This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

If you’re unfamiliar with blockchain-based payments company Sila, it’s worth checking out. The Oregon-based company has an API that offers what it calls Infrastructure-as-a-Service. Overall, Sila helps companies authenticate consumers via a partnership with Alloy, connect with consumer bank accounts via a partnership with Plaid, and move money via the blockchain.

So why is 2021 the breakout year for Sila? The answer can be found in two words: digital wallets.

The pandemic has changed how we think about in-person payments. Germ-riddled cash has fallen out of favor and consumers have adjusted their habits to seek out contactless transactions where possible. One side effect of this has been the uptick in digital wallet usage, both among consumers and merchants. According to Fast Company, mobile payments are expected to surpass both cash and credit card payments (based on transaction number) in 2020.

This has prompted even more investment in digital wallets, which used to be looked at as fintech’s tried-and-failed experiment of 2012. However, not only have PayPal and Google lined their digital wallet offerings with new tools, partnerships, and redesigns; individual retailers are getting in on the game, also. Convenience store 7-Eleven, for example, launched an in-app wallet earlier this month.

Here’s where Sila comes in. All three of its capabilities– authentication, bank account integration, and payments– come together to enable companies to create their own in-app, white-labeled digital wallet. While many food service chains have already launched digital wallets of their own, there is still much room for growth in the digital wallet space in 2021.

Sila was co-founded in 2018 by Shamir Karkal, one of the entrepreneurs who co-founded Simple in 2009. There, he was responsible for integrating the challenger bank’s system into BBVA after it was acquired by the mega bank in 2014 for $117 million. Karkal now serves as Sila CEO.

Sila raised $7.7 million earlier this year. The company’s clients range from startups to established businesses working in finance, insurance, real estate, and blockchain.

Apple launched its newest iPhone, iPhone 12, earlier this month. While many of the new features were expected, such as 5G and a refreshed design, there was one aspect on the iPhone 12 Pro that caught my eye– LiDAR.

LiDAR stands for light detection and ranging and has been around since 1961. So while the technology in and of itself isn’t new, many of the applications it’s used for are cutting edge. Take self-driving cars, for example. Self-driving cars rely on LiDAR to map the surrounding area by measuring distances of nearby objects using light rays.

So with such a powerful technology now placed into the hands of everyday consumers, how can fintechs put their developers to work to leverage the technology? Here are a handful of applications the fintech sector might be able to use iPhone 12 Pro’s LiDAR for.

Mortgagetech

With COVID keeping us socially distant, many lenders are waiving home appraisals for real estate transactions. While this may benefit the homeowner by saving them $500 or more on the appraisal, the lender, which must rely on third party data from Zillow or Trulia, may be at a disadvantage when it comes to estimating collateral values.

The LiDAR on the iPhone 12 Pro may be able to bridge the gap with its room-mapping technology. Combined with AI and machine learning technologies, computers may be able to estimate a home value more efficiently based on a home’s 3D mock-up created by LiDAR.

San Francisco-based Cape Analytics already offers a service like this. The company provides intelligence on the risk of a property for remote buyers and lenders. However, the service is limited to property exteriors.

Insurtech

When it comes to underwriting home insurance policies, the process relies heavily on input from the homeowner. This honor system offers plenty of room for error. Not only may the homeowner incorrectly enter the square footage, they also may not know the difference between flooring types and other important details.

Once again, this is an opportunity for iPhone 12 Pro’s LiDAR room-scanning capabilities. The map may not only help insurers underwrite the home itself, but may also be able to help renters determine the appropriate amount of insurance on their belongings.

Canvas app by Occipital already offers this technology for LiDAR-enabled iPads (11-inch iPad Pro 2nd Generation and 12.9-inch iPad Pro 4th Generation). The company plans to launch room-scanning for iPhone 12 Pro soon.

Security

Using facial recognition for authentication is so commonplace these days that most consumers– even those of older generations– are familiar with how it works. Unfortunately, some consumers who have tried to use facial recognition to log into their account may also be familiar with the technology’s shortcomings. For example, I was originally excited to enroll in my bank’s facial recognition login process when it came out a few years ago, but became frustrated when the technology stopped recognizing my face just weeks later.

With the LiDAR in iPhone 12 Pro promising enhanced photos, false negative issues like this could be less common. This is especially true in low-light photos, where the LiDAR captures more detail. Per Apple’s website, “Night mode comes to both the wide and ultra wide cameras, and it’s better than ever at capturing incredible low-light shots. LiDAR makes night mode portraits possible. And the wide camera lets in 27 percent more light, for greater detail and sharper focus day or night.”

The enhanced facial detail in selfie photos can not only reduce consumer frustration with false negatives, but also has the potential to augment security by reducing false positives, as well.

Across sectors

One of the most versatile capabilities the addition of LiDAR brings is upgraded augmented reality (AR). LiDAR technology allows for better object occlusion, meaning that virtual objects can now appear more real by disappearing behind real objects.

While versatile, however, AR brings little value to banks and fintechs beyond entertainment and novelty. The best use cases for AR seem to be for gaming and interior design. While the fintech sector showed a bit of hype around AR and mixed reality in 2015, there still hasn’t been much value-added development in the area.

