This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Hong Kong’s first digital bank will use payment technology from Fiserv. The firm, ZA Bank, will use the company’s VisionPLUS global payment software, which supports the entire card payment lifecycle from origination and issuance to settlement and customer service. ZA Bank will leverage Fiserv’s suite of APIs to ensure fast and seamless app development and integration.

“We are pleased to partner with Fiserv as we embark on a journey to shift the lifestyle of future banking users,” ZA Bank CEO Rockson Hsu said. “With our companies’ combined knowledge and expertise in banking and technology, we are well-placed to respond fast to the ever-changing market with an agile product development approach.”

Licensed in March of last year, ZA Bank launched as a pilot in December with 2,000 retail customers. The pilot enabled the challenger bank to test services such as remote onboarding, time deposit, and facial recognition. ZA Bank offers 6% interest on three-month deposits of up to $25,000 (HK$200,000). Established by ZhongAn Technologies International Group, ZA Bank emphasizes a “community-driven approach” that seeks to match innovative technologies with the changing lifestyles of its customers.

“Ultimately, we want to offer superb user experiences via a robust and secure platform,” Hsu said. “I am confident that with the support of Fiserv, ZA Bank will be well-positioned to deliver relevant, convenient, and excellent service to our users.”

A long-time Finovate alum, Fiserv demonstrated its technology on the Finovate stage most recently at FinovateSpring 2018. The Brookfield, Wisconsin-based company, founded in 1984, acquired fellow Finovate alum First Data last year, and began 2020 with news of a pair of new credit union partnerships.

Speaking for Fiserv on the ZA Bank partnership, company EVP and head of Asia Pacific Ivo Distelbrink, put the collaboration in the broader context of financial innovation taking place in the region. Distelbrink called the launch of ZA Bank “an important milestone” for financial services in Hong Kong, and praised the firm as a “modern banking option aligned to the changing way people want to move and manage money.”

The Brexit challenge. Rising economies of Central and Eastern Europe. The crisis of confidence in traditional financial institutions. The growing anxiety over the power of new enabling technologies … how will innovation in financial technology be shaped by these competing interests and demands?

Next week in Berlin, Germany, Finovate will host its first fintech conference in continental Europe. From February 11 through February 13, we will present the innovators, the entrepreneurs, the analysts, and the venture capitalists who will share their accomplishments and insights with our 1200+ audience of financial professionals. Below is a sneak peek at what we have in store over the course of our three-day event. Visit our FinovateEurope page for more details.

Industry Stage Day – February 11

This year FinovateEurope kicks off with an Industry Stage Day. This day begins with a pair of keynote addresses leading into the morning’s special address from Steven Van Belleghem, author of Customers The Day After Tomorrow. The afternoon will feature a variety of tracks with their own keynotes, addresses, and fireside chats on themes such as the digital future, insurtech, open banking, and payments.

Our Industry Stage Day will also feature our new Startup Booster program. Read our interview with Finovate VP and host of the Finovate Podcast Greg Palmer on Finovate’s latest commitment to fintech’s startup community.

Demo Stage Days – February 12 and 13

The second and third days of FinovateEurope will introduce our live fintech demos into the mix. In addition to our demos, we will also feature addresses, power panels, and special analyst insight presentations to help contextualize and examine the technologies – and their applications – on display during our Demo Stage Days. Learn more about the companies demonstrating their technologies in our FinovateEurope Sneak Peek series.

Another new feature for FinovateEurope is our Women in Fintech stream on Wednesday. This special opportunity offers keynote addresses, panel discussions, and networking sessions geared toward discussing and promoting gender diversity in the fintech industry.

FinovateEurope Need to Knows

We’re excited about Finovate’s first trip to Berlin, Germany. If you’re planning on joining us, then here’s some information to help you make the most of your stay.

What: FinovateEurope 2020 – a three-day conference in Berlin, Germany featuring live demonstrations of the latest innovations in financial technology

When: The conference begins Tuesday morning, February 11, with registration at 8:30am and opening remarks at 9:15am. FinovateEurope continues through Thursday, February 13.

Where: FinovateEurope will be held at the Intercontinental Berlin, Budapester Strabe 2, Berlin, Germany.

