This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

As we approach the end of the year, it’s time to sit back with a fresh cup of tea, look out the window at the falling snow, and…think about what a significant year it’s been for fintech, of course!

2022 was a turbulent year in our industry. The past year offered real solutions to significant problems unearthed by the pandemic, but also the beginnings of a course-correction that is slowly working its way through the fintech sphere (and the larger tech ecosystem).

One fundamental aspect of the fintech industry is that it has always been able to hold two diametrically opposed truths at the same time. Right now, both of the following statements are true:

1) the future of fintech is as bright (or brighter) than it’s ever been, and

2) there are still more painful situations coming for us in 2023.

Analysis from our resident journalists on the top trends they expect to see making waves in the industry next year

Thought leadership from Headline Sponsor, Frost & Sullivan on how to protect and improve customer financial wellness amidst economic uncertainty

The full collection of Finovate 2022 Best of Show demos videos

Expert opinion on accelerating your data strategy, getting the most out of fintech/ bank partnerships, why crypto is “useless” and investor advice for start-ups looking to get funding right now

Faster, flexible and easy. It would be surprising if those words weren’t the top cited needs for your customers on what they expect when using your fintech app. If you can provide these obvious, yet sometimes elusive characteristics in your next release, you’ve hit the jackpot or, at the very least, met expectations!

Speaking of customer expectations, faster, flexible, and easy ARE the expectations. Any usability friction can at best annoy. At worst, it can cause you to lose customers, particularly when competition is fierce, and especially after the past few years with the rise of the “gig economy.”

What is the Gig Economy?

The gig economy is based on flexible, temporary, or freelance jobs, often involving connecting clients and customers through an online platform. But not only that, the gig economy also connects and attracts those customers who expect speed, flexibility, and ease of use.

Starting in 2020, the gig economy grew substantially as jobs were eliminated, and previous full-time workers turned to part-time and contract work for income. Many workers took delivery service jobs bringing necessities to home-bound consumers.

Thriving within the gig economy is a big opportunity for fintechs. The gig economy spans generations – from those in their first job who have added a side hustle, to those working multiple temp or freelance positions, to those in retirement who want to earn some extra income. What they all have in common is the need for services that are fast, flexible, and easy to use. They don’t have the time or patience to deal with clunky, slow services that don’t deliver to their expectations.

A recent GWI report on U.S. fintech trends shows that the widespread usage of digital financial tools offers brands a huge upside for fintech applications, particularly with the “gig economy.” 30% of Americans participate as workers in the gig economy in some way, and digital financial tools are by far the most preferred way to manage their multiple streams of income.

If You Integrate (Fast, Flexible, and Easy to Use Document Processing), the “Gig” Will Come

Fintech companies may be on the cutting edge of software innovation, but even their most sophisticated applications need the ability to accommodate a variety of document-heavy processes used in the financial services industry. That’s why 94 percent of them leverage some form of digital document management solution.

Developing or enhancing a fintech app for the gig economy is tricky, as they expect more of their software applications than ever before (faster, more flexible, easier). Piecemeal solutions that offer only a few features are being overtaken by more comprehensive platforms that deliver a fuller end-to-end experience. Developers are adjusting by making essential technology upgrades to their tech stack, incorporating more capabilities, while also building innovative features that set their solutions apart from the competition. Thanks to third-party software integrations, they’re able to do it all.

Third-party software integrations allow developers to build more cohesive software solutions that provide all the essential features a customer may require. Instead of pushing them into a separate application to interact with their documents, provide a signature, or fill out a digital form, they deliver an unbroken experience that’s easier to navigate and manage from start to finish.

Upgrading Your Fintech Application’s Potential

By turning to a partner with the right software integrations, fintechs can quickly implement powerful features while keeping their own development efforts focused on designing best-in-class capabilities and bringing them to market quickly.

With more than 30 years of experience helping fintechs enhance their integrations, Accusoft’s collection of SDK and API solutions provides a broad range of document and image processing solutions that can help improve efficiency, reduce errors, and deliver a better overall user experience. Whether you need the viewing, editing, and document processing features of PrizmDoc, or the image clean-up, conversion, and OCR capabilities of ImageGear, our family of software integrations can make it easy for fintechs to incorporate the functionality they need without having to rethink their tech stack. And most importantly, fintechs will be well prepared to meet and sustain the growing expectations of the gig economy for speed, flexibility, and ease of use while using their digital finance tools.

