This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

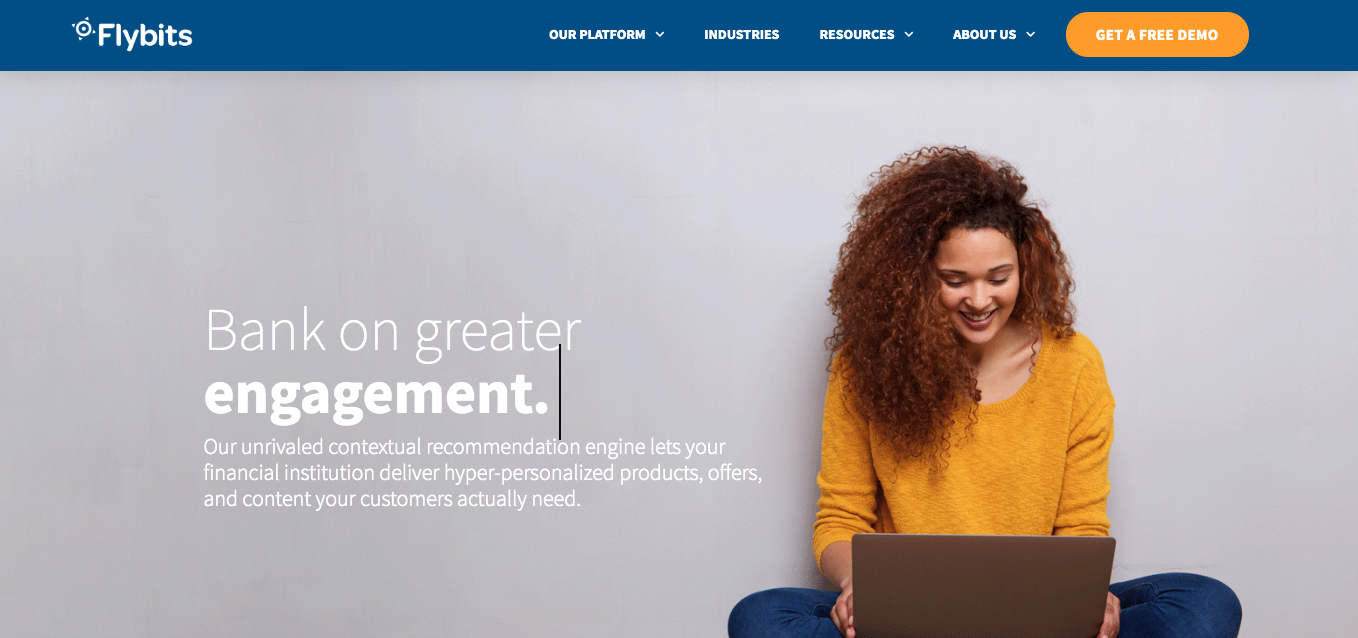

Flybits enables financial institutions to deliver hyper-personalized customer experiences, leveraging contextual intelligence and AI.

Features

Transform your mobile app into a sales channel

Assemble proprietary, public, and device data to deliver contextual experiences

Lower marketing costs and raise conversion rates

Why it’s great Flybits powers mobile, in-app marketing and sales for banks.

Presenters

Amir Yazdanpanah, Managing Director (MENA Region) Yazdanpanah is an entrepreneurial IT executive with extensive experience in software product development, product sales and marketing, business operations, and P/L management. LinkedIn

Rebecca Engelberg, Market Intelligence Manager Engelberg specializes in Market Intelligence, monitoring industry trends and translating them into actionable insights for sales, marketing and product strategy. LinkedIn

Revolut announced a partnership today that is a direct result of new open banking standards. The U.K.-based challenger bank has integrated with QuickBooks to enable Revolut for Business customers to sync their transactions with the bookkeeping software.

In a blog post, Revolut said that this “demonstrates a huge step forward for U.K. businesses” and it’s the first time the company has collaborated with a third party provider to use the new Open Banking APIs.

“It was only natural that we would team up with QuickBooks for this project, not only is it the world’s largest cloud accounting provider, but we also share the same customer-driven values; to deliver a best in class service through innovation,” said Domenico De Fano, Product Owner at Revolut for Business. “We understand the importance of accurate, secure and fast information to our customers, that’s why we invested the time to get the best connections in place with QuickBooks.”

Merchants that connect their business accounts with Quickbooks will receive real-time updates on payments, expenses, and cash balances to help them manage payroll, invoices, and taxes.

Revolut debuted its digital banking technology at FinovateEurope 2015 in London where the company’s CEO and founder Nikolay Storonsky showed off the app’s money transfer capabilities that help users avoid banking fees without actually using a bank.

