This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

After a thrilling weekend of World Cup matches, fans in the US are readying for this evening’s big contest against Belgium. To help you while away the hours until then, here’s a look at some of the top fintech headlines that are coming across our radar today. Be sure to check back with Finovate’s Fintech Rundown all week long for the latest updates.

Digital banking

Cloud-native core banking and payments platform Thought Machinesurpasses $100 million total revenue milestone.

Digital banking platform for small businesses Bluevineexpands its services to selected foreign-resident owners of US businesses.

Back office

VyStar Credit Union expands partnership with FMSI to advance branch performance strategy.

Agentic AI

BBVAcompletes its first AI agent-initiated transaction on behalf of a cardholder.

The first month of summer is upon us! Whether your plans over the next several weeks include time away in exotic locations or sticking to the grindstone, Finovate’s Fintech Rundown is here with the fintech news you need to know. Be sure to check back all week long for the latest updates!

Lending

FinastralaunchesData Insights 2.0, an analytics solution that helps lenders transform complex data into actionable insights.

Baker Hilllaunches one-click loan participation exchange with Participate to help financial institutions scale commercial lending.

Experianbrings personal loan shopping to ChatGPT with new AI-powered experience.

Cross Riverextends $250 million forward-flow commitment for Figure’s crypto-backed loans.

Liliembeds business credit solutions to help small businesses access capital faster.

Embedded finance

Embedded payments and financing solutions provider Adyenteams up with venue management platform ROLLER.

Germany embedded finance fintech Rivertysecures regulatory approval for a Luxembourg banking license and plans to initiate operations in July 2026.

Jack Henrypartners with Woodforest National, a $9 billion, multi-state bank based in The Woodlands, Texas.

Brazil’s Nubankintroduces new offering for customers between 16 and 18 years old called NuCel that combines 5G mobile connectivity with a savings feature.

Payments

European Pay by Bank network TrueLayeracquires Dutch consumer payments company In3.

Modern card platform Highnote unveiled its new Agentic Commerce capabilities this week.

Built using Visa Intelligent Commerce, Highnote’s Agentic Commerce will allow businesses to power AI-initiated payments that feature programmable controls, tokenized credentials, and dynamic authorization.

Headquartered in San Francisco, Highnote made its Finovate debut at FinovateSpring 2022.

Courtesy of a partnership with Visa, Highnote—a modern issuing, acquiring, credit, ledger, and money movement platform—has launched its new Agentic Commerce capabilities this week. Built using Visa Intelligent Commerce, the new offering will enable businesses to securely power AI-initiated payments with programmable controls, tokenized credentials, and dynamic authorization.

The new Agentic Commerce capabilities will allow companies to add payment capabilities to AI agents while enabling software to initiate and execute transactions with predefined rules, spend controls, and approval structures. In a statement announcing the launch, Highnote listed invoice and accounts payable automation, vendor payments, operational spend management, and AI-assisted procurement as some of the initial use cases for the new solution.

“AI is quickly moving from insight to action,” Highnote CEO John MacIlwaine said. “Businesses want AI to do more than recommend or analyze. They want it to initiate and execute real financial workflows. The challenge is making those transactions secure, controlled, and operational at scale. That’s exactly what Highnote is built to do.”

Agentic commerce enables software to participate directly in purchasing and payment decisions based on preset authorization rules. The new capabilities give firms a structured framework for enabling AI-driven transactions with real-time visibility and decisioning across the payment lifecycle. Highnote’s Agentic Commerce offering will also support emerging financial operations powered by AI, such as intelligent procurement, dynamic payment routing, supplier optimization, recurring operational spend, and industry-specific autonomous payment experiences.

“Agentic commerce is already changing how businesses operate,” said Visa VP and Head of Agentic CMS Ivy Lee. “Through Visa Intelligent Commerce, we’re enabling B2B workflows where agents can initiate and complete transactions at scale. Visa provides the underlying infrastructure that makes this possible—handling the complexity so businesses and developers can focus on building differentiated experiences, not payments.”

Headquartered in San Francisco, California, Highnote made its Finovate debut at FinovateSpring 2022. At the conference, the company demonstrated how its modern card platform with a GraphQL-based API enables businesses to make card issuance an embedded capability. The demo also featured the developer experience and financial operations interface that provides control of the payment transaction lifecycle and access to transaction processing data.