In today’s digital-first environment, fraud threats are growing in sophistication and scope, and risks of online and financial crime have intensified. At the same time, fintechs are prioritizing growth, and need to do so in a way that is safe, secure, and keeps bad actors out.

Watch back on this Finovate webinar, with Experian Chief Innovation Officer for Decision Analytics Kathleen Peters, as she explores the meaning of digital identity, and how fintechs can leverage identity-proofing strategies to position themselves for growth without diminishing security. Learn:

The role of digital identities in advancing increased personalization, speed, and growth responsibly in fintech and financial services

How data can aid in making smart, risk-based decisions across the user journey

How to unlock financial growth opportunities by offering solutions to previously unavailable consumers due to verification constraints

The first step of the customer journey is often a user’s onboarding on a platform or application. This critical phase predicates how a user interacts with a business, and often cements their first impression and subsequent brand loyalty.

Identity verification plays an important role in ensuring a user exists and is who they say they are. But businesses must strike a fine balance of friction and convenience. Too little friction in the identity verification process might result in bad actors flooding in. This can damage a business’s reputation, and give the impression that a platform is unsafe. Too much friction might result in user frustration and attrition.

How can businesses seamlessly and securely onboard users? Orchestration holds the key to unlocking customer-centric practices, customizing the user journey, and ultimately ensuring legitimate users are allowed in while bad actors are stopped.

Watch this webinar featuring Hal Lonas, Trulioo Chief Technology Officer, on

What identity proofing orchestration entails and how active and passive methods of authentication can be layered during the onboarding process

How orchestration goes hand-in-hand with a risk-based approach to onboarding and establishing trust and safety between businesses and users

What business, customer risk, and regulatory factors to consider when adopting a risk-based approach

This is a sponsored post by Tim FitzGerald, EMEA Financial Services Sales Manager, InterSystems, Gold Sponsors of FinovateFall 2022.

In today’s fast-moving landscape, financial services firms are under increasing pressure to remain competitive and generate more revenue by developing new products and services faster, while still leveraging their existing resources.

In recent years, this has seen many financial services organisations turn to external fintech solutions to help accelerate innovation and quickly obtain new digital capabilities. And so, fintech partnerships have become critical components of financial institutions’ growth strategies, rather than the technology experiments they started out as.

To ensure innovation success, it’s vital that financial services organizations can easily leverage and provision new fintech services and applications by seamlessly integrating with their existing production applications and data sources. But the true value and potential of fintech solutions can’t be unleashed until integration is quick and easy.

As many firms will attest, arduous and costly integration can see the value of such initiatives dwindle before their very eyes – sometimes to be lost altogether. Common challenges can range from unforeseen issues tying up precious IT resources, to costs spiraling out of control and timescales sliding drastically from what was planned or what is desirable. Ultimately, these delays can result in the loss of any competitive edge as rivals launch similar solutions much faster.

Ensuring successful integration

Fintechs have become increasingly attractive as they incorporate the latest technologies, modern application methodologies, and deployment platforms. However, for banks to make effective use of these opportunities, those technologies need to be woven into its existing infrastructure, much of which is likely to be based on legacy technology.

Consequently, successful integration requires an understanding of the intricacies and idiosyncrasies of those legacy systems. It also demands knowledge of the underlying data architecture and how to connect the new technology to systems that weren’t built to be connected to in such a way. While this isn’t an unsurmountable problem, getting it right will take resources, budget, and time.

Careful consideration is also needed when undertaking the integration to ensure that the resulting architecture doesn’t become overly complex. After all, if it comprises multiple technology layers from different vendors, all with differing versions and releases, any future change could impede the bank’s ability to take advantage of the benefits they set out to achieve.

Next will be to determine how data from existing systems will be fed into the new system and in what format. To get around this, it’s all too easy to layer extraction tools upon a myriad of other tools, including transformation tools, data lineage, master data management, databases, and data lake technologies. However, what firms are then left with is a multi-headed monster that no one person truly understands. This approach to data integration is also complex and costly to design, deploy, manage, and maintain. Fortunately, adopting a smart data fabric approach, a next generation architecture, can provide a way for financial services organizations to overcome these challenges.

