This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Luxoftteams with Softbank Robotics America to bring its humanoid robot Pepper to life.

MicroStrategyreleases 3 new gateways to Microsoft Azure.

Woleet, a blockchain-based timestamp and signature app, is now available on Ledger Nano S.

Grubhub partners with PayPal’sVenmo on bill-splitting feature.

Avokasees positive trends for North American banks in its 2018 State of Digital Sales in Banking Report.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Entersekthires Sherif Samy as SVP for North American operations.

Visa and Billtrust team up to streamline B2B payment reconciliation and support automation of virtual card payments.

PayPalannouncesVemno is now payment option at more than two million U.S. retailers.

Narrative Sciencewins Microsoft Office 2017 App Award for Best Business Value.

TransCardpartners with ExpenseAnywhere to Deliver Automated Payment Process Management Solutions.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Albany, New York-based SEFCU choosesFiserv as technology partner.

FICOselects Amazon Web Services as its cloud provider.

SF Chronicle profiles mortgagetech innovator, Unison, in feature on downpayment assistance for Bay Area homebuyers. Join them next month in New York for FinovateFall.

GoBankingRates highlightsAutoGravity, M1 Finance, Venmo, Mint in list of best personal finance apps

ID.mehires Julie Filion as Chief Marketing Officer.

eMoney Advisormoving into Rhode Island offices, expects to hire 100 by 2020.

FlywireOffers Summertime Deal for International Tuition Payments with Mastercard.

StreetSharesadds Heather Tuason as new Chief Product Officer.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Seventeen years ago PayPal took on Wells Fargo’sBillpoint (joint venture with eBay) and Citibank’s (C2IT) fledgling P2P payment services. It wasn’t a fair fight. With a $400 million VC war chest and an all-star exec team (Elon Musk, Peter Thiel, Max Levchin, David Sacks, Reid Hoffman and so on), the fight didn’t make it past the first round. Within a year PayPal had a stranglehold on eBay payments due to its superior UX and aggressive business model.

Now the banks are back with Zelle, a rebranded version of the clearXchange that has been up and running for six years. The service already has great traction. In 2016, Early Warning, the bank-owned operator (see note 1), processed 170 million transfers totaling $55 billion for the 85 million customers of their big-bank owners. That works out to exactly 2 transactions per customer annually with an average of $320 per transfer.

The value transferred is three times the size of Venmo’s $17.6 billion in volume, though the number of Venmo transactions is probably higher, perhaps considerably higher if its average transaction size is in the $15 to $20 range implying 1 billion venmos last year.