Named to the Forbes Fintech 50 for a second consecutive year, Highnote last month unveiled expanded commercial card issuing capabilities for online travel agencies (OTAs), marketplaces, and travel platforms. The new offering enables these platforms to run on Highnote’s commercial card issuing platform, using virtual card programs that are purpose-built for the challenges of travel supplier payments. Highnote’s solution combines issuing, controls, ledger, and reconciliation into a single system in order to deliver faster reconciliation, bolster supplier relationships, and improve unit economics on every transaction.

The first quarter of 2026 comes to a close tomorrow. And amid the rush of end-of-month, end-of-quarter news, don’t forget that April Fool’s Day, April 1st, is right in the middle of the week.

Every year there are a handful of fintechs that like to take advantage of the occasion by having a little fun with the press, so it’s always a good idea of have a bit of extra skepticism if you come across a headline that seems a little sensational over the next few days. Here on the Fintech Rundown, we promise to do our level best to keep you fool-free!

Digital banking

Metro Credit Union to deployTyfone’snFinia Digital Banking Platform.

Corgi Insuranceacquires Corgi.com domain en route to building its fully-integrated, AI-powered insurance carrier.

Digital communications

AI-powered digital communications governance and archiving technology partner Shieldunveils new enhancements to its Shield Archive solution.

Lending

Worth, a fintech platform that helps financial institutions onboard and undewrite small and medium-sized businesses, raises $30 million in Series A funding.

Spring has sprung, March Madness is in the air, and the fintech headlines are filled with new payment solutions to enhance face-to-face commerce, new developments in the tokenized asset space, and a range of announcements on agentic AI including new tools, new partnerships, and new deployments.

Be sure to check back with Finovate’s Fintech Rundown all week long for the latest in fintech news!

Payments technology company Splititunveils its Splitit Go mobile and API-based solution that brings card-linked installment payment options to in-person commerce.

Fraud prevention and identity verification

Digital identity and compliance platform ComplyCubeunveils its expanded fraud intelligence suite.

Finix and Plaid team up to enhance bank verification and streamline money movement.

Australian fintech Vivi Moneychooses Pismo’s infrastructure to launch new AI-native financial solution on Visa’s global payment network.

Constant AI, an agentic AI firm that specialists in lending operations for credit unions, launches AI Skip-A-Pay agent, Nia.

AI platform Go AbacusunveilsThe Go1, an on-prem AI hardware solution to give banks data sovereignty. Catch Go Abacus in its Finovate debut at FinovateSpring 2026 in San Diego.

Insurtech

AI assistant for financial advisors, Zocks, introduces its new AI assistant for life insurance. See Zocks make its Finovate debut at FinovateSpring 2026 in San Diego, May 5-7.

DeFi

Q2partners with digital asset platform Stablecore to enable banks and credit unions to offer stablecoins, tokenized deposits, and other digital asset products.

TAPP Engine and KoreInside team up to bring financial stablecoins to private capital markets.

With St. Patrick’s Day at the beginning of the week and the first day of spring at the end, it feels as if we are truly leaving winter behind us. Cacti are blooming here in the desert southwest and the fintech news —from new offerings in wealth management to the latest innovations in agentic AI—is flowing. Be sure to check back here at Finovate’s Fintech Rundown all week long for updates.

Digital banking

BankDhofarlaunchesNeo Corporate Internet Banking (Neo CIB), its next-generation digital banking platform.

DNERO, a neobank that caters to Latino customers, readies for a March 24 launch.

Digital asset wealth management platform Abraannounces plans to go public via SPAC merger with New Providence Acquisition Corp at a valuation of $750 million.

Sokinlaunches stablecoin capabilities to provide hybrid finance platform unifying digital assets and fiat.

Agentic AI

Lithuanian fintech Chaseit.aiintroduces AI agents to automate loan servicing and call center communications.

Integrated financial management platform for freelancers and gig economy workers, Finom, launches its embedded interest account.

Iwocaintroduces free financial health resources, including its Credit Compass, for small businesses in the UK.

Lending and Credit

Experian launches its AI-powered Experian Virtual Assistant (EVA) to deliver real-time, personalized financial insights and recommendations on financial products such as credit cards, loans, and insurance.

Ocrolusaccelerates automated conditioning for mortgage lenders with full lifecycle management.

Back end technology

FMSI and Applipartner to help credit union branches drive member revenue.

This week’s edition of Finovate Global focuses on fintech developments in countries located in and around East Africa.

