This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Slice (fka SlicePay), a millennial-focused challenger bank headquartered in India, raised $6 million in a pre-Series B financing round. The investment brings the company’s total funding to $27.7 million in combined debt and equity.

Gunosy led the round. Also participating were EMVC, Kunal Shah, Better Capital, as well as existing investor Das Capital.

According to Slice Co-founder and CEO Rajan Bajaj, the company will use the funds to acquire new users. In fact, Slice hopes to add 500,000 new customers within the next year. This is double the company’s existing active user base of 250,000.

Slice will also use the new $6 million to increase its workforce and explore banking partnerships to release co-branded cards.

Unique to Slice is its underwriting model, which is a key element in a country where customers are burdened with limited or no credit files. To help users build their credit, Slice offers a card that comes with a pre-approved credit line that offers installment loans, enabling users to buy now and pay later.

Slice is one of only a handful of challenger banks in India. Others in the subsector, including PayTM, Google Pay, and Walmart’s PhonePe, are all very large players. However, Slice seems to be fairing well. The company has been profitable since last year. And the simple fact that it raised funds in today’s economic environment where VCs are reluctant to invest speaks volumes of its potential.

“We believe Slice has a sustainable advantage as it has decoded young credit users’ demands and has built a deep understanding of credit risk and low-cost distribution using technology,” said Gunosy Director Yuki Maniwa.

Financial organizations are managing mass amounts of information on a daily basis.

Whether it’s a loan application, credit approval, or new customer records, sharing documents securely is key for effective task completion and departmental collaboration.

With a variety of document formats needed for each of these tasks, professionals must often switch from application to application to complete processes. Standard processes are often outdated and inefficient.

Discover how financial organizations can streamline their workflows and collaborate more effectively within their current applications.

For a year that began with Visa’s headline-making acquisition of Plaid, it seems almost poetic that near 2020’s midway mark, Mastercard would make a major fintech bid of its own.

The company has agreed to acquire Finicity, a real-time financial data and analytics provider and long-time Finovate alum, in a deal valued at nearly $1 billion. This figure represents a combination of the $825 million purchase price of the Salt Lake City, Utah fintech, as well as a potential earn-out for Finicity’s existing shareholders – subject to the company meeting certain performance targets.

“Since our founding, Nick Thomas and I have focused on developing industry-leading technology and building an organization that empowers consumers and organizations to better understand, manage, and use their financial data to improve their financial lives,” Finicity co-founder and CEO Steve Smith said. “Enabling people to access and control their data, while ensuring best practices to protect that data, will continue to drive tremendous innovation that increases financial literacy, inclusion, and health. This partnership with Mastercard helps us accelerate this mission globally.”

Mastercard President Michael Miebach cited open banking as one of the reasons for the company’s interest in Finicity. Referring to open banking as both a “growing global trend” and a “strategically important space,” Miebach praised Finicity’s ability to leverage open banking APIs to enable financial data and insights to streamline lending and mortgage processes, account-based payment initiation, and other PFM services. He also credited the company for its focus on the data rights of the consumer.

“(Finicity) shares our commitment to consumer-centric data practices, ensuring consumers have a say in how and where their information should be used,” Miebach said.

Founded in 2000, Finicity provides financial data APIs, credit decisioning tools, and financial wellness solutions that help financial institutions and fintechs better serve their customers. The company’s technology helps power solutions like ExperianBoost and Rocket Mortgage from Quicken Loans. Named a Best Place to Work in Fintech by American Banker for the last three consecutive years, Finicity began 2020 partnering with SaaS-based marketing automation, CRM, and POS solution provider for banks and mortgage companies, Volly.