However, augmented reality is still worth keeping on the fintech radar. This is especially true as social distancing measures remain in place and people try to find entertainment online and in the virtual realm.

The following is a guest post from RJ Sherman, VP of Innovation, Citizens Bank.

The word innovation is often thrown around casually to describe anything new that an organization is doing. However, for an organization to be truly innovative, it must adopt an “innovation mindset.”

Broadly, this means the organization needs to: take an empathetic approach to customer research to fully understand the customer’s needs; think longer term to identify potential disruptors that are further out on the horizon; and “test and learn, fast and cheap” by quickly exploring new ideas in a calculated manner to understand their value.

Innovation is more than simply creating new products or exploring emerging technologies. Innovation means acting on ideas that accelerate growth and challenge the status quo.

Here are five specific ways an organization can foster innovation:

Focus on the customer experience

Innovation starts with a deep and nuanced understanding of the customer journey and the associated pain points. Innovating for the sake of innovation doesn’t work – instead, use your customer’s pain points as a ‘North Star’ and design a compelling offering around them. Don’t be afraid to iterate in partnership with your customers (the solution is for them, after all). Despite the pandemic, there are still many ways to collaborate and co-create with customers, it just requires us to be more creative with how we conduct research.

Take a balanced approach to building the innovation portfolio

A balanced innovation portfolio is made up of opportunities from all areas of the business, including internal (organization-facing) and external (customer-facing) opportunities. This is critical as it signals to colleagues that all aspects of the business play a role in positioning the organization to win in the future. Continuously monitor your balance and partner with executive leaders across the organization to identify and explore strategically aligned opportunities (especially in underrepresented business areas).

Partner with fintechs when and where appropriate

While fintechs can pose a threat to financial incumbents, there is a significant opportunity for banks and traditional financial institutions to join forces to better serve the customer. Fintechs have a significant advantage when it comes to designing great customer experiences, but lack the customer relationships, scale, expertise, or risk management muscle needed to operate as broad-based financial services institutions. Fintechs can help power and accelerate a smart, data-enabled strategy, and offer a quick and relatively low-risk way to support business strategies.

Create the appropriate organizational mechanisms to explore early stage ideas

Citizens is investing in innovation using an Innovation Fund as part of its annual Tapping Our Potential (TOP) program. The fund operates like an internal venture capital firm, placing small-scale investments in colleague ideas. It is a great way to generate a grassroots movement around innovation and invest in the ideas of colleagues.

Encourage idea generation from everyone in the enterprise

When someone asks me “how big is the innovation team at Citizens?” I say 18,000 colleagues because every person at our organization has a role to play in innovation. Encouraging colleagues to participate in innovation begins at the top and, if done successfully, colleagues will buy-in and it will be embedded into everything you do. That way, when it comes to evaluating new opportunities or reimagining traditional business lines, innovation will always have a seat at the table.

To sum up, there isn’t a single “one size fits all” innovation model that will work for every financial institution to bring new ideas to life. Instead, leaders must create a bespoke solution for their organization, establishing mechanisms to leverage the cumulative power of their colleagues to identify and solve for the most pressing customer problems.

It is a truism that many of our greatest technological innovations have come as a result of trying to empower people challenged with physical limitations. Whether the circumstances are sensory, mobility-oriented, or cognitive, the role of technology for many of us is to make the phrase “differently-abled” something more than a politically-correct euphemism.

The rise of mobile banking itself has been a tremendous boon for many disabled customers, rendering unnecessary those often-expensive, time-consuming, and potentially dangerous regular visits to physical bank branches. Technologies that turn text-into-speech or that enable speech to drive digital processes have revolutionized access to financial services for those with sensory limitations. Even more modest innovations that enable seamless debit card spending controls and transaction monitoring are valuable tools not just for small business owners, but for caretakers of adults with limited cognitive capacity, as well.

In financial services, there have been even more focused efforts to serve the adults with disabilities. One is to build institutions that are dedicated to serving populations that have been overlooked in general because of “able-ism.” Purple is a challenger bank that was launched over the summer by a company called youBelong, who built the first social network for “people with special needs.” The bank is the evolution of youBelong’s mobile bank for families with special need children, youBelong Cash, and emphasizes financial literacy and education as a strategy for helping people with disabilities enjoy security and independence.

Founded by CEO John Ciocca, Purple offers a digital savings account with no hidden fees and no minimum balance. Account holders can set up their accounts to receive any Social Security Insurance and Disability payments they are eligible for. Access to PFM features such as money transfers and transaction tracking are included in Purple’s banking app. The accounts come with a Purple Mastercard Debit card, and Purple donates a portion of its revenues to the Special Olympics with every card transaction.

Among fintechs, True Link Financial is a company that has dedicated itself to improving the financial well-being of people with disabilities as well as vulnerable older adults. Payment cards that can be administered by a responsible family member or guardian on behalf of an intellectually-challenged adult, for example, are among True Link’s offerings. The company announced a $35 million Series B round over the summer and its founder and CEO, Kai Stinchcombe, highlighted the way the platform can serve people with disabilities.