Achieving bidirectional connectivity

By leveraging a smart data fabric, it is possible for institutions to connect and collect real-time event data and obtain unmatched integration capabilities using just one holistic platform. This approach eliminates the complexity and inefficiencies of manual integrations and other legacy approaches to integration and enables firms to integrate applications faster and more efficiently. It does this by essentially creating a dynamic real-time, bidirectional gateway between cloud-based fintech applications and their own production applications and data assets.

The smart data fabric integrates real-time event and transactional data, along with historical and other data from the large number of different back-end systems in use by financial services organizations. It transforms the data into a common, harmonized format to feed cloud fintech applications on demand, thus providing seamless, real-time, bidirectional connectivity and integration with the bank’s existing legacy enterprise data, production applications, and data sources.

Not only does this help firms to realize faster time to value and achieve simpler implementation that is easier to maintain, but it also gives financial services institutions the agility needed to innovate faster and keep critical initiatives on track. Additionally, it helps to futureproof their architecture by making it easier to incorporate any fintech applications and technologies available in the marketplace, thereby empowering them to react to new opportunities and changes in their environments.

Ultimately, there is immense value to be unlocked from fintech solutions and applications. However, that is only possible through swift and simple integration. By implementing a smart data fabric-enabled data gateway, financial services organizations can quickly and easily integrate new solutions within their existing infrastructure to ensure they are able to keep pace in a rapidly evolving landscape.

60+ innovative demos. 100+ expert speakers. 1700+ influential attendees. The connections and ideas you need were at FinovateFall this year. Were you there?

Get a taste of the action below, and catch up on some of the unique insights from the experts who took to the stage!

Bill Harris, CEO at Nirvana Money, joins David Penn, Finovate Research Analyst, to discuss the vision and ambition behind starting Nirvana Money, what advice he’d give to new fintech founders, and why he predicts the demise of crypto.

Gregory Wright, Executive Vice President and Chief Product Officer at Experian, talked with Julie Muhn, Finovate Senior Research Analyst, to discuss the three principles for amplifying your innovation success: innovation with purpose, which helps drive impact for your consumers and their communities; innovation through scale, to get to “yes” faster and more often; and innovation with analytics, bringing together datasets in real time that we’ve never had before.

Julie Muhn, Finovate Senior Research Analyst, sat down with Ann Kuelzow, Global Head of Financial Services at InterSystems, to explore how businesses can get an accurate and (importantly) a real-time view of their data to guide their decisions, and why data fabrics are the future of data management.

David Penn, Finovate Research Analyst, was joined by Bernadette Ksepka, Assistant Vice President & Deputy Head of Product Development, FedNowSM Service at Federal Reserve System, to discuss the U.S. payments landscape, and how the upcoming FedNow service will modernize current payments infrastructure and pave the way for big changes and innovations.

Exciting things are happening in fintech right now, and we’re incredibly grateful to have so many of you joining us at FinovateFall this year to take it all in for yourself. There’s a lot to be excited about! As you may have heard, this year’s FinovateFall is officially our largest show yet, with more than 1,600 of you here in the room with us. After a period of general upheaval and uncertainty, it’s great to see the fintech community coming together en masse to plot a course for the future.

What’s happening is bigger than just the number of people in the room, though. It’s no secret that the last few years have been challenging ones and what we’re seeing now is fintech’s response to that challenge. New ideas, new innovations, and new companies are taking shape right before our eyes; venture capitalists are actively seeking out early-stage investment opportunities; and financial institutions themselves are more receptive to change and innovation than ever before. And most importantly, at every step of the way, the industry is making a concerted effort to help the everyday people who need it most.

Analysis from our resident journalists on the top trends from the event and beyond

Thought leadership from Headline Sponsor, Provenir

The Best of Show demos videos

The Finovate Awards winners, and finalist profiles of Highnote and RBC Clearing

Expert opinion on accelerating your lending strategy, the do’s and don’ts of leveraging emerging technology in fintech and exploring virtual worlds and economies

This is a sponsored post by Strands, Gold Sponsors of FinovateFall 2022.

Nowadays, personalization has become a must in all sectors that affect consumers’ daily lives. Companies such as Netflix and Amazon have already been able to create totally customized and customer-centric experiences thanks to advances in technology, data, and analytics. Digital Banking has also faced these expectations, demanding personalization for different user bases, needs, and underserved segments. With a focus on financial wellness, banks can generate cross-selling opportunities and create personalized journeys according to the interests of their customers.