Earlier this month the company tapped investment bank JP Morgan to conduct a $500 million funding round and issue it a $1 billion convertible loan, which will turn into shares if Revolut receives a U.S. banking license. Last week, the company launched in Singapore and announced plans to make its products available in the U.S. in the next couple of months.

TransPecos Banks has gone live on Nymbus’ SmartLaunch solution to outsource the infrastructure and operations of its digital-only subsidiary brand, BankMD, reports Alex Hamilton of Fintech Futures, Finovate’s sister publication.

Nymbus will provide onboarding, internet banking, and mobile banking for BankMD, which was founded with the intention of serving medical professionals in the state of Texas.

“We are dedicated to creating specialized products and a service culture that meets physicians’ unique needs and demands,” said Dub Sutherland, vice president and secretary of TransPecos Financial Corporation.

Sutherland adds that Nymbus was the only technology partner which took on BankMD’s concept to “bring it to life.” SmartLaunch eliminated the need for the bank to undergo a technology transformation, he said.

SmartLaunch is a banking-as-a-service product provided by Nymbus to stand up banks in a short time. The vendor claims it can do so in just 90 days.

The process involves the outsourcing of a bank’s entire operations to a team working within Nymbus. The platform also utilizes Nymbus’ SmartCore banking system.

“Launching a niche, standalone digital experience has gained tremendous momentum as an opportunity for financial institutions to compete and grow revenue,” said David Mitchell, president of Nymbus.

Other users of the Nymbus SmartLaunch platform include Centier Bank and Pacific National Bank.

NYMBUS, which demoed at FinovateFall last month, also offers a SmartBanking product that includes solutions focused on core, marketing, digital, payments, and services. Since it was founded in 2015, the company has raised $33.4 million and made three acquisitions, including R.C. Olmstead, KMR, and Sharp BancSystems.

Experianlaunches a new Open Data solution: Experian Commercial Acumen.

Mambu’s composable banking solution to help new SME bank Recognise enhance the customer experience.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Invoice and accounting SaaS solution Paper.idannounced a fresh round of funding this week, closing a Series A investment from Golden Gate Ventures and Modalku.

The exact amount of the round was undisclosed, though the company mentioned the funds total “billions of Rupiah” (one billion Rupiah equals just under $71,500). Paper.id will use the funds to expand its SME client base within Indonesia.

“The pervasive problem of collecting and slow cash flow may not be solvable in the short term. In this digital era, however, SME’s need to be educated to understand their cash flow and business performance with a system that is easy to use,” said Paper.id CEO Jeremy Limman. “With Paper.id, business owners can create an electronic invoice with their favorite device…”

Jeremy Limman and Yosia Sugialam co-founded Paper.id in 2017 to help Indonesia-based SMEs manage their business finances by moving their invoicing processes to the digital realm. Using the freemium product, business owners can keep track of receivables, generate cash flow reports, and receive payments digitally.

“Modalku and Paper.id have the same vision where we want to help SMEs to grow through having a seamless flow,” said Iwan Kurniawan, Modalku COO and cofounder. “Furthermore, Paper.id’s business model is in-line with one of Modalku’s products where the usage of invoice is used as the main document to propose [a] loan fund. Through this collaboration, we hope that we can reach more potential SMEs to have funding access without collaterals.”

Limman and Sugialam demoed Paper.id at FinovateFall 2018 in New York, showing how the company’s Supply Chain Financing helps banks offer businesses invoice financing in real time. Paper.id’s users, which number in “the thousands,” have sent more than 30,000 invoices digitally using Paper.id’s platform.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Digital banking firms Backbase and Payveris have signed a partnership deal which will see the creation of an integrated digital payments solution, reports Alex Hamilton of Fintech Futures, Finovate’s sister publication.

According to the two firms, their combined offering will enable financial institutions “of all sizes” to deliver “next generation” payment and money movement services.

“The banking industry’s legacy payment infrastructures are increasingly fragmented, inflexible, costly, and difficult to integrate with,” the companies write in a press release.

“Backbase’s raison d’être is clear: to develop and deliver efficient, effective tools that help financial institutions accelerate their digital transformation and provide superior digital experiences for customers,” said Jouk Pleiter, Backbase CEO. “By integrating the Payveris solution into our own, we are solving yet another pain point for the industry. Banks and credit unions have been crying out for a way to modernize and simplify their payments operating environments.”

Marcell King, chief innovation officer at Payveris, added, “By combining the power of Backbase’s progressive digital banking platform with the flexibility of Payveris’ open API MoveMoney Platform, you end up with a real wow-factor for a user interface, with functionality that delivers low friction digital money movement and management.”