Using Zelle

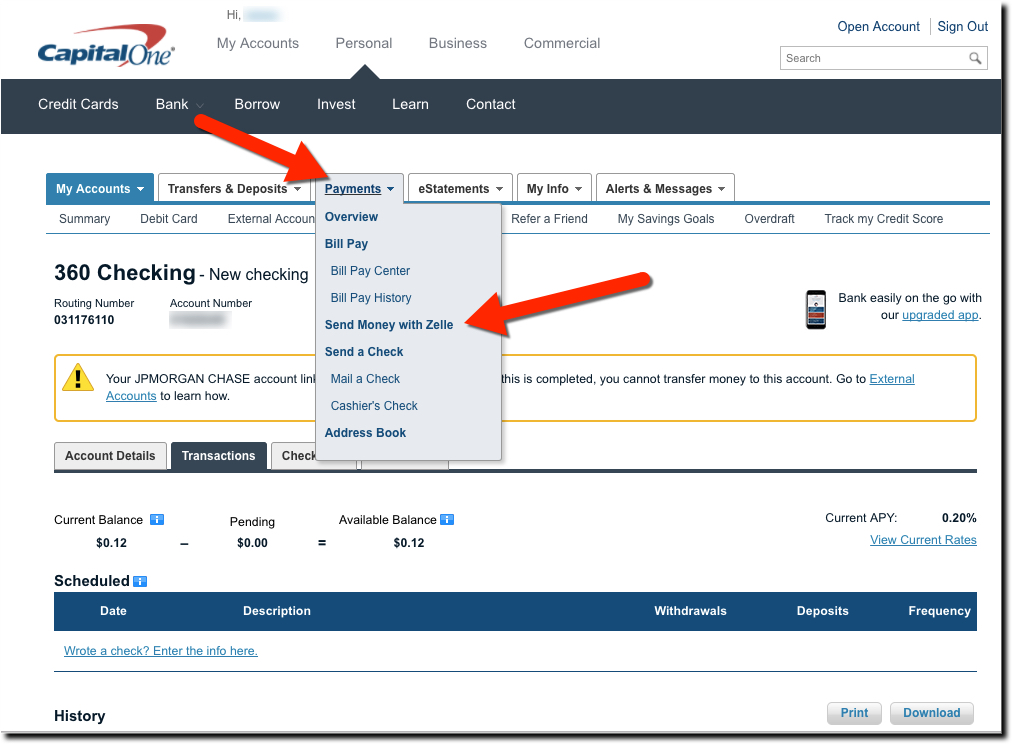

Yesterday and today I used the mobile and desktop Zelle from Capital One for the first time. Other than the glitch with my mobile phone number (see note 3), which would stop many consumers from going further, setup was quick and easy. The desktop version is pretty straightforward, with a Send Money with Zelle link in the middle of the Payments menu (see screenshot below). This assumes you know what Zelle is, or you just ignore it since it comes after the key words, “Send Money.”

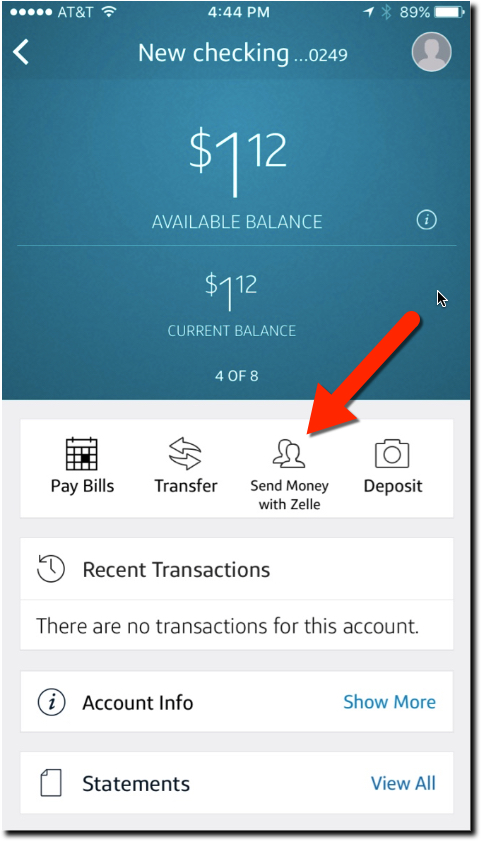

But the mobile UI is less intuitive. It wasn’t initially obvious how to use it because there is no Zelle or payments navigation item in the Capital One app…yet (it’s only been out since June 12). However, once you go to your checking account section, it’s one of the main navigation items at the top (see inset below).

I was initially surprised at what happened with my test payment. I sent a buck to my son (sorry, Paul I only had $1.12 in my account) and I was pleasantly surprised to find that my payment had been “qualified for expedited deposit” and he’d have the cash right away without the usual ACH delay.

