This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Credit Karma has agreed to acquire technology and assets from Zendrive, a mobility risk intelligence provider.

Credit Karma has also brought on certain Zendrive employees, including the company’s CEO Dennis Ellis and its Co-founder and CTO Pankaj Risbood.

Terms of the deal, which is expected to close in the fourth quarter, were not disclosed.

Intuit’sCredit Karmaannounced today that it has agreed to acquire technology, assets, and select employees from mobility risk intelligence provider Zendrive. Terms of the deal were not disclosed.

Credit Karma will use the new technology to accelerate development and adoption of its auto insurance product, Karma Drive. Launched in December of 2020, Karma Drive leverages Zendrive to offer customers a telematics-powered, usage-based insurance savings opportunity based on their driving habits. After a 30-day driving trial, during which users receive continuous real-time feedback on their driving, they are offered a potential discount on a new policy from one of Credit Karma’s auto insurance partners.

Since launch, more than 6 million members have enrolled in the Karma Drive program, which has extended more than 4 million discounted policy offers from Credit Karma’s insurance partners.

“We see opportunities to improve traditional telematics practices that lock consumers into a policy and track driving behaviors in a way that can potentially increase policy costs,” said Credit Karma’s Rory Joyce in a blog post announcement. “We have redefined and simplified consumers’ access to insurance discounts based on mobile telematics data. Karma Drive users can see if they can qualify for a discount from carriers without having to buy a policy or even engage directly with the insurer.”

As part of today’s deal, which is expected to close in the fourth quarter of this year, Credit Karma has acqui-hired certain Zendrive employees, including the company’s CEO Dennis Ellis and its Co-founder and CTO Pankaj Risbood. Credit Karma anticipates the new talent will help it to scale its telematics experience.

Intuit is closing down Mint, which it acquired in 2009.

Mint users are being directed to sign up for a Credit Karma account.

Founded in 2006, Mint is one of the oldest B2C fintechs.

For those of us who have grown up and grown old with fintech, January 1, 2024 will go down in history. That’s because Mint– which is arguably the first-ever direct-to-consumer fintech– is shutting its doors on that day.

Mint parent company Intuit announced earlier this week that it is folding Mint into Credit Karma and is inviting all Mint users to open an account at Credit Karma. “We know the most active Minters use Mint to monitor their cash flow and track their spending, and not only does Credit Karma offer these capabilities, but we’re able to take things even further for our members,” Intuit announced in a blog post.

As a bit of history, Intuit acquired Mint in 2009 for $170 million and purchased Credit Karma in 2020 for $4.7 billion. After acquiring Credit Karma, there was likely a bit of internal unrest at Intuit, since Mint and Credit Karma are essentially rivals. Both companies rely on advertiser spend via product referrals, and growing one brand would hurt the other.

Rolling Mint into Credit Karma will help Intuit double-down on sponsored advertisement revenue. The move will also build Credit Karma into a more robust competitor in the PFM space. Credit Karma was founded in 2007 to offer a flagship credit tracking and credit card comparison service and has since expanded to offer a tax filing service, checking account, savings account, credit-building credit card, and more.

It’s not surprising to see Mint’s demise. Intuit already started to cannibalize the brand earlier this year when it pulled Mint’s team in to build Credit Karma’s new NetWorth feature, a tool that enables users to view and track their net worth in a single place. Also, in a way, Mint died a long time ago. The company, which claimed 3.6 million monthly active users in 2021 but as of this year has had no material revenue, hasn’t released any new features or made any significant announcements in recent years. In fact, my last blog post about the company was titled, “Mint Brings User Interface into 2018.” Meanwhile, the company’s competitors in the PFM space were releasing their own banking tools, lending services, and investment tools.

In the grand scheme of today’s fintech landscape, this announcement will have little impact. However, the news is worth noting for the sake of history. Mint– a company that at one point owned the entire fintech category– stood still while watching the entire fintech industry evolve around it. The company even demoed at the first-ever Finovate conference in 2007. Mint may have been able to keep up had it not been acquired by Intuit, but we’ll never know. Rest in peace, Mint (2006- 2023), and say hello to all of the other fintech ghosts on the other side for me.