Digital banking secures investment in Zambia

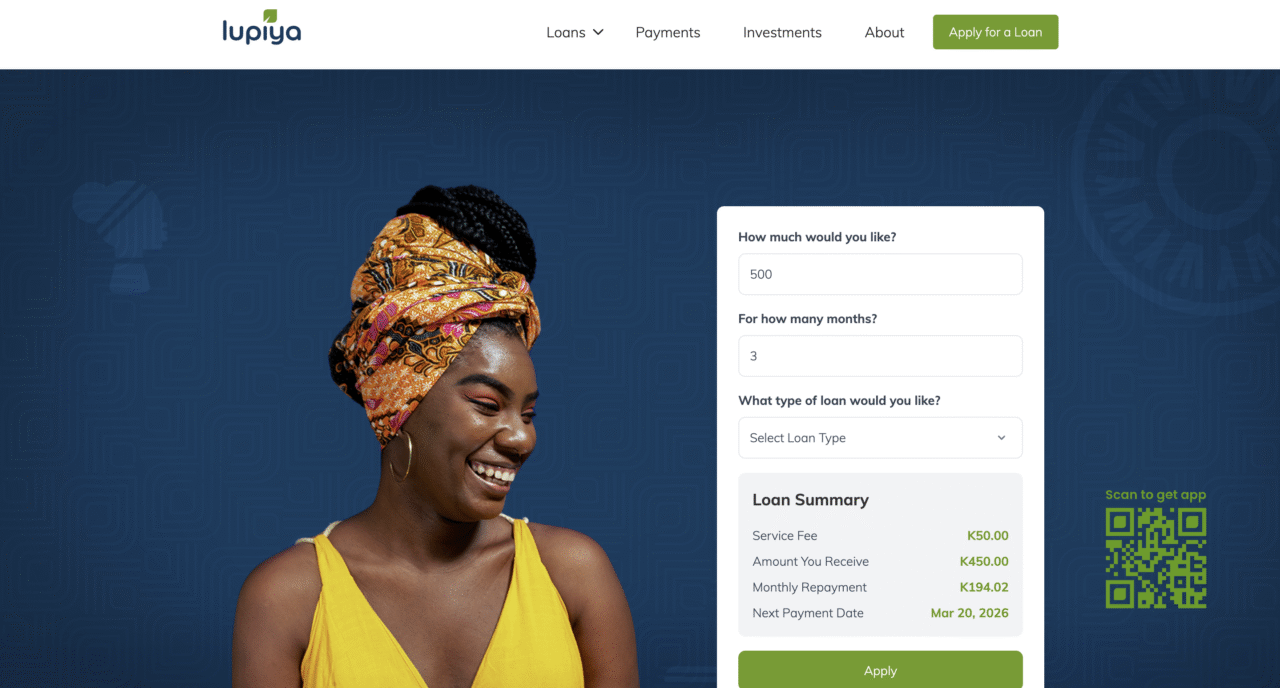

Zambian digital banking platform Lupiya has raised $11.25 million in Series A funding. The round—nearly two years in the making—was led by IDF Capital’s Alitheia IDF Fund, and featured participation from INOKS Capital and KfW DEG, a German development finance institution. Lupiya will use the capital to bolster the digital bank’s technology infrastructure, grow its product range, and enter southern and east African markets beyond Zambia’s borders.

Founded by Evelyn Chilomo Kaingu (CEO) and Muchu Kaingu (CTO) in 2016, Lupiya serves unbanked and underbanked communities in Zambia with credit products and digital payment services via its Lupiya Pay offering. The company has partnered with Mastercard to access payment rails to enable digital transactions and is part of the card network’s financial inclusion strategy. Previous investors in the firm include Enygma Ventures, which contributed $1 million to the company’s coffers. Lupiya has opened an additional funding round this year—alongside its Series A—dedicated to scaling its lending business, enhancing its embedded finance offerings, and bringing Lupiya Pay to new markets.

Lupiya was one of the first companies to earn approval from the Security Exchange Commission in Zambia to offer investments through peer-to-peer lending. Launching this service in-country in 2022, Lupiya expanded operations to Tanzania the following year. Lupiya offers personal loans including collateral-backed loans and salary advances, as well as business financing, invoice discounting, and agriloans. Customers can use Lupiya to send and receive funds via mobile money, P2P, or bank accounts.