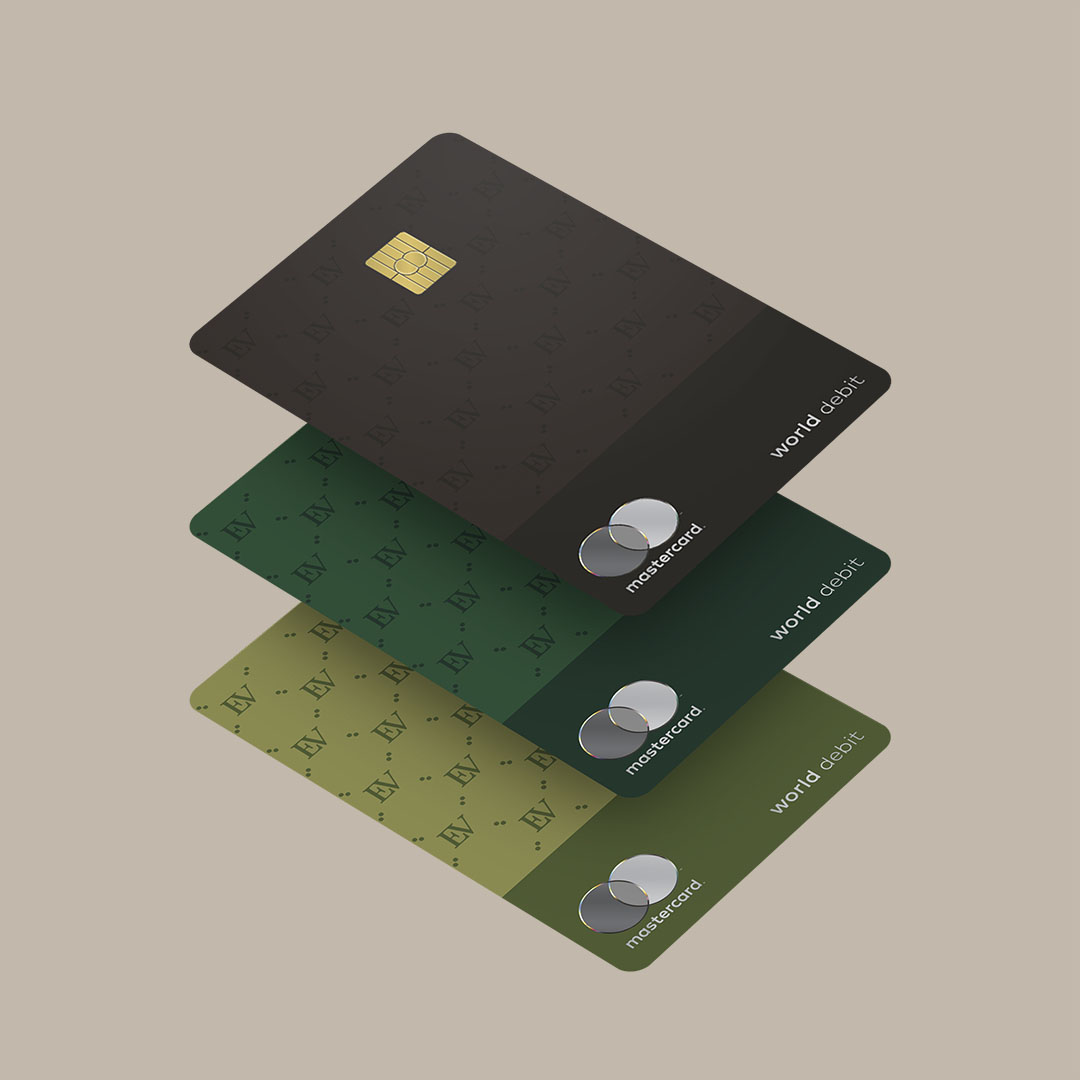

Women-focused wealthtech firm Ellevest unveiled its newest offering today. The company, which was founded by former Merrill Lynch CEO and former Citigroup CFO Sallie Krawcheck, has expanded its online investing platform to launch banking services.

“At Ellevest, our mission is to get more money in the hands of women+ — because we know that everyone deserves the opportunity to build wealth, and that nothing bad happens when women have more money,” the company announced in a blog post. “Today, we’re launching the first-of-its-kind money membership designed to get more money in the hands of women+.”

The new banking services are available with an Ellevest membership, which ranges from $1 per month for the Essential plan to $5 per month for the Plus plan, and $9 per month for the Executive plan. All membership options include banking services, investing opportunities, and educational resources. Other services include personalized retirement recommendations and multi-goal investment accounts.

Ellevest’s fashion-forward debit card

Members can access two accounts– one for spending and one for saving. The checking account comes with a World Debit Mastercard connected to an FDIC-insured account. The accounts boast no hidden fees, no minimum balance requirements, no transfer fees, no overdraft fees, and ATM fee reimbursements.

In the competitive world of challenger banks, none of these features stand out. However, Ellevest has created a bit of a cult following with its women-focused approach and content generation. The company has 180,000 followers on Instagram, which is 10x the number of followers that BBVA-owned Simple has, and more than Revolut, Monzo, and N26.

