovate debut at FinovateEurope 2018. Today, the company protects 15 million people in more than 32 countries and boasts revenue growth of 3x and more than $173 million in gross written premiums over the past four years. Qover has orchestrated embedded insurance programs for a number of major international brands including fellow Finovate alums Revolut and Mastercard; as well as Monzo, bunq, and BMW.

Qover’s fundraising news comes just a few days after the company announced that it had forged a strategic partnership with Willis, a WTW business. Together, the two companies will offer a product-agnostic solution that helps companies launch tailored insurance programs quickly and at scale.

What do banking consumers need most from their banks in 2026? How do these and other financial institutions translate major trends into actionable initiatives that solve problems for individuals, families, businesses, and communities? What role do partnerships between banks and fintech companies play in helping bring cutting-edge financial products and services to market?

We caught up with Meghan Kober, Senior Vice President and Head of Fintech Partnerships & Strategic Investments at U.S. Bank, to answer these and other questions confronting banks and their customers today. In her role at U.S. Bank, Kober leads a cross-functional team that scales innovation portfolios and drives enterprise value through strategic partnerships. Her expertise is in translating emerging drivers and market signals into applied strategies.

This interview is part of Finovate’s annual Women’s History Month commemoration. Previous installments include our salute to the women of FinovateEurope 2026 and our preview of the female founders and leaders who will represent their companies at FinovateSpring 2026, May 5-7.

U.S. Bank has long been active in innovation, but your role sits at a unique intersection. How does the Fintech Acceleration team build on that legacy today?

Meghan Kober: There’s a moment I often come back to early in my career, sitting inside a broker-dealer, trying to connect systems that were never designed to speak to each other. That experience shaped how I think about innovation today.

We’ve entered the Great Convergence. Innovation is no longer built inside a single institution. It is shaped across startups, venture firms, accelerators, and universities.

The challenge is not access to innovation. It is translation and direction. Signals are abundant, but without structure, they don’t convert into outcomes.

That is the role of the Fintech Acceleration team. Since 2020, we have built on U.S. Bank’s innovation foundation to act as a system layer across the enterprise. We translate external signals into enterprise execution across product, risk, and partnerships.

My broader thesis is that we are moving from an innovation economy to a participation economy. The institutions that win will not be the ones that invent the most, but the ones that enable the most people, businesses, and partners to participate in the system. Our role is to help design for those outcomes.

That idea of translation and direction is powerful. How do you take something as abstract as future trends and turn them into clear action inside a large, regulated organization?

Kober: We are operating in a period of convergence. AI, digital assets, and embedded finance are not evolving independently. They are compounding. That creates multiple futures unfolding at once.

The risk for large organizations is reacting too late or moving without alignment. In financial services, you cannot separate innovation from risk, legal, and compliance. Execution requires coordination from the start.

This is where applied foresight comes in. For us, it is not about predicting the future. It is about choosing which future to build toward.

We integrate signals from across venture, academia, and global markets. Through my work nationally in regions such as Utah and Minnesota, as well as globally with the University of St. Thomas and studying ecosystems in places like Tokyo and Seoul, we are looking at how infrastructure, capital, and policy shape participation at a systems level.

We then anchor those insights to a business problem and align with business line leaders.

Leadership, in this context, is about creating clarity. It is about giving teams direction so they can build with confidence. Foresight without execution is noise. Applied foresight is what turns signal into strategy.

When that clarity is in place, where do you see it driving the most meaningful outcomes today?

Kober: If you look at the U.S. economy, small businesses represent approximately 43.5 percent of GDP and nearly half of employment. They are one of the most important economic engines we have.

At the same time, many small businesses are still operating across fragmented systems, spending time managing tools instead of growing their business.

If we are serious about economic resilience, we have to reduce that friction.

In partnership with Shruti Patel, Chief Product Officer for Business Banking, and Business Banking leaders, we focused on how to embed financial services directly into small business workflows. That led to solutions like Business Essentials, partnerships with fintechs like Gusto, and capabilities like U.S. Bank Bill Pay for Business.

What is important here is not just the product. It is the system design. We are moving from standalone banking products to integrated operating systems for businesses.

The outcome is simple but powerful. Business owners get time back. They have better visibility. They can make better decisions. At scale, that drives job creation, stronger local economies, and a more resilient financial system.

That is what participation looks like in practice.

That kind of impact clearly depends on strong partnerships. What differentiates the way you approach fintech partnerships today?

Kober: The market has matured. We are no longer in a phase where experimentation alone is enough. Partnerships need to deliver outcomes and scale.

