This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Onfido to provide identity verification for blockchain identity and payment solution provider Civic.

Ping Identity successfully completes financial grade API (FAPI) conformance testing.

EdgeVerve SystemsunveilsAssistEdge RPA 18.0 to help organizations reach broader automation coverage of their processes.

iSignthisinks Australian Principal Member licensing agreement with Visa.

Business Insider highlightsFlywire CEO’s unique way of attracting investment.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Kantox’sDynamic Hedging solution is the latest FX risk management option for U.K.-based corporate clients of Silicon Valley Bank. The deal with SVB, announced this week, is Kantox’s first bank partnership.

“By offering our Dynamic Hedging software to their corporate clients,” Kantox co-founder and CEO Philippe Gelis said, “we are providing a sophisticated solution which makes the treasurer’s job easier, while providing added value to SVB’s existing FX services.”

Kantox’s Dynamic Hedging technology makes treasury operations more efficient by automating FX risk management. The solution automatically hedges transactions in real-time to mitigate risk and improve competitiveness. Treasurers also gain greater visibility into FX exposure.

Kantox and SVB are no strangers. Silicon Valley Bank was behind the $5.6 million (€5 million) venture debt financing Kantox picked up in April. This marked the second such arrangement between the two parties, having previously inked a financing agreement in December 2017.

Calling Kantox “a technology partner that understands the innovation economy and the sectors in which they operate,” Erin Platts, Head of EMEA and President of SVB’s U.K. branch, explained the importance of efficiently managing FX operations for many of the bank’s corporate clients. “Through this partnership with Kantox, we aim to create genuine value for our clients by bringing automation and efficiency to their transactional FX management activities.”

Founded in 1983, Silicon Valley Bank provides financial services and expertise to companies in innovation centers around the world. More than 30,000 startups have benefitted from the bank’s funding.

Kantox’s first bank partnership announcement comes just over a month after CEO Gelis discussed the challenges of fintech/bank partnerships in a candid post at Kantox’s LinkedIn page.

“One of my key lessons learned is that navigating banks is very complex,” he wrote. “There are many people there whose jobs are basically to spend time speaking with fintechs about innovation – and not much else.” His takeaway? Among other insights, Gelis urged fellow fintechs: “Do not look for partnerships, instead engage with banks that are approaching you proactively.”

Kantox demonstrated its Peer FX solution at FinovateEurope 2013. The London, U.K.-based firm, founded in 2011, works with both top tier companies and SMEs to help them save money when exchanging foreign currencies. Kantox estimates that for every $100,000 transaction, it is able to save clients an average of $1,500. Offering spot and forward transactions in more than 20 international currencies, Kantox serves businesses in a wide variety of verticals ranging from e-commerce to travel to digital advertising.

In June, Kantox announced that clients have exchanged more than $10 billion on its platform. Last fall, the company was named to CB Insights Fintech 250 roster of the fastest growing fintech startups in the world. Kantox has raised more than $35 million in funding, and includes Partech and Idinvest Partners among its equity investors.

With such a fast news cycle in fintech, sometimes it’s helpful to dissect the news based on verticals; looking at them each independently. And we’ve done just that. Here’s a quick synopsis of what’s trending among six fintech verticals.

We’ll be taking a closer look at each of these topics at FinovateFall (September 23 through 25 in New York), where the brightest minds in fintech will discuss what you need to know about the latest news during our breakout streams. Register today to save your seat.

Challenger banks got their start during the 2008 financial crisis after consumers lost trust with mega banks and began looking for an alternative. Recently in this space, we’ve started seeing U.K. banks make inroads into the U.S., where there is less competition for non-traditional banking providers. After amassing a waitlist of 100,000 U.S. consumers, German challenger bank N26 launched in the U.S. this July. A few weeks earlier, Monzo also announced a U.S. expansion after amassing a user base of 2.2 million customers in the U.K.