“When we launched the True Link Card, it quickly became clear that its features could protect a wider range of people who weren’t being served by traditional financial institutions,” Stinchcombe wrote. “We found that people with disabilities and individuals in recovery from addiction could use our product to meet their unique needs and circumstances.”

Other Finovate alums – from Best of Show winner Golden to Eversafe – also have platforms geared toward helping vulnerable seniors that can be similarly leveraged to benefit members of the disabled community and their families.

Still there are significant challenges. According to a Pew Research Center study from 2017, the rate of technology adoption among the disabled across age groups lags behind those without disabilities – and significantly so in some areas. The home broadband gap between seniors with disabilities and seniors without disabilities is more than 20%. The smartphone gap between non-seniors (ages 18 to 64) with disabilities and non-seniors without disabilities is 17%. If anything, the research suggests that an emphasis on not just the disabled, but disabled seniors in particular – where smartphone and home broadband adoption rates are below 40% – would go a long way toward helping the neediest among those with disabilities.

After a a deluge of new announcements during its hardware event last week, Amazon is coming to us with something new again this week.

The company revealedAmazon One, a contactless palm reading device to help users make a transaction in-store, present a loyalty card, or authenticate themselves for entry into a secure location.

Amazon is piloting the new devices in select Amazon Go stores, concept stores that offer consumers a checkout-free shopping experience by using AI to track what they place in their cart. The Amazon One terminals will be offered as an option for consumers to authenticate themselves upon entering the store.

There is a slight bit of friction involved. Upon arriving at the store, the shopper enters their credit card into the Amazon One terminal, hovers their palm over the device, and follows prompts on the screen that associate their card with their unique palm print. Shoppers can enroll with one palm or both.

After enrolling, shoppers can use their palm print to enter Amazon Go stores. In the coming months, Amazon One will be available at additional Amazon stores, as well.

“[W]e believe Amazon One has broad applicability beyond our retail stores, so we also plan to offer the service to third parties like retailers, stadiums, and office buildings so that more people can benefit from this ease and convenience in more places,” said Dilip Kumar, Vice President of Physical Retail and Technology at Amazon.

The tech giant cited a handful of reasons for using a palm print over other biometrics. First, unlike many facial recognition solutions, humans can’t identify a person by simply looking at the palm of their hand. Also, unlike facial recognition, Amazon One requires users to make an intentional gesture by holding their hand up in front of the device. And, of course, the palm reader is contactless, easing fears about virus transmission.

If you’ve been following fintech for any length of time you’re likely aware that Amazon isn’t the first company using contactless palm print biometrics. Both iProov and Redrock Biometrics have been working in the space since 2011 and 2015, respectively.

As biometric authentication methods rise in popularity, we’ll likely see palm prints being the body part of choice for authentication. That’s because, in addition to Amazon’s point regarding the ability to recognize others’ palm prints, it is also much more difficult to spoof someone else’s palm than it is to spoof their fingerprint of face.

I was pretty excited for my first ride in my nephew’s brand new Tesla. The car was a major upgrade from his previous vehicle: a Jeep with “character” that had both broken down and been broken into a few times too many. His visit – and the Tesla’s – also marked the first time my wife and I would have company over for dinner since the COVID-19 pandemic struck, so there was more than a little to look forward to.

And while the Greek burgers were good and the tzatziki and baklava even better, my ride in the brand new Tesla was … kinda underwhelming.

Admittedly the experience as a rider in a Tesla is not identical to the experience as a driver. But as I slowly emerged from my initial shock at the lack of ornamentation, the absence of anything even resembling a full service dashboard and began to appreciate the machine’s unnaturally silent acceleration, its “It’s-All-on-the-Tablet” functionality, and “front trunk,” it dawned on me just how dramatically Tesla had reduced the driving experience to its most essential features and then turned them up to eleven.

What does this have to do with banking?

My Tesla experience reminded me of the challenge of distilling customer experience into its most necessary aspects. This is what drives innovation in everything from PFM apps that provide account balances without requiring login to mobile brokerages that cut out the stock market’s most hated middle man – commissions. Yet what is a trifle to one customer can be a can’t-do-without attraction to another. In the same way that I found myself in my nephew’s Tesla actually missing the dials, buttons, and other dashboard gizmos that had once defined automotive technological sophistication, so will many consumers find the leanness of new digital banks, for example, and perhaps even the trend away from what might be called “the human touch” in financial services to be a less appealing customer experience rather than a more fulfilling one.

In this way, I wonder if it is helpful to think of two innovation tracks for banks and financial services. One track is the one we spend most of our time reading and thinking about in fintech circles: the digital-first if not digital-only mobile bank that caters to the young, the mobile and, ironically, to both the hyper social connected individual and the asocial consumer who believes that automated checkouts at the grocery store are the best thing since sliced bread. Here the innovations are mostly technological, leveraging AI, machine learning, Big Data, and other leading technologies to provide more data, more services, faster, with a premium on seamless, frictionless, no frills interactivity.