Why: Finovate’s combination of keynote addresses, panel discussions and debates, and live technology demos is the most exciting way to keep up with what’s new – and what’s next – in the world of fintech innovation.

How: To get tickets and join us? Visit our registration page today and save your spot! Join us for our Industry Stage Day, our Demo Stage Days, or save big with an All-Access Pass that will enable you to enjoy the entire, three-day event.

The collaboration could begin as soon as March. Amazon has not commented on the report either, other than to affirm that lending is one of the services it provides to its merchant partners. In a statement, the company praised its merchants for “account(ing) for more than half of everything sold in Amazon’s stores.”

Goldman’s potential alliance with Amazon follows news of the investment bank’s 2019 partnership with Apple and Mastercard as part of the Apple Card launch. It also comes as the firm makes a number of moves that suggest it is serious about financial technology. Financial News London noted that in addition to partnership changes in recent years that have led to fewer traders and more investment bankers, Goldman Sachs is also “clearing out space for leaders in the new consumer business (it) is building.” The article highlights a pair of new Goldman Sachs partners – the founder of PFM app Clarity, which Goldman acquired in 2018, and the CEO of United Capital, a recent wealth management acquisition – as evidence of this trend.

Another example of Goldman Sachs interest in fintech, of course, is its digital bank offering, Marcus, launched in 2016. At the company’s first investor day last week, Goldman affirmed its commitment to Marcus, pledging to add a digital wealth management component and a checking account to the platform in 2021. Goldman also unveiled a new mobile Marcus app that enables accountholders to check balances, schedule transfers, and make loan payments. As reported in the company’s fourth quarter results, Marcus has $60 billion in consumer deposits.

A possible partnership with Amazon is not the only fintech headline Goldman Sachs has picked up this week. Yahoo Finance is reporting that Goldman may seek to build its own financial services cloud platform as part of a “transformational, multi-decade effort.” The report quotes Goldman Sachs co-Chief Information Officer Marco Argenti who suggested that the company would leverage it own “core technology services” for external uses in the same way that Amazon has with its Amazon Web Services platform, and potentially provide a significant new revenue stream.

The actual scope of Goldman’s initiative is what has most observers and analysts buzzing. Does the company’s stated “transformational, multi-decade effort” essentially mean Goldman-Sachs-as-a-Service? Or a full-fledged AWS competitor? Bank of America and IBM announced their intention to develop a financial services public cloud platform last fall. It will be interesting to see if Goldman’s ambition is to meet, or exceed, that goal.

Recently I came across an interesting story of how tech native GenZ kids were being paired with aging Boomers to help them navigate a variety of contemporary technology tools – from their smartphones to their SnapChat apps.

At a time when sneers like “OK Boomer” quickly trend on social media, it was a refreshing reminder of the role younger generations can play in making some of the dramatic changes in society – including technology – easier for their older family members, friends, neighbors, and even perfect strangers to navigate.

With this in mind, I wanted to take a look at how entrepreneurs are leveraging fintech to do the same thing: make it easier for seniors to not just participate in online life, but to thrive there.

Ensuring that the online and mobile worlds are a safer place for seniors is one of the important contributions that technology can make. EverSafe, which introduced its solution to Finovate audiences at FinovateFall 2014, specializes in leveraging technology to help protect seniors against financial exploitation. The company’s software examines the senior’s financial transactions and credit report on a daily basis, looking for unexpected patterns and other anomalies that may indicate potentially fraudulent activity. Once suspicious activity is detected, the user is alerted immediately and, if the activity is confirmed, a resolution process is started.

Earlier this year, Eversafe lent its technology to researchers at the Oregon Health & Science University School of Medicine in Portland. The goal is to help medical professionals uncover cognitive test markers that correlate with changes in the financial behavior of seniors. Interviewed in Alzheimer’s News Today, Dr. Kathy Wild noted that these insights could help determine when and to what extent independent living is the best option for a given senior. The results of Wild’s study are expected in 2021.

Eversafe was founded in 2012 by Howard Tischler, who is the company’s CEO. The firm is headquartered in Columbia, Maryland.