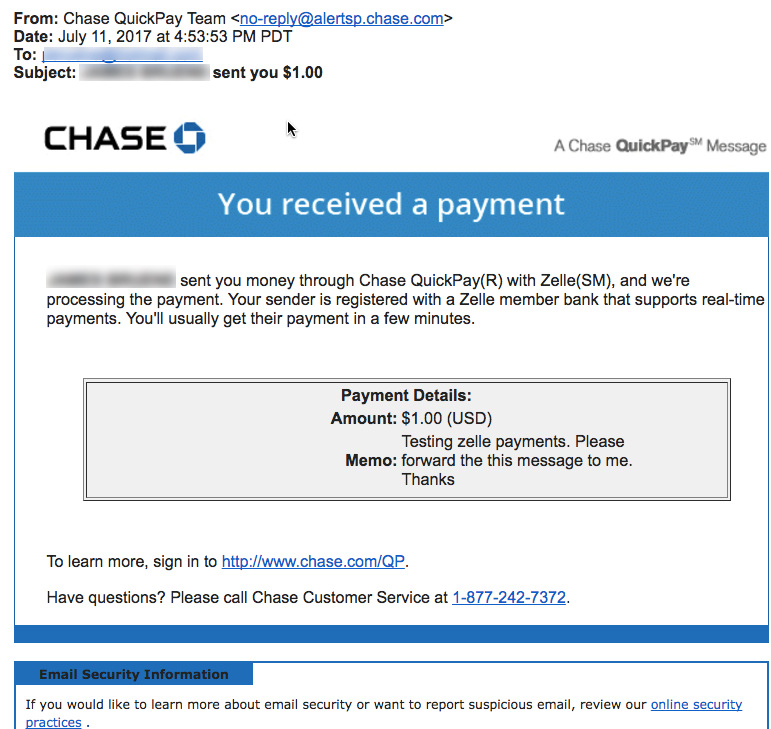

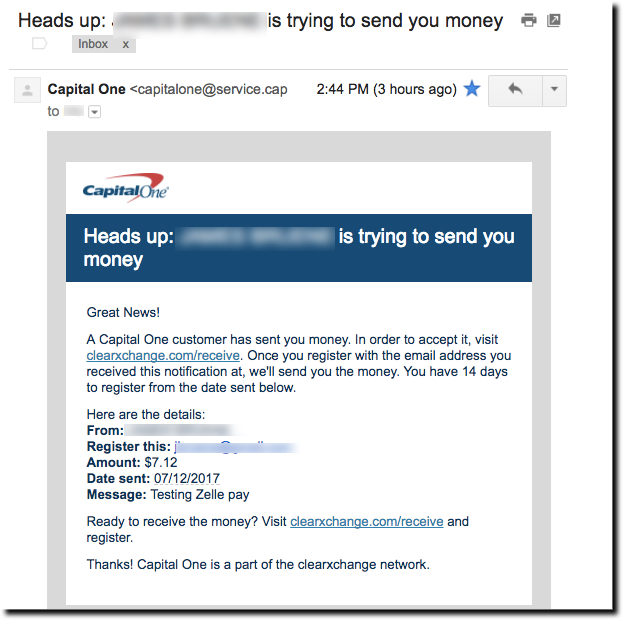

But when my son forwarded the email he received, I was surprised to find that my Capital One payment has morphed into a branded Chase QuickPay with Zelle. There was no mention of Capital One anywhere in the message (see screenshot #1).

That makes sense now. My son has a Chase account and was already registered with Chase QuickPay. If he’d not already been registered, he would have received a Capital One branded email (see screenshot #2 below).

Why the new brand?

Zelle/clearXchange will continue to grow at a good clip if its big-bank owners stick with it. It’s already 3x the size of media darling Venmo (owned by PayPal). But I’m not sure the massive investment in creating a new payments brand is worthwhile (cut to the boardroom discussion of a 2018 Super Bowl ad).

I get that they are trying to create another Visa/Mastercard network that consumers recognize and trust. But unlike credit transactions at the POS in the 1950s and 60s, p2p payments are relatively understood by consumers and have much less need of a third-party organization to achieve the network effects. The big banks are already wired to each other and what’s needed, what clearXchange was already offering, is just a simpler UX inside each bank’s online and mobile application. Adding the Zelle name to the mix seems like a step backwards on that front.

Maybe I’m wrong and we’ll all be Zelling money to Mars in a few decades. But I’m not convinced the new brand will stand the test of time.

Bottom line: Love the service, which I expect to flourish, but confused by the branding.

#1: Email to a pre-registered Zelle recipient banking at Chase

#2 Email to a Zelle recipient not registered with a participating bank

Author: Jim Bruene is Founder & Senior Advisor to Finovate as well as Principal of BUX Advisors, a financial services user-experience consultancy.

