Canadian payments innovator Dream Payments raised $10 million in new funding this week. The Series A round was led by the investing division of Fairfax Financial Holdings, FairVentures, and takes the company’s total capital to more than $17 million. In addition to FairVentures, Connecticut Innovations, Real Ventures, and angel investors also participated.

Citing the timing of the investment, Dream Payments CEO Brent Ho-Young said the funding “propels Dream into the American market at a perfect time to serve the critical needs of businesses that are struggling to support emerging payment technologies like mobile wallets.” The company plans to use the new capital to fuel expansion in the U.S., increase its presence in its native Canada, and drive development of its third party app ecosystem. Connecticut Innovations CEO Matt McCooe praised its “unique go-to-market strategy and product offering” while Janet Bannister, General Partner of Real Ventures, spoke from the position as an “early investor,” saying “(Dream Payments is) experiencing exceptional growth as the only payments cloud powering mobile commerce for the leading North American financial institutions.”

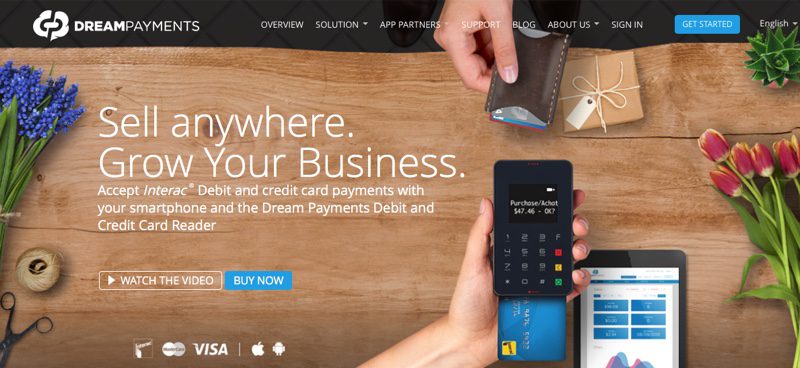

Pictured: Chief Marketing Officer Christian Ali demonstrating the Dream Mobile Point of Sale solution.

Dream Payments Cloud enables businesses across Canada to accept mobile payments by accessing a cloud-based, mobile point of sale (mPOS) solution. The company partners with financial institutions, who can then offer the PaaS solution to their business customers. In this way, Dream Payments helps consumers and businesses take advantage of both the latest and their preferred payment methods anytime, wherever they are.

Founded in 2014 and headquartered in Toronto, Ontario, Canada, Dream Payments demonstrated its mPOS solution at FinovateSpring 2015. Last month the company announced a partnership with Intuit QuickBooks to enables small business owners and entrepreneurs to accept a wider variety of payments including chip and PIN, cash, and mobile wallet. And, last fall, the company won the Global Fintech Challenge, taking home a $1.5 million investment award. In addition to Intuit QuickBooks, Dream Payments includes TD Merchant Solutions and TruShield Insurance among its partners and, later this month, expects to announce a new partnership with JP Morgan Chase.

CREALOGIX

CREALOGIX Dorsum

Dorsum ebankIT

ebankIT

Horizn

Horizn ICAR

ICAR ITSector

ITSector Mitek

Mitek

Swaper

Swaper Trustly

Trustly Wealthify

Wealthify Xignite

Xignite