This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Adding to the big-bank-to-big-tech partnerships announced in recent weeks, Standard Charteredsecured a three-year partnership with Microsoft today.

The bank will leverage Microsoft to take a multicloud approach that will port its significant applications to the cloud. Specifically, Standard Chartered is planning to make its core banking and trading systems and digital ventures such as virtual banking and banking as-a-service cloud-based by 2025.

“Cloud is a cornerstone of Standard Chartered’s strategy to meet the present and future banking needs of our clients,” said Group Chief Information Officer of Standard Chartered, Michael Gorriz. “Using cloud services improves our ability to be agile and innovative, while increasing our operational efficiency and resilience. As disruption in the financial industry continues, we can focus on client benefits by deploying our solutions quicker and allowing for faster integration of new business models and partners.” Gorriz added that today’s partnership is a “major milestone” in Standard Chartered’s journey to become cloud-first.

Standard Chartered will pilot the launch by moving its trade finance systems to Microsoft Azure. The move is expected to facilitate cross-border trade at the bank.

The partnership extends to Microsoft’s workplace tools. Standard Chartered’s 84,000 employees will be working on Office 365 and communicating via Microsoft Teams.

This news comes during a time of widespread digital transformation across the banking sector. Banks and fintechs are seeking to move their operations to the cloud to update their infrastructure and create a better customer experience. There are two factors driving this change: the global health crisis that has moved many in-person interactions to online channels and the rise of competition from challenger banks.

“Cloud computing is an enabler for financial institutions to modernize their infrastructure and systems, to gain the agility they need to respond to competitive pressures, regulatory environments and customer demand,” said Bill Borden, Corporate Vice President of Worldwide Financial Services at Microsoft. “We are committed to helping Standard Chartered Bank in its ongoing digital transformation journey as it strives to address evolving customer needs and build the next generation of banking experiences.”

Branded payments provider Blackhawk Network has teamed up with open finance data and intelligence platform Moneyhub to ensure compliance with open banking standards. Via the partnership, Blackhawk Network will be able to validate third-party providers, connect to them through live applications, and enable them, with user consent, to access user data and initiate payments.

“Using Moneyhub’s compliance solution means that we can adopt the industry best-practice approach to PSD2 in authorizing our unique prepaid card offering,” Stacey Richards, who handles Product Management for Blackhawk Network, explained. “We share the fundamental desire to deliver a transformative experience for the end-user with Moneyhub, and we look forward to working with the team to deliver on our ambitious vision for the future.”

Blackhawk Network helps businesses leverage branded payments to reach more customers, build engagement and loyalty, and increase revenue. A Finovate alum since 2012, the company has more than 3,000 workers around the world, and serves 26 countries with its branded payment solutions. Blackhawk features 1,000+ brands in categories ranging from dining and entertainment to retail and home improvement. The Pleasanton, California-based company went public in 2013, and was acquired by Silver Lake and P2 Capital Partners in 2018 in a deal valued at $3.5 billion.

More recently, Blackhawk acquired Edge Loyalty Systems, an Australian sales promotions and loyalty firm, for $23 million (A$32.2 million). This spring, the company purchased SVM Cards for an undisclosed sum.

Moneyhub’s partnership with Blackhawk is the company’s third collaboration this year. In June, Moneyhub teamed up with Lumio, a money management app. The following month, the company partnered with investment performance analytics firm, ARQ.

“Our Open Banking expertise means that we are able to deliver a comprehensive compliance solution to Blackhawk Network, ensuring that it remains a leader in the market and delivers excellence to current and future clients,” Moneyhub CTO Dave Tonge said. “Our growing product offering and the multi-use nature of our proposition means that we are able to work alongside Blackhawk Network and help support their growth and aspirations.”

Founded in 2011 and based in Bristol, U.K., Moneyhub made its Finovate debut at our European conference in 2015. Nationwide Building Society is the company’s primary investor, having led a corporate round for Moneyhub in the fall of 2018.

For better or for worse, modern society has adapted to expect things instantly. We want a quick lunch delivery, a fast Uber pick-up, and we expect Netflix to buffer our movies in microseconds. Even Amazon’s two-day shipping takes too long.

Recognizing the value of the real-time economy, Orumlaunched its flagship product, Foresight, last week. The new tool helps banks move money in real time for instant account funding, overdraft protection, and consumer-focused pre-delinquency tools.