At FinovateEurope 2018, Backbase unveiled the Customer OS in a demo that won the Amsterdam-based company Best of Show honors for the fourth time. Last July, the company teamed up with Jumio to deliver online ID verification services and in December the company partnered with Polish bank BGŻ BNP Paribas Bank.

This week’s Finovate Podcast episodes are both focused on small and medium sized businesses, and the opportunities that fintech is creating for bankers, innovators, and small business owners themselves.

Our first guest is Karen Mills, former Small Business Administrator for the Obama Administration, and author of the book Fintech, Small Business & the American Dream. Greg caught up with Karen to talk about how the Great Recession hurt small businesses in particular, and how fintech has been able to step in and help.

Our second episode features Jeremy Berger of Arival Bank, a Best of Show winning demoer from FinovateAsia 2018. Arival is a challenger bank reaching out to unbanked/underbanked small businesses all over the world. The company is expanding from Asia into the United States and Europe, and Greg spoke with Jeremy about the company’s fintech-first solution to the challenges facing SMB banking.

Next week Greg will be speaking with Wayne Miller of The Venture Center, a fintech accelerator with ties to FIS and the ICBA.

JumiolaunchesJumio Go, a real-time, automated identity verification solution powered by AI.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

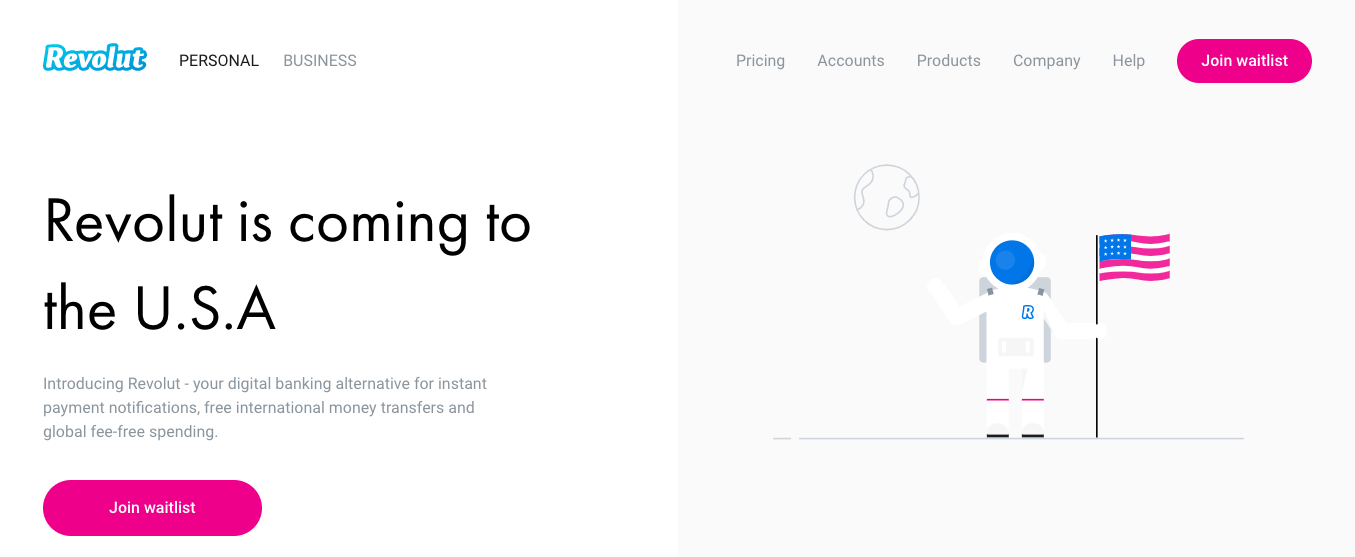

Digital challenger bank Revolut has chosen Singapore as its first entry into the Asian market. And now, after a successful beta period during which the company gained 30,000 new members and learned valuable lessons about the Singapore market and culture, Revolut is ready for business in Asia.

As of this week, Revolut Singapore customers will be able to instantly send and receive funds to and from fellow Revolut customers in Singapore, the U.K., Europe, and Australia for free. Revolut Singapore customers will also benefit from instant spending notifications, access to the real exchange rate in 150+ countries for fairer overseas spending, free international ATM withdrawals, and in-app currency exchange. PFM features like bill-splitting, round up payments, and budgeting and analytics will also be included.

“The journey to Singapore so far has been both exciting and challenging,” Revolut Head of Marketing and Communications Chad West wrote at the company blog. “For every new market into which we expand, there are different rules and regulations. The challenge for us is to build things that work as we, and our customers, want them to, while adhering to official guidelines. Not always easy, as you might imagine.”