But there is – or at least could be – another bank. And while it is digital, as well, and provides many if not most of the same basic financial services as any other bank, this bank focuses more on responding to the personal and social worlds of its customers. This bank puts financial inclusion and wellness at the center of its mission, sponsoring and providing educational opportunities for members of the local community – including their children who are likely getting precious little financial education in school. In-person credit counseling and financial planning would also be a good fit for an institution like this, which would play a role in the private sphere of a community that is similar to the role a local library or post office plays in the public sphere. At more advanced levels, coursework and training for individuals looking for careers in financial services could be offered, as well.

Not necessarily 100% or exclusively brick and mortar, this truly community-based financial institution would provide a customer experience that would be very different from its all-digital cousin, but one that could be just as innovative by using technology to make finance and financial services easier to understand and easier to incorporate constructively in the average working and middle class person’s life.

A couple weeks back I had a conversation with Andrew Besheer, Head of North America for Appway, about the rise of challenger banks. Our discussion centered around some of the data points in Ron Shevlin’s piece, The Online Banking Insurgency of 2020, published in Forbes last month.

One of the questions that came up was if this surge in new challenger bank accounts is an accident of digital transformation? In other words, are Millennials and Gen Z consumers gravitating towards challenger banks because their websites appear more digitally savvy?

At its core, this is a chicken-and-egg question. Are challenger banks successful because their tech-first approach satisfies consumers? Or are underserved consumers driving challenger banks to create new products and services that banks are unable (or unwilling) to offer?

First, its important to recognize that both challenger banks and incumbents know their target market. That is, the challenger banks are catering to an audience looking for a different bank experience than the one that appeals to their parents.

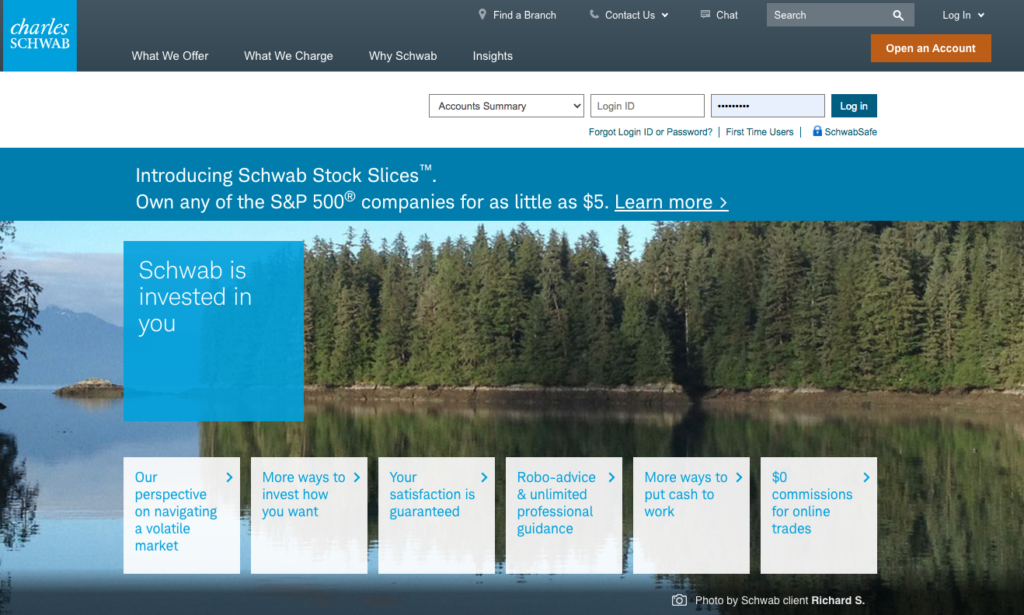

To answer this question, first, take a look at the outward appearance. Traditional banks’ websites are text-heavy, with long-winded fine print, and are intimidating enough to drive away less experienced consumers. Conversely, challenger banks use colloquial language and present websites that look simple and transparent. As an example, take a look at Charles Schwab’s website:

