This week’s edition of Finovate Global looks at recent fintech headlines from India.

CRED raises $900 million in round led by Meta

CRED, a membership-based, credit rewards platform that offers solutions across payments, lending, insurance, wealth, and lifestyle, has secured $900 million in Series H funding. The round was led by Meta, and will be structured through a combination of primary and secondary share purchases. Meta will join the CRED cap table as a minority investor; CRED will earn a post-money valuation of $4.5 billion.

With 1.7 million members engaging with its platform every month, CRED processes more than 40% of credit card bill payments in India, and has seen its lending business grow to more than $2.5 billion in managed assets. The investment will enable the company to accelerate growth, build “institutional muscle,” and extend its leadership across verticals. The company announced that its founder, Kunal Shah, will transition from his operating role as CEO to head WhatsApp internationally. India is WhatsApp’s largest market, with more than 500 million users. Miten Sampat, who has led strategy and finance for CRED since 2020, will take the helm as interim CEO.

“I started CRED in 2018 with a belief that creditworthiness deserves to be rewarded,” Shah said. “In under eight years, that belief has turned into a new category: millions of members, $325 million in revenue, profitability, a full stack of licenses, and a strong brand. On this foundation, with additional capital and an extraordinarily talented team, CRED is poised to become an enduring institution for decades to come.”

CRED is headquartered in Bengaluru, Karnataka, India. The company’s investment announcement comes as the firm launches a new AI-powered credit coaching solution for CRED members. The AI credit coach provides personalized, real-time guidance based on the user’s credit profile to help them better understand their credit status and improve their credit health.

Navi UPI enhances fraud protection capabilities

Navi UPI, a popular UPI app, has unveiled Navi Secure, a new unified framework that combines the platform’s existing fraud prevention, risk monitoring, and user protection capabilities. The offering is designed to help merchants and users deal with the proliferation of increasingly sophisticated fraud attacks that leverage social engineering, compromised devices, false merchants, and more.

With intelligent risk signals, contextual alerts, and preventive safeguards embedded in the customer journey, Navi Secure helps firms reduce risk across a range of fraud scenarios, including scam-driven payments and manipulation-based fraud; compromised devices and apps; unsafe networks and environments; and high-risk entities and transaction behavior.

“Given digital payments have become central to everyday life, fraud prevention needs to be real time and contextual. Navi Secure reflects our commitment to building trust-first financial infrastructure, where safety is embedded into every transaction, not added as an afterthought,” Navi Limited MD and CEO Rajiv Naresh said. “By combining advanced risk intelligence with user-friendly safeguards, we are ensuring that customers can use UPI with confidence, knowing that Navi is actively working in the background to protect their money.”

Navi UPI is among the fastest growing financial services companies in India. The company’s UPI transaction volumes grew from more than 709 million to more than 824 million between January and May 2026. The company currently has 3.6% of India’s UPI market share; a market dominated by PhonePe (46.2%) and Google Pay (32.7%).

Bengaluru-based Navi is a financial services company that provides personal and home loans, insurance, mutual funds, and gold investing, as well as UPI, India’s flagship instant real-time payments system (Unified Payments Interface). Navi UPI is the company’s money transfer solution, which leverages UPI to deliver money transfers anytime, anywhere. Navi was founded in 2018.