What differentiates successful partnerships is alignment and readiness. We start with a clearly defined business problem and align on shared outcomes from the beginning.

We typically partner with founders who have achieved product market fit, understand regulated environments, and are often backed by venture capital firms.

But what is often overlooked is that partnerships are not just about capability. They are about system effects.

When we partner with a startup, we accelerate our speed to market. We solve real problems for our clients. At the same time, we support that company’s growth, which drives job creation, attracts capital, and strengthens the ecosystem.

It creates a flywheel.

My role is not just to participate in that ecosystem, but to help shape how it connects. Where capital flows, where partnerships form, and where innovation translates into real economic outcomes.

You’ve mentioned participation a few times now. I’d love to connect that back to your own journey. How has your path shaped this perspective?

Kober: My path into fintech was not traditional, but in many ways that is what gave me this perspective.

I started by trying to understand systems: connecting data, teaching myself to code, and building dashboards to make better decisions. That curiosity led me into Minnesota’s innovation ecosystem, where I was inspired by leaders like Susan Langer, CEO of Spave, at Twin Cities Startup Week and became involved with the Minnesota Fintech Collective.

I had the opportunity to join and help build the Fintech Acceleration team alongside some great leaders, and over time, help scale that into a broader platform across the enterprise.

What I learned through that experience is that innovation is not a technology problem. It is a participation problem.

Who has access to networks. Who gets exposure to opportunities. Who is able to build, invest, and contribute.

Leadership is about expanding those surfaces. Creating more entry points into the system so more people can participate and shape it.

Looking ahead, how are technologies like AI and digital assets influencing how you think about the future of financial systems?

Kober: We are at an inflection point where financial infrastructure itself is being redefined.

AI is changing how decisions are made. Digital assets are changing how value moves. Together, they are enabling more programmable, intelligent systems.

But the real question is not what the technology can do. It is how we design systems around it.

At U.S. Bank, we are applying AI across operations and exploring digital asset capabilities, including stablecoin infrastructure on networks like Stellar. These efforts are grounded in real use cases and informed by collaboration across fintech partners, venture ecosystems, and global research.

The opportunity is significant, but so is the responsibility. These systems must be built with trust, resilience, and inclusion at their core.

If we get that right, we are not just improving financial services. We are redesigning how participation in the economy works.

Finally, during Women’s History Month, how do you define leadership in this moment, especially within fintech and financial services?

Kober: The strength of our financial system is directly tied to how many people can participate in it.

Throughout my career, I am grateful to have benefited from mentors, founders, investors, and institutions that created opportunities for me to step in, learn, and build. These ecosystems matter, spanning from accelerators and venture capital to universities and corporate leadership.

Leadership, to me, is about doing that intentionally and at scale.

It is about bringing applied foresight and direction to teams so they can build systems that drive resiliency and prosperity. It is about expanding who gets to participate in shaping the future.

Because ultimately, the next era of financial services will not be defined by who innovates the fastest.

It will be defined by who builds systems that work for the most people.

Once again, Finovate celebrates fintech’s best and brightest with the 2026 Finovate Awards!

Every year, the Finovate Awards showcase the banks, credit unions, financial service providers, and fintechs that are driving innovation in our industry. With award categories recognizing achievement in consumer lending, digital banking, fintech partnerships, and more, the 2026 Finovate Awards will crown winners in more than 30 different categories!

Now in its eighth year, the Finovate Awards recognize both individuals and organizations who are creating meaningful advances in financial technology. From making payments faster, safer, and easier, to helping small businesses secure the financing they need to grow, to promoting greater financial inclusion and wellness, Finovate Award winners are leaders in their respective fields, setting the pace for innovation in financial services today.

Why apply?

Showcase your innovation! Highlight your innovations to the broader banking and fintech community.

Gain recognition from industry experts! Boost confidence with customers, partners, and investors as an acknowledged industry leader.

Position yourself as a pioneer! Establish your firm as a key driver of innovation in financial services.

Submit your nomination today! Entry criteria and instructions are available at our Finovate Awards hub. Winners will be announced during FinovateFall 2026 in September.

Don’t delay! The Finovate Awards nomination window will run through May 22. Submit your nomination before April 24 and save $100.

FinovateSpring 2026 comes to sunny San Diego, California, from May 5 to 7. Tickets are on sale and going fast. Save your spot, book your room, and get ready for a full-court press on many of the biggest issues in fintech today: from AI and embedded finance to stablecoins and hyperpersonalization in the customer experience.