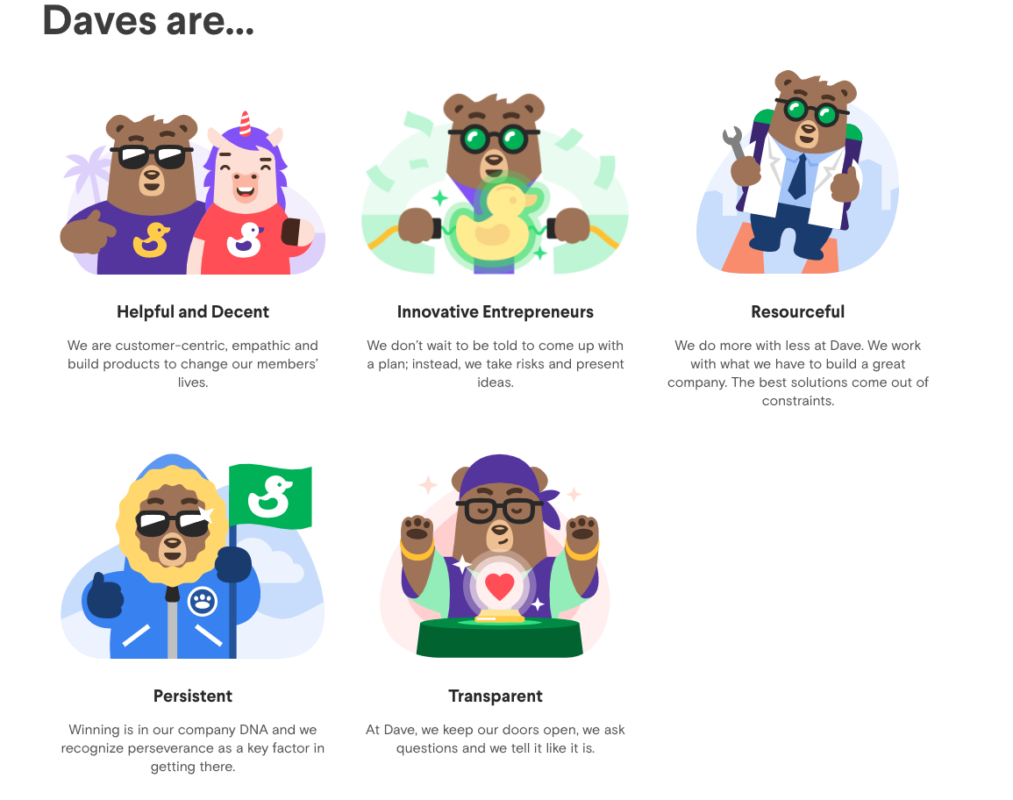

And now look at Dave’s:

Both are relatively technologically and digitally advanced banks, but they are appealing to two entirely different demographics.

Taking a look under the surface, the products and services each bank offers are also different. Schwab’s are heavily geared toward investing and trading, while what Dave offers– paycheck advances and credit building tools– seems to center around keeping its users afloat.

In the end, the two approaches are perfectly suited for users on opposite sides of the generational spectrum. My father and grandfather would never bank somewhere that had a cartoon as a mascot. And younger, Generation Z users don’t trust incumbent banks’ language and apparent lack of transparency.

Now, to answer the question, “are Millennials and Gen Z consumers gravitating towards challenger banks because their websites appear more digitally savvy?” The answer is no. Challenger banks are built from the ground up to entice this generation of users. And while the banks’ advanced digital capabilities help to draw users in, they are not the sole reason younger, tech-savvy users choose them.

You can check out the full interview, where Besheer and I delve further into the challenger banking conversation, on Appway’s website.

If there are any lingering doubts about the power (and popularity) of the Buy Now Pay Later (BNPL) movement, installment payments platform Splitit has 71.5 million reasons to cast those doubts aside.

The New York-based company, which made its Finovate debut as PayItSimple in 2014, announced that it has raised $71.5 million in a private placement and share purchase plan (SPP). With institutional investors such as Woodson Capital Management, the company plans to use the capital to “accelerate sales and marketing, plus (make) further investments in product and technology” according to a statement. Splitit boasts more than 1,000 ecommerce merchants using its technology, and 300,000+ shoppers with an average order value of $893.

Splitit’s fundraising comes as the company reports record Q2 growth, including processing more than $65 million in merchant sales volume, and growth of 1.76x quarter over quarter and 2.6x year over year. In discussing the company’s success, CEO Brad Paterson credited a new willingness on the part of consumers to “maximize their existing credit to preserve cash flow” while at the same time not incurring additional new debt.

Paterson also noted that while the COVID-19 crisis has helped move digital transformation in ecommerce toward the top of the agenda, it was important for those involved in payments to make it easier for merchants to accommodate their customer’s cash management requirements.

As such, it’s hard not wonder if, once again, crisis is responsible for accelerating innovation. After all, one of the initial innovations in retail, the layaway program, emerged during the Great Depression as a way to maintain at least a minimal level of consumption of non-essential goods during a severe economic retraction. By enabling customers to pay for items in small increments over time and then receive those items once they had been fully paid for, the growing retail economy was able to survive an extended period of historically low demand.

The buy now pay later phenomenon is layaway in reverse, allowing customers to gain the benefits of the purchase immediately and moderating the impact of the cost by paying for that purchase over time. But the goal – to accelerate consumer activity and expand the ability of people to spend – remains the same. The only difference is that layaway tended to disappear once credit cards became ubiquitous, while buy now pay later appears to be rising at a time when we are realizing that affordable consumer financing might not be as ubiquitous as we thought.

For Finovate fans, Klarna has been the pioneer in the Buy Now Pay Later space, with fellow alums like Sezzle also earning recognition for its interest-free buy now pay later option. Founded in 2005 and 2016, respectively, both companies are reminders of how fintechs have been providing consumers with alternative financing options well before the coronavirus hit.

That said, it is clear that COVID-19 has stimulated interest in Buy Now Pay Later options. The Business of Finance reported earlier this week that BNPL had become “fashion’s go-to during the pandemic.” Also this week, American Express announced that it would extend its buy now pay later service to more of its cards. The Wall Street Journal featured Australian Buy Now Pay Later specialist Afterpay at the beginning of this month in the wake of the firm’s announcement that it had signed up more than 1.6 million U.S. users since the onset of the coronavirus in March. And Shopify announced this month that merchants on its platform would have access to BNPL financing from installment payment company Affirm. Affirm looks like it is ready to maximize the Buy Now Pay Later moment with an initial public offering, according to reporting in the Wall Street Journal.

