This week’s edition of Finovate Global highlights recent fintech announcements from the countries of the Caribbean.

Belize Bank Inks Digital Modernization Partnership with Backbase

The biggest bank in Belize is also among the first financial institution in the Caribbean to embrace a full retail and business digital banking stack in addition to AI-powered lending and onboarding. Belize Bank Limited announced this week that it has partnered with Backbase in a major, six-year partnership to implement the company’s AI-native banking OS.

The financial institution, with more than $1 billion in total assets and the nation’s largest branch network, had sought a platform that would scale with its growing operations and provide consistently high-quality digital experiences across its customer base. Deploying Backbase’s AI-native Banking OS for both retail and business banking will enable Belize Bank to replace fragmented workflows with self-service, accelerated digital onboarding, and unified cash-flow visibility for business customers. Importantly, Backbase’s Banking OS sits above Belize Bank’s existing banking core, leveraging Backbase’s Connectivity Layer (Grand Central) to provide seamless integration with the bank’s existing systems.

“Belize Bank is exactly the kind of institution Backbase was built for—a market leader that takes its responsibility to customers seriously and wants technology that matches that ambition,” Backbase CEO Jouk Pleiter said. “Embarking on this comprehensive modernization across retail, SME and digital lending is a true reflection of the strategic discipline of the team at Belize Bank. We are proud to partner with them to architect the financial backbone of Belize’s future economy.”

Belize Bank Limited is both the country’s oldest and largest financial institution. The full-service commercial bank holds approximately 43% of the nation’s total banking assets and serves 100,000 retail and business banking clients. Headquartered in Belize City, Belize Bank was founded in 1987.

“Our strategic partnership with Backbase represents a transformative step toward delivering a new era of banking—one that is seamless, intelligent, personalized, and built around the evolving needs of our customers,” Belize Bank Limited Executive Chairman Filippo Alario said. “By combining Backbase’s innovation with Belize Bank’s commitment to excellence and customer-first vision, we are laying the foundation for a future where digital banking goes beyond transactions—creating more meaningful connections, empowering our customers, and transforming the way Belizeans experience banking.”

Four-time Finovate Best of Show winner Backbase was founded in 2003 and is headquartered in Amsterdam. The company’s AI-native Banking OS transforms fragmented banking operations and workflows into a unified frontline in which customers, employees, and AI agents work as one across digital channels, front-office, and operations. More than 120 leading banks around the world use Backbase’s technology solutions across verticals ranging from retail, small business, commercial, and private banking to wealth management.

Creditinfo Group Acquires EveryData Group to Boost Caribbean Presence

UK-based Creditinfo Group has completed its acquisition of EveryData Group, a data, analytics, and software company operating in the Caribbean. The acquisition is the culmination of a long-term partnership between the two firms, and will enable Creditinfo Group to bring advanced technology and new data solutions to financial institutions and consumers throughout the region. The greater technology integration and shared infrastructure across Creditinfo Group’s global network will also benefit customers of both firms.

“This acquisition reinforces our commitment to helping build stronger financial ecosystems around the world,” Satty Saha, Group CEO at Creditinfo Group, said. “EveryData has built an impressive business with a strong reputation across the Caribbean, and together we are well positioned to bring greater innovation and value to customers throughout the region. By combining our global expertise with EveryData’s deep local knowledge, we can accelerate the delivery of new products and technologies that improve access to finance and support economic growth.”

The transaction fortifies Creditinfo Group’s international presence, specifically in the Caribbean, adding primary credit bureau operations across Jamaica, Barbados, Guyana, and the Eastern Caribbean Currency Union (ECCU) of St. Lucia, Antigua and Barbuda, St. Kitts and Nevis, the Commonwealth of Dominica, Grenada, St. Vincent and the Grenadines, Anguilla, and Montserrat. The company noted that it will continue investing in technology, talent, and innovation throughout the region, helping leaders and professionals in financial institutions make better decisions while promoting financial inclusion and sustainable economic development.