According to the World Bank, Zambia’s financial inclusion rate has improved significantly in recent years, climbing from 59.3% in 2015 to 69.4% in 2020. Regional disparities are significant, however, with Lusaka Province, home to the capital city, Lusaka, having a financial inclusion rate of more than 87%, with more rural areas having inclusion rates of approximately 40%. The landlocked country shares borders with the Democratic Republic of Congo, Angola, Zimbabwe, Mozambique, Malawi, and Tanzania.

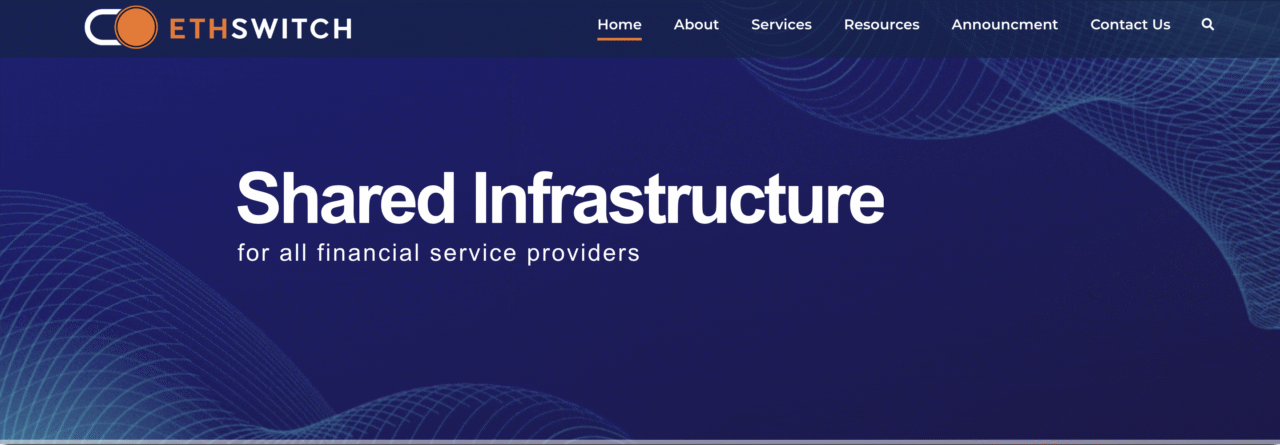

Ethiopia goes live with instant payments

Instant payments are sweeping the globe—and now businesses, communities, and banks throughout Ethiopia will be able to leverage the technology to provide centralized automated reconciliation, new card and e-wallet services, and more.

In partnership with the National Bank of Ethiopia, the country’s national switch EthSwitch has launched Ethiopia’s National Instant Payment System. Powered by BPC’s SmartVista platform, the system was officially introduced in December 2025, and now connects 32 banks, 12 MFIs, three PSOs, and three PIIs. The unveiling of EthioPay-IPS will enable EthSwitch to offer banks and other financial institutions modern payment rails capable of delivering faster and more economical payment transactions. These include account-to-account and wallet-to-wallet transfers, payments with interoperable QR codes, as well as requests-to-pay and alias-based payments that allow users to transfer funds using a simple identifier.

BPC’s SmartVista suite is a modular payment processing solution for banks, financial institutions, payment service providers, and fintechs. The technology combines banking, commerce, and mobility platforms to facilitate digital banking, payment processing, ATM and switching, fraud management, financial inclusion, and more. Founded in 1996 and headquartered in Switzerland, BPC has more than 500 customers across 140 countries.

Established in 2011, EthSwitch is a share company owned by Ethiopia’s private and public banks, as well as the National Bank of Ethiopia, MFIs, PIIs, and PSOs. The organization has a mandate to support the modernization of Ethiopia’s payment system and to enhance financial inclusion throughout the country. This includes EthSwitch’s 2016 initiative to enable the interoperability of ATMs and POS terminals operated by the nation’s banks.

“Our goal is to provide simple, affordable, secure, and efficient digital payment infrastructure to every retail payment provider and through them, to every Ethiopian,” EthSwitch Chief Portfolio Officer Abeneazer Wondwossen said. “With SmartVista, we have built an interoperable nationwide ecosystem for instant payments that is locally governed, future-ready, and open to innovation. This launch is a point of pride for Ethiopia and a milestone for our financial sector.”