Credit Karma is launching Net Worth, a new tool that will enable users to view and track their net worth in a single place.

Intuit’s Mint business has joined the Credit Karma team to facilitate the new Net Worth tool.

At launch, the Net Worth tool will be available to U.S. consumers with credit scores above 720.

Intuit-owned Credit Karma is expanding from credit building into wealth building this week with its new launch, Net Worth. The new tool aims to help the company’s 120 million U.S. members track their net worth, and places Credit Karma one step closer toward its goal of becoming a full service personal financial management platform.

Intuit subsidiary Mint is key to today’s launch and has joined the Credit Karma team to implement the new offering. Mint launched in 2007 to help users keep track of all of their accounts in a single place. The company was one of the first to offer account aggregation in a direct-to-consumer offering.

“Credit Karma’s mission is to champion financial progress for all, but we know that financial progress looks different for everyone,” said Credit Karma CEO and Founder Kenneth Lin. “This next evolution of Credit Karma will combine the expertise and momentum generated by Mint with Credit Karma’s scale and technology, and enable us to help more Americans, in particular those who are faced with a new set of financial challenges and are looking to elevate and protect their net worth.”

At launch, Net Worth will be quite simple. The tool will help members understand the components of their net worth, monitor changes, and track their transactions over time. Future iterations will enable users to protect their net worth, maximize credit card rewards based on spending habits, and view investment insights. Interestingly, each of these secondary iterations comes with potential revenue streams, such as selling insurance, credit card promotional partnerships, etc.

Credit Karma is making Net Worth available to U.S. consumers with credit scores above 720 and hopes to expand the tool to more users over time. “Net Worth was built for U.S. consumers who have already made significant progress on their credit score and are looking for that next financial health indicator to track and take action on, as they continue their financial journey,” said Mint General Manager Ryan Steckler. “Before we can help consumers grow their net worth, we’ve built a seamless product experience that gives consumers a holistic view of all of their financial accounts, directly within the Credit Karma app.”

You can thank Gen Z’s “I want it now” mentality for Credit Karma’s freshest release. Dubbed Instant Karma, the newest product is the latest to come from Credit Karma Money, the company’s challenger banking service.

According to TechCrunch, which covered the launch, Instant Karma rewards users by randomly reimbursing their purchases.

Credit Karma General Manager Poulomi Damany told TechCrunch that, since the purpose behind Credit Karma Money is to “change people’s relationship with money” the new rewards product is an extension of that goal.

There are two major differentiating factors of Instant Karma over traditional payments rewards programs. The first is that the rewards are issued based on purchases made on debit cards, not credit cards. That’s because, as Credit Karma Product Manager Kyle Thibaut said, “Gen Z do not necessarily like credit cards. When you talk to them, they like debit cards and debit cards are the way they spend. Debit card usage is higher than credit cards in the U.S., and it’s actually growing while credit card usage is declining.”

The second point of differentiation is that the reward is issued the instant the user makes the transaction. Traditional cash-back programs, in contrast, will only issue rewards based on a time scale (eg., monthly) or once they reach a certain threshold (eg., the balance reaches $25).

So far, Credit Karma has rewarded $5 million in rewards on 100,000 transactions.

Founded in 2007, Credit Karma added a checking feature to its Credit Karma Money suite in October of last year. This complements the savings tool the company launched in October of 2019, when it initiated its entrance into the neobanking space. Prior to this, Credit Karma operated solely in the financial wellness space, in which it continues to offer its 110 million members access to credit scoring data, loan and credit card marketplaces, identity monitoring, and tax filing tools.

An integration between two of Intuit’s top acquisitions, consumer financial technology platform Credit Karma and TurboTax tax management software, will help put the former’s new U.S. checking account – Credit Karma Money Spend – in the hands of more consumers.

The integration will provide a seamless process for getting refunds to eligible taxpayers when they file their taxes with TurboTax – and then turn those taxpayers into Credit Karma checking accountholders. Filers on TurboTax will have the ability to open a Credit Karma Money Spend account and have their refund sent directly to that new checking account. Users then can access the full Credit Karma Money experience – for example, setting up direct deposit and adding debit cards to their digital wallets – from within TurboTax. The checking account’s Instant Karma feature also encourages users to make payments with their Credit Karma Money Spend accounts by offering monetary rewards for actions like on-time credit card bill payments and automating direct deposits.

