This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Backbase announced today the availability of its new managed cloud platform, Backbase-as-a-Service. The solution makes the company’s broad portfolio of digital banking offerings available to FIs looking to accelerate their ability to develop and offer new technologies to customers.

In their statement, the company depicted banks as challenged by not one, but two types of technologically-driven competitors: digitally-native neobanks and big tech-first companies that are beginning to develop financial products (“TechFin”). The problem of legacy, non-digital infrastructure, according to Backbase, is a key hurdle for most banks when it comes to “keeping pace” with the new digital services these rivals are able to offer. Backbase-as-a-Service enables FIs to develop their digital solutions faster, and to bring them to market without having to overcome their outdated infrastructure – or bear the high cost of replacing it with another on-premise system.

Backbase CEO Jouk Pleiter called the cloud “an exceptional tool” to help financial institutions transition to becoming digital first. “We believe the move to cloud is an unstoppable one, and one which every financial institution needs to embrace,” he said. “Our clients want the freedom to innovate and maintain their competitive edge, so launching Backbase-as-a-Service is the logical step or us.”

The technology will enable banks to take advantage of innovations in account aggregation, security and identity verification, personalization, and smart banking. Developers benefit from the option to use shared or dedicated Backbase environments, as well as multiple sandbox environments to support the development and testing of new integrations and products. BaaS provides 99.9% uptime, database backups and multi-zone redundancy, as well as end-to-end encryption for all communications. The solution meets regulatory requirements, including the ability to audit across environments.

A multiple-time Finovate Best of Show winner, Backbase most recently demonstrated its digital banking platform at FinovateEurope 2018. Headquartered in Amsterdam, the Netherlands, and founded in 2003, the company inked a deal with Payveris late last year to provide FIs with an integrated digital payments and money movement solution. With more than 100 FIs using its technology, Backbase includes Barclays, Citi, KeyBank, Navy Federal Credit Union, and Societe Generale among its customers.

Supply chain payments company Tradeshift just unveiled details about a $240 million funding round today. The investment– a combination of debt and equity– comes from new and existing investors. Tradeshift’s total funding is now $672 million.

The San Francisco-based company will use the investment to boost expansion efforts and gear toward a “direct path to profitability in the near future.” The funding will also be used to grow Tradeshift’s network finance program that provides liquidity to companies in 100+ countries.

And it appears that Tradeshift is already on the right track. Last year the company tallied record expansion; growing its revenue more than 60% and closing more than 300 enterprise deals. What’s more, 40% of the total transaction volume across its platform occurred in the last 12 months.

“It’s clear that the investor community has a strong focus on growth combined with profitability and they like our plan,” said Tradeshift CEO Christian Lanng. “As a network business, growth is always going to be a key part of our story. But it’s also important that we manage that growth responsibly.”

Tradeshift’s business commerce platform connects more than 1.5 million companies across 190 countries. To date, the company has processed more than half a trillion dollars in transaction value. After Tradeshift’s most recent funding round of $250 million last spring, the company’s valuation was boosted to $1.1 billion.

As for 2020 plans, Lanng said that the company’s focus “will be about doubling down in areas where we’re seeing the greatest momentum while continuing to ensure we have the necessary balance in place to fully capitalize on the enormous opportunities in front of us.”

A look at the companies demoing at FinovateFall on September 14-16, 2020. Register today and save your spot.

Horizn’s award-winning platform equips frontline employees & customers directly with the knowledge needed to improve customer experience and dramatically increase digital adoption across all channels.

Features

Get employees & customers fluent on latest digital innovation

Improve customer experience & drive digital adoption

Combine simulation microlearning methodology with gamification/analytics

Why It’s Great Using Horizn, banks increased digital adoption by 25% and brought call center times down by 45 seconds. Using the in-branch demo with non-digital customers, up to 20% converted to digital banking.

Presenter

Steve Frook, VP Sales Frook works closely with financial institutions to significantly increase adoption and awareness of new and existing innovations. LinkedIn

A look at the companies demoing at FinovateFall on September 14-16, 2020. Register today and save your spot.