Technology advancements have enabled companies to collect, analyze, and use data from a variety of sources, including internal and external channels, enabling banks to make better decisions, offers, and actions than ever before. Unfortunately, most banks still struggle to know their customers or to interact with them timely and relevantly – to provide the right offers at the right time to the right customers.

This is what customer centricity means, which is vastly different from product or brand centricity. When a financial institution has a deep understanding of its customers, it can provide solutions that are tailored to meet their specific needs, life stages, values, and interests beyond their typical sociodemographic information.

As part of this approach, extra data sources are tapped, such as third parties, in addition to what’s available within core banking as open banking data, surveys, social media, and other data sources consented by the customers, integrating machine learning, categorized transactional data, and other customer experience solutions that can enrich the available raw data.

How to derive and use such insights is now the question. In the first stage of data enrichment and analysis, core application data can be used to understand how the customer interacts with the bank, the recency, frequency, channels, etc. Through this information and analytical models, it is possible for financial institutions to predict proactively what the customer is likely to want or need in real time.

How to power rapid approvals and accelerate your SME lending processes

Forty-four percent of SMEs look to funding to meet operating expenses, with this number expected to grow considerably during times of economic uncertainty. Fifty-six percent of SMEs seek funds to expand business operations or to pursue new market opportunities. But waiting months or even weeks for credit approval and funding can mean the difference between innovation and business closure.

Traditional financial services organizations may find lending to SMEs difficult, but fintechs are rising to the challenge. Simplified application processes, rapid approvals, and access to funds quickly makes working with digital lenders an obviously attractive choice.

Because if you aren’t making it easy for SMEs to get the credit they need, your competitors will.

Catch up on this panel discussion with industry experts, in collaboration with Provenir, and discover how to: • Power faster, simplified application processes • Make smarter, faster decisions and get to market faster • Future-proof your decision technology to keep up as market trends/demands evolve • Use advanced, predictive analytics like AI to keep risk in check

Featuring Corinne Llelti, Commercial Sales Director, EMEA, Provenir; Alex Daly Chief Finance and Risk Officer, Ask Inclusive Finance Group; and Julie Muhn, Senior Research Analyst, Finovate.

The customer journey is vital in today’s financial services landscape and cloud-enabled business innovation is the vital ingredient.

A good user experience is a critical factor in helping consumers differentiate between firms and helping brands build lasting relationships with customers.

According to the Harvard Business Review, firms with leading customer satisfaction rankings can grow their revenues two and a half times faster than their competitors. Moreover, research by Forrester demonstrates that customers are over twice as likely to stick with a brand when their problems are solved quickly.

Yet, great digital experiences rely on intuitive GUIs and an agile, cloud native strategy, both of which are not easy to achieve. In this article, we’ll demystify how to get started with cloud computing in software engineering for banking and help you develop a leading customer UX.

What Are the Challenges of Cloud Business Innovation in Banking?

Approximately US$1.3 trillion was spent in 2020 on digital transformation, yet Deloitte data shows 70% of projects fail. That equates to over US$900 billion wasted — so what’s going wrong?

Just as an HD TV relies on good HD content, great apps need high interactivity with data, an always-on presence, security, and scalability to perform under high demand.

Eric Newcomer, WSO2 CTO, argues that cloud business innovation goes wrong when there’s a messy middle. In other words, when there’s a lack of clarity about how strategy, outcome, and skill coordinate the microservices within a platform, cloud business innovation becomes dysfunctional.

Within banking specifically, the stakes of digital transformation are extremely high. Today’s financial services firms must deal with an onslaught of cyberattacks and regulatory constraints, not to mention increased competition from new fintech entrants better-equipped to deliver excellent customer experiences. So how can financial institutions ensure they foster an innovative and successful cloud-first environment?

How to Overcome These Challenges

Great cloud computing in software engineering needs equally great cloud native practices and technology, focusing specifically on integration and APIs. Without this focus, customers lose the always-on, always integrated feel that today’s users demand.

Therefore, financial services firms require an all-in-one platform delivering accelerated and enhanced engineering processes to speed up innovation in their cloud environment. Unfortunately, building robust and agile platforms from scratch can be timely and costly.

Instead, partnering with existing solutions providers allows financial service firms to focus on developing cloud banking innovations and better deliver security, compliance, and ideal customer experiences. You can read more about overcoming challenges for banks to generate fintech innovation here.

