- Account-to-account (A2A) payment infrastructure company Token.io has received a strategic investment from HSBC. The amount was not disclosed.

- The investment underscores the two companies’ history of collaboration, which includes Token.io’s support for HSBC’s Open Payments solution.

- Token.io made its Finovate debut at FinovateSpring 2015 and returned to the Finovate stage two years later for FinovateEurope in London.

Token.io, an account-to-account (A2A) payment infrastructure innovator, secured a strategic investment from HSBC this week. The amount of the funding was not disclosed. The two firms have been partners since 2019, when Token.io helped the bank launch its HSBC Open Payments solution.

“We are excited to deepen our partnership with HSBC as we embark on this collaboration,” Token.io CEO Todd Clyde said. “This investment will not only accelerate Token.io’s growth and innovation, it will also advance our shared vision of making Pay by Bank a mainstream payment method—delivering benefits for HSBC’s customers across the region.”

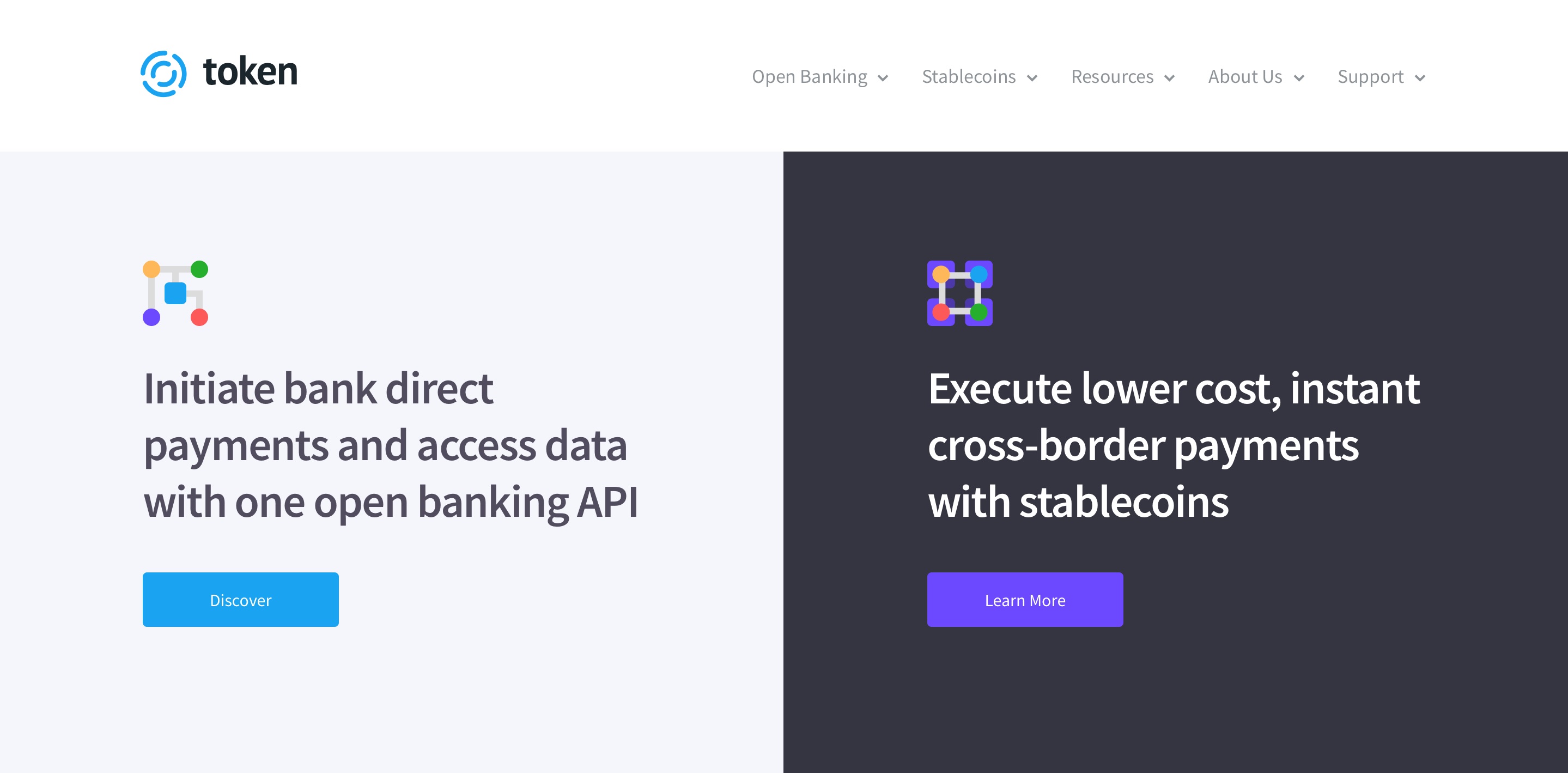

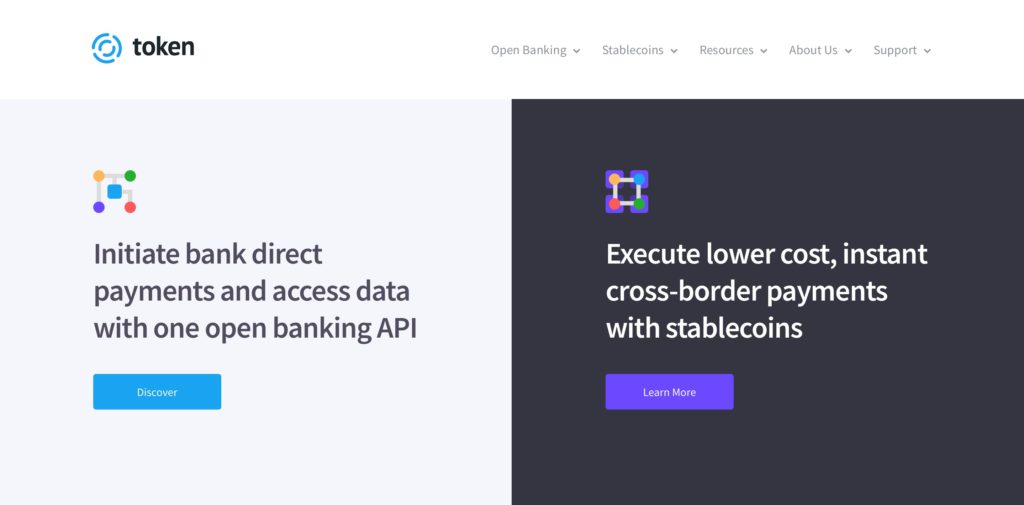

Pay by Bank is a payments service that gives customers a secure, fast, and convenient way to conduct peer-to-peer payments, account deposits, and loan repayments, as well as securely authenticate transactions via their banking app. Supported by open banking and real-time payment infrastructure, Token.io’s technology makes the service available to anyone with a UK or European bank account. In a statement, the company noted that analysts believe in the future growth of Pay by Bank, predicting that three-in-four Europeans will be regular Pay by Bank users by 2029. In fact, by 2030, analysts estimate that use of Pay by Bank for e-commerce transactions in Europe will become more popular than all other digital payment options, with the exception of digital wallets.