These non-traditional banks are also experiencing a funding boom. Last month alone brought major funding rounds to three challenger banks. U.K.-based Atom raised $60 million at a $644 million valuation, N26 raised an additional $170 million investment at a $3.5 billion valuation, and MoneyLion raised $100 million at a valuation of almost $1 billion. And in June U.K.’s Monzo raised $144 million at a $2.5 billion valuation.

Geographical expansion and strong investor confidence in this space indicate it is ramping up, and we can expect more competing challenger banks to enter the arena soon. The influx of funds also brings the likelihood that, as the startups continue development efforts, new products and features may be on the horizon.

In the past, regtech has been looked at as the ugly cousin within fintech sub sectors. While not as sexy as investing technology, this vertical has seen increased popularity as of late. With the API economy making bank-fintech partnerships the new norm, regulators are begging for oversight and regulation-as-a-service companies have stepped in with the solutions banks need to stay compliant.

Similarly, as enabling technology expands, so does the need for regulation. Fortunately, along with this need comes the advances in technology for the regtech sector itself, which has benefitted from increased automation and scalability as AI and machine learning gain traction and become more accessible for firms.

The final deadline for PSD2 is looming. September 14 is the final deadline by which all EU companies must comply with PSD2’s regulatory technical standards and impose strong customer authentication methods. This has sparked a lot of recent conversation as it has been reported that 41% of EU banks missed the original deadline. And the stakes are high– not only can regulators impose fines, they can also revoke payment providers’ licenses.

Last fall the hot button topic was customer experience. Since then, there have been endless debates on Twitter and the blogosphere on the necessity of bank branches. Some argue that online and mobile channels are the best avenues to serve consumers whereas others contend that physical bank branches are essential to maintain a personal connection with customers. The biggest voice in this debate, however, are the numbers. According to the Financial Brand, 81% of banks and credit unions do not plan to close any branches this year.

It’s hard to talk about the customer experience without bringing up chatbots. The AI-powered technology can be used to scale and humanize the online experience. Not only have we seen an increase in chatbot technology providers, we’ve also been seeing more companies build chatbot capabilities into their own apps.

It’s true that banking and payments is almost too broad to be considered a vertical of its own. And with such a big category, it can be difficult to narrow down current trends. One topic that has been bubbling up lately, however, is the need for real-time payments in the U.S. Just a couple of days ago, the Federal Reserve announced it will develop a real-time payment and settlement service, called FedNow, that will support faster payments in the U.S.

Voice banking technology has been another widely discussed topic among banks, fintechs, and analysts in the past few months. With voice assistants such as the Amazon Echo, Google home, and Apple’s Siri becoming commonplace in homes, consumers are getting used to asking their AI assistants for answers to quick questions. However, the possibility of using the technology to conduct day-to-day banking activity hasn’t been on consumers’ radar– that is, until recently. On July 1, the classic game of Monopoly released a voice banking version that eschews paper currency. Instead, Rich Uncle Pennybags (the Monopoly man) manages the players’ money. When consumers get used to using voice technology in a game, they will soon be looking for it in their real bank.

Wealth management and roboadvisory technologies haven’t changed dramatically since 2015, the height of the roboadvisor boom. However, in the past few months some wealthtech companies have been broadening their offerings to compete with traditional banks. Betterment, Wealthfront, and SoFi, for example, have all launched checking accounts. Many firms have also unveiled additional capabilities, as well, such as tools for trusts, donation features, 529 plan options, and more.

And as AIs get smarter and work harder, there will be a backpedaling of pure roboadvisory plays. Many wealthtech companies already offer a hybrid option that combines roboadvisor tools with advice and guidance from human advisors. The human touch will rise to the top as a must-have option as consumers manage their nest egg.

We’re delighted to announce the finalists for the first ever Finovate Awards! We were amazed by the number of quality entries, and paring the field down to the short list in each category was no easy feat. And of course it doesn’t get any easier for our impressive team of judges, who now have the challenging task of selecting a single winner in each category.