Ellevest’s gender-filtered approach further differentiates it when it comes to investing. The company’s personalized investment portfolio “includes a gender-aware investment algorithm that factors in important realities like pay gaps, career breaks, and average lifespans.”

Today’s announcement isn’t the first time a wealthtech platform has broadened its offerings to become a challenger bank. Betterment, Wealthfront, SoFi, M1 Finance, and Personal Capital all offer online-only checking accounts.

Ellevest was founded in 2014 and is headquartered in New York. The company has raised $77.6 million.

It’s the FraudTech day of the Finovate Fintech Halftime Review, and we welcome Jeff Tinsley, CEO of MyLife to talk fraud management and prevention and how MyLife can be used by financial institutions to educate and add value for their consumers.

David Penn, our own Finovate Analyst, asks what sort of things go into creating a Reputation Score, and how MyLife protects people from fraud?

Watch the full interview.

Find out more about MyLife and get in touch with Tim ([email protected]) for any questions or partnership inquiries.

In a brief statement shared on Monday, the Wilmington, North Carolina-based company reported that it had publicly filed a registration statement on Form S-1 with the U.S. Securities and Exchange Commission for their proposed initial public offering. nCino made its Finovate debut at FinovateEurope in 2017.

The company’s announcement did not disclose the number of shares to be offered, nor the price range of the offering. Renaissance Capital reported that nCino is seeking to raise $100 million. The company expects to trade on the Nasdaq Global Select Market under the ticker “NCNO.”

Underwriting the IPO are Bank of America Securities, Barclays, KeyBanc Capital Markets, and SunTrust Robinson Humphrey.

nCino’s Bank Operating System, built on the Salesforce platform, provides financial institutions of all sizes with an end-to-end banking solution that enables them to deliver the kind of digital experience banking customers have come to expect. The platform combines customer relationship management, loan origination, workflow, enterprise content management, as well as business intelligence and reporting, all in a single, secure, cloud-based environment. On average, financial institutions using nCino’s Bank Operating System have enjoyed a 40% decrease in loan closing time, a 92% reduction in servicing costs, and a 127% increase in account opening completion rates.

Founded in 2012, nCino has raised more than $213 million in funding. The company reported revenue growth of almost 50%, reaching $44.7 million, for the quarter ending in April. nCino also reported revenue of $138.2 million in its most recent fiscal year, ending in January. This year, the company has forged partnerships with Alterna Bank, a subsidiary of Alterna Savings and Credit Union Limited, and with Swedish SME lender Yourban. Additional partnerships announced in the first half of the year include collaborations with Fulton Bank and Black Hills FCU. Pierre Naudé is President and Chief Executive Officer.

In the middle of the first month of the year, one of the biggest names in the payments business acquired one of the most innovative fintech infrastructure companies in the industry, in a deal valued at more than $5 billion.

Six months later, Visa’sacquisition of Plaid almost seems like news from another time.

The arrival of the coronavirus to virtually every corner of the globe – and the worldwide response to the killing of a black man in police custody in the U.S. – have sent shock waves through the fintech industry – as they have the rest of the world. Now, at the same time, fintech is engaged in both the struggle to help businesses and consumers cope with the closures and shelter-in-place restrictions of the COVID-19 crisis, as well as the challenge of correcting decades of discriminatory practices against African Americans and members of other underrepresented ethnic groups. As we approach the middle of 2020, fintech is facing different kind of crisis that, while not of its own making, will require a response that is uniquely tailored to the world it operates in.

This is a world that is both heavily technical, relying on the latest innovations in machine learning, artificial intelligence, and distributed ledger technology, while simultaneously pledging to bring the benefits of 21st century financial services to the underbanked and underserved populations of both post-industrial and developing economies. This is a world that has grown tremendously through the contributions of people from diverse backgrounds, representing cultures from almost every corner of the globe. Yet, at the same time, it is a world that is still struggling to achieve true gender and ethnic diversity, particularly in the C-suite and in the boardroom.

There are many ways to value an industry: the quality of the goods it produces; the entertainment, education, or simple well-being its services provide; even just the degree of pure, gee-whiz innovation the industry may deliver, often seeming to grant us what we want even before we summon up the nerve to wish for it.