Instead of leveraging the blockchain for real-time transfers like Ripple does, however, Orum takes a different route. The startup uses AI to predict the availability of funds within an account and pre-authorizes transactions, incurring limited risk.

“At Orum, we are creating a paradigm shift for the way money moves,” said Orum founder and CEO Stephany Kirkpatrick. “We are leaving behind siloed accounts and manual transactions and building toward fully automated and point-to-point money movement. Technology has created an on-demand economy, but our money has yet to catch up.”

In addition to Kirkpatrick, Orum’s team includes former N26 employee Ryan Cooke and former Stash VP Christine Hurtubise.

Along with Orum’s new product announcement, the New York-based company landed $5.2 million in Seed funding led by Homebrew with contributions from Inspired Capital, Acrew, Bain, Clocktower, Box Group, and angel investors. Impressively, the round was both opened and closed during a pandemic.

“Today’s tools for immediate money movement leave enterprises decades behind what customers demand. Orum is tackling this challenge head on,” said Homebrew Partner Satya Patel. “We’re excited about Orum’s vision. The early demand they’ve seen—both from cutting-edge fintechs and incumbent financial institutions—speaks for itself. It’s clear the market understands the value of moving money in a new, more efficient way.”

According to Crunchbase, Orum is already working with 50 customers and has a waiting list.

The incumbents in the real-time payment (RTP) space in the U.S. have seen some traction, however none have seen widespread adoption. Aside from Ripple, other players working on RTP solutions include The Clearing House, which launched its RTP scheme in 2017 and now counts 32 banks and 19 technology providers as clients. According to Forbes, however, fewer than half of these members are operational on the RTP platform.

The U.S. Federal Reserve is also in on the game, having announced its own RTP scheme, FedNow, last year. Since its announcement, there has been much debate within the fintech industry over whether or not the government can effectively compete with the private sector with real time payments. However, given the lack of traction in the area, the Federal Reserve ultimately decided to pursue FedNow. In true government fashion, however, the offering is not slated to launch until 2023 or 2024.

Remember how society expects everything to happen instantly? The slow traction of incumbent players in the RTP space isn’t meeting expectations. That said, there is a lot of room for Orum in the RTP space and I think we’ll be hearing about a lot more traction from them in the second half of this year.

2020 may be a tough year overall, but it has been quite good to the cryptocurrency space. PayPal announced plans for a cryptocurrency offering, Visa revealed plans to incorporate cryptocurrencies into its payment network, and Mastercard expanded its existing cryptocurrency program.

Late last week, another development took shape: cryptocurrency payments platform Wirex announced it received its first money transmission license in the U.S. The license, issued by the State of Georgia Department of Banking and Finance, comes two years after Wirex received its e-money license from the U.K. Financial Conduct Authority.

Receiving the license is a major step in the direction of a U.S. launch. In fact, Wirex said it will formally launch in the U.S. “in the coming months.”

“We are very excited to receive our license as a money transmission business for the State of Georgia,” said Wirex CEO and co-founder Pavel Matveev. “With the sector growing rapidly, approval of this license is an important step in Wirex’s endeavor to ensure the company complies with money transmission regulations and cryptocurrency laws worldwide. This is an important step in realizing our vision to grow cryptocurrency adoption and use with a mainstream audience in the U.S.”

Wirex was founded in 2014 and helps its 3 million customers in 130 countries buy, hold, and exchange fiat money and cryptocurrencies. Among the company’s offerings is a contactless, crypto-compatible debit card that enables customers to transact at the 54+ million locations where Visa is accepted. Wirex is also known for Cryptoback, a cryptocurrency rewards scheme that offers up to 1.5% back, paid in Bitcoin, to customers who use their Wirex card in-store.

The fintech industry will look back at 2020 as a year of change in many areas, including digital transformation, payments, and in-person services. However, one of the most impactful changes taking shape this year is the broader acceptance and usage of cryptocurrencies.

Part of the evidence here is the formation of partnerships between crypto companies such as Wirex and traditional incumbents such as Mastercard. Last month, the two struck a deal that allows Wirex to directly issue cards on Mastercard’s network.

Wirex has received $3.2 million in funding and became profitable earlier this year.