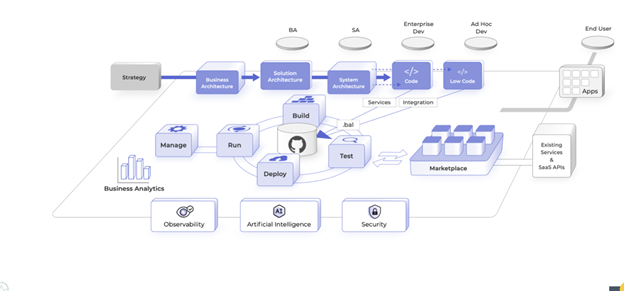

The Role of Digital Platform-as-a-Service Within Financial Services

An “opinionated” digital platform-as-a-service (digital PaaS) accelerates cloud banking innovation by tackling some of the core complexities of developing digital applications. As a result, you can build, deploy, and iterate new versions more easily.

Digital PaaS platforms enable diagrammatic and low-code functionality, providing a great developer experience. In turn, your teams can increase their productivity and attention to quality assurance for end-users.

Moreover, digital PaaS integrates with automated deployment tools using Docker and Kubernetes. As a result, you can test, develop, and deploy new user features for maximum customer satisfaction faster than ever before, using just a few clicks.

Digital PaaS solutions deliver seamless platform functionality and integration with your existing data warehouses, allowing you to leverage efficient and scalable consumer solutions.

How Low-Code Digital PaaS Enables Cloud Computing in Software Engineering

There isn’t a one-size-fits-all solution to cloud computing in software engineering, so what makes a digital PaaS-based method the most appropriate for financial services?

A digital PaaS approach provides a highly stable environment to create and manage APIs since it establishes core conventions and assumptions within your workflows. These assumptions include the programming language and dev environment, all the way to the publishing process on software marketplaces. As a result, you can remove barriers to collaboration and shorten project lead times. Similarly, as a cloud-enabled solution, you provide collaborative space for your teams to work.

Moreover, you can easily build platform microservices and provide teams with autonomy over their software output. Software teams can publish updates to critical platform elements accordingly without jeopardizing the rest of your platform or relying on slower project teams, keeping your user experience competitive.

However, the benefits don’t stop when you hit publish. Digital PaaS solutions allow you to run professional DevOps systems and make improvements in step with live user trends. Consequently, you can remain competitive and establish a close relationship with customers.

Finally, once your APIs are built, you can share them through marketplace and import or export data with other SaaS platforms. As a result, you can leverage other data sources for enhanced features. For example, you can capitalize on open banking ecosystems, enhance your security through additional identity checks, and more.

And so, with complex development and deployment tasks that are both easy to learn and use, you can deliver fresh digital services faster — and more accurately — than ever.

Introducing Choreo by WSO2

With around only three in ten digital transformations being successful and the heightened competition within banking today, financial services companies need to innovate at speed and scale.

Choreo is a digital PaaS that helps companies manage and develop APIs, services, and integrations quickly. Choreo enables developers and operations teams to go from ideation to production in hours or days versus weeks and months via a seamless environment that eliminates the complexity of cloud native computing.

Choreo provides a diagrammatic and pro-code environment side by side, allowing you to create an outline and make detailed tweaks in minutes. It includes a developer marketplace with over 400 pre-built connectors that makes it easy to discover, reuse, publish, and share.

With security and transparency at its foundation, you can easily trace code changes and root issues across your entire development history. You can also benefit from AI-assisted coding and enhanced governance features.

Find out more about Choreo and create an API with just a few clicks.

The fintech and payments industries are rapidly evolving. Isn’t it time fraud and dispute management processes did as well? Financial institutions not seeking alternatives to legacy infrastructure are constrained in their ability to automate and streamline lengthy and manual processes, such as chargeback management.

In this webinar, Quavo’s SVP, Revenue Executive Brittany Usher, and KeyBank’s Head of Enterprise Fraud Services, Jen Martin, will join Finovate’s Julie Muhn to discuss initial steps toward automation for issuing financial institutions seeking to overhaul their pre-existing manual and legacy systems. Along with providing business case examples, Brittany and Jen will elaborate on the lessons learned from implementing new software, conducting a cost analysis examining price per transaction, chargeback recoveries, manual intervention, fines, and overhead costs.