“We believe consumers should have a checking account that helps them make financial progress, which is why we created Credit Karma Money Spend,” Credit Karma founder and CEO Kenneth Lin explained. “We’re starting 2021 off by leveraging our relationship with Intuit to bring Credit Karma Money to millions of tax filers this tax season.” Lin referred to tax refunds as “the biggest paychecks” many Americans receive, and added that getting taxpayers the refunds they are owed and helping them put that money to work “(maximizing) their day-to-day spending and billpay” is a critical role the new integration will play.

Acquired by Intuit in a deal just completed in December, Credit Karma is among Finovate’s earliest alums, demonstrating its consumer credit score monitoring platform back in 2008. Now with more than 110 million members in the United States, Canada, and the U.K., Credit Karma offers a wide range of financial wellness solutions for individuals including identity monitoring, credit cards and loan shopping, insurance, high-yield savings accounts and, most recently, its new checking accounts backed by bank partner MVB Bank.

The integration news comes in the wake of a flurry of recent criticism that Credit Karma’s credit scores varied from what users were expecting when engaging with credit card companies or prospective lenders. The differences have since been explained – Credit Karma uses a credit score model, VantageScore 3.0, that not only examines factors other than those traditionally considered for FICO scores, but also can weigh like factors differently. But the issue may reflect a growing trend of popular annoyance with some of the ways fintechs are able to provide the services they do. This “Robinhood Syndrome” is a challenge that is only likely to grow as more customers – with varied expectations and financial sophistication – continue to migrate to fintech platforms.

From in-house innovation to outright acquisition, businesses have myriad paths to consider when looking to expand their product portfolios. We learned late last week that mobile payments company Square has taken one of the less flashy routes to growing its offerings: paying $50 million in cash for Credit Karma’s tax business. Square will add the service’s DIY tax filing functionality to its own Cash App.

The free tax filing option will be featured along with the app’s other financial tools, including P2P payments, Cash Card, direct deposit, and the ability to make fractional investments in stocks and bitcoin. Cash App was launched by Square seven years ago as a P2P money transfer service and has grown into an integrated financial ecosystem with more than 30 million monthly active customers as of June 2020.

“We created Cash App to provide more access to the masses of people left out of the financial system and are constantly looking for ways to redefine our customers’ relationship with money by making it more relatable, instantly available, and universally acceptable,” Cash App lead Brian Grassadonia said.

One in two tax filers – a total of 80 million taxpayers – prepared and filed their own Federal income taxes electronically in 2020, according to the IRS, and the trend is expected to accelerate. Credit Karma Tax Director of Engineering Patrick Fink underscored this point, noting that despite the “challenge” of filing taxes, more customers are transitioning toward filing taxes on their own. “Credit Karma Tax provides a seamless, mobile-first solution for individuals to file their taxes at no cost,” Fink said. “We’re excited to be joining an entrepreneurial team and continue to build simple, innovative tools for Cash App customers.” Credit Karma tax processed more than two million tax filers last year.

The acquisition is expected to close by the end of 2020 and is subject to customary closing conditions.

Square’s investment in its Cash App is timely. At the beginning of the month, the company noted in its third quarter financial reporting that Cash App had generated more than $2 billion in net revenue and $385 million of its gross profit for the quarter. The performance reflected gains of 5.74x and 2.12x, year over year, respectively.

The timeliness of the transaction also has a lot to do with Intuit’s acquisition of Credit Karma, which was cleared by the U.S. Department of Justice last week. Announced at the beginning of the year, the $7 billion deal is Intuit’s largest acquisition to date, and by shedding Credit Karma’s tax business, an obstacle to the union between the two companies has been removed. Intuit is the developer of it own online tax filing service, TurboTax.

“We are very excited to reach this important milestone today,” Intuit CEO Sasan Goodarzi said. “This brings us one step closer to transforming personal finance by making it simpler for consumers to find the right financial products, put more money in their pockets, and provide financial expertise and advice.”