The news that eBay is teaming up with LendingPoint to help finance small merchants on its platform is the latest example of how technology marketplaces are going the extra mile to look after the merchants who make their platforms possible.

“We are committed to empowering entrepreneurs to make their dreams a reality and we are continuing to partner with our sellers to provide them with the tools they need to thrive,” Vice President of Global Payments at eBay Alyssa Cutright said.

The new program is called eBay Seller Capital powered by LendingPoint, and will provide eBay sellers with access to installment loans with flexible terms of up to 48 months. Currently being run as a pilot effort, the program offers funding of up to $25,000, with no origination or early payback fees.

“LendingPoint’s purpose is to accelerate and democratize commerce,” LendingPoint CEO and co-founder Tom Burnside said. He called eBay sellers “some of the world’s most dynamic ecommerce players,” and both companies have noted that the partnership is a first step toward providing the platform’s merchants with more and better tools to manage and grow their businesses.

Headquartered in Atlanta, Georgia, and founded in 2014, LendingPoint began the year with news that it had closed on $246 million in securitizations. More recently, the company launched its Lending Operating System SDKn, which integrates into existing payment platforms to provide businesses with a consumer financing solution with a variety of fulfillment options ranging from virtual cards to money transfers.

The news from eBay comes a few weeks after InstaPay announced a new financing solution that provides third-party sellers on Amazon – who often wait up to two weeks to be paid by the platform – with a daily payment that helps them better manage their cash flow. Google removed commission fees for merchants enrolled in its Buy on Google program last month, and said it is opening up its platform to third party providers PayPal and Shopify.

In a late-breaking announcement on Thursday, Intercontinental Exchange (ICE) announced that it has agreed to purchase mortgagetech platform provider Ellie Mae from Thoma Bravo. Valued at $11 billion, Ellie Mae will add to Intercontinental Exchange’s growing presence as a major workflow solutions provider for the U.S. residential mortgage industry. This growth includes ICE’s acquisition of a majority stake in MERS in 2016, and the comany’s acquisition of Simplifile three years later.

Ellie Mae President and CEO Jonathan Corr referred to these other players and the chance to collaborate with them in his remarks about the acquisition agreement. “We are excited to be joining the Intercontinental Exchange family and having the opportunity to work closely with Simplifile and MERS in helping our industry to realize the true digital mortgage,” Corr said. “We have been on a journey, as we have long said, ‘to automate everything automatable’ for the mortgage industry, and joining ICE, which has followed a parallel journey in global exchanges, will allow us to further accelerate realizing our vision.”

Founded in 1997 – and acquired by Thoma Bravo in February of last year in a deal valued at $3.7 billion – Ellie Mae offers a digital lending platform to help mortgage lenders originate more loans, reduce origination costs, and shorten the time to close. An alum of both our developers conference, FinDEVr, and making its Finovate debut in 2017, Ellie Mae reports that its customers save an average of $813 per loan, and close loans seven days faster, producing an average annual ROI of 698%.

During its time as part of Thoma Bravo, Ellie Mae recorded “nearly double revenue” while improving profitability, partnered with firms like AI Foundry to further streamline the mortgage origination process, and acquired fellow mortgagetech company Capsilon. Both AI Foundry and Capsilon are also Finovate alums.

“We partnered with Jonathan Corr, Joe Tyrrell, and the Ellie Mae team to advance their vision to automate the residential mortgage industry while also using Thoma Bravo’s deep software expertise to greatly improve the company’s operations and accelerate growth,” Thoma Bravo Managing Partner Holden Spaht said. “We are confident that being part of ICE will enable Ellie Mae to continue transforming an industry still in the early innings of digitization, and we look forward to following Ellie Mae’s continued success as part of ICE for many years to come.”

A Fortune 500 company formed in 2000, Intercontinental Exchange owns financial and commodity exchanges, operating 12 such regulated institutions in the United States, Europe, and Canada. The Atlanta, Georgia-based company also owns and operates six central clearing houses around the world. With revenues of $6.5 billion in 2019, Intercontinental Exchange is publicly traded on the NYSE under the ticker ICE. The firm has a market capitalization of $54 billion.

This week for Finovate Global, we caught up with Mohammed Aziz, co-founder and CEO of Dapi, a fintech startup that offers a suite of open banking APIs to help connect customer bank accounts, initiate payments, and access data in real-time. Founded in 2019, the company currently operate in six countries in the Middle East and Africa, and is headquartered in both San Francisco, California, and the UAE.