Best of Show winner at FinovateFall 2018, Golden offers technology geared toward helping older Boomers take care of their parents, many of whom are entering assisted living communities. The company’s Financial Caregiving Assistant app and Family Collaboration platform provide an array of services such as security for online accounts; automatic, on-time billpay; expense review; and a family document vault. The offering also helps seniors and caretakers to discover government benefits and drug discounts they may be eligible for. Partnerships with a variety of financial services companies gives Golden users the ability to offer branded services – including legal, financial, estate, and wealth management services – to their customers, as well.

The first company to win AARP’s Financial Innovation Award and Blue Cross Blue Shield’s Aging Innovation Challenge, Golden was launched in 2016 by CEO Evin Ollinger, and is headquartered in San Francisco, California.

Even among hardened fintech fans there was an audible gasp in the room when FinovateAsia 2019 Best of Show winner Bereev‘s CEO announced bluntly that her company’s goal was to help you “plan for your death.” Then again, it’s hard not to take a company that uses the Twitter hashtag #DeathPlan seriously.

Malaysia-based, Bereev digitizes and simplifies a life-planning process that is not only complex, but is also typically paper-intensive and burdensome. In explaining the origins of the company, founder and CEO Izumi Inoue compared the unexpected, end-of-life experience of her grandmother with the passing of her grandfather soon afterward, who had learned from his wife’s death the importance of end-of-life planning. And not just for important documents and the numbers to bank accounts, either. More personal instructions like which friends to contact were also a part of Inoue’s grandfather’s plan. They are a part of Bereev, as well.

A legacy planning solution, Bereev helps guide an individual’s family on what to do in the event of their injury, incapacitation, or death. Bereev has four components to building this contingency plan: a digital vault for important documents such as wills and insurance policies; the ability to record and save “last words” to be sent or shared with loved ones; and an accessibility console that enables the user to determine who gets access to which data and information in Bereev.

The fourth component is a guided journey that helps ensure that users provide clear instructions on how they want their affairs handled after death. The solution is set up so that all the user has to is answer a pair of questions each week, and Bereev will build out over time a personalized set of end-of-life instructions based on the user’s responses. “Before you know it,” Inoue said, “you’ll have very clear instructions left behind.”

Poignantly, Inoue notes that there are many innovations in technology in general and fintech in specific, that help you prepare and take advantage of the happier times in life: getting married, buying a first home, planning for a family. “But what about the darker and tougher times in life,” Inoue asks, “who is going to help you then? At Bereev, our goal is to help you cope through those difficult moments of life – with technology.”

Sequoia Capital has led a $35 million funding round for payments infrastructure specialist Finix. The investment, which also featured participation from Acrew Capital, Bain Capital Ventures, Activant Capital, and Inspired Capital, takes Finix’s total funding to more than $55 million. The Series B will enable the company to further grow its product and engineering teams, as well as accelerate innovation in its payments-infrastructure-as-a-service offering.

Finix’s goal is to help companies “own their payment stack” which enables them to create the payment experience that best fits their customers and business. From enhancing the merchant onboarding experience to managing the flow of funds, Finix sees control over the payment process as a “strategic imperative” that companies should not relegate to third party payment service providers. In the same way that companies like Marqeta and Plaid have made it easier for businesses to issue cards and access financial information, Finix sees itself as empowering businesses to own payments.

“Every day, our customers prove to us they are able to build superior product experiences that delight both consumers and merchants when they have full control over their payment stacks,” Finix CEO Richie Serna said.

Finix also differentiates itself by the way it charges for its service. Instead of taking a cut from each transaction, Finix opts for a fixed pricing model plus a sliding scale fee based on the number of payments processed. Finix notes that companies can go live with its system in as few as two months and at a significant savings compared to building their own in-house solution.

“Historically, software companies have had two options: either take (the) pain and integrate payments into your software, or give it to your customers in the form of a disconnected experience,” Sequoia partner Pat Grady explained. Instead, he said, companies can use Finix’s “developer-friendly building blocks” to create an integrated, seamless payment experience for customers while adding payments as a new source of revenue.

Finix was founded in 2015 and is based in San Francisco, California. The company’s customers include Passport Labs, a mobility management platform, retail POS company Lightspeed POS, and small business financing and cash flow solution provider Kabbage.