But as the fintech industry edges closer, inexorably, toward maturity, it now finds itself increasingly judged on the kind of criteria Corporate America – often to its own surprise and bewilderment – can find itself judged on from time to time. This is a judgement that has less to do with what Corporate America makes and sells, and more with who Corporate America is and what it values.

Both the global public health crisis and the renewed determination to fight racial inequality are providing fintech as an industry with an opportunity to show the world just what it’s made of. As we move into the second half of this historic year, I am hopeful and optimistic that fintech will rise to the challenge.

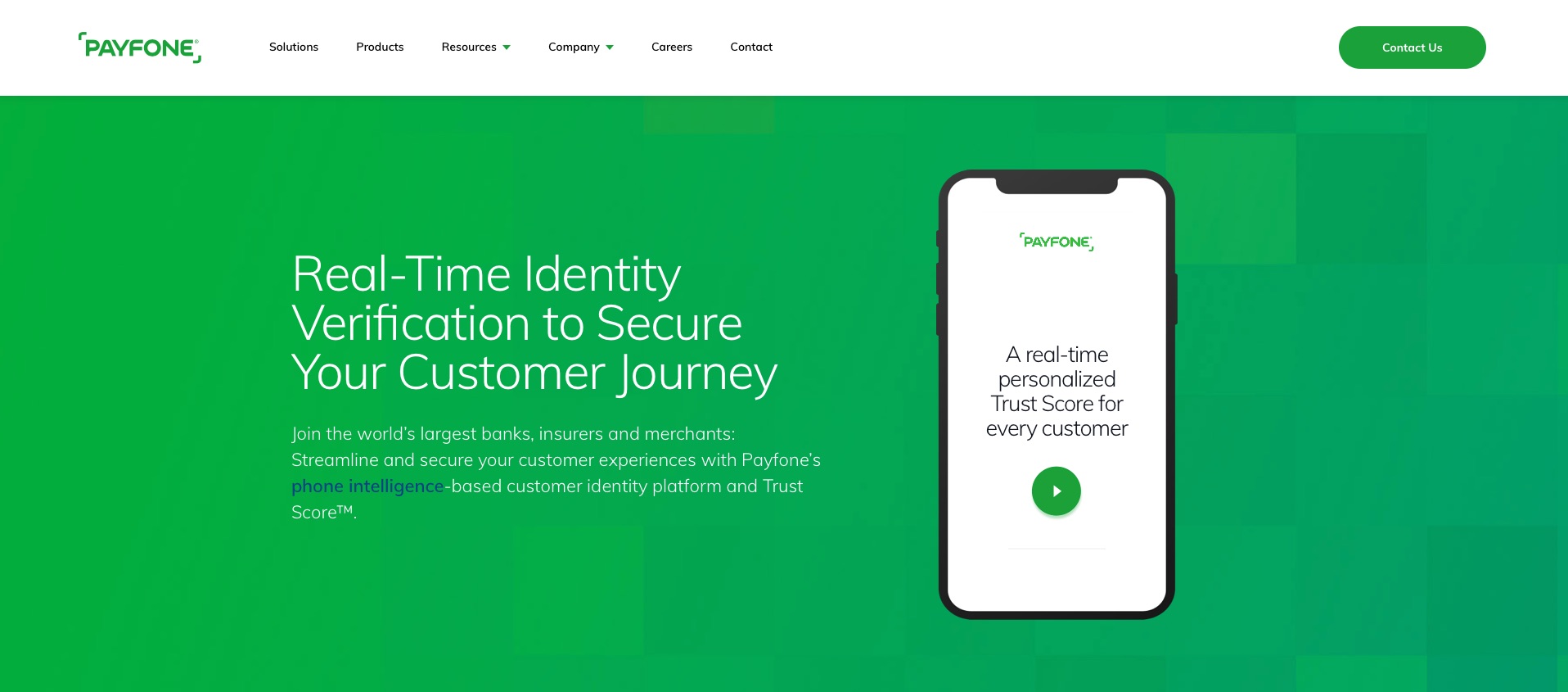

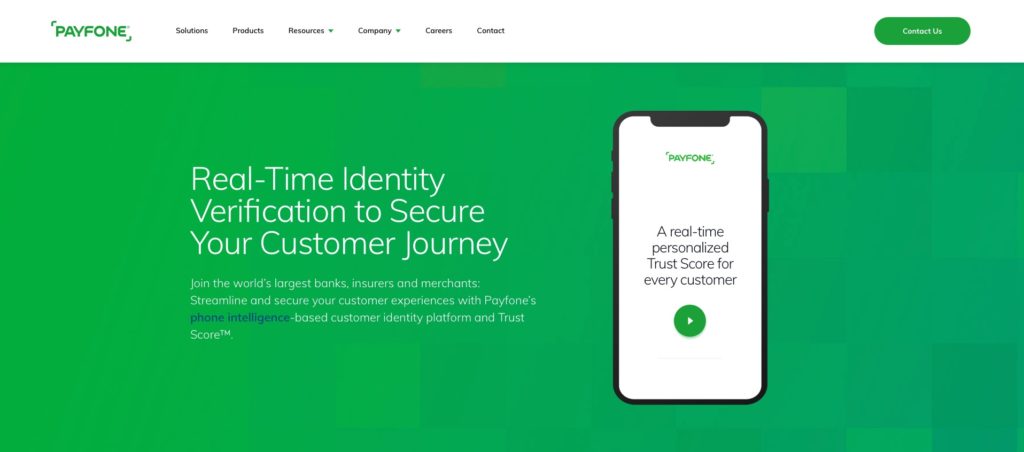

Identity verification and authentication company Payfone – which made its debut on the Finovate stage more than a decade ago – has announced a major fundraising of $100 million. The Series H investment, led by funds advised by Apax Digital (the growth equity division of Apax Partners), takes the company’s total funding to more than $217 million, according to Crunchbase. Although no valuation information was provided in last week’s announcement, TechCrunch noted that Payfone had earned a previous valuation of $270 million with its previous fundraising in April 2019.

Payfone’s customer identity platform helps financial institutions identify a range of potentially fraudulent activities – from the presence of a burner phone or a synthetic identity to spoofed calls and real-time SIM swap fraud. The company’s authentication solutions use proprietary “phone intelligence,” which processes behavioral signals in real-time to measure a phone number’s reputation and risk. This gives the authenticating party a Trust Score that helps them separate potentially suspicious activity from legitimate transactions. In addition, Payfone provides call verification solutions that run in the background of the phone call, making it easier and faster to resolve any authentication issues that arise.