Glia is a digital customer service platform that connects financial institutions to their customers using Chat, Voice, Video, CoBrowsing and AI.

Seamlessly move between modes of communication

Receive improved sales results and customer satisfaction via richer customer interactions

Deliver the best experience for customers and agents

Features

Why it’s great By employing a digital-first approach to customer conversations, financial institutions improve customer satisfaction, reduce customer effort, and gain operational efficiencies.

Presenter

Dan Michaeli, CEO & Co-Founder Michaeli is the driving force behind Glia’s vision to combine the human touch with technology to create the best customer experiences. LinkedIn

The company that is bringing credit data clarity to the cryptocurrency industry is entering 2020 with a new name. Credmark, which made its Finovate debut as Graychain at FinovateAsia earlier this year, is reintroducing itself with a new Southeast Asia headquarters and partners who are helping develop the cryptocurrency lending market.

“We’ve been wanting to rebrand for awhile,” Credmark CEO Paul Murphy said. “When we decided to move the company from Hong Kong to Singapore, we realized it was the right time to rebrand.”

Murphy believes the rebrand will make it easier for people to understand what the company is about – especially in a field like cryptocurrencies, which can be intimidatingly complex to both businesses and consumers. “We are the only company giving credit ratings to blockchain addresses, not individuals or corporations,” Murphy explained. “This allows us to address a much wider range of use-cases including anonymous and pseudonymous borrowing, and smart contract credit, as well as more traditional uses of credit.”

Murphy agrees with those who see cryptocurrencies as the foundation of a new financial system. Like any other financial system, he said, cryptocurrencies will need credit (what he called “a proxy for trust”) in order to function efficiently. And in order to extend credit, you need data. And that’s where Credmark comes in.

“Credmark is developing a product to remove friction in the crypto space caused by lack of trust,” Murphy said. “This product will help minimize systemic credit risk whilst simultaneously speeding up business transactions.”

One example he shared was his company’s collaboration with a firm that is tokenizing sneakers in order to use them as collateral for crypto loans. “Crypto finance is proving endlessly creative. Building on top of centuries of technology in a global, decentralized environment is a rare opportunity. This work will have a profound impact on everyone, from the world’s richest to its poorest,” Murphy said.

In addition to Murphy’s 12 years of building software for financial firms on Wall Street, Credmark benefits from the talents of co-founder Neil Zumwalde, the company’s Chief Technology Officer. Zumwalde is a veteran software developer and engineer whose experience includes building complex distributed systems in the IOT/energy space.

About the company’s technology, Murphy said Credmark is a big user of blockchain technology (“we currently work with nine different chains!”), Credmark also leverages AI to build its cutting-edge prediction models. The company currently offers three products – Credmark Wealth, Credmark Clear, and Credmark Clear for Business – which help crypto businesses, lenders, and investors evaluate the value of digital asset holdings on a company’s or address’ overall net worth and creditworthiness.

Credmark’s decision to relocate from Hong Kong – where the company has been headquartered since its founding in 2018 – to Singapore is also a key part of the company’s evolution. In addition to putting some distance between itself and Hong Kong’s civil unrest of recent months, the move will enable Credmark to remain in a major fintech hub while building its position in the rapidly growing Southeast Asia cryptocurrency industry.

“Singapore is a fantastic jurisdiction in which to do business,” Murphy said. “Rules are very clear, bureaucrats are efficient, and legal and financial services are of very high quality. I personally ran several businesses in the U.K., so Singapore’s legal system is very familiar.”

The rebrand also comes as the company issues its second Crypto Credit Industry report (CCR). Credmark’s CCRs are a compilation of industry data with analysis and commentary to help readers learn about the crypto credit industry, the vendors that participate in it, and the different products they offer. The company’s first report was released in late August, and covers industry developments through Q2 2019.

“Our latest industry report reveals growth of 23% in the third quarter,” Murphy said of the Q3 report. “And institutional lending products are starting to mature.” He added that one way the CCR will benefit readers will be in bringing greater clarity and transparency to the world of crypto financing.

“The industry uses some vanity metrics that are confusing and sometimes misleading,” Murphy explained. “We’re calling those out and planning to de-emphasize them.”