The Credit Karma Tax announcement also comes one month after Square announced a $50 million investment in bitcoin, a sum the company said represented “approximately one percent” of the firm’s total assets as of the end of Q2 2020. Bitcoin trading has been available on Square’s Cash App since 2018 and, as of 2019, the company’s Square Crypto team has been contributing to bitcoin open-source efforts.

“We believe that bitcoin has the potential to be a more ubiquitous currency in the future,” Square Chief Financial Officer Amrita Ahuja said. “As it grows in adoption, we intend to learn and participate in a disciplined way. For a company that is building products based on a more inclusive future, this investment is a step on that journey.”

Taxes, especially in the U.S., can be anxiety-inducing not only for consumers but also for small businesses. And even though this year’s tax filing deadline has been extended to July 15, the filing and payment requirements remain unchanged.

“The daunting task of gathering documents for a year that has passed is one that is difficult for small business owners, especially when they already feel overwhelmed at tax time,” said Lil Roberts, CEO and founder of Xendoo. “Coupling that pain point with small businesses feeling that federal tax is a “black box” and understanding how to maximize tax savings is also extremely frustrating.”

Fortunately, where there is a financial problem there is a fintech solution. There are many fintechs available to help both individuals and businesses not only understand their taxes but also to facilitate tax payment. Below, we’ve highlighted the top 10 tax-focused fintechs.

ANNA

ANNA offers a business bank account and mobile tax app that help merchants with their invoicing, expense tracking, and taxes. The company’s app reminds businesses about tax deadlines and helps them prepare by estimating how much they owe as they earn revenue. ANNA also has a team of accountants to help prepare and submit tax returns.

Avalara

Avalara offers tax compliance tools for a range of businesses. The Seattle-based company, which counts customers such as Pinterest, Adidas, and Bed Bath & Beyond, offers products to help companies calculate sales tax, gather data to prepare and file tax returns, as well as collect, store, and manage tax documents on behalf of the business. Avalara offers products tailored to specific businesses, including ecommerce, lodging, communications, and restaurants.

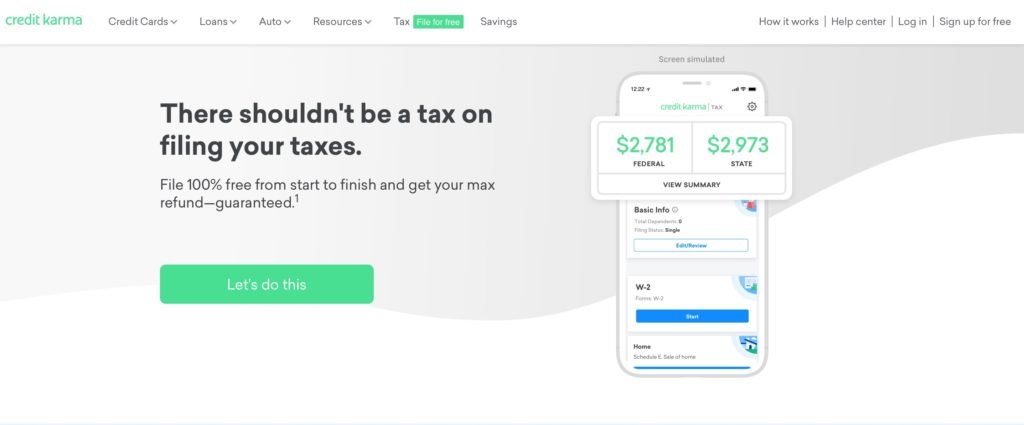

Credit Karma

In 2016, financial health company Credit Karmalaunched a free tax filing service. Interestingly, the company was recently purchased by TurboTax parent Intuit for $7 billion. In comparison with Credit Karma’s free service, TurboTax charges users anywhere from $60 to $120 for a federal return and $45 for a state return.

DAVO

DAVO launched in 2011 to be the ADP for merchants’ sales tax. In other words, DAVO automates the entire sales tax process on a business’ behalf. The company connects to the merchant’s point-of-sale technology to collect sales data and sets aside taxes on a daily basis. When sales tax is due, DAVO files and pays on the small business’ behalf.

