Personal finance solutions fintech Meniga launched a new product called Fini, an MCP server that enables banks to bring agentic AI into their existing platforms.

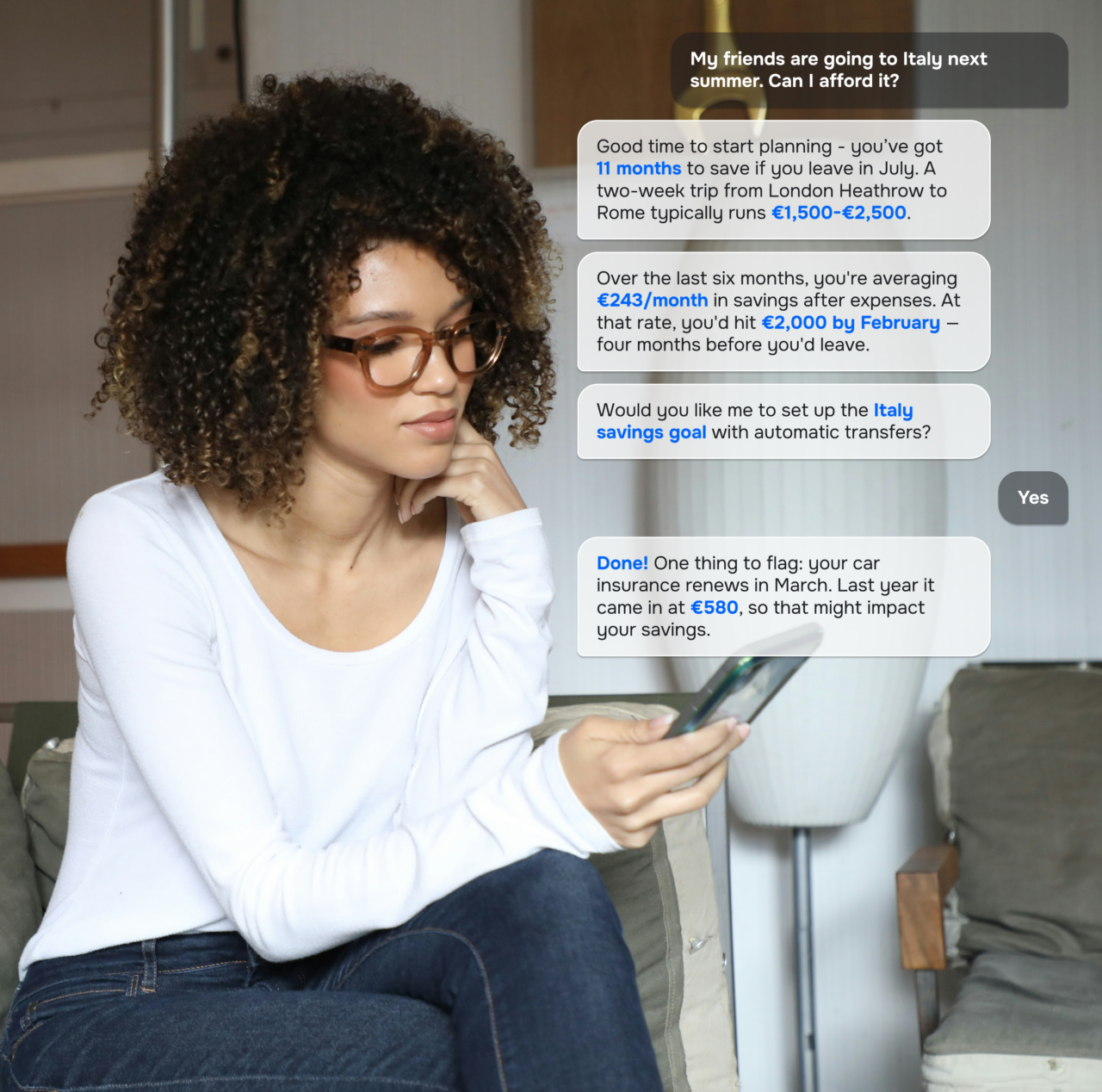

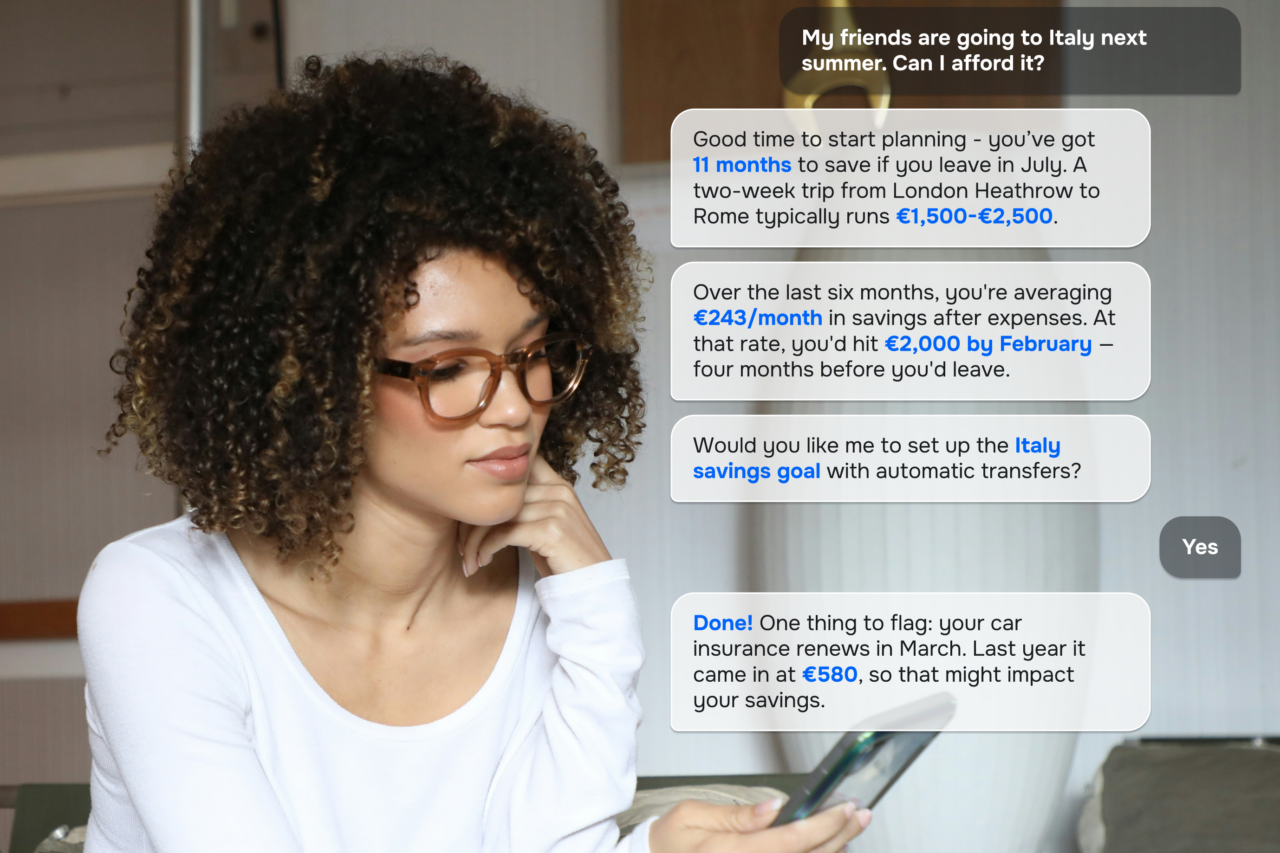

Fini, which was built with the input of five large banks, serves as the bridge between a bank’s preferred large language model (LLM) and Meniga’s personal finance, enrichment, and insights capabilities. Rather than building its own AI model, Meniga enables banks to pair Claude, GPT, Gemini, or another LLM with the company’s financial intelligence platform, allowing customers to ask questions about their finances in natural language within the bank’s website or mobile app.

Founded in 2009, Meniga serves over 100 million banking customers across 30 countries. The UK-based company’s clients include UniCredit, Groupe BPCE, UOB, Swedbank, SAB, Tangerine, and Riyad Bank. Meniga’s intelligence and personalization layer helps banks turn financial data into insights and proactively anticipate customer needs, promoting engagement.

Meniga anticipates that this conversational interface will benefit banks by engaging with consumers on a deeper level, increase satisfaction, lower support costs, and offer insights into customers’ individual needs. The new tool also meets consumers where they are, especially as their preferences shift away from features and towards conversational interfaces that offer instant, personalized answers.