Asked where he thinks Credmark will be a year or two from now, Murphy responds, “If we’d been asked that question two years ago our predictions would have been completely wrong. The industry is moving fast. We are careful to take this rapid, uncertain evolution into account as we design our products. We have taken a big bet on crypto, but have remained blockchain-independent.”

“No matter how things evolve, we expect to play a central role in this emerging financial system,” he said.

A look at the companies demoing live at FinovateEurope on February 11-13, 2020 in Berlin. Register today and save your spot.

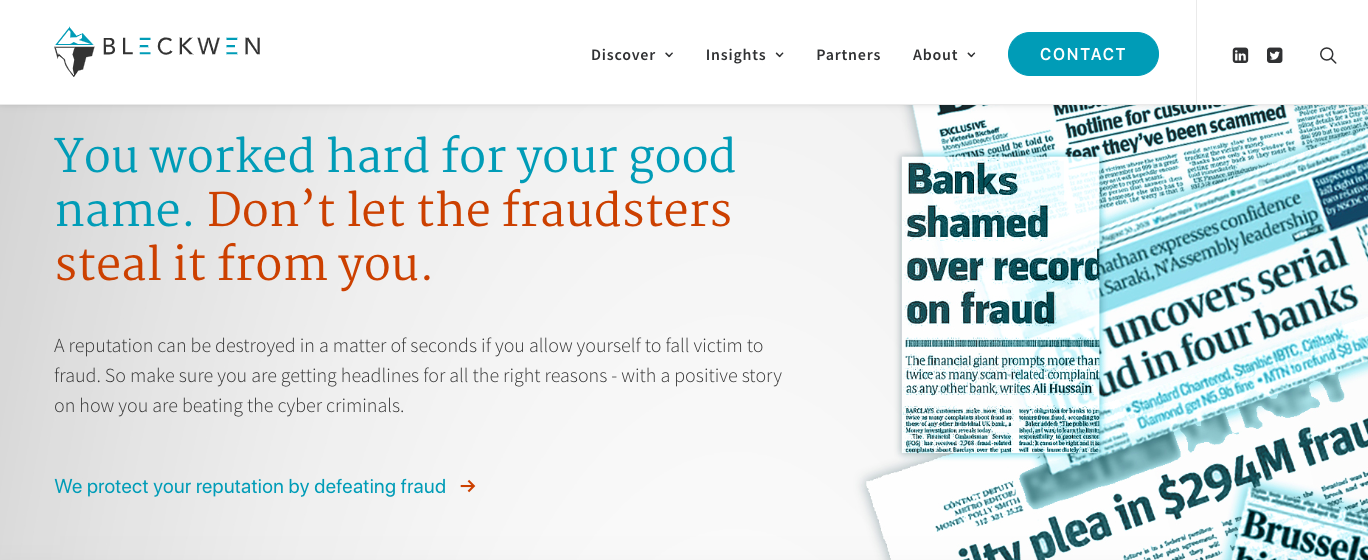

Bleckwen: Real-time Machine Learning solution for financial crime detection. In partnership with banks, we combine Behavioral Analytics with AI to provide an effective response against fraud.

Features

Reduce false positives, customer friction and costs of financial crime detection

Reduce time to manage alerts with our white box approach

Comply with increasing regulatory requirements

Why It’s Great Bleckwen’s real-time, dynamic Behavioural Analytics & Explainable AI-engine is well placed to detect the surging fraud threats in payments in today’s open banking world.

Presenters

David Christie, CEO Christie has a global view of the challenges of managing Fraud from multi-jurisdictional, technology and business process perspectives with 20 years in financial services. LinkedIn

David McLaren, VP Sales EMEA McLaren is an Enterprise Sales and Financial Crime specialist with experience in new business sales, SaaS and managed services with extensive engagements working with Financial Institutions and Corporates. LinkedIn

Updated 1/14/2020: The first big fintech acquisition of the year just crossed the headlines: Visa has agreed to acquire innovative fintech Plaid for a reported $5.3 billion in “total purchase consideration.”