We’ll be announcing the winners at a gala dinner taking place on September 24 (the middle night of FinovateFall) at the Edison Ballroom in Manhattan. In the meantime, please join us in celebrating the individuals and companies who have made it to this stage.

Don’t miss out on the chance see which individuals, companies, and technologies take top honors. Individual seats, half-tables, and full tables are all available for purchase. If you’d like to learn more about how to attend click here for more information or email [email protected] to reserve your table.

InCommpartners with LA Metro to expand locations where customers can purchase and reload TAP cards.

Jack Henry & Associatesnamed one of the best places to work in Alabama by Business Alabama.

Bpm’online CEO and Managing Partner Katherine Kostereva recognized in The Software Report’s Top 50 SaaS CEOs of 2019 feature.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

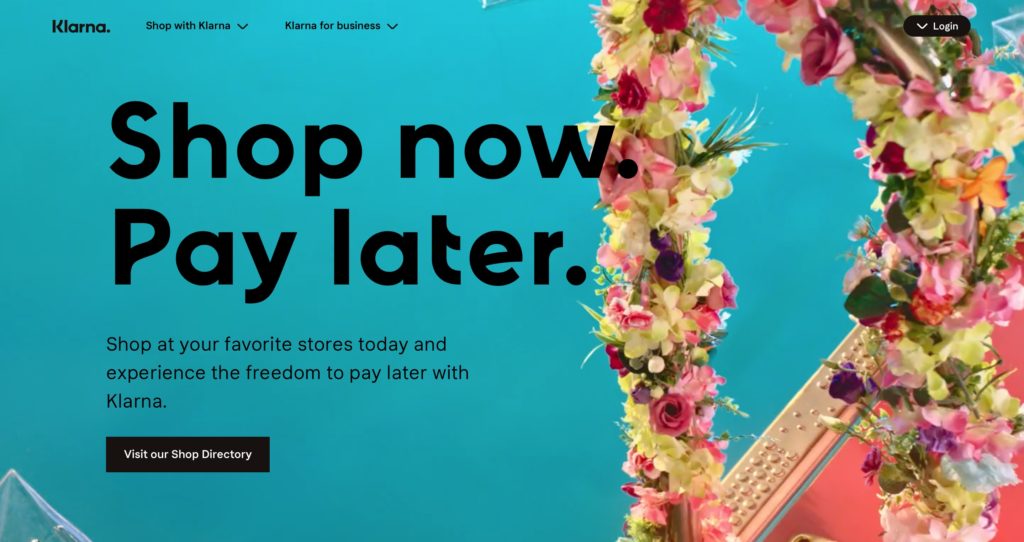

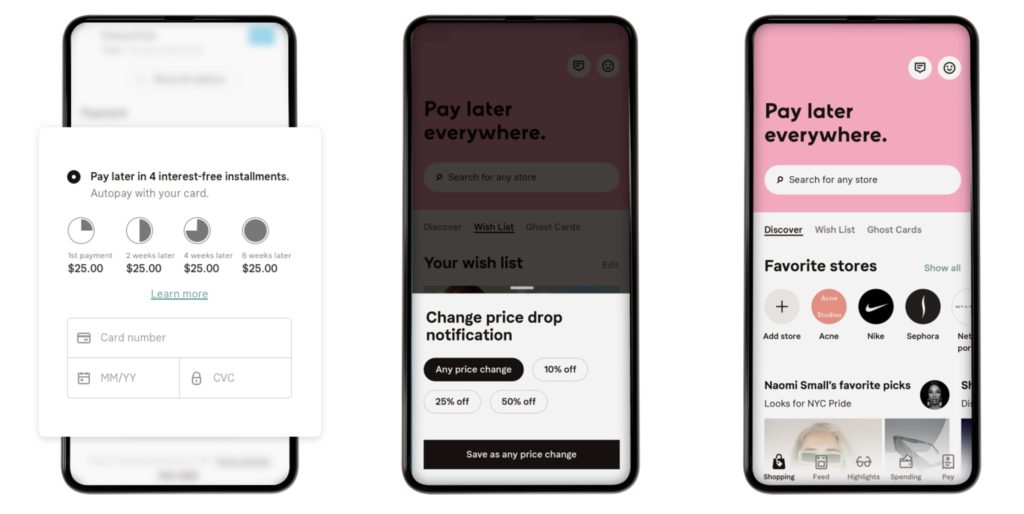

An investment of $460 million in Swedish e-commerce payments innovator Klarna takes the company’s valuation to $5.5 billion, and makes it the largest private fintech firm in Europe. The funding will help fuel Klarna’s international growth, especially in the United States, where it has been gaining new customers at a rate of six million a year.

Dragoneer Investment Group led the round. Commonwealth Bank of Australia, HMI Capital LLC, Merian Chrysalis Investment Company Limited, Första AP-Fonden (AP1), IPGL, IVP, and funds and accounts managed by BlackRock also participated. Combined with the financing from a round this spring, the investment gives Klarna more than $1.2 billion in total capital.

For company CEO and co-founder Sebastian Siemiatkowski, the funding comes at a moment of great opportunity for fintechs like Klarna that are innovating in the area of consumer finance. “This is a decisive time in the history of retail banking,” he said. “Finally, transparency, technology and creativity will serve the consumer, and there will be no more room for unimaginative products, non-transparent terms of use or lack of genuine care of ones customers.”