Gusto

HR and payroll company Gusto has a robust set of services to make small business owners’ lives easier. The company automatically files payroll taxes and distributes I-9s, 1099s, and W-2s to employees. Gusto also helps businesses stay compliant by staying up-to-date on changing tax laws and doing all tax-related calculations on the business’ behalf.

Refundo

Refundo offers a suite of solutions to help tax preparers bring their operations into the digital age. Among the company’s products are mobile document transfers, audit assistance, tax preparation fee collection service, payment acceptance tools, and refund advance technology. At the end of the day, the company’s solutions not only make the tax preparer’s life easier, they make the lives of their taxpaying clients easier, as well.

RoamHR

With a mission to make self-employment easier, RoamHR automatically removes tax withholdings from users’ accounts once they get paid and places the funds into a RoamHR Tax Withholding Account. The company also offers tools that help users track deductible expenses, such as mileage, and helps them file their business taxes each quarter.

Taxnology

Taxnology has built a digital tax compliance center, a web-based solution to help businesses manage their taxes digitally. The company stores business’ historical tax data in the cloud so that it can be used for future cash flow planning and budget purposes or retrieved in the event of an audit. Taxnology is currently only available in Hungary.

Xendoo

Xendoo offers bookkeeping and CPA services that connect with businesses’ financial accounts to deliver monthly reports, business insights, and tax filing. Because Xendoo has a comprehensive view of the merchant’s financials, the company is able to provide tax consulting services, as well.

Xero

Cloud accounting software company Xero has been helping small businesses with their bookkeeping since it was founded in 2006. The company also offers solutions to help tax preparers who have Xero clients automate and customize tax-related tasks. For businesses who prepare taxes on their own, Xero offers tools to file taxes online, as well as prepare sales tax returns using software that leverages a company’s sales data to automatically calculate the taxes.

Roberts added one final thought for those businesses working toward that July 15 deadline. “For a smooth process, best practice is to have monthly bookkeeping done so tax benefits are being collected all year, and having books in order to make tax time more peaceful.” And during a pandemic, anything that can make a process more peaceful is worth doing.

How’s $7 billion for good karma? One of Finovate’s earliest alumsCredit Karma is reportedly the target of what would be Intuit’s biggest acquisition to date. According to The Wall Street Journal, the cash and stock deal could be announced as early as Monday.

Credit Karma will continue to function as an independent company with founder and CEO Kenneth Lin at the helm. The acquisition gives Intuit, maker of online tax filing service TurboTax, another contact point with the online personal finance world. Credit Karma provides its members with access to their credit scores and borrowing histories, helps them monitor their accounts for security breaches and, perhaps most relevantly, has offered a free online tax preparation service since 2017.

If the deal holds up, Intuit will be paying a significant premium for Credit Karma. The personal financial wellness company was last valued at $4 billion, based on a 2018 private market transaction.

With another Finovate conference in the books, our Finovate Best of Show ranks has a new set of members. Congratulations to Dorsum, Glia, Horizn, iProov, Sonect, and W.UP for taking home top honors earlier this month at FinovateEurope!

The victory may have been especially sweet for Sonect, whose Best of Show award-winning demo was also the company’s Finovate debut. The Switzerland-based start-up offers what it calls “the world’s first social cash network” that enables consumers to access cash without having to visit a bank branch or ATM. Sonect offers merchants the ability to grow their business via increased traffic and gives financial institutions a way to extend their ATM networks without the cost of additional hardware.

The Best of Show win was also a first for Horizn. The company, which made its Finovate debut three years ago at FinovateEurope, offers a platform that helps employees and customers maximize the opportunities of digitized financial services. Horizn uses simulator microlearning, as well as gamification and advanced analytics, to promote digital adoption across channels.

And last but not least, a special tip of the hat to Dorsum, Glia, iProov, and W.UP, all of whom won Best of Show honors at FinovateEurope for a second year in a row.

Here’s a round up of recent news from our Finovate alumni.

Larkyenters reseller agreement with Access Softek.

Bison Bank in Lisbon, Portugal selects PSD2-ready software from ndigit.

OurCrowdexpands focus on growing early stage tech companies.