“Today marks an important milestone for our company and for fintech,” company co-founder and CEO Zach Perret wrote on the Plaid blog earlier today. “What started with two founders building in a cramped conference room has become an incredible network that enables millions of consumers to interact with over 2,500 digital finance products.”

Plaid’s technology connects digital consumers with thousands of apps and services ranging from Transferwise and Betterment to Chime, Acorns, and popular payment app, Venmo. The company estimates that one in four individuals with a U.S. bank account have used Plaid to connect with thousands of developers across 11,000+ financial institutions.

Visa said the acquisition will bolster the company’s capacity to serve and reputation with fintech developers – especially when it comes to providing them with enhanced payment functionality and related value-added services. Visa also believes the acquisition will help open new business opportunities both in the U.S. and around the world.

“We are extremely excited about our acquisition of Plaid and how it enhances the growth trajectory of our business,” Visa CEO and chairman Al Kelly said. “Plaid is a leader in the fast growing fintech world with best-in-class capabilities and talent. The acquisition, combined with our many fintech efforts already underway, will position Visa to deliver even more value for developers, financial institutions, and consumers.”

Visa participated in Plaid’s Series C round in 2018, which was led by Index Ventures and Kleiner Perkins. The company raised $250 million in that funding raising effort. Plaid began the year with an acquisition of its own, purchasing account aggregation and data analytics technology provider Quovo in January of 2019. The value of that deal was not disclosed; Bloomberg reported that the sticker price for Quovo could have been as high as $200 million. Quovo, incidentally, is also a FinDEVr alum, participating in our New York developers conference in 2017.

Plaid demonstrated its technology at FinDEVrSiliconValley in 2014, demonstrating how its API for Financial Infrastructure enabled developers to leverage data quickly, efficiently, and securely power fintech applications. Headquartered in San Francisco, California and founded in 2012, Plaid had raised $310 million in funding previous to today’s announcement.

The ripples from the acquisition news are reverberating throughout the fintech community. And while some are worried about the ability of the innovative startup from San Francisco continue to drive change in the industry, others are busy heralding the news as a victory for fintech and incumbent financial services firms, alike.

Indeed, the acquisition of Plaid by Visa has put other fintechs involved in financial data on notice that they too may hear an inquiring knock on their proverbial doors. One observer on Twitter asked “Will $MA pick up Finicity now?” As of this writing, neither company has deigned to comment.

Risk management and advisory services firm INTL FCStone announced today that its London-based subsidiary has agreed to acquire GIROXX for an undisclosed amount.

Headquartered in Germany, GIROXX offers international bank transfers and currency hedging. INTL FCStone plans to leverage this technology to expand its current client base to small-and-medium-sized enterprises (SMEs).

As part of the agreement, INTL FCStone’s advisory services will be made available to GIROXX’s clients. GIROXX founders Klaus Hoffmann and Jörg Sonnenschein said that the deal will help the company “gain the resources to offer hedging services on a multi assets basis.” As a result, the founders anticipate that GIROXX will solidify its client base and boost company expansion.

The purchase marks INTL FCStone’s sixth acquisition and its fourth in less than 10 months. The company said that these purchases, combined with internal restructuring, are part of an effort to protect clients from negative effects of Brexit.

“Our objective is to offer SME’s the ability to hedge all parts of their production processes, and to allow these corporates to have access to a digital payments and hedging platform,” said Carsten Hils, Global Head of INTL FCStone’s Global Payments Division.

Following the deal, INTL FCStone plans to open its client base to companies with less than 1,000 employees in Europe, a market with 350+ correspondent banks. The acquisition is pending approval from BaFin, Germany’s financial regulatory authority.

Founded in 1981, INTL FCStone is publicly listed on the NASDAQ under the ticker INTL. The company has a market capitalization of $947 million.

There were more than a few provocative presentations at FinovateAsia last fall. And Celent’s Dan Latimore was the man responsible for delivering one of them. Latimore, who is Senior Vice President of Celent’s Banking group, weighed in on a topic that is increasingly on the minds of technology analysts inside and out of fintech: the impact of 5G (which stands for “fifth generation wireless”) on financial services.