“The mobile phone is rapidly becoming the secure passport for navigating our digital lives,” Payfone CEO Rodger Desai said. “With one in three U.S. consumers already authenticated by Payfone, this investment accelerates our ability to set the standard for the authentication process. As we build out a cross-industry consortium, more enterprises will be able to access Payfone’s real-time fraud and risk signals to prevent account takeovers while passing more transactions.”

In addition to helping the company build the forementioned industry-spanning consortium, the additional capital will be used to acquire strategic assets, and bolster the machine learning capabilities of its digital identity and authentication technology.

Also participating in the Series H round were new investors Sandbox Insurtech Ventures, and individual investor Ralph de la Vega, former Vice Chairman at AT&T. Existing Payfone investors MassMutual Ventures, Synchrony, Blue Venture Fund, Wellington Management LLP, as well as individual investor Andrew Prozes, former CEO of LexisNexis, were also involved in the fundraising.

Headquartered in New York City and founded in 2008, Payfone launched in the U.K. this spring with its Mobile Authentication product. The solution gives financial institutions in the U.K. a secure and easy-to-use alternative to one-time, SMS-based passwords for activities like customer onboarding, login, and two-factor authentication.

Payfone VP Keiron Dalton explained that while one-time passwords (OTP) have a role to play in the authentication process, they often fall short of what is required in the financial services industry. “(The) market demands placed on financial institutions in the U.K. are particularly acute,” Dalton said, “leading to a clamor of activity as these institutions search for what’s next in terms of authentication.” He called Mobile Authentication a “game-changing experience” for customers that provided a superior level of security against fraud, and added that the solution has seen “huge success in the U.S.”

Named one of the fastest growing companies on Deloitte’s 2019 Technology Fast 500 last fall, Payfone earned similar commendations this year from the Financial Times. The U.K.-based publication featured the company in the top 500 of its inaugural, The Americas’ Fastest Growing Companies 2020 roster.