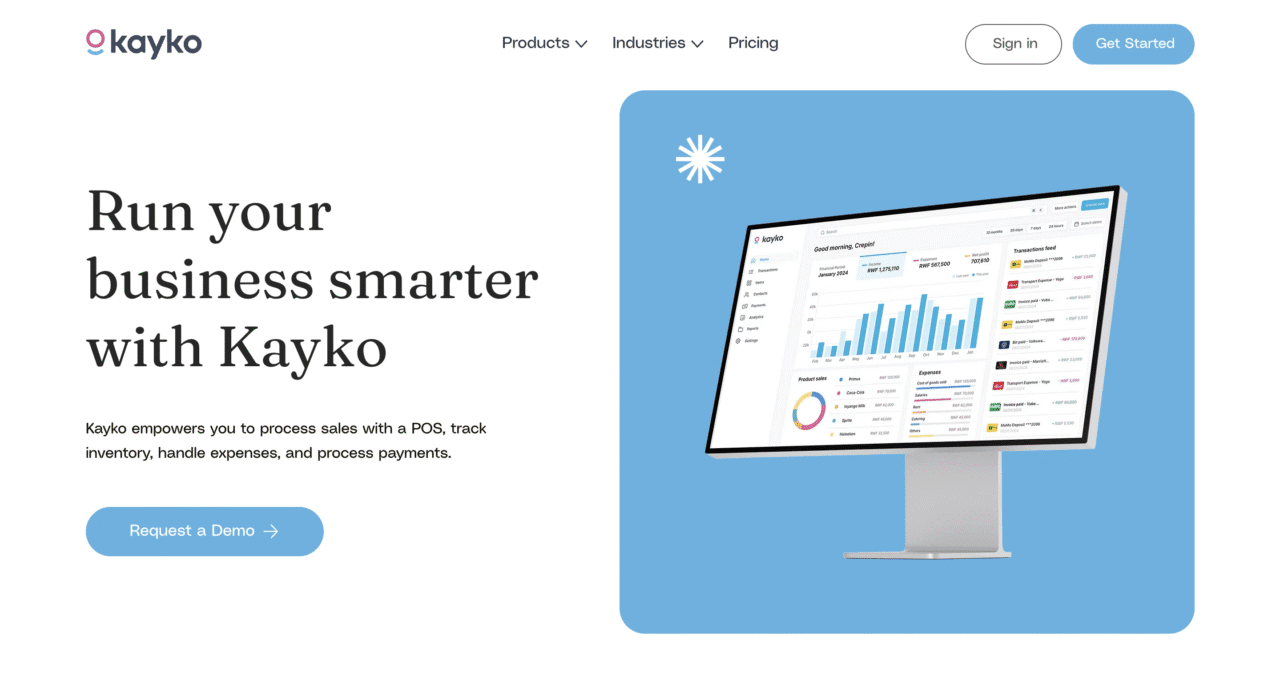

Kayko Raises $1.2 million to help SMEs in Rwanda

Kayko, which offers a small business financial management platform for companies in Rwanda, has secured $1.2 million in seed funding. Participating in the investment were Burrow Capital, the Luxembourg Development Agency, and Hanga Ignite by BRD and develoPPP Ventures. The company, founded in 2021 by brothers Crepin and Kevin Kayisire, will use the capital to fortify its infrastructure, expand its data capabilities, and build credit scoring and lending tools based on real transaction data.

Kayko serves more than 8,500 Rwandan SMEs with bookkeeping, inventory, and tax support. The fintech helps boost SME access to credit in a country in which many businesses have incomplete or informal financial records that make it difficult to secure financing or to scale operations. For these and other small businesses, Kayko provides a point-of-sale and business management system that helps them process sales, track expenses, and accept payments, while turning everyday business activity into structured financial data for analysis and insights.

Kayko’s funding news coincides with the Kigali-based fintech securing an Electronic Money Issuer (EMI) license from the National Bank of Rwanda (NBR). “With this license, we move from planning to execution,” Crepin Kayisire said in a statement on the company’s LinkedIn page. “We can now operate regulated payments, merchant wallets, and data-driven financial services that improve access to financing for small businesses.”

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

South African crypto platform Luno introduced crypto and tokenized stock bundle.

Blockchain infrastructure provider Binance and African mobile network operator Africell announced a collaboration to boost blockchain education and digital asset literacy across Africa.

Ethiopia’s national switch, EthSwitch, launched the country’s National Instant Payment System, in partnership with the National Bank of Ethiopia and powered by BPC’s SmartVista platform.