Notes:

Owners of Early Warning (aka Zelle) are: Bank of America, BB&T, Capital One, JPMorgan Chase, PNC, U.S. Bank, and Wells Fargo.

If I were any bank other than BofA and Capital One, I’d be crying foul over how the banks are listed in alphabetic order. On the desktop, it doesn’t matter (yet) since they are all above the fold. But on mobile, you can only see BofA and Capital One, and there is no indicator that you should scroll for more.

I received a fatal error message when I tried to use my mobile number as contact to send Zelle payments (see inset) from Capital One’s mobile app. This could be something particular to my account, but from the cryptic popup message, it sounds like my phone is registered at another bank. And that would be a big concern for most customers who would fear that identity thieves are hard at work draining their accounts.

Rabobank selectsFinastra (the merger of Misys and D+H) payment services hub for cross-border payments.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

PYMNTS reports: TransferWise To Move Headquarters Out Of UK Due To Brexit.

NICE Actimize Launches ActimizeWatch, a Fraud Analytics Optimization Solution.

Fiservto power core processing for SouthEast bank.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Virtual Piggybrings on President &CEO of Broad Street Consulting Advisors as its Senior Advisor.

Cachetstreamlines RDC check settlement process for Banks and Credit Unions.

Finovate/FinDEVr alums populate TradeStreaming Fintech’s companies to watch in 2017 list.

Finance Disrupted interviewsXignite CEO and founder, Stephane Dubois.

Venmo, LearnVest, Qapital, LevelMoney, and PayPalfeatured in PC Mag’s Best Mobile Finance Apps of 2017.

From Founder to CEO talks with GainX founder & CEO Angelique Mohring. See GainX at FinovateEurope 2017 in London in February.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

A look at the trending topics of the past two weeks, co-authored by Finovate’s research analysts David Penn and Julie (Schicktanz) Muhn.

Big handshakes

Cardtronics acquires DirectCash Payments

In a $460 million deal, Texas-based ATM operator Cardtronics has acquired Canada-based DirectCash Payments. The deal is expected to help Cardtronics expand into Canada and the United Kingdom. DirectCash Payments has 25,000 ATMs around the globe, primarily in Australia, Canada, and the U.K. Once the deal closes in Q1 of 2017, it will boost Cardtronics’ network to 225,000 ATMs across North America, Europe, and Asia Pacific.

Jack Henry & Associates (F10) teams up with Visa (F10)

In a new partnership, Jack Henry & Associates has integrated with Visa to allow customers to send P2P payments directly to a recipient’s Visa debit card. This eliminates the need for a recipient to provide their account and routing number to the sender. With increased competition in the P2P payments industry (PayPal/Venmo (FDNY 16), Square Cash, Zello), banks are feeling pressure to compete by offering faster delivery of funds. The partnership enables banks to offer funds-transfers a day sooner, or even same-day. Jack Henry began offering P2P payment capability in 2005 and expects the new method to boost usage.

Sberbank (F16) and MasterCard (F11) partner to launch ApplePay in Russia

Starting this week, Mastercard cardholders in Russia can now pay using ApplePay, thanks to a new partnership between Russian bank Sberbank and Mastercard. In a statement, the bank’s Deputy Chairman of the Executive Board, Alexander Torbakhov, said, “Apple Pay is driving the popularization of contactless payments in Russia and globally. Many of Sberbank clients actively use new technologies, and an increasing number of them will prefer cash-free and contactless payment using their smartphones.”

This is the Russian bank’s second big move this week. On Monday the company inked a partnership with Hyperledger to begin working on the Hyperledger Project.

PayPal (F11) and Vodafone partner for in-store NFC mobile payments

Acting on a partnership it first initiated in February, PayPal partnered with Vodafone to enable U.K. users to make NFC payments from their PayPal accounts using their Android phones. The agreement enables consumers to make transactions of up to £30 ($36.60) at 400,000 retail locations. For more expensive purchases, Vodafone Pay users can use their Vodafone wallet (launched in 2013), which requires a PIN.