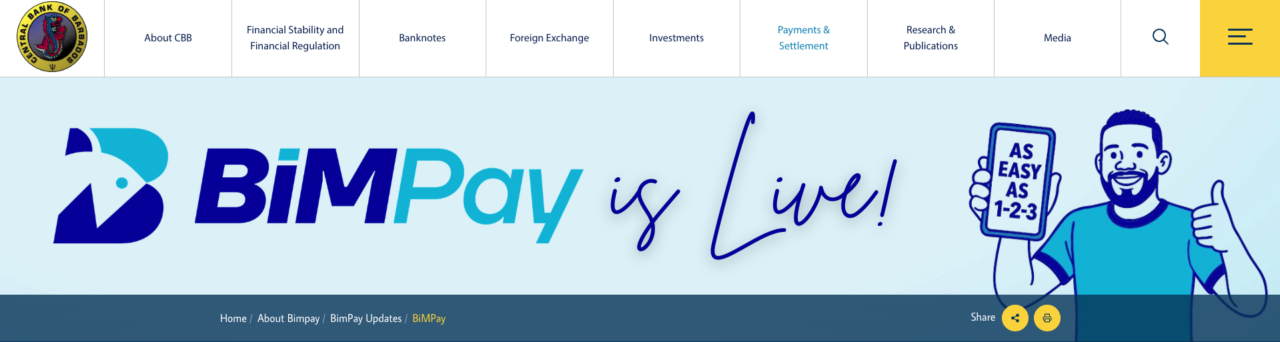

Barbados Launches Instant Payment System BiMPay

Launched by the Central Bank of Barbados, a new instant payment scheme BiMPay is now available to individuals and businesses in the country. The new system operates 24/7, on weekends and public holidays, enabling users to send and receive money in seconds. BiMPay, according to officials, will help modernize the country’s financial system by making payments faster, more efficient, and more convenient. The first transaction on BiMPay was conducted by Barbados Prime Minister Mia Amor Mottley, who sent money to a local vendor.

“A modern economy needs a modern payment system,” Central Bank Governor Kevin Greenidge said. “People need to be able to send money quickly. Businesses need to be able to receive funds and have them available to spend. Vendors want to get their funds and access their money immediately. We need a space to innovate, to compete, and to build the fintech industry that needs to be built.”

The launch of BiMPay comes after months of testing with financial institutions and other stakeholders. Currently, six commercial banks and the country’s three largest credit unions are connected to the BiMPay system. Seven institutions are also linked to the BiMPay e-wallet, which enables users to make payments, request funds, and complete transactions using phone numbers, email addresses, or QR codes.

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

- Israel-based payments and loyalty platform Nayax teamed up with mark-to-market credit and structured finance infrastructure company Zaria Systems.

- One Zero, a digital bank based in Egypt, announced a new initiative to allow customers to use the AI agent of choice to receive financial information.

- PayPal and stc pay Bahrain launched a cross border transfer service.

Central and Southern Asia

- Indian fintech Cred has raised $900 million in Series H funding from Meta.

- Pakistan-based fintech group Abhi announced plans to launch an IPO of its microfinance bank.

- HonestAI inked a Memorandum of Understanding with Mongolian financial IT company Nubisoft.

Latin America and the Caribbean

- Creditinfo Group aquired EveryData Group to boost its presence throughout the Caribbean

- Grupo Cibest acquired 100% of Colombian fintech Avista Colombia.

- Belize Bank announced a new six-year partnership with Backbase to modernize its digital banking operations.

Asia-Pacific

- Malaysian fintech and digital bank Boost launched its agentic AI banking platform.

- South Korean fintech KSNet signed a memorandum of understanding with the Solana Foundation to jointly build next-generation digital asset payment infrastructure.

- VNExpress looked at the evolution of Vietnam’s digital asset industry.

Sub-Saharan Africa

- Pan-African payments firm Moment secured $22 million in Series A funding.

- Africa-based fintech PalmPay has begun preparations for a Hong Kong IPO.

- Yellow Card, a stablecoin infrastructure company founded in Nigeria and currently based in Atlanta, Georgia, raised $40 million.

Central and Eastern Europe

- Lithuanian regtech solution provider iDenfy has added Czech Bank iD to its verification platform.

- Wealth management platform FNZ announced plans to sell its German FNZ Bank business to Advent.

- Cryptocurrency platform Bybit obtained an Electronic Money Institution (EMI) license in Austria.

Photo by Jamie Tudor on Unsplash