Central and Eastern Europe

The Bank of Lithuania supplemented the electronic money institution (EMI) license for TransferGo Lithuania, enabling the fintech to expand beyond money transfers and payment account services.

Open banking solutions provider Salt Edge and financial management platform NoCFO teamed up to bring Pay by Bank to SMEs in Germany and Finland.

US-founded banking and investment platform Fasset announced plans to enter the Pakistan market via a partnership with Habib Rafiq Limited (HRL).

Latin America and the Caribbean

Uruguayan fintech dLocal partnered with online English-language platform Open English to introduce a new payment method, Bre-B, for students in Colombia

Visainked a deal to acquire Argentinian payment companies Prisma Medios de Pago and Newpay from private equity firm Advent International.

Peru’s Banco de la Microempresa selectedTemenos SaaS to modernize its core banking infrastructure.

We’re fresh off an outstanding FinovateEurope conference in London (meet our Best of Show winners!) and already gearing up for our Spring event in San Diego. In the meanwhile, here’s a look at some of the fintech headlines that have crossed the wire in recent days. Be sure to check back here at the Fintech Rundown all week long for updates!

Digital banking

Oklahoma-based Blue Sky Bank partners with Jack Henry, deploying the fintech’s Banno Digital Platform along with other integrated solutions.

UK-based embedded insurance company Wriskacquired real-time financial intelligence platform Atto to build an integrated embedded finance platform.

DeFi

Payoneerteams up with stablecoin infrastructure platform and Stripe company Bridge to support its launch of new embedded stablecoin capabilities.

Netherlands-based paytech and stablecoin issuer Quantozteams up with Visa, enabling the firm to issue irtual Visa debit cards as serve as a BIN-sponsor for third-party fintechs and platforms.

Welcome to Finovate’s final Fintech Rundown of 2025! DeFi and crypto have dominated the fintech news in recent weeks, with some companies in the space launching stablecoins and stablecoin-related services, while others announce expansion into new markets. We will update this post over the next several days to keep you informed on the final big headlines of the year.

Visa has launched USDC stablecoin settlement in the US, enabling issuers and acquirers to settle transactions in Circle’s dollar-denominated stablecoin using blockchain infrastructure.

Cross River Bank and Lead Bank are piloting the capability to deliver faster, always-on settlement and improved treasury efficiency while remaining compatible with existing payment rails.

The move signals stablecoins’ shift from experimentation to bank-ready infrastructure.

Visaunveiled today that it has launched stablecoin settlement in the United States. The payments giant is partnering with Circle’s USDC dollar-denominated stablecoin to enable US issuers and acquirers to settle with Visa in USDC.

USDC settlement relies on blockchains to offer issuers faster money movement and seven‑day settlement windows that will improve both speed and liquidity, modernized treasury management with automated treasury operations, and interoperability between traditional payment rails and blockchain-based payments.

“Visa is expanding stablecoin settlement because our banking partners are not only asking about it— they’re preparing to use it,” said Visa’s Global Head of Growth Products and Strategic Partnerships Rubail Birwadker. “Financial institutions are looking for faster, programmable settlement options that integrate seamlessly with their existing treasury operations. By bringing USDC settlement to the US, Visa is delivering a reliable, bank‑ready capability that improves treasury efficiency while maintaining the security, compliance, and resiliency standards our network requires.”

Piloting the launch are Cross River Bank and Lead Bank, which are leveraging the Solana blockchain to settle with Visa in USDC. Visa is planning broader availability in the US in 2026. Cross River Bank, a leading infrastructure provider that offers embedded financial solutions, reinforces the importance of true interoperability. “Fintech and crypto innovators increasingly ask us to bring stablecoins into their existing product suite,” said Gilles Gade, Founder, President and CEO of Cross River. “A unified platform that natively supports both stablecoins and traditional payment networks is the foundation for how value will move globally. As one of the first US banks to enable USDC settlement with Visa, we’re demonstrating how a tech-forward, deeply integrated banking partner can connect blockchain networks and legacy systems at scale.”

Today’s announcement comes the same week that Visa Consulting & Analytics launched its Stablecoins Advisory Practice to offer education and guidance on market fit and implementation. VyStar Credit Union and Pathward are early participants in the program, which they will use to find new opportunities in the $250 billion stablecoin market.

Visa, which became one of the first major payment networks to settle in stablecoins in 2023, has been positioning itself at the forefront of the stablecoin revolution. Last month, the company’s monthly stablecoin settlement volume passed a $3.5 billion annualized run rate threashold.

