U.S. challenger bank-turned BBVA subsidiary Simplehas a surprising new offering for its mostly millennial client base. The bank wants its customers to start using paper checks.

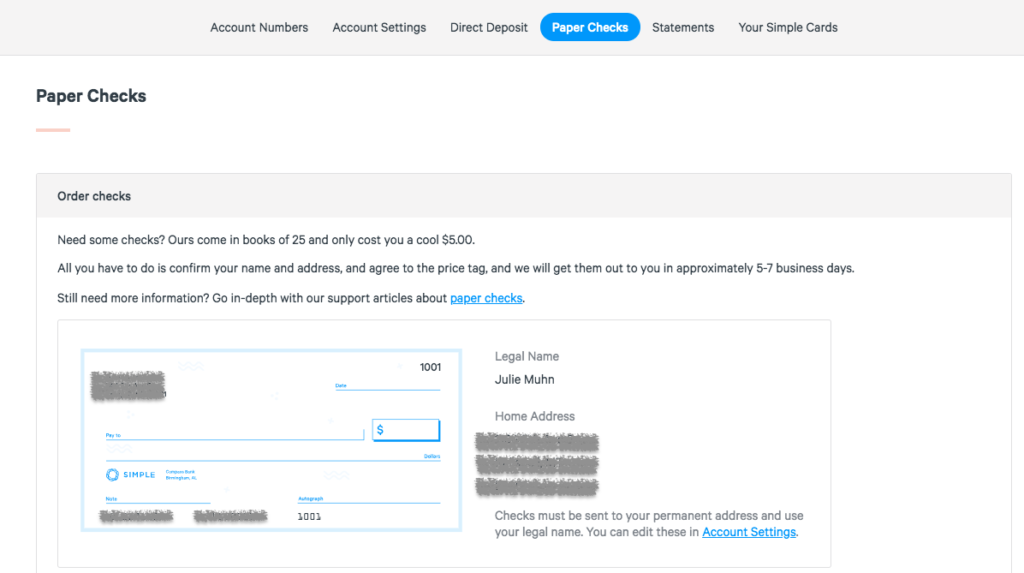

The Portland-based bank unveiled the news in an email to members yesterday. “We heard you: sometimes you just gotta write a check, even if you do your banking online. So here they are in all their glory—Simple paper checks,” the email read.

The checkbooks are available for $5 for a book of 25 checks and, as Simple noted, “they work just like regular checks (Cursive not required.)” For its clients who may not be familiar with checks, Simple included a special section in its FAQ on paper checks, including a subsection titled, “writing a check” that offers step-by-step instructions.

So why checks, and why now? Simple’s addition of paper checks is likely a patch of sorts. That’s because, along with today’s announcement, the bank also told clients that it is shutting down its billpay service. Starting July 9, users will need to use paper checks to pay bills.

It’s also possible that Simple truly did receive pressure from customers requesting the service. If this is the case, it says two things about the state of fintech. First, it’s a downvote for cash. It’s also a humble reminder that, despite all of the tech available, fintech still lacks proper digital channels that connect consumers with the right recipients. The checks aren’t a substitute for peer-to-peer payment apps such as Venmo and Zelle. Instead, Simple’s customers will likely use the paper checks to pay bills and small contractors who do not accept credit cards.

Founded in 2009 and launched two years later under the name BankSimple, Simple debuted at FinovateFall 2011. In 2014, BBVA purchased the challenger bank for $117 million. In September of 2018, Simple announced it will pay 2.2% interest on savings accounts with balances of more than $2,000. Late last year, seven months after Simple’s CEO and Co-Founder Josh Reich announced plans to leave, the digital bank appointed David Hijirida, a former executive at Amazon, as CEO.