The NFC payment capability with Vodafone was piloted in Spain. PayPal also has agreements in place with other global telcos, including America Movil, Telcel, and Claro.

Regulation

Happy birthday, U.S. EMV. It’s been one year since EMV regulation in the United States was placed into effect. If you live in America, you’ve likely noticed that adoption is low. In fact, according to a recent report from Mastercard, 88% of consumers have been issued chip cards, but only 33% of merchant locations accept them.

Mobile POS company CardFlight (F13) released data on EMV usage in the U.S. over the course of the year and found:

78% of cards now contain EMV chips, up from 46% in October 2015

American Express leads the way in EMV card issuance, with 96% of their cards now EMV-enabled

Mastercard is the runner-up: 71% of cards issued contain an EMV chip

Though usage remains low, Mastercard reported this week that it has seen an overall decrease in fraud since the EMV change. The company reports that between April 2015 and April 2016, retailers who have transitioned to EMV experienced a 54% decrease in counterfeit fraud.

Ready, set, ACH

As of September 30, a new rule from NACHA requires all banks to process incoming same-day ACH credits. Most ACH payments are currently settled on the next business day: the new rule-change offers originators the option to send an ACH transaction to any recipient account for same-day processing. NACHA has imposed a same-day fee on every same-day ACH transaction to help financial institutions receiving the funds to recover the cost to enable same-day ACH. Phase two of NACHA’s Same-day ACH initiative will take effect 15 Sept 2017.

Capital One integration with Amazon Echo

Technologies: AI, chatbots, and natural language processing (NLP)

The industry-wide obsession with chatbots continues. Finovate last month showcased a dozen variants on the chatbot theme. One of our newer alums, Personetics (F16), is even holding a Chatbot Bootcamp next month in San Francisco. And our chatbot-banking post in March is our fourth most-read. But the bigger conversation is around natural language processing (NLP) and how it can be used to retrieve information and perform tasks. A new report from Juniper Research estimated that NLP would drive $2.1 TRILLION in annual purchases via mobile five years from now (2021).

The tech world is in a tizzy over Amazon’s Alexa capabilities. We showcased two demos of her at FinovateFall from BankJoy (F16 demo) and FIS (F09) (F16 demo). Capital One is the only bank with a live Alexa integration (called “Skill”), but Lloyds Bank put together a proof of concept this spring. There are currently 2,904 skills listed in the unofficial Alexa database, but very little in the financial realm. Expect to see much more activity as financial institutions and fintech companies develop applications using Amazon’s Alexa and the new Google Assistant.

Sibos 2016 celebrates the blockchain

The annual Sibos 2016 conference in Geneva took place at the end of September—between the last Fintech Trending meeting and this one. Organized by SWIFT, Sibos is considered to be the world’s premier financial services event covering areas such as payments, securities, cash management, and trade.

So what was big at Sibos 2016 this year? The blockchain. 2016 was the first year that Sibos dedicated a track “exclusively to distributed ledger” technology. And the event’s startup-industry challenge was all about how to use the blockchain in the securities industry. The three startups that won the challenge will develop PoCs using technologies like smart contracts (SmartContract), distributed ledgers (Rise Financial Technologies), and open-source blockchain platforms (Coin Sciences).

Some have ascertained the irony in SWIFT’s embrace of the blockchain: Its $6 billion payment-messaging service is one of the technologies “widely perceived to be at risk for disintermediation” by blockchain technology. And indeed, companies like Finovate alum Ripple (F13) have made great strides in helping FIs like Bank of America, Santander, and Royal Bank of Canada use distributed-ledger technology to provide a global blockchain-payments network with “near-instant” settlement. Interestingly, Ripple recently hired former SWIFT board member Marcus Treacher as its new global head of strategic accounts. Treacher told CoinDesk in September that SWIFT was the “de facto way everyone moves money through countries.” And cross-border payment is something he specifically believes Ripple “can do better.”