We talked about the opportunity for open banking to fuel innovation in financial services in emerging economies, as well as the overall environment for fintech innovation in the MENA region. We also discussed the impact of the COVID-19 crisis on pre-existing trends such as digitization.

Finovate: Dapi is the third company you’ve founded, but your first fintech. What made you want to focus on the opportunities in this industry? What do you bring to fintech from your experience in other areas?

Mohammed Aziz: Dapi was the result of a problem that I personally faced when trying to build “Spendy” a hybrid between a peer to peer payment application and a personal financial management app. We were unable to build out Spendy for most emerging markets due to the lack of bank connectivity which got us super keen to build out the underlying infrastructure that would power the future of fintech in these markets.

Finovate: Tell us about Dapi. What problem does your company solve and who are your primary customers?

Aziz: Dapi’s mission is to provide the building blocks for a thriving fintech ecosystem in emerging markets around the world. Our API serves as the bridge between financial applications and banks, empowering developers to create digital wallets, budget trackers, investment applications and more. Our clients are developers working on fintech applications, businesses hoping to include financial services in their mobile and web offerings, and anyone that wants to include bank functionality within their digital offerings.

Finovate: Your business strategy relies on an embrace of open banking in the MENA region. How strong is the movement toward open banking there?

Aziz: The MENA region is a very exciting space to be operating in right now. Fintech is only beginning to develop here and the market is pretty much untapped, so we are hoping to serve as an influence towards the region embracing open banking and all the opportunities that come with that. I would also like to point out that we are able to activate and build connectivity regardless of open banking being present or not. We like to take the approach that companies like Plaid in the US or Truelayer in the UK did, whereby they were connected to banks despite frameworks and regulation being in place.

Finovate: Aside from open banking, what are some of the other exciting trends in the fintech industry in the Middle East/Abu Dhabi right now?

Aziz: There’s a general trend of growing interest for the kinds of applications that financial technology empowers, from digital wallets and peer to peer applications to investment platforms and digital banks. The market is new and rapidly evolving.

Finovate: We talk about the Middle East and North Africa as a region. But there is a great deal of variation among countries in MENA. How does this impact your ability to market your technology in the area?

Aziz: Beyond market considerations, the regulation surrounding the use of APIs in financial applications varies greatly from country to country. This is a new and mostly unregulated space, but we have had to consider completely separate approaches to integrating our services in the UAE as opposed to KSA, for example. Culture is also another important factor, as it varies between countries and impacts the products that you would want to launch along with the go-to-market approach.

Finovate: How has COVID-19 impacted the fintech industry in the region? Early in the crisis, we heard news from countries like Iran, but not as much since. How are businesses, especially fintech businesses, faring?

Aziz: The COVID-19 pandemic and its push towards social distancing and remote work has actually increased interest in digitization of financial services. For example, there have been a number of announcements within the UAE that the country will be moving towards enabling more online payments and other financial services without the need to physically go to a bank.

Finovate: You participated in the Y Combinator program. What was that experience like? What advice do you have for startups with the opportunity to pursue a similar path with a top-notch accelerator?

Aziz: Y Combinator has been a phenomenal experience for us. It really put us out there on the map and helped expand our network in silicon valley. From our experience, investors and VCs in the US are not usually convinced about investing in early stage MENA startups, but YC really helps establish that credibility.

Finovate: Tell us about your experience of setting up your business in Abu Dhabi.

Aziz: Abu Dhabi is an exciting place to work, since it is a rapidly growing and developing market, as mentioned above. Furthermore, we have received a lot of support from our involvement in ADGM and Hub71, which provided resources for us to establish and grow our operations in these beginning stages.

Finovate: What can we expect from Dapi over the balance of 2020 and beyond?

Aziz: We are very excited to continue growing and expanding into a variety of developing markets, beyond the UAE. At the same time, we have a number of exciting partnerships in our sights for the UAE, which we hope will bring our vision of a strong fintech ecosystem in the MENA region closer to reality.

Here is our look at fintech around the world.

Asia-Pacific

Singapore-based MatchMove launches cross-border remittance platform for businesses.

Clik, a payment aggregator and merchant acquirer based in Cambodia, raises $3.7 million in seed funding.