Visa’s move to bring USDC settlement to the US shows that the early momentum in stablecoin activity this year is set to continue into next year as the payment rail moves from experimental to a bank-ready settlement tool. By embedding stablecoin settlement directly into its network, Visa is making programmable, always-on settlement a practical option for traditional banks seeking to improve liquidity management, shorten settlement cycles, and bridge existing payment rails with blockchain infrastructure.

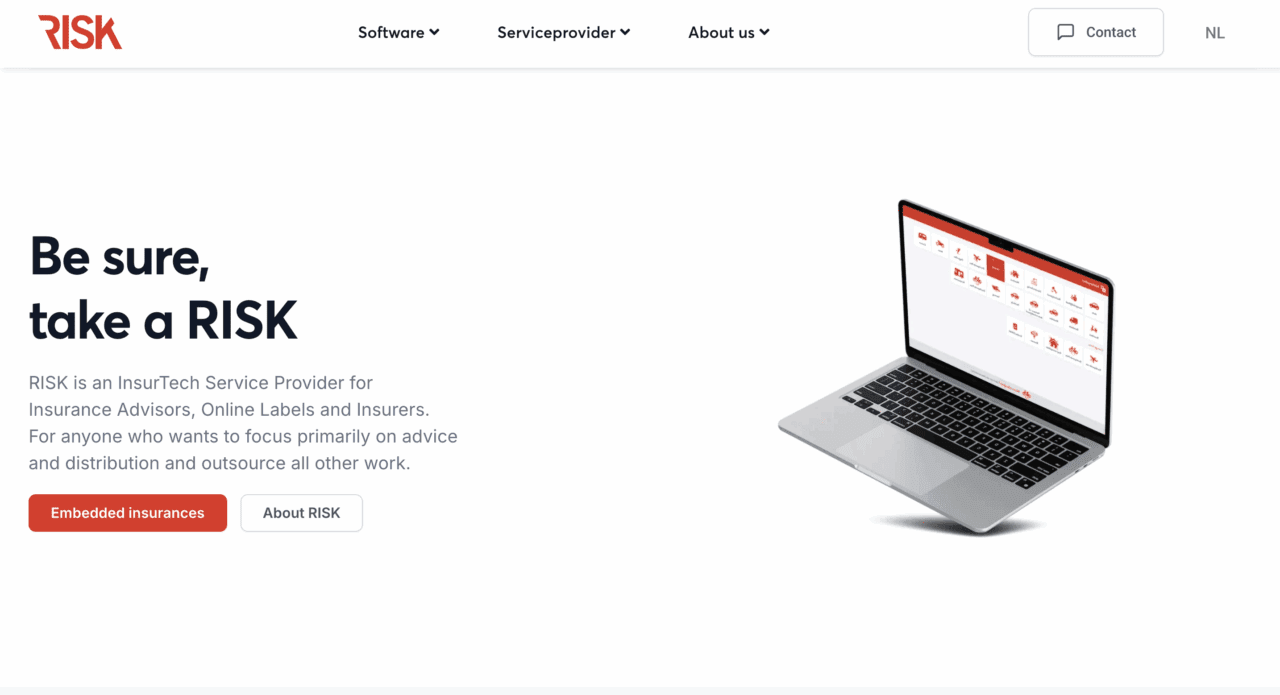

Dutch insurtech RISK has acquired Amsterdam-based savings app Dyme. Terms of the transaction were not disclosed. The deal will enable Dyme to boost its presence in the Netherlands as well as enter the German market. Courtesy of the agreement, both Dyme’s brand and management team will remain intact.

“From being featured on Dragon’s Den to becoming one of the largest finance apps in Europe and reaching profitability, our mission has always been the same: helping people take control of their money,” Dyme noted on its LinkedIn Page. “This step opens up some great opportunities for Dyme and its customers: expand the product, especially with great insurance packages and service, reach millions more people through the RISK ecosystem, and take Dyme international, beginning with Germany.”

Dyme currently has more than 600,000 consumers who have linked their bank accounts to the Dyme platform. The company’s app serves as a personal financial assistant to help users lower costs, and uses smart algorithms to automate subscription cancellations and provide financial guidance. Dyme announced its first profitable quarter in 2024, and has said that it has helped users save more than €40 million since inception. The acquisition will combine RISK’s market expertise and technological platforms with Dyme’s user-friendly financial solutions that enable users to easily manage their expenses, budgets, and more.