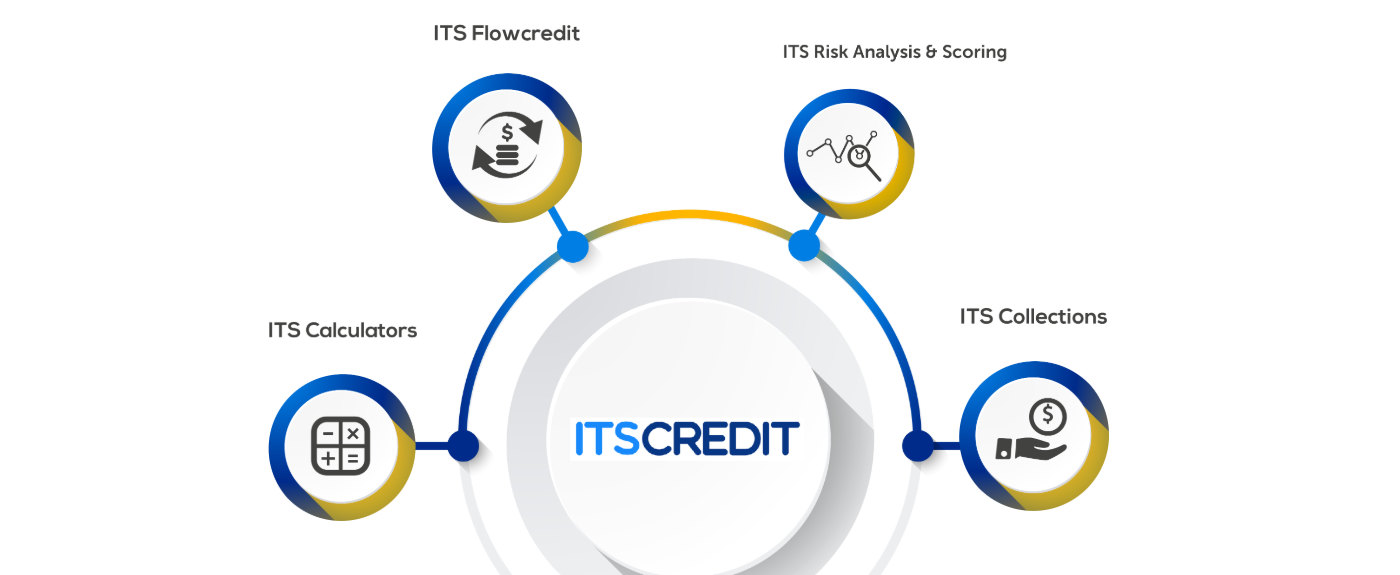

As part of our Finovate FinTech Halftime Review, Finovate Analyst David Penn sat down with João Lima Pinto, Chairman of ITSCREDIT. With nearly 20 years of solid experience in the financial sector, actively participating in the design and implementation of innovative omnichannel and credit solutions, Pinto has garnered much success by leading a variety of business development, product and project management, business analysis, and product operations functions.

Among the topics discussed include ITSCREDIT’S Genie Advisor app, how the company has seen the COVID-19 crisis impact its customer base, and its plan to address the challenges and move forward in 2020.

The international fintech community received an unexpected jolt on Friday on news that the CEO of Wirecard, Markus Braun, was stepping down. Braun’s resignation comes amid reports that the German digital financial platform he has led since 2002 cannot account for $2.1 billion in cash, and a delay in the release of its 2019 financial report. Reuters reported that the company admits it could be have been “the victim of fraud of considerable proportions.”

Up until recently Wirecard appeared poised for success as a leading European payment processor for both consumers and businesses. The company reported revenues of $2.2 billion in 2018 and, by the fall of that year, had reached a valuation of $26.9 billion.

But suspicious of the company deepened early last year. A Financial Times report in January alleging suspicious financial activity in Singapore, and the announcement of an official investigation by Singapore authorities a month later, tarnished Wirecard’s image despite the company’s denials. This was followed by claims of further questionable financial activity – this time in Ireland – in October.

In this week’s news, auditors at EY, formerly known as Ernst & Young, were not able to locate cash at two Asian banks – Bank of the Philippine Islands and BDO Unibank – where Wirecard said $2 billion had been deposited. Both banks have denied having a business relationship with Wirecard. Moreover, documents indicating that such a relationship did exist, according to BDO, were falsified and bore forged signatures.

In a statement, Wirecard announced that James Freis, who was recently appointed to the company’s management board, will serve as interim CEO. the Federal Financial Supervisory Authority, known as BaFin, is investigating.

Here is our weekly look at fintech around the world.