Leading Asian financial services platform GoBear teams up with UnionBank to launch lending-as-a-service solution in the Philippines; announces new Chief Financial Officer.

Sub-Saharan Africa

Fiservinks partnership with Absa Regional Operations (ARO) to enhance credit card management and processing in nine African countries.

Ecobank Group unveils the finalists for its fintech challenge, now in its third year. Ten African startups from seven different countries made the cut out of an applicant pool of more than 600.

Salaam Gateway looks at the development of Islamic fintech in Kenya.

Central and Eastern Europe

Onfido to streamline digital identity verification for Poland’s Alior Bank.

Russia’s Tinkoff Banklaunches new charitable program, Cashback to Give Back.

Austrian regtech kompany lands $7.14 million in funding.

Middle East and Northern Africa

Salt Edgepartners with Jordan Ahli Bank Cyprus, making it one of the first banking groups in Cyprus to achieve PSD2 compliance.

Israeli fintech Approve.com raises $5 million in seed funding for its technology that automates the procurement process.

Infosys Finacle to deploy its Liquidity Management platform with National Bank of Bahrain.

Central and Southern Asia

Uzbekistan’s People’s Bank partners with Finastra to automate its risk management business.

TerraPay collaborates with Bank Alfalah to enable instant money transfers to Pakistan.

Indian B2B fintech Signzy announces plans to hire “close to 70” employees over the next six moths in response to increased demand.

Latin America and the Caribbean

Feedzaiexpands partnership with PayU, enabling the company to enhance its fraud prevention capabilities in Latin America and the EMEA region.

TechCrunch profiles Mozper, a digital banking service based in Latin America that caters to parents and Gen Z kids.

MercadoLibre announces plans to launch branded credit cards in Brazil and Chile “in the near future.”

As part of our #WomeninFintech series, Finovate speaks to inspiring women about their career in financial services and technology, their unique insights into the challenges and solutions for the industry today, and their advice for the next generation of women leaders just starting out. Today, we join Lena McDearmid, COO at Artis Technologies, a provider of embedded financial services platforms for digital, point-of-need lending and payments. Lena helped launch the startup earlier this year with a mission to refine the consumer lending experience by merging the art of technology with the science of finance to create the best consumer experience possible.

What led you to fintech and specifically down a path toward acquiring the expertise you have now?

Lena McDearmid: It started with my mother responding to an ad in the paper looking for someone to manage short-term loans from retail locations. Here I, unfortunately, learned about the negative side of lending, but also how to build programs to help get people out of destructive cycles. This inspired me to move to Atlanta where I joined an online mortgage startup company.

However, in 2008, I could see a coming shift away from the trending jumbo hybrid real-estate loans into more stable and traditional loan types. With that foresight, I moved into conventional lending where I would diversify my underwriting experience with mortgage refinances, auto loans, personal credit cards as well as debt consolidation. I learned the importance of empathizing with customers’ needs and offering more customized products based on their unique loan usage.

From there, I went to a company that focused exclusively on underwriting auto loans, where I had my first realization of a “culture-first” experience proving that employees who are happy and positively impacted by their work culture are better able to focus on the customer’s experience. I believe completely that a customer’s experience is the most important part of business.

After my time there, I was then recruited to build out the credit department at GreenSky where, for the first time, I had direct contact with technology and could see what tech could do for my operations. I spent eight years going from credit operations, to project management, and finally to technical product ownership, before leaving to start Artis.

The journey of my career is one of constant learning and growth. I am a builder of companies, products, teams, and experience. Had I not had the good fortune to walk down so many different paths, there is no way that I would be here today having the confidence knowing that at Artis, we are building a company and products that are ultimately helping the consumer with more accessible financing, the most important part of business.

Where do you see the future of the fintech heading in the next 12 months?

McDearmid: Continually increasing reliance on big data and the ability to incorporate alternative data for better decision making, especially when it comes to credit. Stronger reliance on user experience and customizations per user.

How can the financial services industry humanize AI and gain the trust of its customers? How is Artis Technologies helping?

McDearmid: It starts with the data scientists and the data. We have to know, throughout the design process, that there are humans analyzing this data. We also have to know what data elements are sensitive and understand how biases can get into the models so that we can design bias-free models and analytics. Finally, we must study the outputs and analyze their impacts on humans to ensure there are no adverse effects.