The combination of Worldline and Ingenico will create the world’s fourth largest payment services provider with 20,000 workers in 50 countries serving nearly one million merchants and 1,200 financial institutions.

Worldline announced today that it would acquire Ingenico for $8.6 billion (€7.8 billion) in a stock and cash deal. The combination would give the new entity broad reach across Europe – blending Ingenico’s strength in Germany, the Nordic countries, and France, with Worldline’s strong presence in Switzerland and Austria. The acquisition also will help the companies expand and take advantage of opportunities in the U.S., Asia, and Latin America.

Worldline Chairman and CEO Gilles Grapinet will be CEO of the combined entity. Bernard Bourigeaud, Ingenico Chairman, will take the role of non-executive Chairman of the Board of Directors once the deal is closed.

“I am proud to announce that today is a great day for Worldline and for Ingenico, and more widely for our Payment industry,” Grapinet said in a statement. “Together we create the European World-Class leader in digital payments.” In praising the Ingenico team and its leadership, Grapinet also highlighted two areas – online payments and merchant acquiring – where he expected the new entity to excel.

In his statement, Bourigeaud put the deal in the context of the other recent mega mergers – FIS and Worldpay, Fiserv and First Data, TSYS and Global Payments – in the payments space. “The combination of Worldline and Ingenico offers a unique opportunity to create the undisputed European champion in payments on par with the largest international players,” he said. “This transaction comes at (a) time of accelerating consolidation of the industry and I am convinced that the joined forces of both leaders will deeply transform the industry.”

Worldline estimates that the new company will have projected 2019 net revenues of $5.8 billion (€5.3 billion) and operating margins of $1.3 billion (€1.2 billion).

An alum of our FinovateEurope conference, Worldline demonstrated its Worldline Connected Piggy Bank solution at our London event in 2017. The offering helps provide financial education for children, encouraging savings at an early age by combining an actual, physical piggy bank with a mobile app and savings account.

Opentech has leveraged Mastercard Send APIs to offer a new solution, OpenPay Send, that will give financial institutions across Europe powerful money transfer capabilities.

“Opentech’s mission is to be the enabler of digital payments

for banks, leveraging state-of-the-art infrastructures to build highly reliable

and flexible solutions, ready to be deployed to the end user,” Opentech CEO Stefano

Andreani said. “The partnership with Mastercard and the integration with their worldwide

network is a perfect fit to our strategy, bringing a great value and

convenience to our customers.” Andreani called OpenPay Send “an important

addition to our offering.”

OpenPay Send will also enable firms to offer a broad range of services – from remittance and micropayments to insurance claim distribution and real-time P2P payments. Available via a single integration, the solution helps institutions transfer money to more than 100 corridors – including as many as three billion bank accounts – as well as mobile wallets, payment cards, and cash-out locations worldwide.

The new technology gives banks and other FIs the flexibility to tailor its offering, specifying which countries and sending channels to be activated, and at what costs. OpenPay Send also features a customizable UI for both mobile and web, as well as an administrative portal. Opentech will demo OpenPay Send later this month at FinovateEurope in Berlin, Germany.

Mastercard’s Arne Pache, VP of Digital Payments and Labs, praised the collaboration as an example of how the Mastercard Send platform improves the process of global money transfer. “(We) designed the Mastercard Send platform envisioning a better, faster, and smarter way to send money all over the world in multiple ways by leveraging our expertise and the existing relationships with our customers.” Pache added that the partnership with Opentech and launch of OpenPay Send “brings this vision to life.”

Opentech demonstrated its white-label mobile app, OpenPay for Business, at FinovateEurope 2018. The company is headquartered in both Italy and Switzerland.

Here is our weekly roundup of the latest news from our Finovate alumni:

Revolutoffers free airport lounge access to users if their flight is delayed by more than one hour.

Billtrust’s Business Payments Network is now integrated with Corporate Spending Innovations to enable their customers to automate supplier payment delivery.

Voleotaps Glen Wilson as its interim CEO. Company founder Thomas Beattie will remain as Voleo CCO.

Xignite now available in Amazon Web Services (AWS).

Jack Henrylaunches core-agnostic banking platform.