Even the big banks are getting into the Buy Now Pay Later game. Goldman Sachs has introduced a new, installment payment feature called MarcusPay – in partnership with JetBlue Airways – as part of a bigger “build-out” of its Marcus by Goldman Sachs digital banking platform. This week, Citi partnered with Amazon to launch its own BNPL offering Citi Flex Plan.

It’s been five years since eBay and PayPal split into separate companies – which means the five-year operating agreement that maintained the firms’ payments relationship in the years since the breakup is about to run out.

This week eBay announced that it is now ready to expand the managed payment system that will take PayPal’s place. Developed in partnership with payments provider Adyen, the new payment system is being used by 42,000 sellers – with more than 255,000 additional merchants who the company said will be activated by the end of the year. eBay has processed more than $4.7 billion in volume in the U.S. and Germany via its managed payments offering, and the company reported that sellers using managed payments have saved $17 million in transaction fees. eBay President and CEO Jamie Iannone praised the momentum behind managed payments, and said he expects it to “deliver $2 billion in revenue and $500 million of operating income in 2022.”

eBay is currently managing payments in five countries – the U.S., Canada, Germany, Australia, and the U.K. – and plans to expand the program to all countries where it operates.

For buyers, eBay’s managed payments provides a more flexible checkout experience with more payment options. Sellers benefit from a simplified process – involving one company (eBay) rather than two (eBay + PayPal) – that provides for easier reconciliation, faster service, and more effective support when issues arise. The company quoted one 20-year veteran eBay merchant from Germany who has been using managed payments since the spring. “I don’t care how the payment goes,” she said, “the main thing is that the customer buys and pays and my account fills up.”

VP of Global Payments Alyssa Cutright added that the offering was a win for both buyers and sellers that provides a simpler, more modern managed marketplace. “By managing payments, eBay is taking control of its own destiny,” Cutright wrote. “We are investing in our buyers and sellers, creating an integrated end-to-end platform, and enhancing the eBay experience by breaking down and removing complexities for our customers.”

Adyen, eBay’s payments partner, is based in Amsterdam, The Netherlands, and was founded in 2006. Companies ranging from Facebook and Uber to Microsoft and Singapore Airlines rely on Adyen’s technology to deliver seamless, friction-free payments across mobile, online, and in-person channels. The company, which processed $278 billion (€240 billion) in volume last year, is publicly traded on the Euronext and has a market capitalization of $47 billion.

With a growing consciousness worldwide on the topic of systemic racism, corporations are doing everything from pro-diversity affirmations (arguably not enough) to mass board resignations (arguably far too much) in order to stay (or get) on the right side of public opinion on a key issue for many of their customers.

We took a look at some of the ways those fighting in favor of a more inclusive financial services and fintech sector can learn from the successes of the women’s movement a few days ago. Here, we offer a few more specific examples of not just what financial institutions can do to help promote ethnic diversity in their companies, but also what financial institutions and fintechs are actually doing.

Celebrate Diversity

With Juneteenth taking place this Friday, some financial institutions have decided to treat the date – which marks the moment African slaves in Texas in 1865 learned of the Emancipation Proclamation – as the official occasion many African Americans have always believed it to be. Fifth Third Bancorp and Truist Financial are among a number of companies that have elected to recognize Juneteenth as a holiday for their employees and customers.

“As we consider the tremendous significance of this day and what it represents, it also reminds us of how far we still must go to have equality and inclusion for all,” Greg D. Carmichael, chairman, president and CEO of Fifth Third Bancorp said earlier this week. “As we observe Juneteeth, each of us should pause, reflect, and contemplate its significance and what it meant 155 years ago, what it means today, and how we might take action to make tomorrow better for everyone.”

Fifth Third will close its offices early on Friday, shutting down at 2pm local time. And while a number of other major financial institutions have made similar commemorations, Fifth Third is believed to be the first FI to offer its employees Juneteenth as a paid holiday.

Show the Money

The $40 million Netflix CEO Reed Hastings and his wife Patty Quillin have announced they will donate to the United Negro College Fund, and a pair of historically black colleges Spelman and Morehouse, is an example of the kind of “put your money where your mouth is” act that many pro-diversity advocates have called for.

Some of the biggest financial services companies and banks in the United States have unveiled similar initiatives. Citi, for example, announced that it will direct $8 million to the NAACP Legal Defense Fund, the Lawyers’ Committee for Civil Rights, the National Urban League, and the National Fair Housing Alliance.

Also pulling out the checkbook in the name of diversity are firms like Bank of America, which announced a $1 billion/four year commitment to help local communities of color at a time when the COVID-19 crisis is making a disproportionate impact on black and brown Americans.

“Underlying economic and social disparities that exist have accelerated and intensified during the global pandemic,” Bank of America CEO Brian Moynihan said earlier this month when the initiative was announced. “The events of the past week have created a sense of true urgency that has arisen across our nation, particularly in view of the racial injustices we have seen in the communities where we work and live. We all need to do more.”