Finovate Alum Features and Profiles

eToro’s Evolution – Social trading and investment platform eToro has never been one to stand still for very long. The company’s development cycle is fast enough to make even the most sprightly fintech jealous.

Lending Club Snaps Up Radius Bank for $185 Million – When Lending Club was founded in 2007, the startup aimed to serve as a place to help borrowers avoid dealing with banks. In a somewhat ironic move today, that same startup is becoming a bank itself.

The 100 million members of Credit Karma will soon have access to more than just tools to better understand and improve their credit scores. The company announced this week that it is launching a new, high-yield savings account with no fees, no minimums and an initial rate of 2.03%. Credit Karma added that it will leverage its partnerships with as many as 800 banks to find and switch to those institutions offering the best rates on cash.

“We spent the first 12 years focusing on helping Americans manage their debt,” Credit Karma CEO and founder Ken Lin said. “We want to make savings accessible to every American in the same way we have with credit scores. We look forward to helping our members grow their money with Credit Karma Savings.”

Credit Karma will facilitate the opening and managing of the savings accounts, while the funds themselves will be kept and insured by FDIC-licensed partner MVB Bank to the tune of $5 million. The current rate offered by Credit Karma Savings is more than 20x the national average. The solution will be available via the Credit Karma app, and members can begin signing up for the new feature on October 28.

“When we built Credit Karma Savings, we wanted to develop a product that made opening a savings account as easy as possible for our members,” Credit Karma General Manager of Savings and Tax Jagit Chawla said. “We’re also making it possible for members to see the power of high-yield savings with our savings simulator, which shows how your money could grow over time.”

The move by the company comes as more fintechs are focusing on savings solutions as a way to add value to their personal finance or roboadvisory offerings. Companies like MaxMyInterestannounced a few weeks ago that it is adding a high-yield checking account to its high-yield savings option. Other fintechs in the wealthtech space, such as Betterment and Wealthfront have also introduced high-yield savings options. We took a look at the way fintechs are innovating on the savings side in our feature by senior analyst Julie Muhn: The Race is On in the High Yield Savings Game.

Founded in 2007 by Ken Lin (CEO) and headquartered in San Francisco, California, Credit Karma demonstrated its technology at FinovateSpring 2008. One of Finovate’s earliest alums, the company began the year with news it had been added to the Forbes Fintech 50 roster of the most innovative companies in fintech.

Credit Karma has raised $868 million in funding. The company includes Silver Lake Partners, SV Angel, QED Investors, CapitalG, and Susquehanna Growth Equity among its investors.

Credit KarmaUnveils New High Yield Savings Accounts

Finovate Global: PayPal Goes to China; Dubai Named Top Ten Global Financial Center

Around the web

Tradeshift to implement QEDIT’s privacy solution to preserve the full privacy of transactions.

Pendo Systemsannounces a new strategic partnership with Market Alpha Advisors.

Meniga to collaborate with Nordic Innovation House in Singapore.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

A baker’s dozen of Finovate alums has been honored this week with spots on the 2019 Forbes Fintech 50, an annual aggregation of what the editors called “the most innovative companies in fintech.”

“Recognition as a leading innovator in fintech is tremendous validation for the hard work we’ve done at Marqeta to open the industry up to the possibilities and opportunities of modern card issuing,” company CEO and founder Jason Gardner said. Marqeta is among the 20 companies to make its first appearance on the Forbes Fintech 50 roster.

Also earning their first appearances on Forbes Fintech 50 roster are New York based mobile investment platform Stash and San Francisco supply chain payments innovator Tradeshift.

“Very excited to be included in the 2019 Forbes Fintech 50!,” Stash tweeted once the news was released at the start of the week, “Monday = made.”

“We made the list!” Tradeshift tweeted this morning.

Summarizing this year’s selection of top fintechs, the editors noted that while 19 out of the 50 fintechs featured are unicorns with valuations of more than $1 billion, a nearly equal amount – 20 startups – are making their first showing on Forbes top fintech list. The two areas where newcomers were more prevalent, according to the editors, were payments technology and startups serving the un- and underbanked.

Just a month after unveiling its new auto insurance tool, financial health company Credit Karmaannounced it is once again expanding– this time across country borders.