What does being one of the company’s women co-founders mean to you? And how does this set the example for other women looking to break into the field?

McDearmid: It means a great deal; most of the women in my family were entrepreneurs and as a co-founder, I now feel as if I am in their company. I imagine that the more women see other women as co-founders and leaders, this will encourage them to strive for these roles, as the women in my family inspired me. Each light on a path makes the path a little brighter and easier to follow.

How are you tackling the challenges and redefining the role of women at Artis?

McDearmid: One of the reasons I co-founded Artis was because I saw an opportunity to overcome the typical challenges women face in being heard and seen as leaders. Because Artis is a startup, it’s given me the opportunity to help define, not redefine, the importance of women and diversity at our company from the beginning. All of which are supported by my other like-minded male co-founders.

Why is it important to have multiple voices in the room, and hold each other accountable throughout the journey?

McDearmid: Diversity leads to quality. The ability to draw on multiple perspectives and experiences enriches discussions and solutions. And, without accountability, there can be no real growth, honesty, or radical transparency. Through accountability, we hold ourselves to our standards and continue our growth — regardless of gender.

What advice would you give to women starting out in fintech now?

McDearmid: Find a mentor and advocate. Believe in yourself and be assertive while learning as much as you can about all aspects of the business and industry.

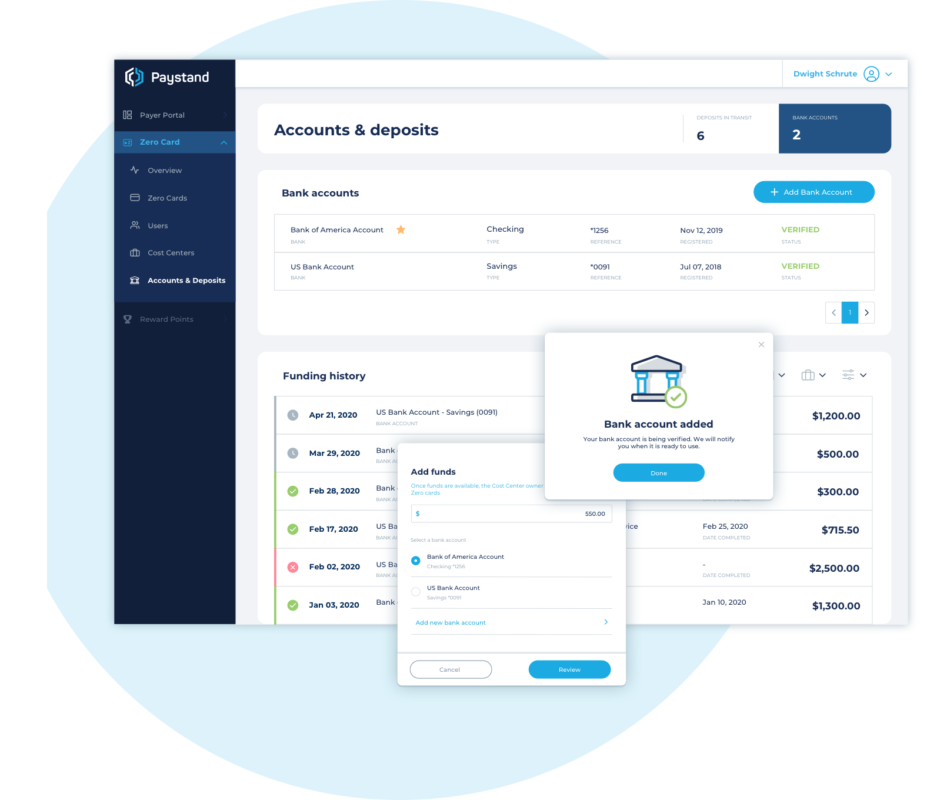

Paystand’sZero Card, launched today, offers businesses a touchless, prepaid corporate expense ePayable solution that leverages Paystand’s zero-fee payment network to eliminate the cost of transaction fees.

Geared to help mid-market businesses in particular, which often require a high degree of flexibility and control over their budgets, the Zero Card streamlines expense management operations such as invoice processing, expense reporting, and payment execution. The prepaid virtual expense card also enables businesses to manage, track, and control spending in real-time. The offering includes fraud prevention controls and the ability to capture and add critical remittance data to transactions to make expense reporting and reconciliation easier.