Klarna’s Shop Now Pay Later approach to e-commerce enables consumers to pay for purchases at leading, brick and mortar retailers as well as with online merchants, with a variety of interest-free, no-fee financing offerings. These include a four installment payment option that charged every other week to the customer’s credit or debit card, and 30-day payment period that begins once the item is shipped or received.

Klarna has more than 60 million shoppers using its offerings, and 130,000 retailer partners around the world. Richard Watts of Merian Chrysalis Investment Company credited Klarna with providing its merchant partners with “considerable improvement in customer engagement and sales.” In fact, Klarna reports that merchants that are offering its four installment payment plan have experienced a 68% increase in average order value, a 44% increase in conversion v.s. cards, and a 21% higher purchase frequency.

“Klarna is one of Europe’s great fintech success stories and the company continues to develop truly innovative payment solutions,” Watts said.

The funding news for Klarna arrives amid a flurry of new service offerings, such as making its Shop Now Pay Later option available in-store, as well. It has also been a big year for products, from the launch of its global customer authentication platform to unveiling of its open banking platform. 2019 has also been a busy year in terms of partnerships: Klarna joined global fashion retailer ASOS in an expansion to the U.S., teamed up with U.K. fashion brand Superdry, and partnered with Canadian e-commerce and in-store point-of-sale financing company PayBright.

Founded in 2005 and headquartered in Stockholm, Sweden, Klarna demonstrated its platform at FinovateSpring 2012.