HSBC’s Open Payments solution is based on this infrastructure. The technology enables businesses to connect their checkout pages with online apps or mobile platforms used by customers. Purchasers are given a request for pre-populated payments and, once the payment is authorized, the seller is granted an “instant and irrevocable credit” to their account. The new offering helps businesses get working capital faster and keeps both the risk of fraud and the cost of collections low.

“Our investment in Token.io reflects the trust and confidence we have in their team and technology, and our firm belief in the role that innovative Open Banking solutions play in transforming the payments experience for both corporates and consumers,” HSBC Head of Global Payments Solutions Manish Kohli said.

Founded in 2015 and headquartered in San Francisco, California, Token.io made its Finovate debut at FinovateSpring 2015 and returned two years later to demo its latest technology at FinovateEurope in London. A major account-to-account payment infrastructure provider for banks and other financial institutions, Token.io’s partners include three of the largest financial institutions in Europe as well as companies such as Global Payments and fellow Finovate alums Mastercard and ACI Worldwide.

Last month, Token.io became the first third-party provider to be admitted to the giroAPI scheme. This will enable the company to provide account-to-account payment solutions to its partners—including micropayments that are exempt from Strong Customer Authentication (SCA) requirements. Launched by the German Banking Industry Committee associations—BVR, DSGV, VÖB, and the Association of German Banks—at the beginning of the year, the API scheme is built on the Berlin Group’s openFinance API framework and provides a standardized, secure, and commercially governed interface to connect banks with third-party providers such as Token.io.

“By joining giroAPI, Token.io is enabling the next wave of premium, API-driven payment services—making it easier for businesses to offer innovative payment options and for consumers to benefit from seamless, secure experiences,” Token.io Chief Product Officer Charles Damen said. “We are proud to lead the way in bringing the full potential of open banking-enabled payments to the European market.”