“The Paystand Zero Card combines the consumer-like experience of peer-to-peer payments with the speed and security of Paystand’s no-fee payment network,” Paystand CEO Jeremy Almond said. “We completely re-engineered the corporate card so businesses can move away from reactive spend management tactics to a place where they have visibility of spend before it happens.”

One of the aspects of the Zero Card the company is touting is the way it brings a common payment infrastructure to accounts payable and accounts receivable operations. In its statement, the company referred to this disconnect as “one of the biggest challenges in B2B payments today,” which pits payers and receivers against one another as “technology and process improvements for one group often lead to inefficiency and friction for the other.”

In contrast, the Zero Card is designed for both accounts payable and accounts receivable, natively connecting both AP and AR to keep costs low, ensure swift and secure payments, and effectively bridge what the company calls “the payables gap for B2B payments”

Challenges like the payables gap, according to Paystand VP of Marketing Mark Fisher, are why he believes B2B payments have “a long way to go before it achieves the ease and speed of consumer payments.” Fisher credited the Zero Card for helping B2B payments catch up. “When money moves over our network,” he said, “it’s instant, automated, and comes at no cost. That’s good for businesses and that’s good for the economy overall.”

Founded in 2013 and headquartered in San Francisco, California, Paystand secured $20 million in funding in February in a round led by DNX Ventures. Mitch Kitamura, Managing Director at the firm put the company’s latest offering in the broader context of the “cashless transformation” led by fintech innovators like Paystand. In a statement, he referred to the Zero Card as “a critical step … in driving more seamless interaction between businesses to help realize the true economic value of digital infrastructure.”

If there are any lingering doubts about the power (and popularity) of the Buy Now Pay Later (BNPL) movement, installment payments platform Splitit has 71.5 million reasons to cast those doubts aside.

The New York-based company, which made its Finovate debut as PayItSimple in 2014, announced that it has raised $71.5 million in a private placement and share purchase plan (SPP). With institutional investors such as Woodson Capital Management, the company plans to use the capital to “accelerate sales and marketing, plus (make) further investments in product and technology” according to a statement. Splitit boasts more than 1,000 ecommerce merchants using its technology, and 300,000+ shoppers with an average order value of $893.

Splitit’s fundraising comes as the company reports record Q2 growth, including processing more than $65 million in merchant sales volume, and growth of 1.76x quarter over quarter and 2.6x year over year. In discussing the company’s success, CEO Brad Paterson credited a new willingness on the part of consumers to “maximize their existing credit to preserve cash flow” while at the same time not incurring additional new debt.

Paterson also noted that while the COVID-19 crisis has helped move digital transformation in ecommerce toward the top of the agenda, it was important for those involved in payments to make it easier for merchants to accommodate their customer’s cash management requirements.

As such, it’s hard not wonder if, once again, crisis is responsible for accelerating innovation. After all, one of the initial innovations in retail, the layaway program, emerged during the Great Depression as a way to maintain at least a minimal level of consumption of non-essential goods during a severe economic retraction. By enabling customers to pay for items in small increments over time and then receive those items once they had been fully paid for, the growing retail economy was able to survive an extended period of historically low demand.

The buy now pay later phenomenon is layaway in reverse, allowing customers to gain the benefits of the purchase immediately and moderating the impact of the cost by paying for that purchase over time. But the goal – to accelerate consumer activity and expand the ability of people to spend – remains the same. The only difference is that layaway tended to disappear once credit cards became ubiquitous, while buy now pay later appears to be rising at a time when we are realizing that affordable consumer financing might not be as ubiquitous as we thought.

For Finovate fans, Klarna has been the pioneer in the Buy Now Pay Later space, with fellow alums like Sezzle also earning recognition for its interest-free buy now pay later option. Founded in 2005 and 2016, respectively, both companies are reminders of how fintechs have been providing consumers with alternative financing options well before the coronavirus hit.

That said, it is clear that COVID-19 has stimulated interest in Buy Now Pay Later options. The Business of Finance reported earlier this week that BNPL had become “fashion’s go-to during the pandemic.” Also this week, American Express announced that it would extend its buy now pay later service to more of its cards. The Wall Street Journal featured Australian Buy Now Pay Later specialist Afterpay at the beginning of this month in the wake of the firm’s announcement that it had signed up more than 1.6 million U.S. users since the onset of the coronavirus in March. And Shopify announced this month that merchants on its platform would have access to BNPL financing from installment payment company Affirm. Affirm looks like it is ready to maximize the Buy Now Pay Later moment with an initial public offering, according to reporting in the Wall Street Journal.