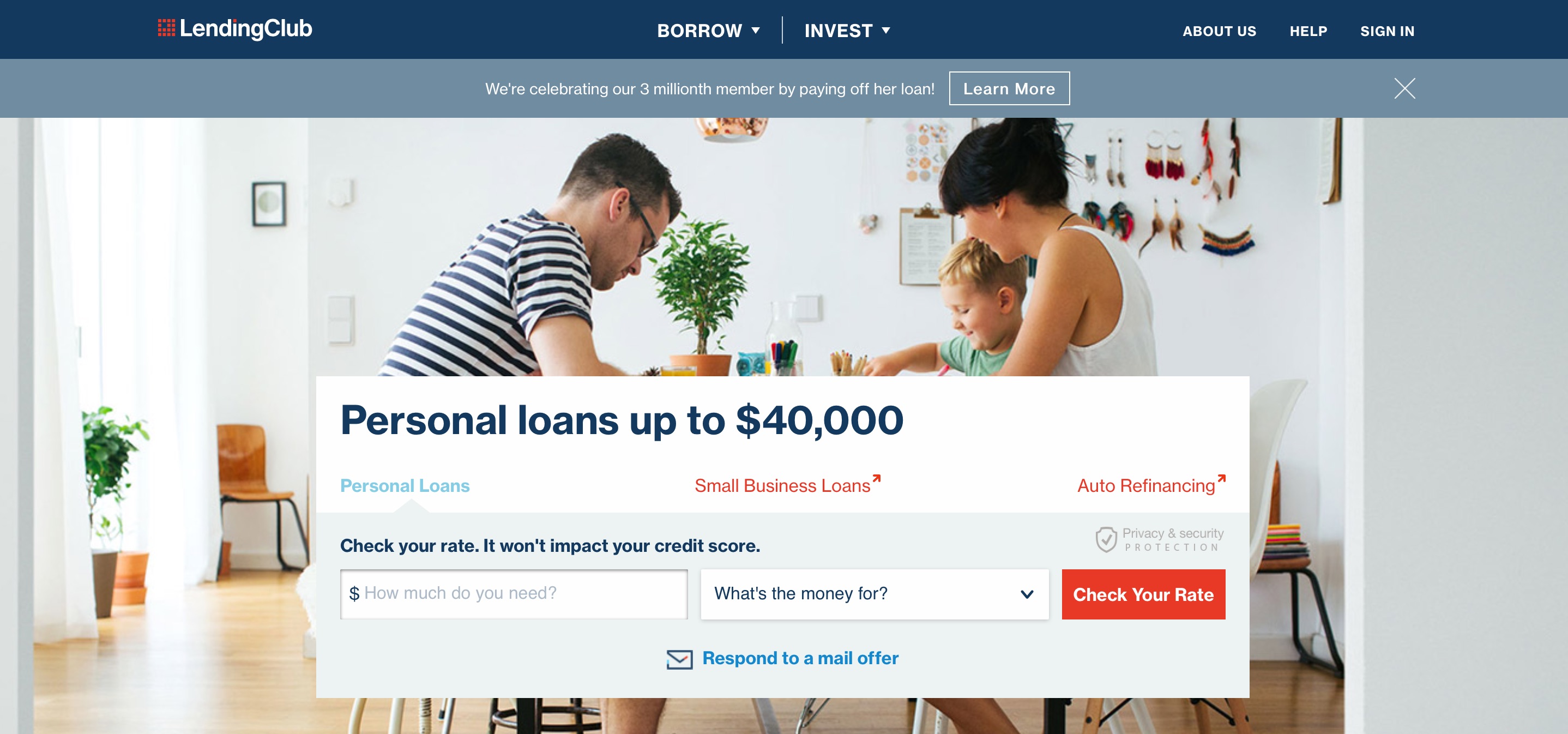

Months after LendingClubannounced that it was closing its small business lending division, the online P2P credit marketplace is back in the fintech headlines with the launch of the Select Plus Platform. The solution enables sophisticated investors to participate in the financing of borrowers “who fall outside current criteria” of bank lenders.

Select Plus provides these borrowers with the opportunity to get the access to credit they need, while giving investors the ability to pursue potentially attractive risk adjusted returns. The solution will also boost LendingClub’s customer base, and help the company facilitate the more than 14 million applications for loans it received in 2018 alone.

Growing from inception to execution in less than a year, Select Plus is a testament to LendingClub’s product-building ability, according to company Chief Capital Officer Valerie Kay. In addition to getting to market quickly, Select Plus shows how the company is uncovering new ways to leverage its platform.

“This is a huge step forward in our evolution as we continue to unlock the power of the marketplace model to generate access and ultimately savings for borrowers by finding and matching the right capital sources with the right borrowers,” Kay said.

Select Plus already has its first investor. Theorem Partners, a firm that leverages data science and machine learning to invest in marketplace loans, will integrate its Theorem Score credit investment model with LendingClub’s new solution.