DefenseStormreports zero attrition and 50% customer growth in 2019.

FISpartners with alternative SMB funding company LiberisFinance.

Pacific Service Credit Union selectsDigital Onboarding to enhance member onboarding.

Quidmerges with social media analytics company NetBase.

ndgit and Konsentuspartner for PSD2 compliance. This week, ndgit also released version 2 of its API platform.

Arxan Technologiesrecorded 30% subscription growth in 2019.

Here’s How Far We’ve Come with Voice AI in Customer Service – When it comes to customer service, even in-person interactions can be unpleasant. And doing business over the phone is usually markedly worse, especially if there is a bot involved. There is one fintech fighting that stereotype, however.

Currencycloud Raises $80 Million in New Funding – B2B cross border payments innovator Currencycloud has locked in $80 million in new funding.

Citi Unveils Digital Investment Platform Powered by Jemstep – Launched by Citi last week and powered by Jemstep, Citi Wealth Builder is the latest addition to the world of digital investing platforms.

LendUp Tops $2 Billion in Consumer Loans Mark – Since its launch in 2011, socially responsible lender LendUp has surpassed $2 billion in consumer financing via its digital lending platform.

FICO Suite 10 Brings New Precision and Flexibility to Credit Scoring Decisions – The new technology from FICOleverages trended credit bureau data to boost its predictive power, enabling lenders to make more precise decisions on credit risk.

Splitit Taps Stripe to Facilitate Merchant Onboarding for Payment Installments – The agreement makes Stripe the payment facilitator for all new merchants who onboard with Splitit.

Also on Finovate.com

PSD2 Turns Two: Where Do We Go From Here? – Break out the PSD2 birthday cake! On January 13 the Second Payment Services Directive (PSD2)– what we now generally think of as open banking– turned two years old.

Digital Dollars and E-Euros: The Case for National Digital Currencies – In recent weeks and months, we’ve heard news of a growing number of central banks investigating the pros and cons of digitizing their money supply.

Stop Looking at Your Customer Base as a Faceless Mass – f you ask Balázs Vinnai, president of W.UP, one size does not fit all when it comes to banking. In fact, his company’s entire premise is built around creating a personalized user experience.

Follow the Money: FinovateEurope’s VC All Stars Talk Fintech Investment in Europe – This year at FinovateEurope, we’ve added a panel called Investor All Stars. It’s stacked with investors who will offer up their take on the top topics for venture capital funding in fintech.

Citi Wealth Builder is the latest addition to the world of digital investing platforms. Launched by Citi this week, the new solution features a low initial investment of $1,500 and no advisory fees for Citi Priority and Citigold clients on their initial portfolios. Citi Wealth Builder is powered by Jemstep, which demonstrated its digital advisory technology at FinovateSpring in 2013.

“We have worked closely with Citi to configure the Jemstep digital advice platform to provide a compelling client experience that supports Citi’s value proposition, omni-channel delivery capabilities and robust operational and compliance requirements,” Jemstep CEO and President Simon Roy said. Based in Los Altos, California and founded in 2008, Jemstep was acquired by Invesco in 2016.

Citi Wealth Builder works by pairing customers with one of six portfolios based on the customers’ responses to questions about their investment preferences and goals. Factors ranging as the customer’s ability to tolerate volatility to the current amount the customer already has saved are used to help ensure a good fit between customer and portfolio. The technology works automatically, monitoring and rebalancing the investment allocations; customers have the ability to adjust investment levels and see in real-time how those changes likely will affect investment outcomes.

“Citi Wealth Builder makes it easy for clients to start investing so they can reach the next level of their financial journey,” Head of Citi U.S. Consumer Wealth Management John Cummings said. “It’s part of Citi’s holistic approach to banking and wealth management. In just a few minutes, customers can start building a solid foundation for years to come.”

The new release from Citi comes a year after the firm’s launch of Citi Wealth Advisor, which gives Citigold clients their own relationship team to help them design and implement personalized financial plans. The unveiling of Citi Wealth Advisor was accompanied by Citi’s announcement that it would offer commission-free trading on ETFs and new-issue U.S. Treasury purchases for Citigold clients.