“Banks need to think about the implications of being able to access really heavy compute power remotely and centrally, whether it’s over the cloud or on premises,” he said during his presentation on 5G late last year. “What that does is turn every device into a thin client- which will have some very interesting implications.”

Dan Latimore returns to the Finovate stage next month in Berlin for FinovateEurope. He will host an afternoon interactive Q&A session titled What’s Hot: Money Disrupt on February 11, and later will share his views on “What’s Hot & What’s Not in Fintech” as part of our Analyst Insight showcase on February 12. Check out our FinovateEurope conference page for more details.

Calling 5G “something banks aren’t even thinking about,” Latimore said, “we believe the effects of 5G are going to be subtle and profound over time.” He dared indulge the “superhighway” metaphor – previously coined to describe the rise of the Internet in the late 1990s – to compare the potential of 5G with its predecessor technology 4G (to say nothing of the “dirt road” that was 3G). Relative to 3G, he noted, 5G’s “fiber over the air” approach represents a 26,000x improvement in speed, as well as major improvements in capacity and latency (“the time it takes for the stimulus to create a response”).

For reference, the first commercial 3G networks were introduced in 2000. The first commercial 4G networks were introduced less than ten years later in 2009.

While it is generally (though not universally) acknowledged that 5G will represent major opportunities for innovation in a variety of industries – from entertainment to autonomous vehicles to the Internet of Things (IoT) – many observers have overlooked the potential impact of 5G on financial services. Because 5G will enable mobile devices to serve as thin clients which can simply “point back” to the backend server, Latimore explained, banks will be able to leverage massive computing power to provide everything from centralized updates and better contextual advice to personalized interfaces on ATMs.

To this point, Latimore indicated that 5G would be one of the key avenues toward a post-smartphone future, as well. “Don’t forget about wearables,” he warned, “because that’s now a thin client that can be a much more viable way for people to interact with their bank, probably activated by voice.”

Check out more from Dan Latimore on 5G, including the shift from hardware spend to data spend, how institutions can negotiate the transition from 4G to 5G, the potential for new security challenges, and more. Celent subscribers can access his report. To see his presentations live next month at FinovateEurope, visit our registration page and pick up your ticket today.

Demo spots for FinovateEurope are still available! If you’re a fintech company with innovative, problem-solving technology, FinovateEurope is your opportunity to show the world!

Contact our Event Team today for more information on how to join us on stage as a demoing company at FinovateEurope next month in Berlin!

With Visa’sTap to Phone app arriving pre-installed on the new, enterprise grade smartphone from Samsung, a broad range of merchants will have access to yet another way to accept payments from customers. The solution works with any Android smartphone and enables everyone from microbusiness owners to retail sales professionals to make on-the-spot transactions with customers without relying additional hardware.

Visa’s Tap to Phone technology enables consumers to make payments in seconds by tapping their contactless payment card – or smartphone or smartwatch – against the vendor’s Tap-to-Phone enabled smartphone. And because it is built on an EMV chip transaction, Tap to Phone is able to generate the same dynamic security for transactions as a traditional terminal does, ensuring both parties that the transaction is secure.

Visa notes that its Tap to Phone technology is currently being piloted in more than nine markets, including in Canada, the U.K, Ukraine, Turkey, Costa Rica, and Malaysia. Additional pilots are scheduled for Poland, Australia and a few other countries “over the next several months.”

Samsung has selected its Galaxy XCover Pro enterprise smartphone to be integrated with Visa’s Tap to Phone technology. The company expects the combination to be valuable in a variety of verticals both within and beyond ecommerce, such as logistics and healthcare.

“The Samsung Galaxy XCover Pro is a robust retail POS platform for a true retail digital transformation,” Visa’s Head of Seller Solutions Mary Kay Bowman said. “Its applications for businesses such as healthcare, airlines, and restaurants are a great example of how Visa together with Samsung can democratize access to payment experiences that consumers increasingly expect, no matter where they are.”

Samsung has demonstrated its technology on the Finovate stage, teaming up with Fiserv to provide biometric authentication for the payment giant’s Commercial Center: Security solution at FinovateFall 2018. Visa participated in our developers conference, FinDEVr Silicon Valley in 2014, discussing “The Future of Commerce” and introducing its API-less, Visa Checkout integration solution.