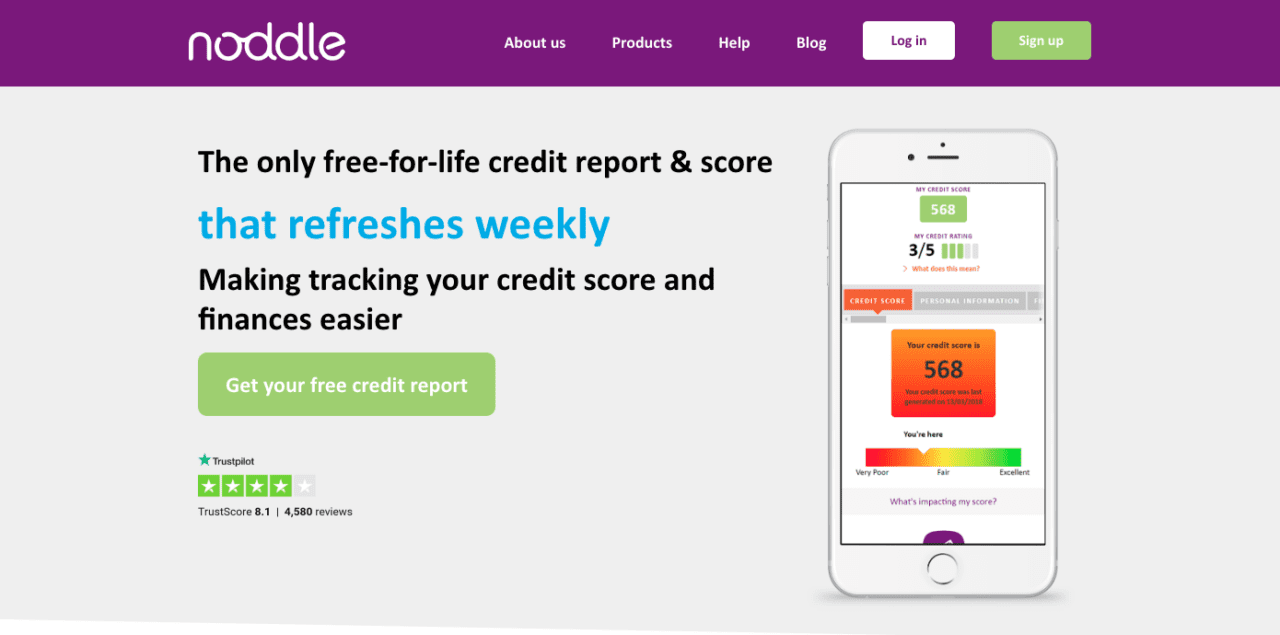

Prompting this move is the San Francisco-based company’s acquisition of Noddle, a startup headquartered in the U.K. that offers users free access to their credit report. Credit Karma made the purchase from TransUnion, which received Noddle as a part of its purchase of CallCredit for $1.4 billion in April of this year. The financial terms of the agreement are not disclosed but it appears to be purely cash-based; TransUnion is not taking any stake in Credit Karma. The deal is expected to close later this year or early next year.

“Noddle’s similar mission and history as the first provider of free credit information in the U.K. made this a clear decision for Credit Karma,” said Credit Karma’s VP of International, Valerie Wagoner. “We’re confident our depth of experience working across data providers along with banks and lenders will accelerate the number of services we provide to help consumers make the most of their money.”

Noddle’s 35+ employees will join the Credit Karma workforce of more than 700. Credit Karma has “immediate plans” to expand its team in the U.K., and aims to “more than double” the U.K. team– which will be based in London and Leeds– over the next year. The acquisition includes Noddle’s employees, technology, and clients– more than 4 million of them. This number boosts Credit Karma’s existing North American user base which currently sits at more than 85 million members.

Founded in 2007, Credit Karma CEO Ken Lin demonstrated the company’s platform at FinovateSpring 2009, when the company had just five employees. Since then, Credit Karma has finalized five acquisitions, making today’s purchase of Noddle its sixth. After receiving a $500 million secondary investment round in March, the company boosted its valuation to $4 billion.