India is the latest country to announce that it is looking into development of a national digital currency – or what’s known in the industry as a Central Bank Issued Currency (CBDC). In recent weeks and months, we’ve heard news of a growing number of central banks investigating the pros and cons of digitizing their money supply. Japan announced last week that it is considering the advantage of a “digital yen.” The Central Bank of the Bahamas is also examining the issue, as is, ahem, North Korea. Tunisia made fintech headlines last fall when a Russian news agency reported the country had digitized its currency. But Tunisian authorities have since denied the story.

The case for digitizing national currencies includes the idea that, at a minimum, central banks need to keep up with – if not get ahead of – the trend toward the digitization of money. More constructively, central bank-issued digital currencies (CBDC) could provide significant benefits in terms of reducing the costs and risks to the payments system and, according to a 2018 report from the IMF, “could help encourage financial inclusion.”

However as the report makes clear, there are a wide variety of risks associated with CBDCs – the most immediate of which may be a simple lack of demand. The IMF’s Christine Lagarde made the point a few years ago in her address subtitled “The Case for New Digital Currency,” delivered at the Singapore Fintech Festival. The same “winds of change” that are driving central bankers to consider digitizing the money supply are also stimulating innovation in other forms of payment and value-storage. Any digital currency issued by a central bank still would have to compete with digital payment and value-storage offerings from the private sector.

In some ways, this is the most interesting consideration in the debate over digital currencies. Issues of safety and anonymity remain paramount, and themes like regional specificity remind us that what works for one geography may not work for another. But it is increasingly easier to imagine a world in which digital national currencies exist than it is to imagine a world in which they do not.

For more on the national digital currency movement around the world, check out Stephen O’Neal’s in-depth examination of the topic in Cointelegraph from the summer of 2018. O’Neal divided the world of state-issued currencies into the Adopters, the Rejectors, the Experimenters, and the Researchers. Note that Tunisia, as reported above, is no longer in the Adopters category, however the country’s central bank did note that it is “exploring” digital payment options including CBDC.

Additionally, some of the countries that have rejected national digital currencies have appeared to reconsider in recent years. A report from last fall suggested that private bankers and lenders in Germany, for example, have expressed interest in a form of “digital central bank money.”

This week on the Finovate blog we celebrated the second birthday of PSD2 in Europe, and highlighted the advances Israeli startup and Finovate Best of Show winner Voca.ai has made in deploying voice AI in customer service. We also previewed our upcoming FinovateEurope Venture Capital All Stars presentation on fintech investment trends in Europe.

Here is our weekly look at fintech around the world.

Asia-Pacific

Contour, a blockchain-based trade finance platform headquartered in Singapore, announces investment of undisclosed size from Standard Chartered.

Malaysian cross-border payments company Tranglo integrates with Ripple.

Digital-only banks may be coming to Thailand as the country’s central bank considers offering digital banking licenses.

Sub-Saharan Africa

South African fintech Oyi launches prepaid medical savings card.

Inlaks, a Nigeria-based ICT infrastructure solutions provider, introduces new line of “ultramodern” ATMs that feature the ability to access customer service via a live video connection.

FinTech4U Accelerator names the five Zambian fintechs that will join its program this month.

Central and Eastern Europe

Leading browser provider Opera acquires Estonian banking-as-a-service startup Pocosys.

German fintech Heidelpay is on the hunt for acquisition opportunities and is considering an IPO.

EU Startups features Cashpresso in its look at top Austrian startups to watch in 2020.

Middle East and Northern Africa

Arab News features Nosaibah Alrajhi, founder of Shariah-compliant P2P lending platform Forus, scheduled to go live in Saudi Arabia later this year.

Al Khaleej Bank of Sudan to deploy Path Solution’s core banking iMAL platform.

A digital rupee? That’s the proposal from India’s National Institute for Smart Government (NISG).

Fintechs are not the only ones disrupting financial services in India. Increasingly, smartphone brands are getting into the act.

Indian fintech startup Mera Cashier raises $250,000 in seed funding.

Latin America and the Caribbean

Softbank strikes again! The Japanese firm has led a $125 million Series B round for Mexico’s AlphaCredit.

Americas Quarterly looks at ways that fintech can become “a priority” in Latin America.