RISK offers an advanced IT platform, SureBase, that assists financial advisors, online labels, and insurers in product comparison and distribution. SureBase, according to RISK CEO Harm Vollmuller, will serve a key base for the new synergy between RISK and Dyme. “By combining that with our platforms and market knowledge, we can reach people at a time when financial breaking space is more important than ever,” Vollmuller said.

“This new facility is a testament to the trust and confidence Brand New Day Bank has placed in Factris and our vision for SME financing,” Factris CEO Brian Reaves said. “As we continue to scale across Europe, this partnership ensures we can meet the increasing demand for alternative financing and provide SMEs with the liquidity they need to thrive.”

Founded in 2017 and headquartered in Amsterdam, North Holland, Factris specializes in invoice factoring for small and medium-sized enterprises. The company offers selective factoring to enable companies to decide which specific invoices to factor, fund availability within 24 hours of invoice submission, credit insurance to protect against customer non-payment or bankruptcy, and debtor management for collections and account receivables.

Brand New Day Bank is a Netherlands-based digital-first, challenger bank and fintech that began operating in 2010. The financial institution serves both individuals and small-to-medium sized businesses with savings accounts, investment and pension products, tax-advantaged savings and investment solutions, and annuity payment services. Brand New Day Bank has more than €8 billion in assets.

Digital banking experience platform Plumeryannounced a suite of new features and integrations designed especially for credit unions in Canada. These new capabilities will give these institutions the ability to provide personalized, compliant, and modern digital banking experiences for their members.

The Amsterdam-based fintech leveraged a collaboration with Aequilibrium, a digital services and technology consultancy headquartered in Vancouver, British Columbia, to make sure its Canadian-ready platform is built based on the way that Canadian credit union members prefer to bank. This includes not just hyper-personalized, mobile-first, and intuitive digital journeys, but also support for everyday payments and transfers including billpay and Interact e-Transfers, and Canadian savings and lending products like GICs.

Plumery’s move comes as Canadian banks and credit unions face a range of challenges including evolving customer expectations, fintech competition, and the pressure to modernize their legacy systems. More immediately, Canadian credit unions are scrambling in the wake of Central 1 Credit Union’s announcement that it will wind down its digital banking platform Forge (formerly MemberDirect). More than 170 credit unions across Canada had been relying on the technology.

“With Forge winding down, Canadian institutions have a rare opportunity to modernize on their own terms, rather than being tied to outdated systems,” Plumery CEO and Founder Ben Goldin said. “Our platform provides an immediate, future-ready option that puts control back in the hands of credit unions. By working with Aequilibrium, we are combining global banking innovation with local expertise to deliver experiences that meet the unique needs of Canadian credit unions’ members.”

Founded in 2016, Plumery enables financial institutions to offer unique mobile and online experiences on top of either their modern or legacy core banking platforms up to 80% faster. Plumery’s technology features foundations that are pre-integrated into its digital banking journeys that accelerate app development and shorten time-to-market while maintaining complete control over both design and functionality.

India’s Bank of Baroda launched its eRUPI Person-to-Person (P2P) gifting solution.

TBC Uzbekistan extended financial services to non-residents.

Indian fintech Kiwi unveiled its interest-backed EMI on UPI.

Latin America and the Caribbean

Brazilian digital banking giant Nubank has applied for a US national bank charter.

Unlimit announced securing Principal Membership with Mastercard and Visa in Peru.

Brazi-based proptech Lastro raised $15 million in Series A funding in a round led by Prosus Ventures.

Asia-Pacific

Cambodian MSME-focused bank Chief Bank teamed up with payment solutions provider BPC to launch its new Chief Mobile 3.0 mobile app.

The People’s Bank of China opened a digital yuan operation center in Shanghai.

The Hong Kong Monetary Authority (HKMA) and the Hong Kong Science and Technology Parks Corporation (HKSTP) launched IADS Developer Hackathon to promote bank-fintech collaboration.

According to a report in Bloomberg, JP Morgan is going to make fintechs pay up if they want access to customer financial data. Fighting words? Or just signs of what’s to come? Check out this news and more in this week’s edition of Finovate’s Fintech Rundown!

Identity management

Digital identity platform Signicatacquires Dutch NFC-based digital identity verification solutions provider Inverid.

Lending

Digital lending platform Yabxlaunches GenAI-powered voice solution designed to increase financial literacy among its underserved borrowers.