Latin America and the Caribbean

Brazil-based SME lender BizCapital raises $12 million in Series B funding to support development of new products.

Banco Sabadell partners with IBM to enhances its digital banking operations in Mexico.

Banco Safra, based in Brazil, to deployACI Worldwide’sUP Retail Payments solution and UP Framework.

Asia-Pacific

Vietnam Plus reports surge in contactless payments in Vietnam.

Crowdfund Insider investigates the rise of Sharia fintech in Indonesia.

Malaysian fintech Curlec, which helps businesses manage recurring payments and cash flow, secures investment from 500 Startups.

Sub-Saharan Africa

South African open banking startup – and FinovateAfrica alum – truIDannounces seed funding.

Nigeria’s Chipper Cash secures $13.8 million in Series A funding.

WapiPay, a fintech based in Kenya and Singapore that provides platform-to-platform integration for virtual and global accounts, raises seed funding via accelerator network FutureHub.

Central and Eastern Europe

Estonia’s Planet42 announces $2.4 million seed round led by Change Ventures. The company helps facilitate automobile access for the underbanked in South Africa.

Russia’s Tinkoffteams up with online marketplace goods.ru.

Bokuacquires Estonia-based mobile payments company Fortumo in deal valued at $45 million.

Middle East and Northern Africa

UAE-based Buy Now Pay Later e-commerce company Postpay introduces a trio of new installment payment options.

The Fintech Times takes a look at the state of the fintech and financial services industry in Lebanon.

Tpay Mobile, based in Dubai, acquires Turkish payments company Payguru.

Central and Southern Asia

Cryptocurrency exchange Binance joins the Indian Tech Association.

Kaspi, an e-commerce banking app based in Kazakhstan, to expand to Azerbaijan and other neighboring countries.

India Infoline launches #IIFLDisrupt, an initiative to help early-stage Indian fintechs during the COVID-19 crisis.

India-based Buy Now Pay Later company Tabby raises $7 million in funding to support expansion into Saudi Arabia.

Six companies that have demonstrated their fintech innovations on the Finovate stage have been recognized this year by CNBC as part of their Disruptor 50 roster for 2020.

This year’s list, the eighth in the series, is marked by the high number of billion-dollar companies, or “unicorns.” Fully 36 of the firms in the 2020 CNBC Disruptor 50 have reached or surpassed the $1 billion valuation mark. Combined, the 50 companies have raised more than $74 billion in VC funding and achieved an implied market valuation of almost $277 billion.

The companies making the cut range in industry from cybersecurity and healthcare IT to education and, of course, fintech. In fact, the top-ranked company in the 2020 Disruptor 50 is none other than Stripe, the $36 billion payments platform founded in 2010. Stripe earned a #13 ranking in last year’s Disruptor 50 roster, and likely owes its first place appearance this year to a major $600 million funding raising – the company’s largest to date – and the economic and social consequences of the global health crisis.

“With many people throughout the world under lockdown to prevent the spread of Covid-19,” CNBC’s capsule on the company noted, “the move to shopping online has never been greater. That’s good news for digital payments platform Stripe.”

Stripe was not the only fintech to earn high marks from the 2020 Disruptor 50’s methodology. In addition to the half dozen Finovate alums below, some of the other fintechs on this year’s roster include:

Virtual bank WeLab (Hong Kong)

Digital mortgage company Better.com (New York City)

“Buy now pay later” e-commerce company Affirm (San Francisco, California)

Challenger bank Chime (San Francisco, California)

Banking app Dave (Los Angeles, California)

Microfinancier TALA (Santa Monica, California)

Trading and investing platform Robinhood (Menlo Park, California)

Also earning spots in this year’s list were a pair of insurtech companies, Lemonade and Root Insurance, as well as cybersecurity and biometric authentication firms SentinelOne and CLEAR, respectively.

Here’s a look at the Finovate alums that made this year’s list.

The following is a guest post by Natalie Myshkina, Strategic Business Development, FSI at Adobe.

Like many industries and businesses right now, financial organizations in banking are finalizing and implementing business continuity/contingency plans as well as enabling all employees to work from home. At the same time, they are diligently working to meet changing client needs and building new ways to serve clients. Beyond the operational actions underway, banks and capital markets need to start developing medium- and longer-term plans to address each element of financial, risk, and regulatory compliance, and create new environments to support the business in fully digital settings.