Olivia, a Brazilian financial wellness app, raises $5 million in funding from BV (formerly Banco Votorantim).

As Finovate goes increasingly global, so does our coverage of financial technology. Finovate Global is our weekly look at fintech innovation in developing economies in Asia, Africa, the Middle East, Latin America, and Central and Eastern Europe.

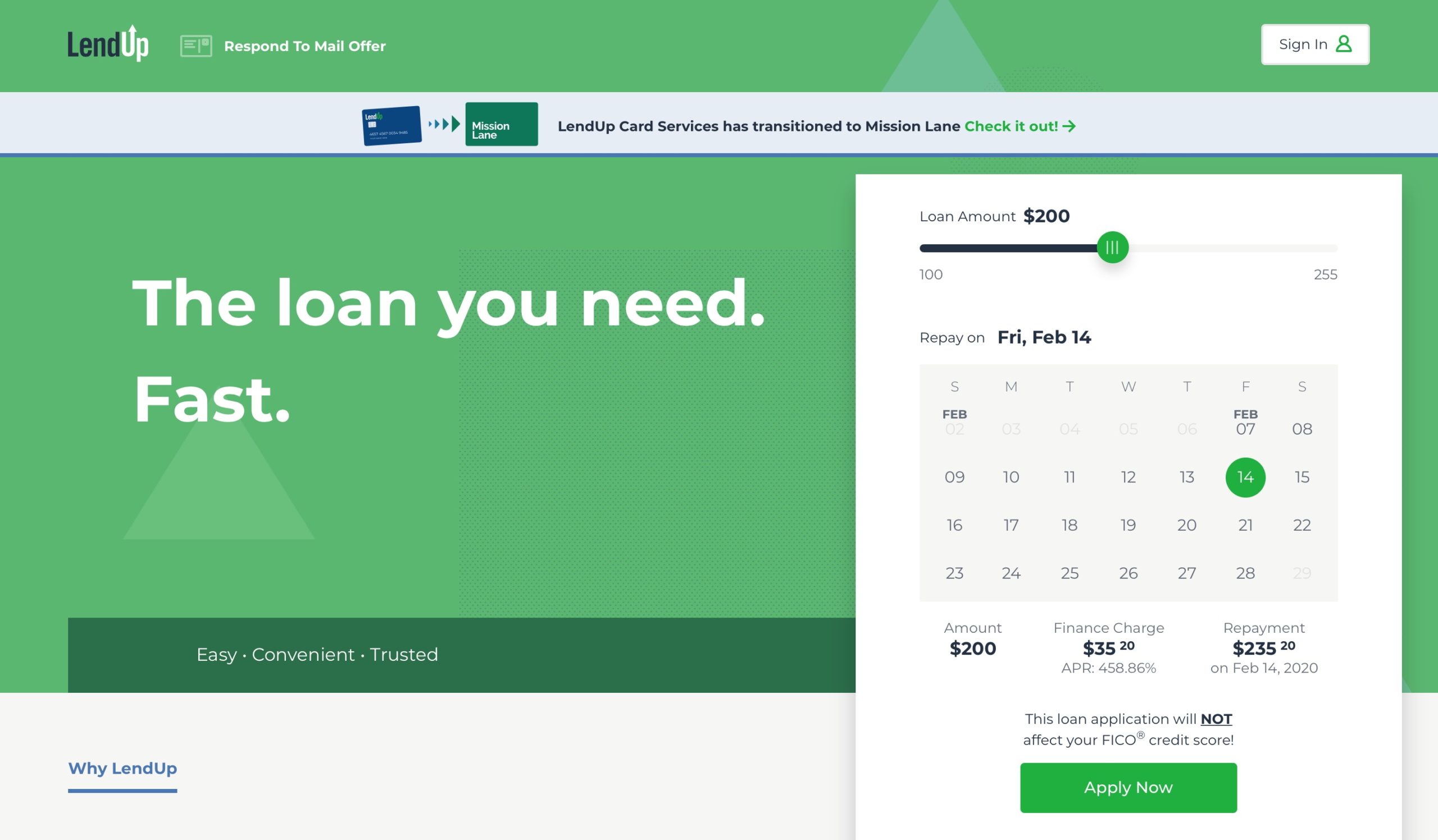

Since its launch in 2011, socially responsible lender LendUp has surpassed $2 billion in consumer financing via its digital lending platform. This represents 6.5+ million loans, with an average loan value of $300.