Starting in Q2 of this year, Mastercard customers will be able to get a new, “augmented” understanding of the benefits and rewards available to them as cardholders. The augmented reality app, announced by Mastercard late last week, will offer cardholders a virtual tour of three different portals representing Mastercard’s three reward categories: Experiences, Everyday Value, and Peace of Mind.

Each category inside Mastercard’s augmented reality environment has its own appearance: a home setting for Everyday Value, for example, and a spa for Peace of Mind. Within each portal is a virtual room with various benefits denoted with representative symbols and avatars (i.e, tapping on a golf club image generates a pop-up option to explore Mastercard’s Priceless Golf benefits).

Mastercard chief marketing and communications officer Raja Rajamannar put the app in the broader context of the company’s ongoing efforts to provide more engaging, interactive experiences. “At Mastercard, we’re using our technology and solutions to deliver multi-sensory experiences for consumers every day – whether they’re shopping, taking transit, or exploring the card benefits they care about,” Rajamannar said.

AR as a marketing solution for fintechs is a use case familiar to Finovate audiences. Alums ranging from ebankIT (and its parent company, ITSector) to Fiserv has demonstrated how they have leveraged AR to deliver compelling marketing content to customers.

Augmented reality in fintech will featured in a keynote address at FinovateEurope in Berlin next month. When Will AR & VR Become Meaningful Tools in Customer Engagement? will be held on Tuesday, February 11 on the Future Tech Industry Stage.

On Finovate.com

2020: A Breakout Year for Fintech in Emerging Markets? – From major investments in fintechs in Latin America and Africa to the challenger banking “space race” in Singapore, 2020 could turn out to be a breakout year for fintech in many growing economies around the world.

8 Banks You’ll Compete with If You Offer More Than 2% on Savings – Banks are facing an increased number of competitors these days. Not only are traditional banks vying for customer deposits, but fintechs and challenger banks want part of their funds, as well.

China Says 你好 to American Express – The People’s Bank of China (PBOC), China’s Central Bank, announced it has accepted an application from American Express (AmEx) that expressed the company’s intention to operate in China.

Future Banking: Creating an Incumbent Challenger – Finovate talks with Ronit Ghose, global head of banks research and co-head of the fintech theme group at Citi about the future of challenger banks and why some shouldn’t be calling themselves a “fintech” at all.

Treasury Management Innovator HighRadius Earns Unicorn Status – HighRadius, a company that offers AI-powered order-to-cash and treasury management solutions, announced today that it has raised $125 million in Series B funding. The investment boosts the Houston, Texas-based firm’s valuation to $1 billion, earning it the status as one of the first new fintech unicorns of 2020.

Sprint and Wirecard to Deliver the Internet of Payments – Telecommunications giant Sprint and German financial services provider Wirecard announced they are teaming up to deliver the Internet of Payments.

Influencers as Innovation: Fintechs Turn to the Famous in Bid to Boost Visibility – As Snoop Dogg celebrates his first anniversary as a high-profile Klarna shareholder and RDC announces that it has hired a network of social media influencers to help promote its new digital banking app, it’s clear that firms are all-in when it comes to using celebrity to showcase everything fintech.

banqUP, PSD2, and the Future of Open Banking in Europe – We reached out to banqUP CEO and founder Krzysztof Pulkiewicz to talk about the company’s latest accomplishments in open banking, as well as what the landscape for fintech innovation is like inside and outside the CEE region.

ING’s Katana Becomes a Standalone Fintech – Dutch financial services corporation ING announced today it is spinning off Katana into its own entity called Katana Labs. As a part of its move to independence, Katana has closed $3.9 million in funding, half of which ING contributed “to enable further growth and to pave the way for an independent future for Katana.”

Finovate Podcast Episode 21: Romeo Maione, Launchfire – New Year and a new episode of the Finovate Podcast! Romeo Maione, Director of Business Solutions, Lemonade by Launchfire, joins host Greg Palmer to discuss marketing through training, and why the U.S. could be falling behind on digital adoption.

