One basic feature missing from most online and mobile banking services is the ability to edit/annotate transactions. Some banks, BMO Harris for example, support transaction and/or category editing in their PFM modules. But it’s very rare to see it within basic digital banking.

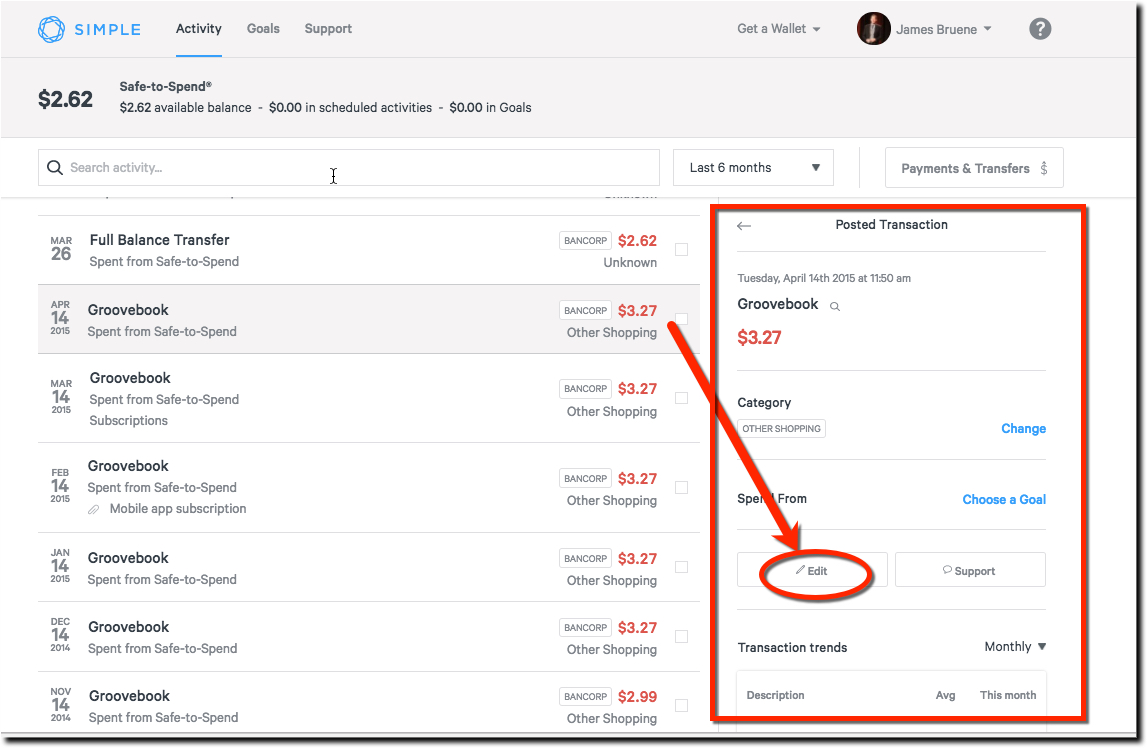

One exception, is BBVA Compass’s Simple banking unit. Simple allows full editing of the transaction name, category, and goal. And users can add a memo and an attachment to individual transactions. Clicking on a transaction brings up the detail section along the right (see screenshot below). The feature is functional on the desktop, but it’s easier to use, and more robust, on a mobile phone where the built-in camera aids photo attachments. And the transaction is visually more appealing after editing on mobile (see After mobile screenshot).

Thoughts: While it’s a little harder to use than I’d like, it feels wrong to complain about UX issues at Simple, when the vast majority of FIs don’t allow any editing whatsoever. But my job is to whine, so I’ll make this suggestion. The best user experience is to edit directly within the transaction record rather than following commands over to the right. And on mobile, voice editing should be supported.

Bottom line: While Simple’s transaction editing may not quite live up to the digital banking pioneer’s name, it’s head and shoulders above the competition. And that’s no simple feat.

Transaction editing on the desktop

Step 1: Select transaction on left; if desired, change category (#1), or funding source (#2), then press “edit”

![]()

Step 2: Annotation options (1) Edit name, (2) Add memo, (3) Upload image, (4) Add location

![]()

Transaction editing on mobile

Before edits After edits

Author: Jim Bruene is Founder & Senior Advisor to Finovate as well as

Principal of BUX Advisors, a financial services user-experience consultancy.

I am not a

I am not a

{kind=link}