Global Banks Partner to Form Blockchain Payments Network—CoinDesk

Speaking of blockchain, a number of companies with blockchain and distributed-ledger technologies will be presenting at our developers conference, FinDEVr Silicon Valley, next week. These companies include PwC, which will present its blockchain-as-a-service technology to improve trade finance, and IBM with its hyperledger implementation in the cloud that helps manage and test blockchain-dev projects. Also on hand will be distributed database specialists Aerospike (FD16) and Cognitect (FD16).

InsurTech rising

From FT Partnersrecent report on the boom in insurance-technology innovation, to InsurTech Rising’s event, Informa, to launch on 21 Oct, this area of financial technology is garnering increasing attention.

Why? As FT Partners pointed out in their 247-page report, the insurance industry is one of the areas of finance that so far has been least affected by the technological disruption nearly commonplace elsewhere. The insurance industry is a multitrillion dollar business; property and casualty insurers alone generated more than $64 billion in net income in 2014. And it sits at the nexus between the drive to better engage customers (is there anything enjoyable about insurance from a consumer perspective) and the need to accommodate complex and shifting regulatory landscapes (something the rest of finance is becoming increasingly familiar with).

What are the focuses of insurtech? Most technology innovation in the area revolves around trends in distribution and administration: data and analytics, and marketing and customer engagement. This includes everything from the kinds of products offered to consumers, such as micro-insurance, to using mobile channels and interactive technologies to make insurance products easier to understand, choose from, and purchase.

How are industry players responding and what to watch for? From partnering with innovative startups to acquisitions, incumbent insurance firms are increasingly aware of the challenge. FT Partners reports that more than 40% of traditional insurers surveyed by Ptolemus Consulting said they were planning to “acquire, or have already acquired, innovative startups to help them expand their digital capabilities” and more than half say they have already invested in social media, data mining, and predictive modeling. Nearly 70% have embraced mobile technology.

Wave Mechanics: FT Partners Report Highlights Trends Driving Rise of Insurtech—Finovate

Prepare for the InsurTech Wave: Overview of Key Insurance Technology Trends—FT Partners

——

Note: Finovate alums have the year of their first appearance listed after their name. For example, FIS first appeared at Finovate in 2009, so there is a (F09) after their name, with a link to that first demo.

U.K.-based challenger bank Atom opens to the public. The bank’s iPhone and iPad app is built on the Unity gaming platform and is the only way to access the mobile-only bank. Atom has a customer service team equipped with AI and machine learning, and has bolstered its security using voice and face biometric login. Atom Bank is the first of a handful of U.K. challenger banks set to launch this year, including Mondo, Starling Bank, and Tandem. Atom is headquartered in Durham and is already valued at almost $190 million. Check out Business Insider’s coverage.

Deals

Akamai (FEU 15) acquires Soha Systems, which offers secure access as a service for enterprises. This matches well with Akamai’s aim to offer cloud-based services to enterprises, and places it in a good position for a potential acquisition. See our coverage.

Jack Henry & Associates (FF 15) collaborates with Visa (FDSV 14) to accelerate P2P payments to debit cards. This may help banks compete with other services that have sped up settlement times, such as Zelle (formerly clearXchange) and Venmo (FS 13). See the press release.

IBM (FF 16) announced a $200 million investment for a new global headquarters for its Watson IoT business. The headquarters will be located in Munich and is one of IBM’s largest-ever investments in Europe. This move is part of a $3 billion initiative to bring Watson’s computing expertise into the world of IoT. See IBM at FinDEVr Silicon Valley, 18/19 Oct 2016. See VentureBeat’s coverage here.

Banking Technology reported that Misys (FEU 15) is preparing to issue an IPO in Nov 2016 with a $6.9 billion float. Advisory firm Moelis will be overseeing the move. Misys was delisted from the London Stock Exchange in 2012 when it merged with Turaz. Misys CEO Nadeem Sayed says going public is a “logical step in our evolution.” See Banking Technology’s coverage.

Aire (FEU 15) raised $2 million. Along with the funding announcement, the alternative credit-scoring platform announced it is now authorized and regulated by the Financial Conduct Authority (FCA), the U.K.’s financial regulator. This places it on a more level playing field to compete with the big three credit bureaus. See our coverage.