“The banks that win agentic banking will be the ones that ground their conversational layer in real financial context. Not a generic chatbot, but an assistant that actually knows a customer’s spending patterns, their goals, and their upcoming bills, and is able to act on them,” said Meniga CEO Raj Soni. “With Fini, banks can enter the AI-agent era on the platform they already trust, without rebuilding what’s underneath, and without their data ever leaving the bank.”

Beyond answering questions, Fini supports agentic AI workflows that allow customers to complete certain banking tasks, like opening new accounts or setting up automatic transfers, directly within the conversation. This eliminates the need to navigate to separate screens.

Because Fini is model-agnostic, banks can build their AI assistants on Claude, GPT, Gemini, or their own proprietary model while relying on Meniga to provide the underlying financial context. Banks also retain control over their own guardrails, identity and access controls, and customer data, which never leaves the bank.

Meniga’s launch is similar to those of other fintechs racing to capture the LLM opportunity for consumer financial management. Rather than developing proprietary large language models, banks are increasingly viewing AI as a layered architecture. Foundation models such as Claude, GPT, or Gemini provide the conversational interface, while companies like Meniga provide the financial intelligence needed to ground those conversations in a customer’s actual spending patterns, cash flow, subscriptions, and financial goals. This approach enables banks to adopt new AI models as they emerge without rebuilding the personal financial management capabilities that differentiate their customer experience.