One of Finovate’s oldest alums, LendingClub demonstrated its “online lending community” at the very first Finovate conference in 2007. In the years since, the company has grown into the largest P2P lending marketplace in the world with more than three million customers and more than $50 billion in loans facilitated on its platform. In June, the company celebrated its three millionth member by paying off the borrower’s 6% APR, $40,000 debt consolidation loan in full.

Last month, LendingClub introducedLevered Certificates, a new financial product that combines an equity certificate based on a pool of unsecured personal loans with a fixed rate note to provide consistent financing over the term of the certificate. The company began the year partnering with U.K. data vendor Brismo to provide standardized performance metrics for lending.

Publicly-traded on the New York Stock Exchange under the ticker LC, Lending Club has a market capitalization of $1 billion. The company was founded in 2006, and is headquartered in San Francisco, California. Scott Sanborn is President and CEO.

Swiss digital banking software provider, CREALOGIX, is moving from its traditional initial license to a Software-as-a-Service (SaaS) model, reports Jane Connolly of Fintech Futures (Finovate’s sister publication).

Although the intended transition has resulted in a drop in profitability of just over $5 million (CHF 5 million), sales have increased by 17% to exceed $101.5 million (CHF 100 million) for the first time.

Reporting preliminary results for the 2018/19 financial year, CREALOGIX states that the move to a SaaS-based, multi-year subscription model will result in greater revenue stability and sustained profitability increases in the long term.

The company believes that it will see solid cashflow levels and double-digit EBITDA margins from 2020/21 onwards. CREALOGIX notes that the continuing uncertainty around Brexit has had a pronounced negative impact on the UK business.

Recent new deals for the company have included agreements with Hampden & Co, LGT Vestra and MeDirect.

Founded in 1996 and headquartered in Zurich, Switzerland, CREALOGIX demonstrated its TimeWarp solution at FinovateEurope 2019, winning Best of Show. TimeWarp enables banking customers to run simulations of various scenarios in their financial lives to better understand how today’s decisions are mostly likely to affect financial outcomes.

King Klarna: New Investment Boosts Valuation to $5.5 Billion.

LendingClubUnveilsSelect Plus for Sophisticated Investors.

Around the web

Israel’s third largest bank Mizrahi-Tefahot to deploy core banking technology from Temenos.

Experianreports surging interest in Open Banking, with the number of API requests made in the U.K. growing by more than 2x since February.

Russia’s Tinkoff Bank to sell the speech recognition technology behind its Oleg chatbot to corporate customers.

LeapXpertearns spot in 2019 FinTech Innovation Lab Asia-Pacific.

Mortgage Cadenceenhances data verification, fraud prevention and compliance with integration of DataVerify to its Enterprise Lending Center.

AT&T launches new bug bounty program in partnership with HackerOne.

Jumiotakes gold in the Security Software category of the 2019 IT World Awards.

Lendiotops $1.5 billion in small business loans financed.

OndotintroducesTransaction Intelligence to make it easier for consumers to recognize purchases.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Helping small businesses in the U.K. maximize the opportunities of Open Banking is the goal of the new partnership forged between AccountScore and financial data sharing and standardization specialist Validis. The two companies announced that they will work together to ensure that SMEs get access to more transparent financial services, and that U.K. institutions gain the most accurate financial overview of their clients.

The agreement between the AISP accredited Open Banking platform and Validis will enable small businesses to share financial data with a single click through a single, consent-driven workflow. Banks can visualize the data from an “insight-fueled interface” and track critical processes like loan originations. This collaboration will help institutions develop more personalized banking services for specific businesses, and enhance their ability to make better, more accurate decisions faster.

“As Open Banking becomes more established, having a single intuitive workflow where SMEs can share their data easily and securely opens up huge possibilities for financial services,” AccountScore CEO Emma Steeley said. “Our unique relationship with Validis ensures we can visualize all the financial data required to help these institutions tailor their services, make the right decisions, and identify insights that they could not previously.”