Tech

Thomson Reuters (FF 12) unveils blockchain-dev platform, BlockOne ID. Built for Ethereum, BlockOne ID is an experimental framework in which app owners can manage access to their blockchain contracts in a controlled environment. See Banking Tech’s coverage.

Currency Cloudpartners with Arkea Banking Services to provide faster payments and better reconciliation. Join Currency Cloud in New York next week for FinovateFall 2016.

A look at the trending topics of the past two weeks, co-authored by Finovate’s research analysts David Penn and Julie Schicktanz.

Payments

Venmo competition heats up

We’ve lately noticed more P2P payment app competitors trickle in. They have Braintree-owned Venmo’s (FD2016; F2013) millennial-focused social components stamped all over them:

Founded by former N26 employees, Cookies launched this week to offer Germany-based users a free P2P payment solution. The simple UI has a messaging platform for senders and recipients to engage with, and it allows people to include emojis with their payments (Cookies calls them paymojis). Some paymojis have special powers, for example, a lightning bolt that allows users to send the money faster. Unlike Venmo (more like Square Cash), users do not maintain a balance on Cookies; instead, Cookies connects directly to a user’s bank account.

Tilt originally began as a crowdfunding platform but launched P2P payments functionality this week. While the user interface is very Venmo-esque with emojis, gifs and a social feed, Tilt has a few differences. Aside from being based on a crowdfunding model where users pool money for weekend road trips and pizza nights, Tilt lists fundraising campaigns in its social feed and is available outside the U.S. Tilt has already launched in the U.K., Canada, and Australia.

Our last Fintech Trending post described the growth of P2P payment service clearXchange, which scored Fiserv (F2016) as a distribution partner and added MasterCard Send debit cardholders to its client base. The Wall Street Journal reported this week that clearXchange is rebranding to Zelle in October to step up its competition with Venmo. While there is no word yet on UI and UX specifics such as emojis with special powers, gifs, and social feeds, there have been a few questions about the name Zelle, which Urban Dictionary defines as “a girl who is attractive and intelligent.”

New mobile payments methods are everywhere (and that’s not a good thing)

Last week, CVS joined a group of other retailers, banks, technology providers and payment services companies to launch its own mobile wallet. With the launch, the pharmacy intends to streamline the use of its rewards points with point-of-sale (POS) payments, but what it may actually be doing is adding yet another wet log to the slow-burning, mobile POS-payments fire.

The issue lies in part with low consumer interest and adoption; it’s still faster to swipe (or insert) your credit card than to take out and unlock your phone, open an app, and try to convince the cashier it is a legitimate way to pay. Also at fault is the large, fragmented number of suppliers. We’ve lost count, but here’s a partial list:

Apple Pay

Android Pay

Cake Pay

CVS Pay

Walmart Pay

MasterPass

Samsung Pay

Wells Fargo Wallet

Chase Pay

Starbucks

Capital One Wallet

Other news in the payments space

UnionPay’s mobile payments launched in Canada. The China-based payments network is the third largest in the world (following Visa and Mastercard). The launch enables Canadian cardholders to use UnionPay’s QuickPass EMV cards or app to pay at participating merchants.

Visa (FD2014; F2010) is in discussions with Nigerian banks to roll out mVisa, its QR code-based mobile payments service, by the end of this year. Consumers will be able to use their smartphone or feature phone to pay for goods with merchants, send domestic P2P payments, and access cash.

Apple expands carrier billing to Taiwan and Switzerland. The Taiwanese carrier is EasTone and while there’s no word yet on the carrier in Switzerland, it is expected to be Swisscom. This expands Apple’s carrier-billing partnerships, already operating in Germany and Russia, to four countries.

A big deal in ATMs gets a second look

Diebold (F2014) finalized its merger with German ATM maker Wincor Nixdorf last week, a deal that combined two of the largest three ATM companies. The deal closed for $1.8 billion and makes Diebold Nixdorf the world’s largest ATM company, claiming a third of the worldwide market.