People Who Need People

Honoring the past is important. And putting real resources to work to make opportunities possible for historically excluded groups is a critical component in achieving a more inclusive world. But, without putting too fine a point to it, the best way to promote diversity is to hire more diverse people.

Analysts looking at the barriers to increasing diversity have cited three chief hurdles: (1) finding diverse candidates to interview, (2) retaining diverse employees, and (3) getting diverse candidates past interview stage. And while the second two issues have a lot to do with the culture of a company, something that may not substantially improve until after diversity and inclusivity gains are made, the first challenge – finding good candidates – is one all companies and organizations should pledge to overcome.

For many companies, this may mean looking in typically overlooked places for otherwise untapped talent. Student organizations, including a very active African American collegiate and post-collegiate fraternity and sorority system, can be a an excellent way to reach today many of the people who will be leaders in their communities tomorrow. Diversity-oriented venture capital firms – such as Harlem Capital Partners, the Black Angel Tech Fund, and Base Ventures – are excellent sources for insight into black and brown entrepreneurship in the technology sector.

As Chamath Palihaptiya, venture capitalist and founder of Social Capital, wrote almost five years ago:

We need to recapture our potential and open the doors. Invite more people into the decision making: young people, Blacks, Latinos, females, LGBT and others who aren’t necessarily part of the obvious majority. Surround ourselves with a more diverse set of experiences and maybe we will prioritize a more diverse set of things. Maybe we will find more courage to do the hard things.

Half a decade later, many of us in the technology community in general and the fintech world in specific are still waiting. But it appears increasingly the case that, for now, our communities are ready to act.

Taxes, especially in the U.S., can be anxiety-inducing not only for consumers but also for small businesses. And even though this year’s tax filing deadline has been extended to July 15, the filing and payment requirements remain unchanged.

“The daunting task of gathering documents for a year that has passed is one that is difficult for small business owners, especially when they already feel overwhelmed at tax time,” said Lil Roberts, CEO and founder of Xendoo. “Coupling that pain point with small businesses feeling that federal tax is a “black box” and understanding how to maximize tax savings is also extremely frustrating.”

Fortunately, where there is a financial problem there is a fintech solution. There are many fintechs available to help both individuals and businesses not only understand their taxes but also to facilitate tax payment. Below, we’ve highlighted the top 10 tax-focused fintechs.

ANNA

ANNA offers a business bank account and mobile tax app that help merchants with their invoicing, expense tracking, and taxes. The company’s app reminds businesses about tax deadlines and helps them prepare by estimating how much they owe as they earn revenue. ANNA also has a team of accountants to help prepare and submit tax returns.

Avalara

Avalara offers tax compliance tools for a range of businesses. The Seattle-based company, which counts customers such as Pinterest, Adidas, and Bed Bath & Beyond, offers products to help companies calculate sales tax, gather data to prepare and file tax returns, as well as collect, store, and manage tax documents on behalf of the business. Avalara offers products tailored to specific businesses, including ecommerce, lodging, communications, and restaurants.

Credit Karma

In 2016, financial health company Credit Karmalaunched a free tax filing service. Interestingly, the company was recently purchased by TurboTax parent Intuit for $7 billion. In comparison with Credit Karma’s free service, TurboTax charges users anywhere from $60 to $120 for a federal return and $45 for a state return.

DAVO

DAVO launched in 2011 to be the ADP for merchants’ sales tax. In other words, DAVO automates the entire sales tax process on a business’ behalf. The company connects to the merchant’s point-of-sale technology to collect sales data and sets aside taxes on a daily basis. When sales tax is due, DAVO files and pays on the small business’ behalf.

Gusto

HR and payroll company Gusto has a robust set of services to make small business owners’ lives easier. The company automatically files payroll taxes and distributes I-9s, 1099s, and W-2s to employees. Gusto also helps businesses stay compliant by staying up-to-date on changing tax laws and doing all tax-related calculations on the business’ behalf.

Refundo

Refundo offers a suite of solutions to help tax preparers bring their operations into the digital age. Among the company’s products are mobile document transfers, audit assistance, tax preparation fee collection service, payment acceptance tools, and refund advance technology. At the end of the day, the company’s solutions not only make the tax preparer’s life easier, they make the lives of their taxpaying clients easier, as well.

RoamHR

With a mission to make self-employment easier, RoamHR automatically removes tax withholdings from users’ accounts once they get paid and places the funds into a RoamHR Tax Withholding Account. The company also offers tools that help users track deductible expenses, such as mileage, and helps them file their business taxes each quarter.

Taxnology

Taxnology has built a digital tax compliance center, a web-based solution to help businesses manage their taxes digitally. The company stores business’ historical tax data in the cloud so that it can be used for future cash flow planning and budget purposes or retrieved in the event of an audit. Taxnology is currently only available in Hungary.

Xendoo

Xendoo offers bookkeeping and CPA services that connect with businesses’ financial accounts to deliver monthly reports, business insights, and tax filing. Because Xendoo has a comprehensive view of the merchant’s financials, the company is able to provide tax consulting services, as well.