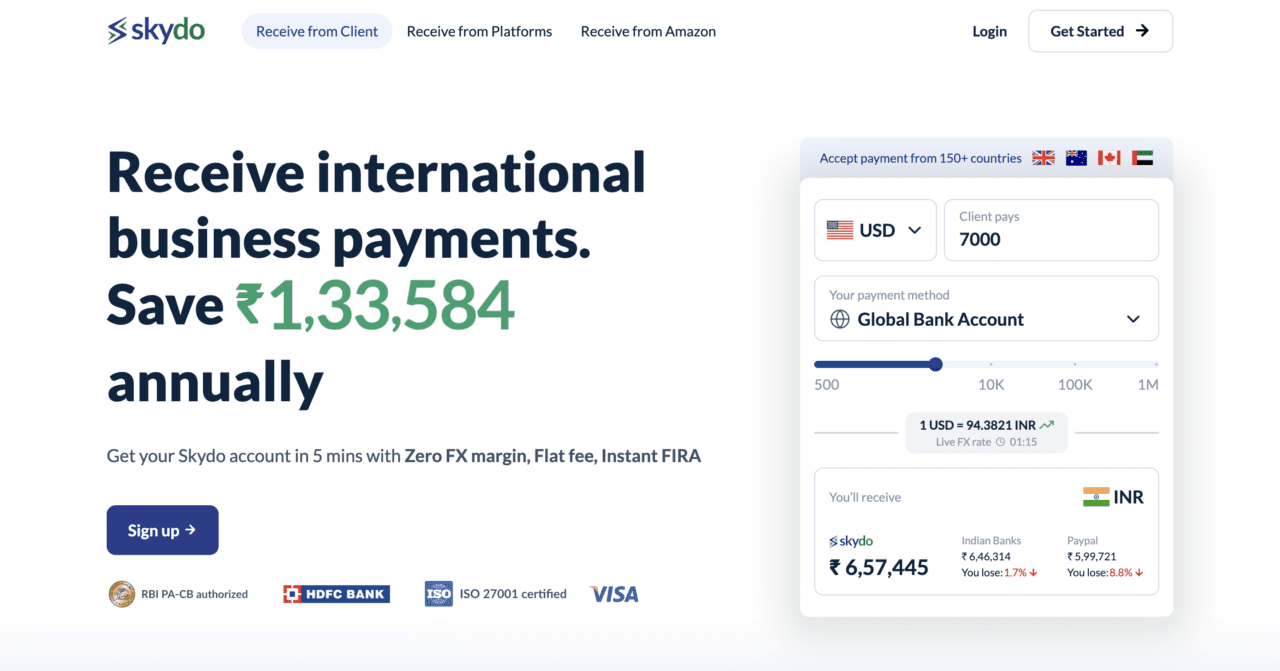

Indian paytech Skydo expands to Canada

Payments platform Skydo has won its first regulatory approval outside of its native India. The Bengaluru-based company has secured an international payment license in Canada that will enable the company to offer two-way payment flows, including local collections and payouts, between India and Canada.

“Securing our first international license marks Skydo’s evolution from an India-focused cross-border payments platform to a multi-country payments operator,” Skydo CEO and Co-Founder Srivatsan Sridhar said. “With Canada, we are expanding beyond collections to enable seamless two-way payment flows and support growing India-Canada commerce.”

Founded in 2022, Skydo is a cross-border B2B payments specialist, reducing foreign exchange charges for businesses by more than 50%. The company partners with leading banks around the world, providing businesses with their own foreign virtual accounts to enable them to receive payments without tax or compliance complications. Supporting more than 150 countries, Skydo’s platform processes more than 200,000 payments a year and is used by 40,000+ Indian exporters.

Skydo has referred to Canada as a strategic market, given the scale of trade activity between India and Canada. In 2025, India and Canada reached $10.9 billion in bilateral merchandise trade. Both countries have indicated that they would like to more than double two-way trade, currently at just over $30 billion annually, to $70 billion by 2030.

“Our ambition is to build for the world, from India,” Skydo Co-Founder Movin Jain said. “Canada strengthens our global footprint, enables local collections and payouts, and creates a strong foundation for future expansion across North America.”

Skydo’s regulatory win in Canada comes just a month after the company received in-principle approval to operate as a Payment Service Provider (PSP) in the International Financial Services Centre (IFSC) at Gujarat International Finance Tec-City.

Here is our look at fintech innovation around the world.

Asia-Pacific

- Japanese financial giant SBI Holdings agreed to acquire crypto exchange Bitbank for $298 million.

- Singapore-based fintech platform Airwallex earned a valuation of $11 billion after securing $320 million in Series H funding.

- Mynt, the parent company Philippine mobile payments and finance superapp GCash, has filed for an $1.5 billion IPO on the Philippine Stock Exchange.

Sub-Saharan Africa

- Nigerian fintech Daya secured $2.4 million in pre-seed funding to expand its stablecoin payments technology for African businesses.

- Kenya-based fintech WapiPay received a Money Services Business license from Canada’s Financial Transactions and Reports Analysis Center (FINTRAC).

- Pan-African fintech DigiPay and French fintech Belmoney launched DigiTransfer, a mobile app that enables money transfers between France, Belgium, the Republic of the Congo, and the Democratic Republic of Congo.

Central and Eastern Europe

- Albania launched its first fully digital bank, Jet Bank.

- Mastercard and PrivatBank announced completion of Ukraine’s first payment executed by AI agent.

- Austrian-Swiss global payout infrastructure startup Talentir raised €4 million in seed funding in a round led by Redstone.

Middle East and Northern Africa

- Egyptian fintech MNT-Halan announced plans for an IPO that could give the company a valuation of $1 billion.

- Lean Technologies and Ziina teamed up to launch the UAE’s first One-Tap Pay by Bank experience.

- Israeli fintech Payoneer agreed to be sold to Canadian firm Nuvei for $2.7 billion.

Central and Southern Asia

- Indian fintech Cred secured $900 million in Series H funding in a round led by Meta.

- Karachi-based easypaisa digital bank inked a Memorandum of Understanding (MoU) with Binance to “explore innovative opportunities” in fintech, digital savings, and investment solutions.

- Indian UPI app Navi UPI, unveiled a new unified safety framework, Navi Secure.

Latin American and the Caribbean

- CSU Digital, the largest independent card processor in Latin America, has embarked upon its US expansion.

- Iupana looked at how new governments in Colombia and Peru are seeking to bolster the fintech sectors of their respective countries.

- Payward, financial infrastructure platform and parent company of Kraken, secured a Virtual Asset Service Provider (VASP) registrations from the British Virgin Islands Financial Services Commission (BVI FSC).

Photo by Shiv Prasad on Unsplash