Even the big banks are getting into the Buy Now Pay Later game. Goldman Sachs has introduced a new, installment payment feature called MarcusPay – in partnership with JetBlue Airways – as part of a bigger “build-out” of its Marcus by Goldman Sachs digital banking platform. This week, Citi partnered with Amazon to launch its own BNPL offering Citi Flex Plan.

Place another notch in the belt of the challenger banking crowd. This week banking alternative Bnextextended its Series A round by $13.08 million (€11 million), adding to the $26.7 million (€22.5 million) the bank brought in last October.

Bnext’s Series A round now stands at $39.2 million (€33 million) and its total funding is now in excess of $47 million (€40 million). Existing investors DN Capital, Redalpine, Speedinvest, Founders Future, Enern, Digital Horizons, Kreos Capital, and Cometa contributed to this week’s follow-on round.

Bnext will use the funds to further its growth in its home territory of Spain, as well as build its presence in Latin America by focusing on its expansion into Mexico. The bank initially launched in Mexico at the beginning of this year and now has 60,000 users in the region.

“At Bnext we have always had a clear objective: to be a banking alternative that allows our users to end the bad experiences of traditional banks,” said Bnext CEO Guillermo Vicandi. “Since its launch, our growth has been constant both in services and products and in users, and we are proud to have the support of the best investors to design and execute a strategy that allows us to achieve our objective. Our position to change the banking sector in the Spanish-speaking world is unbeatable and we have a duty to take advantage of it.”

The challenger bank has amassed 400,000 clients since it launched in 2018 and currently processes $119 million (€100 million) per month in transactions. Last month Bnext launched its Premium account and added to its Rewards program.

The latest offering from Envestnet | Yodlee enables financial service providers to combine actionable insights, peer benchmarking, and personalized views to build digital financial experiences that better serve and engage their customers across channels. Insight Solutions, unveiled today, provides a set of new APIs that will help companies leverage data to improve the quality of their virtual financial assistance offerings.

“Hyper-personalization is the new baseline for success, and financial institutions and FinTechs who have a more advanced understanding of consumers and tailor their offerings accordingly will have a strategic and competitive advantage,” Envestnet | Yodlee SVP of Product Brandon Rembe said. “Through our Insights Solutions, financial service providers will have access to meaningful consumer insights faster and more affordably than by growing their own data science team.”

Users will be able to take advantage of features like predictive cash flow; spending, credit limit, and refund monitoring and alerts. The new tool will also provide transparency into subscription-based and other recurring expenses. The solution puts the power of machine learning and algorithms to work to provide users with a comprehensive overview of their personal finances, enhancing their ability to save for retirement, build an emergency fund, as well as manage their everyday spending.

With more than 26 million users worldwide, more than 1,300 partners (including 16 of the top 20 U.S. banks), and 50+ patents, Envestnet | Yodlee offers data aggregation and analytics technology solutions that support financial wellness and sound wealth management. Envestnet acquired Yodlee, one of Finovate’s oldest alums and a multiple-time Best of Show winner, in 2015 in a deal valued at $660 million.

Envestnet | Yodlee began this year with the acquisition of financial data aggregation and analytics platform, FinBit.io. This month, the company issued a report looking at income and spending trends during the COVID-19 crisis. In the form of an eBook, the report looks at how retailers in different industries – from restaurants and transportation to barbershops and gaming – were impacted by consumer behavior shifts due to the economic effects of quarantines, lockdowns, and other efforts to fight the pandemic.

Barrons featured Envestnet co-founder and current CEO Bill Crager in an interview last month. Crager took the helm at the company after the tragic death of previous Envestnet CEO Jud Bergman in a 2019 automobile accident. Crager discussed the personal and professional challenges of the succession, as well as plans for 2019 acquisition MoneyGuide, and the company’s strategy for serving its clients during the global pandemic.

Envestnet | Yodlee is a publicly traded company – ENV on the New York Stock Exchange – and has a market capitalization of $4.4 billion.