In late 2019, an Arizent survey commissioned by the Credit Union Journal and American Banker reported that only 30 percent of organizations have a digital first, enterprise-wide strategy and readiness. Other organizations are still in the middle or beginning of the digital transformation of their businesses.

While most organizations have business continuity plans, they have been heavily tested over the last few weeks. I’d like to highlight a few operational steps that are essential to consider now for banks:

Transparency and trust Continue to adjust a communication plan to quickly liaise with employees, customers, business partners, regulators, investors, and vendors. Keeping close communications with customers and other stakeholders creates the opportunity to strengthen the relationship.

Operating model Implement a dynamic, scalable, and flexible operating model to ensure business continuity in any scenario. For example, in the case of temporary closures, branches need to quickly train branch employees to provide online help or assist the call center in serving clients.

Remote services and capabilities Many enterprise organizations have an extensive set of workflow tools, document management tools, document collaboration, and electronic signature solutions in place, but they are not fully utilized. For example, one department in the organization may fully embrace digital documents and electronic signatures, while another department keeps receiving and sending snail mail. The solution here would be to review best practices and tools across the organization, understand the full capabilities of available solutions, and offer them to unit managers to utilize as immediate solutions.

Digital project prioritization Conduct project prioritization exercises, and speed up projects related to offering digital products and services (client onboarding, product enrollment, etc.) or operational inefficiencies. If possible, speed up time-to-market or release solutions with limited/partial functionality or limited integration points.

Organizational culture Communicating and fostering the culture that maintains employee morale is becoming extremely important, and it can be done in different forms: through top-down communication and leaders acting as role models, by encouraging grassroots initiatives, by providing platforms for team collaboration, creating virtual watercoolers, etc.

Peer communications Be in close contact with industry groups for information to get best practices and requests to obtain waivers from regulators if required.

The coronavirus pandemic is already leading to major changes in how customers manage their finances and how financial organizations support their customers. Next we would be seeing activities related to meeting changing client needs due to financial stress, supporting client activities in digital channels, rapid digitalization in commercial and corporate banking, and more.

Here are a few notable areas financial organizations should address:

Proactively address new customer needs To operate in the new environment, banks would need to rapidly meet different client needs and serve them in ways outside the norm. Scalable solutions to process and approve requests for forbearance, mortgage holidays, deferred loan repayments, etc. would need to be implemented quickly as well as quickly scale up the Paycheck Protection Program (PPP) via the SBA program.

Branchless banking and self-service options in digital channel Due to the temporary closing of branches and reduced ATM availability and usage, the branchless banking or virtual branches idea is becoming more popular. As many interactions move online, expect to see more and more consumers want to use self-service tools on the web and in their mobile devices.

Rapid digitalization and digital service accessibility across all customer lifecycles stages For many organizations, their digital transformations began with onboarding new clients. But often we see that many other client touchpoints in the customer lifecycle are not fully digitized, and some require manual/paper steps. In the new environment, most of the client-initiated activities would be done on digital platforms. Automation is essential to provide clients with fast service and a consistent experience while keeping cost-effective operating model in place.

Expending successful digitalization of customer touchpoints beyond retail banking Over the last few years, we have seen substantial efforts and budgets spent on elevating customer experiences and moving clients to digital platforms. This has been done for many reasons, one of them was a demand from a digitally native consumer to have a better experience and the competition coming from neobanks (aka digital-only banks).

Commercial and corporate banks were behind this trend partially because the lack of these drivers and the complexity of the processes. In the new reality, we would be seeing a lot of rapid digitalization of customer-facing and internal activities in commercial/corporate banking and capital markets.

Data use, extraction and manipulation Going forward, the ability to extract and process data from multiple documents will be essential to manage risks and to create cost-conscious processes. Immediately, we could see requests for solutions to process documents to feed systems assessing portfolio health in stressed markets, or complete search thought legal documents.

Adaption of cloud solutions As financial services organizations have been behind the curve in the cloud solution adaption, this situation will trigger a revisit of internal policies and expedite further cloud adoption for both client-facing and internal solutions to improve efficiencies, eliminating the need for a larger security and maintenance staff, and creating cost-effective, scalable environments.

During these trying times, banks can best serve their clients by delivering products and services for business continuity today while working on business resilience for the future. Industry experts predict that the current situation will accelerate the digital transformation in the industry over the a short period of time. That time starts now.