Xero

Cloud accounting software company Xero has been helping small businesses with their bookkeeping since it was founded in 2006. The company also offers solutions to help tax preparers who have Xero clients automate and customize tax-related tasks. For businesses who prepare taxes on their own, Xero offers tools to file taxes online, as well as prepare sales tax returns using software that leverages a company’s sales data to automatically calculate the taxes.

Roberts added one final thought for those businesses working toward that July 15 deadline. “For a smooth process, best practice is to have monthly bookkeeping done so tax benefits are being collected all year, and having books in order to make tax time more peaceful.” And during a pandemic, anything that can make a process more peaceful is worth doing.

There are two things that the COVID-19 crisis is teaching us. Be careful of what you touch. And be careful of who you are near.

Neither one is a good message for the future of cash nor the bank branch, two staples of 20th century financial life whose demise analysts and prognosticators have been anticipating for decades.

Could a global pandemic that forces society into “social distancing” prove to be the final straw that breaks the back of both our commitment to cash and what’s left of the bank branch?

Cash: The Irresistible Force

For all the innovations in digital payments, and the increasing adoption of these technologies by younger generations, the persistence of cash in modern economies has been impressive. In part, this is because technology has not yet been able to outperform cash where it performs best: convertibility, convenience, and anonymity.

Of late, however, one of cash’s biggest – and probably least considered – downsides has become impossible to ignore: cash is dirty. At the end of the day, regardless of whatever hero, politician, or artistic talent adorns it, cash is a slip of cotton paper passed from hand to hand, over and over again. In a article published in Scientific American three years ago, Dina Fine Maron noted:

The fibrous surfaces of U.S. currency provide ample crevices for bacteria to make themselves at home. And the longer any of that money stays in circulation, the more opportunity it has to become contaminated.

And bad news for those who limit their cash exposure to a “just couple of bucks” for tips and tiny purchases.

Lower-denomination bills are used more often, so studies suggest our ones, fives and tens are more likely to be teeming with disease-causing bacteria. Some of these pathogens are known to survive for months …

Countries around the world have already begun a coronavirus-induced assault on cash, with South Korea’s central bank both quarantining and even burning bank notes, as well as resorting to a “high-heat laundering process” to help stem the spread of the virus. Paper money has faced a similar fate in China, and even the U.S. Federal Reserve is getting into the act (albeit with currency imported from China).

Not everyone believes that COVID-19 will herald the beginning of the end of cash. Maybe it is because of doubts that, as dirty as cash is, paper money may not be a reliable transmitter of viral infection. Possibly, like young revelers at beaches in Florida well into last month, we are just too accustomed to our habits to change.

But again, the emphasis on which “we” is being discussed is probably what matters. While there is a tendency to equate people’s willingness to use digital payments as one of many options with a desire to use digital payment method exclusively, the generational trends away from cash are clear. For those who grow up in a world in which cash is increasingly under assault from one source or another, it may simply be the passage of time that ends up accomplishing what neither global pandemic nor technological innovation – combined – could not.

Branches: The Immovable Object

As thousands of traditionally on-premises employees find themselves working from home, businesses all over the world are seeing a version of themselves that is far less dependent on a brick and mortar presence – let alone multiple ones. In banking, where the value of the local branch office with lobby, tellers, and loan officers is hotly debated, it seems like the COVID-19 crisis will make the case for branches that much more of a challenge to make.

Although essential businesses that are allowed to remain open in most instances during the pandemic, banks have dramatically cut back on access to their physical locations. Often, as is the case with my bank, access is limited to a drive-through window – complete with gloved and masked teller who has you to sign your withdrawal receipt with a branded pen she asks you not to give back.

As someone who still regularly visits his bank branch – and has for decades – I actually found the experience no less impersonal than the ATMs I’ve avoided for years. Could our social distancing response to the coronavirus pandemic encourage a long-time branch-lover like me to stay away? Asked whether the COVID crisis will accelerate the trend toward fewer bank branches, KeyBank EVP and head of digital banking Jamie Warder told The Financial Brand’s Jim Marous that more “thoughtful consolidation” wouldn’t surprise him. But Warder suggested that the world still had a need for the branch, even as it “continue(d) to morph and become more digitized.”

Many innovations in the branch designed to accommodate a more digitally-savvy customer, for example, could survive the demise of the branch. Self-service kiosks that enable bank customers to perform a number of routine banking tasks without the intervention of a human teller could find homes in locations ranging from fitness centers to restaurants and other recreation hubs. The ubiquitous bank branch in any U.S. supermarket of even middling size is a reminder of how compatible these banking kiosks could be with a wide number of environments.

Unfortunately, those innovations that are geared toward making the branch itself a more enjoyable place to spend your time may struggle in the current public health climate. More luxurious accommodations – including addition of full-service cafes – could be a weak draw in a world in which we are conditioned to keep our distance.

The strain between distancing and the branch will be most acute for those who live in communities where the bank branch serves as the center of everyday financial activity. Often this consists of bill payments, check cashing, money transfers, but notably does not include short-term personal loans, a major source of financial activity in many of these communities. While a great deal of time is spent envisioning a Branch 2.0 that would appeal to the digitally-savvy and already well-banked, it may be the case that the future of the branch – to the extent that there is one – is best geared to the real needs of these communities above all others.