Today we highlight eight top fintech trends that will dominate the conversation at FinovateSpring this year—from main stage plenary keynotes to executive briefings and special spotlight sessions. We’re also showcasing where on the agenda you can find presentations and panel discussions on each theme.

It’s All About Agentic AI

AI is undeniably the most compelling and in-demand technology in banking and financial services today—and the innovation in AI that is attracting the most attention is agentic AI. Agentic AI systems are designed with a degree of autonomy and decision-making ability that allows them to complete an expanding range of tasks independently without requiring human intervention. In a relatively short time, this technology has evolved from pilot projects to powering e-commerce, fraud prevention, automated investment, credit risk assessment, and more.

Getting Serious about Stablecoins in Financial Services

With growing use cases in financial services and increasing regulatory clarity, stablecoins have become the most constructive innovation to emerge from the DeFi movement. From cross-border payments and remittances to serving as a stable medium of exchange, store of value, and hedge against volatility for cryptocurrency users, stablecoins enable banks and other financial institutions to leverage blockchain innovation while benefitting from price stability.

While much of the conversation about embedded finance focuses on how it empowers non-financial entities to offer financial services, it is also true that embedded finance offers banks and other financial services providers a way to scale and diversify their offerings while reaching new markets, customers, and members.

A Heat Check on the Open Banking Opportunity in the US

Open banking and finance are thriving in many places around the world, and while there have been gains in the US, it still lags behind peers in Europe and Australia. The absence of a regulatory mandate makes open banking in the US largely a market-driven phenomenon, but the continued debate over Section 1033 of the Dodd-Frank Act (which ensures consumers can access their financial data upon request) creates uncertainties and challenges for banks and fintechs regarding data sharing and the extent of customer control over their data.

Fighting Financial Crime: New Challenges, New Solutions

Using AI to stay ahead of AI-wielding fraudsters and financial criminals has been a key strategy for fintechs and financial institutions aiming to protect themselves and their customers. At the same time, a growing number of companies are recognizing that, beyond technological solutions, collaborating to fight common fraud threats offers significant benefits compared to firms relying solely on their own resources.

Financial crime and cybersecurity sessions at FinovateSpring

Leveraging Data, Analytics, and AI to Enhance the Customer Experience

With more data than ever before at their disposal and powerful new analytical capabilities—including AI—at hand, financial institutions are looking at ways to better serve their customers and members with increasingly personalized products and services. In many ways, the ability to meet customers where they are—at home, on the go, or in the middle of a transaction—is increasingly seen as an opportunity for financial institutions to differentiate their offerings, as well as learn from and compete more effectively against non-financial rivals.

Third-Party Risk and Building Better Partnerships in the Post-SVB Era

How are banks and fintechs addressing partnership and third-party risk in the post-SVB era? As regulators sharpen their focus on the risks in bank-fintech partnerships—and a growing number of fintechs decide to “cut out the middleman” and become banks themselves—it remains critical that banks and fintechs understand what it takes to build constructive alliances and collaborations that benefit all stakeholders—including regulatory bodies.

Third-party risk/Bank-fintech partnership sessions at FinovateSpring

Customers Still Count on Credit Unions and Community Banks

Large national banks may have the lion’s share of customer money, but with 73% of Americans having favorable views of credit unions compared to 56% of Americans having favorable views of national banks, it is hard not to see an opportunity for smaller financial institutions to leverage that trust into bigger customer bases, memberships, and deposits. Credit unions and community banks that embrace modernization and fintech innovation will be best positioned to offer the kind of services and products that often attract customers to national brands.

Community banks and credit union sessions at FinovateSpring

The first quarter of 2026 comes to a close tomorrow. And amid the rush of end-of-month, end-of-quarter news, don’t forget that April Fool’s Day, April 1st, is right in the middle of the week.

Every year there are a handful of fintechs that like to take advantage of the occasion by having a little fun with the press, so it’s always a good idea of have a bit of extra skepticism if you come across a headline that seems a little sensational over the next few days. Here on the Fintech Rundown, we promise to do our level best to keep you fool-free!

Digital banking

Metro Credit Union to deployTyfone’snFinia Digital Banking Platform.

Corgi Insuranceacquires Corgi.com domain en route to building its fully-integrated, AI-powered insurance carrier.

Digital communications

AI-powered digital communications governance and archiving technology partner Shieldunveils new enhancements to its Shield Archive solution.

Lending

Worth, a fintech platform that helps financial institutions onboard and undewrite small and medium-sized businesses, raises $30 million in Series A funding.