Days after unveiling the newly formed entity, the ATM giant is facing an “in-depth merger investigation” from the U.K. Competition and Markets Authority. The agency said that it is concerned the deal will reduce the number of companies supplying ATMs in the U.K. The companies have until April 26, 2017, to “offer undertaking to address competition concerns.”

This further highlights the opportunity for disruption in the ATM space, a realm where companies such as Liqpay (F2013) have showed off solutions that allow cardholders to use their smartphones for a contact-less way to withdraw cash from ATMs.

Lending

Making Sense of Student Loan Debt—notwithstanding Bernie Sanders’ promises of free college tuition for all, the challenge of student loan debt isn’t going away anytime soon. Unfortunately, a recent report from the Consumer Financial Protection Bureau (CFPB) suggests that loan servicers are a part of the problem, at least when it comes to income-driven repayment plans.

As reported in PYMNTS.com, much of the problem is bureaucratic, with “delays and rejections” that can expose student borrowers to greater interest, penalties, or even lost eligibility. “Student Loan servicers continue to fall short when it comes to helping borrowers address $1.3 trillion in student debt,” CFPB Director Richard Cordray said in a statement. “It’s time servicers focus more effectively on processing applications for income-driven repayment plans properly.”

And the CPFB is focused on more than just the student loan servicers. Wells Fargo was slapped with a $3.6 million fine this week for “illegal fees … and [depriving] others of critical information needed to effectively manage their student loan accounts,” according to Cordray. Wells Fargo said that it has already made changes to the processes criticized by the CPFB in its consent order.

It’s impossible to read about student loan debt in the headlines and not think of Student Loan Genius (F2016), which made its Finovate debut this spring. The company empowers employers to help millennial workers in particular pay off their student loan debts faster. This not only helps reduce what is often an onerous debt load (especially relative to the income of the average recent college graduate), but also enables young workers to start saving better.

Development

Make Room for Dev—Google(FD2016 ; F2011)is the latest major technology company dedicating major square footage to support collaboration between “local and international developers and startups.” Writing in the Google Developers Blog, Global Lead Roy Glasberg revealed that more than 14,000 square feet at 301 Howard Street would be the home of a variety of dev-friendly events ranging from Google Developer Group meetings to Tech Talks. The new facility will also host Google’s equity-free, three-month accelerator for emerging market startups, LaunchPad Accelerator.

Earlier this summer, IBM (F2016) announced the opening of its developer space, Bluemix Garage, in New York City. The New York garage, IBM’s sixth, will be hosted by developer networking and education organization, Galvanize. In the U.K., Allied London announced a new fintech co-work space called “The Vault” that will occupy 20,000 square feet in Manchester’s business neighborhood. Meanwhile in Germany, ING-DiBa announced its sponsorship of the latest fintech hub in Frankfurt.

Meanwhile in Asia, PayPal (FD2014; F2012) announced this week the opening of an innovation lab in Singapore, its first such lab outside the U.S. The lab joins PayPal’s other Indo-Asia Pacific innovation lab in Chennai, India, and will be focused on improving productivity among SMEs in the food and beverage industry. We also learned this week that the Monetary Authority of Singapore is setting up a fintech innovation lab, Looking Glass @ MAS1 in that country.

ING-DiBa backs new Frankfurt fintech hub – Finextra

PayPal opens Innovation Lab in Singapore for next generation fintech – Deal Street Asia

Singapore’s MAS gets in on the fintech innovation lab game – Tech in Asia

Fintech Groups Will Unite into Global Hubs – Fortune

Life in the blockchain

Swiss-based UBS announced a year ago its work on a virtual currency—Utility Settlement Coin—to facilitate faster transaction settlement. This week, UBS announced it has joined forces with Deutsche Bank, Santander, BNY Mellon, and ICAP to convince central banks to agree to a commercial launch by 2018. Competition for this digital currency include Citigroup’s Citicoin, Goldman Sachs’ SETLcoin, and a similar, yet-unnamed, offering from JPMorgan.