Covering:

Discover tips on the first steps to take when seeking to overhaul preexisting manual/legacy systems with real life examples and lessons learned. This is a common obstacle to implementing new software.

Learn how to set up data requirements, merchant collab software, accounting, and more.

Conduct current cost analysis – price per transaction, chargeback recovery, manual intervention, fines, overhead, and more.

This is a sponsored post by Ann Kuelzow, Global Head of Financial Services at InterSystems.

A staggering 86% of financial services firms globally are concerned about using data to drive decision-making within their organizations, according to the latest research from InterSystems of 554 business leaders within financial services companies, including commercial, investment, and retail banks, across 12 countries globally. This lack of confidence largely stems from an inability to access data from all the needed sources and the time taken to access data. Given the wealth of data financial services firms have, this is a major concern, with the potential to open organizations up to risk and severely impede key business initiatives. In fact, more than a third of firms in the survey cite the primary impact of these challenges as being difficulty in gaining a 360-degree picture of customers.

As competition intensifies within the financial services sector, customer 360 is something that all firms must confidently be able to obtain. Doing so will empower firms to provide clients with the products, services, and hyper-personalized, real-time experiences they have come to expect across all aspects of their lives. But this relies on gaining access to accurate, consistent, and real-time data encompassing all touchpoints. Consequently, firms must first address underlying issues with their data architecture.

Solving data challenges

Gaining a holistic view of the customer requires firms to pull together all available information on each customer. As customers are likely to interact with a variety of different departments and personnel within the firm, this information can be spread across multiple systems and silos, including trading, savings, credit cards, loans, insurance, CRM, support, data warehouses, data lakes, and other applications and silos, as well as data from external sources and suppliers. The data is often in dissimilar structures and formats and follows different naming conventions and metadata. Therefore, making sense of this dispersed data typically requires significant effort and expense, and using it to make informed, accurate, and fast decisions is a major challenge.

As organizations look to solve these problems, data fabrics, a next-generation architectural approach, have emerged to provide financial services firms with a way to speed and simplify access to data assets across the entire organization. It does this by connecting to existing systems and data silos containing relevant data, both inside and outside the organization, and ingesting the relevant data on demand as it’s needed. It accesses, integrates, and transforms the data as it’s being requested, providing a real-time, consistent, harmonized view of the data from different sources, all from a single view. This allows firms to gain a complete 360-degree view of the customer.

Going a step further

A smart data fabric takes this approach a step further by providing built-in analytics capabilities which enable business users to understand customer behaviors and actions better and even to predict the likelihood of future behaviors, such as purchase of new services, churn, or response to targeted offers. It also provides the business with self-service analytics capabilities, so line-of-business personnel can drill into the data for answers without relying on IT, eliminating the usual delays associated with adding custom requests to the IT department’s queue.

This next generation approach also helps solve latency issues, as smart data fabrics lets the data reside in the source systems, where it’s accessed on demand, as it’s required.

Adopting this approach will help to restore firms’ trust in their data, ensuring that they can quickly access consistent, reliable, and accurate information on which to base decisions, fuel data initiatives, and build up a comprehensive view of the customer.

Elevating the customer experience

Being able to leverage the wealth of customer data inside and outside of the organization for customer 360 will empower firms to offer a vastly improved customer experience. For instance, with a single view of the customer, advisors, help desk, and support teams will be able to provide customers with the immediate answers and recommendations and thereby enhance their interactions with the organization.

Armed with customer 360, firms will also be able to increase revenue streams by predicting customer behavior to maximize cross-sell and up-sell opportunities. For example, incorporating and analyzing dozens of data points from different systems enables firms to determine which customers are likely to respond to a premium credit card offer and least likely to default on payments. This allows firms to identify which customers to target with particular offerings and services. Similarly, firms will be able to predict which customers are at risk of churning and take appropriate corrective actions in advance to reduce churn.

Together, these capabilities will help to elevate the experience and services being offered to customers, while also helping financial services firms to create and cement a competitive edge.

Restoring trust in data

Ultimately, by adopting smart data fabrics, firms will be able to overcome the data challenges that are currently preventing them from using their data to make better decisions by leveraging a more complete and more current 360-degree view of each and every customer. With a complete and trusted 360-degree view of the customer, firms will be in a strong position to fuel new customer initiatives, enhance the customer experience by delivering cohesive and personalized interactions and offerings across departments, and set their institution apart.