In addition to helping businesses and financial institutions make more of their data, the ability of different datasets to complement each other – using management account data to confirm bank transaction data, for example – adds new value to the processes financial institutions conduct every day. This is value institutions have not been able to capture until recently.

“We are excited to sign this partnership agreement with AccountScore,” Validis CEO Joel Curry said. “For too long financial institutions were only seeing individual pieces of the puzzle, but now they will have access to all the data, all in one place.” Curry called the partnership “a truly innovative step forward for small business financial services.”

AccountScore demonstrated its consents.online solution at FinovateEurope earlier this year. Consents.online is the consent management feature of the company’s Open Banking solution, and helps users manage their online consents in one centralized location. Customers can visit consents.online and review what data has been accessed and by whom, as well as change consent permissions.

Founded in 2016 and headquartered in London, U.K., AccountScore has partnered with The Insolvency Panel earlier this year to develop a solution for the debt and debt solutions sector to give financially challenged individuals the ability to more easily share their financial data with financial institutions. In February, Freedom Finance announced that it had reduced application time to five minutes thanks to technology from AccountScore.

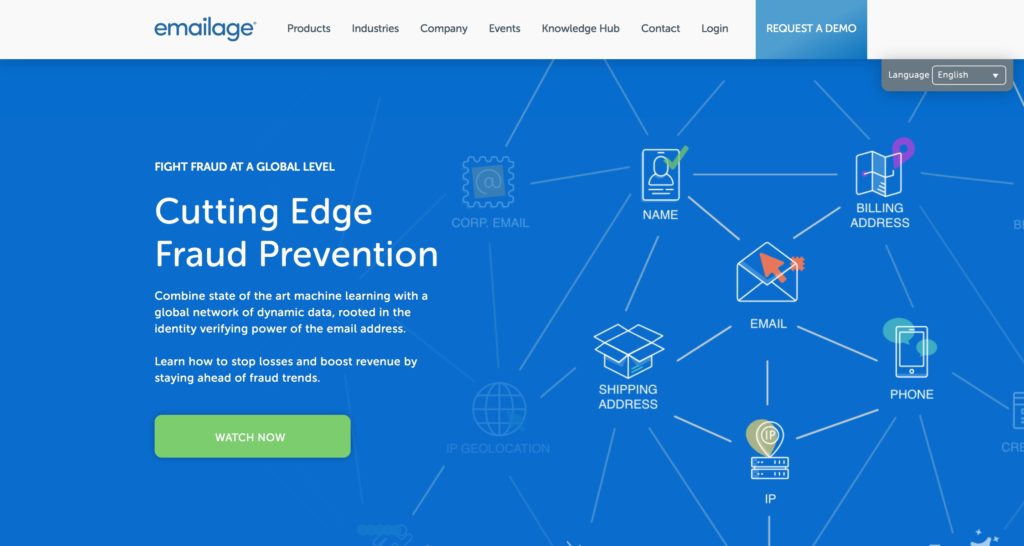

The newly announced collaboration between email risk assessment innovator Emailage and fraud prevention and risk management firm Featurespace is designed to combat online application fraud, a problem that grew by 159% last year according to U.K. Finance.

The partnership integrates Featurespace’s ARIC Fraud Hub with Emailage’s data and risk assessment scores. The combined solution identifies and reports application fraud in real time, boosting the accuracy of customer authentication during processes like onboarding and account maintenance. The integration will also make it easier for institutions to comply with the latest payment regulations.

“In order to keep up with the fast-changing payment landscape, we are always on the lookout to leverage our expertise and that of other providers,” Chief Partnership Officer at Emailage Tim White said. “Emailage and Featurespace are two companies moving in the same direction in terms of innovation and growth. Therefore, we felt this collaboration was a highly strategic opportunity.”

“This is yet another step in our journey to provide our customers with full regulatory compliance and a best-in-class solution,” White said.