The company’s expansion to Asia comes as Revolut fortifies its U.S. business via a partnership with Mastercard that will bring Revolut cards to the U.S. by year’s end. Other big deals for Revolut of late feature the company collaborating with Xero to enable real-time expense monitoring, teaming up with DriveWealth to offer commission-free trades to its cardholders, and working with financial API provider TrueLayer to support secure access of financial data via open banking.

This month Revolut announced that it had hired JP Morgan to manage its $500 million funding round, as well as issue the company a convertible loan for $1 billion. The company currently has more than $336 million in capital from investors including Index Ventures, Balderton Capital, DST Global, TriplePoint Capital, and Mastercard Start Path.

Founded in 2015 by Vlad Yatsenko (CTO) and Nikolay Storonsky (CEO), Revolut demonstrated its platform that same year at FinovateEurope. Since inception, the company has served more than eight million customers, and processed 350+ million transactions valued at more than $44 billion (€40 billion).

As Finovate goes increasingly global, so does our coverage of financial technology. Finovate Global: Fintech News from Around the World is our weekly look at fintech innovation in developing economies in Asia, Africa, the Middle East, Latin America, and Central and Eastern Europe.

Fresh off a successful return to Singapore for FinovateAsia, we are happy to announce that FinovateMiddleEast will be back in Dubai next month, November 20 and 21. For more information about our upcoming fintech conference in the UAE, visit our FinovateMiddleEast page today.

Central and Eastern Europe

Berlin-based, pan-European digital debt marketplace, CrossLend, picks up €34 million in round led by Santander.

Bank of Lithuania namesIBM and Tieto as finalists in its LBChain technology initiative.

Islamic, mobile-only, challenger bank insha goes live in Berlin, Germany.

Middle East and Northern Africa

Partnership with Diebold Nixdorfhelps Lebanese Bankmed become first bank in country to introduce cash recycling.

Bloomberg Intelligence recognizes the UAE as the world’s top Islamic fintech hub, with Bahrain as a rising challenger.

MAGNiTT and ADGM launch new publication focusing on fintech and venture capital funding in the MENA region.

Central and Southern Asia

Pakistan’s JS Bank launches chat banking via WhatsApp.

Western Union enables real-time payments and money transfers to India.

Paytm president Madhur Deora encourages Indian fintechs to appreciate the differences between Indian and Chinese markets “and adapt accordingly.”

Brazilian fintech Nubank reaches 15 million customer mark.

Posnet, a First Data/Fiserv company, helps Argentine consumers make purchases using digital wallets and QR codes.

Asia-Pacific

Revolutlaunches in Singapore after successful 30,000 customer beta.

CIMB Bank Singapore completes first structured trade finance transaction on blockchain.

In partnership with Compass Plus, Mongolia’s largest bank, Trade and Development Bank (TDB) introduces the nation’s first instant card issuance project.

Sub-Saharan Africa

Nigerian digital SME lender Lidyaexpands to Poland and the Czech Republic.

Fintech Futures features Absa’s Thabo Makoko on the challenges and opportunities in the African payment industry.

Ghana government makes plans for a cashless future.

Danish challenger bank Lunar has chosen financial services software provider Temenos to tackle financial crime on its platform, reports Ruby Hinchliffe of Fintech Futures (Finovate’s sister publication).

Ticking boxes such as watch-list screening and fraud prevention, as well as covering anti-money laundering (AML) and Know Your Customer (KYC) services, Temenos will deliver on its comprehensive security promise by integrating with Lunar’s core banking and payments technology.

The mobile-only banking app bought the product, which is called ‘Financial Crime Mitigation’ (FCM) and runs on the cloud, in a bid to “address stringent regulatory demands” and to safeguard its customers and reputation, said Temenos in a statement.

“As a challenger bank it is crucial for us to be in full control and create a scalable and agile setup in the Nordics,” said Lunar’s COO Morten Sønderskov, who says the bank’s choice to go with Temenos will get it “ahead of the curve in financial crime prevention”.

“We are building a Nordic bank from scratch and realizing our vision of becoming a financial Super App,” Sønderskov added.

Founded in 2015, Lunar now has more than 100,000 users and recently secured its European banking license from the Danish Financial Supervisory Authority. The fintech now has plans to extend its offering even further throughout the Nordics.

Temenos said more than 200 banks depend upon its FCM product now. “[We] proudly support the momentum of challenger banks around the world,” said Temenos’ MD for Europe Steen Jensen.

Temenos was founded in 1993 and is headquartered in Geneva, Switzerland. The company demoed its Connect Mobile Banking solution at FinovateEurope 2015. Temenos is also an alum of our developers conference, presenting a discussion on its B2B Financial Apps Marketplace at FinDEVRSiliconValley 2015.