Bankjoy and Zogo Finance Team Up to Onboard and Educate Gen Z Customers – Bankjoy and Zogo Finance are betting that helping credit unions and community banks educate their members rather than “sell” to them is the key to better engagement for CUs and better financial health for consumers.

The Digital Identity Infrastructure and What it Has to do with Fintech – The last decade brought about a lot of discussion around digital identity. Dozens of security companies created new solutions to help banks authenticate their user’s identity and verify their personal information.

Proptech Advances in Latin America As Loft Raises $175 Million in New Investment – The $175 million in Series C funding raised by Latin American digital real estate platform Loft this week offers an insight into how proptech is providing new investment opportunities within the emerging markets of countries like Brazil and Mexico.

Nebula Merges with Open Lending, Forming a New Publicly Traded Company – Lending solutions provider Open Lending has agreed to merge with Nebula Acquisition Corporation, an acquisition company sponsored by True Wind Capital.

Alumni News

DAVO Technologiespartners with restaurant management platform Toast.

Clearview Federal Credit Union partners with Insuritas to launch an insurance agency.

Will 2020 be the year of emerging markets fintech? From major investments in fintechs in Latin America and Africa to the challenger banking “space race” in Singapore, 2020 could turn out to be a breakout year for fintech in many growing economies around the world.

And while attention is deservedly shifting to exciting news in fintech in countries like Mexico, Brazil, and Nigeria, it is also worth considering which regions might have interesting fintech developments which, while flying under the radar now, could end up dominating international fintech headlines by mid-year.

With this in mind, we turn to Europe in general and the Central and Eastern Europe region in specific. Here’s a look at our conversation with Krzysztof Pulkiewicz, founder and CEO of the Belgian-based and “proudly developed in Poland” fintech innovator banqUP. We talked with Pulkiewicz on the latest developments with his company, as well as his outlook on open banking and the differences between business inside and outside the CEE.

Here is our weekly look at fintech around the world.

Middle East and Northern Africa

Ziraat Participation Bank, headquartered in Sudan, to deploy the iMAL Islamic core banking system from Path Solutions.

Emirates NBD announces completion of the third phase of its core banking systems upgrade.

Abu Dhabi Investment Office leads Series A funding round for blockchain-based regtech firm, Securrency.

Central and Southern Asia

Netherlands-based payments company PayU acquires majority stake in Indian fintech PaySense, plans to merge company with Indian consumer lender LazyPay.

Royal Bank of India announces new rules to enable companies to participate in remote customer onboarding.

Two U.K.-based credit unions, Voyager Alliance CU and Retail CU, go live on TCS Bancs, a core banking solution from Indian technology company Tata Consultancy Services.

Latin America and the Caribbean

IBMpartners with Argentina’s Chamber of Fintech to support digital transformation projects in the country’s fintech and banking sector.

Central Bank of the Bahamas to launch digital version of its currency.

Business Insider calls Mexico “a top neobank market to watch in 2020.”

Asia-Pacific

What trade war? China unveils new regulations that make it easier for foreign lenders to access the Chinese market.

Horizons Ventures leads Series A+ round for Hong Kong-based financial data and analytics provider MioTech.

Lightnet, a Thailand-based blockchain company operating in the remittance market, has raised more than $31 million in new funding.

Sub-Saharan Africa

fin24 features OkGo.live, The People’s Fund, Isiduli, and a non-profit, blockchain pilot program in its look at four South African fintechs to watch in 2020.

Chipper Cash, a U.S.-based fintech that offers no fee, mobile P2P services in six African countries, raises $6 million in funding.

Ventureburn lists 10 ways Africa’s fintech sector boomed in 2019.

Central and Eastern Europe

Qonto, a challenger bank for SMEs launched in France two years ago, announces expansion to Germany.

Lithuania’s biggest postal service provider extends cooperation agreement with payment card authorization firm Ashburn International.

As Finovate goes increasingly global, so does our coverage of financial technology. Finovate Global is our weekly look at fintech innovation in developing economies in Asia, Africa, the Middle East, Latin America, and Central and Eastern Europe.