Emailage turns email addresses into global digital identifiers. The company leverages a worldwide data network to assess the likelihood that the individual who provided the email address is reliable as a potential customer or applicant. Via the integration, digital identities that are established by Emailage are then processed by the Adaptive Behavioral Analytics of Featurespace’s ARIC platform, which builds individual behavioral profiles. This improves the ability of the machine learning models to automatically detect risk and to combat new threats as they develop. Emailage noted that it has helped organizations around the world mitigate $2.8 billion in fraudulent purchases and applications.

“This integration makes it easy for all of our customers to leverage the combined power of our innovative Adaptive Behavioral Analytics and Emailage’s proprietary data set to improve risk scoring and reduce exposure to sophisticated online threats at the point of application,” Featurespace CEO Martina King said.

Founded in 2008, Featurespace demonstrated its ARIC Fraud Manager solution at FinovateFall 2016. The company’s partnership announcement with Emailage comes at the same time as a report that banking and payments solutions provider Contis has completed deployment of Featurespace’s ARIC Fraud Hub.

In June, Featurespace announced that it would power transaction monitoring for Ireland’s Permanent TSB. This spring, the company was highlighted by Aite Group in its 2019 report on anti-fraud and AML machine learning platform vendors, and its CEO was profiled by Hypepotamus on the topic of workplace diversity.

Earlier this year, Featurespace announced a partnership with retail finance technology provider Deko, and launched its technology in Singapore. The company began 2019 with a major fundraising, bringing in $32.3 million (£25 million) in new capital in a round led by Insight Venture Partners.

Emailage demonstrated its Browser Extension at its Finovate debut in 2015. The extension marks email with an easily identifiable icon that enables users to get an instant analysis on the risk associated with the email. With the extension, users of Chrome, Firefox, and Internet Explorer can leverage Emailage’s fraud-detecting technology to assess the risk of emails and websites.

Emailage wonBest E-commerce Initiative at the PayTech Awards in London last month. This spring, the company introduced a trio of new points of presence in Singapore, Australia, and Germany, in what company CTO Rafael Loureiro said demonstrated the company’s “strategic commitment” to making its technology available worldwide. An office in Dublin, Ireland, was opened in June.

Emailage also announced it added a “big four” U.S. bank, a major Asian payment platform, and a global e-commerce solution provider to its shared intelligence network in the first quarter of this year. Founded in 2012, the company has raised $15.7 million in funding from investors including Anthos Capital, Cobre Capital, and Mucker Capital. Rei Carvalho is CEO.

UBS has formed a partnership with BizEquity, an online provider of estimated business valuations. This will allow a select group of UBS financial advisors in the US arm of its global wealth management business, to access BizEquity’s database of businesses and valuation information, reports Sharon Kimathi of Fintech Futures (Finovate’s sister publication).

Enterprise access through BizEquity will support UBS financial advisors to provide clients with informal valuation reports that will assist them with their financial planning needs.

James Jack, director of the business owner strategic client segment at UBS Financial Services said: “Our advisors are constantly looking for new ways to grow their business and expand their reach, particularly in middle-market businesses. Access to the BizEquity platform will help us to deliver highly tailored advice to our clients.”

“UBS is one of the preeminent names in the wealth management industry and we are proud to announce our partnership. The clients and prospects that it serves will benefit from our service to help them answer one of the most important questions they will ever ask: ‘What is my business worth?’” said Michael M. Carter, founder and CEO of BizEquity.

BizEquity is a leading provider of business valuations, distributing its cloud-based service through thousands of financial advisors to help better inform businesses of their lending, insurance, and wealth management needs and potential.

Founded in 2010, BizEquity demonstrated its BizEquity One UK solution at FinovateEurope 2015. The technology provides real time, dynamic valuations, “Zillow-esque” search functions on more than two million pre-valued businesses in the U.K., real time advice and alerts during the valuation process, and an dashboard that provides an infographic-like overview of business value and KPIs.

BizEquity has raised $5.1 million in funding. Brinker Capital and Frost Books are among the company’s investors.