“We’re very proud of this significant lending accomplishment, the progress we’ve made in driving disciplined, profitable, and sustainable growth, and our role as a standard bearer for responsible and inclusive lending and banking,” LendUp CEO Anu Shultes said.

One of the fintechs to embrace early the concept of financial wellness, LendUp combines access to financing via its short-term installment loans. The company offers financial education and a specific-but-personalized strategy to help consumers improve their credit, the LendUp Ladder. This resource uses gamification, education, and good borrower behavior to enable borrowers to earn points that allow them to apply for larger loan amounts at better rates. The company notes that its customers have taken more than two million financial education courses via its platform.

“Through our lending, education, and savings programs, we’ve helped customers raise their credit profiles by hundreds of thousands of points cumulatively and saved them hundreds of millions of dollars in interest and fees from much higher cost products,” Shultes explained. She added that the $2 billion mark was a “real testament to the impact that financial service providers like LendUp can and should have on the market.”

It’s worth noting that this week’s announcement comes on the one-year anniversary of Shultes’ appointment as CEO; Shultes took over the company last January from co-founder Sasha Orloff. Shultes was formerly LendUp’s GM and has been credited for helping grow the company’s loan originations to more than 5.5 million.

LendUp demonstrated its financing platform at FinovateSpring 2014. The San Francisco, California-based company has raised more than $360 million in funding from investors including PayPal Ventures and Victory Park Capital. The company spun-off its credit card business, Mission Lane, as a stand-alone entity a year ago, which has allowed LendUp to focus on its lending and financial wellness businesses.

FICO announced this week that its latest credit risk solutionFICO Score 10 Suite will be available to lenders via the U.S. credit reporting agencies this summer. The new technology leverages trended credit bureau data to boost its predictive power, enabling lenders to make more precise decisions on credit risk.

The company said that the new Score 10 Suite could reduce the number of defaults in a lender’s portfolio by up to 10% for newly originated bankcards, and 9% among newly originated auto loans versus the previous, FICO Score 9. The new solution performs even better with newly originated mortgage loans, the company added, with a 17% reduction in defaults.

“FICO is a cornerstone for consumer lending decisions,” Jim Wehmann, executive vice president for Scores at FICO said. “We continuously innovate using the latest, most robust data, while maintaining consistency with previous models to ensure backward compatibility and minimize operational changes required to adopt a new score.”

The company is touting the use of trended data as one of the key enhancements of the new technology. Trended data provides a historical view of data like account balances which gives lenders a more complete understanding of how an applicant manages their finances. At the same time, FICO Score 10 maintains FICO Score minimum scoring criteria, and features backwards compatibility with previous versions of FICO Score. This helps ensure that lenders experience a seamless transition to the new offering with maximum ease of use and stability.

In addition to the emphasis on trended data, the new scoring regime also takes an interest in personal loans that the applicant may have. The increasing use of personal loans, to pay down credit card debt for example, has grown in recent years. MarketWatch noted earlier this week that personal loans are the fastest-growing debt category in the U.S. The takeaway is that FICO Score 10 will make it easier for those who are managing their finances well to avoid being penalized for instances when debt might spike due to a large, single-instance purchase. Meanwhile, those who are adding debt (personal loan, home equity loan, etc.) as a strategy to manage their debt may find the new scoring criteria more challenging.

FICO closed out 2019 with the release of two new products and an acquisition. In November, the company launched FICO Identity Proofing, a digital onboarding solution; and FICO User Authentication, a set of multi-factor authentication functionalities. Both new solutions were made possible by the company’s acquisition of security access provider EZMCOM that month.

An alum of our developers conference, FinDEVr New York 2016, FICO was founded as Fair Isaac Corporation in 1956. The company is based in San Jose, California.

Five months. A quarter of a million new U.S. customers.

That’s the news from Berlin, Germany-based challenger bank, N26, which announced this week that it has added 250,000 new customers in the U.S. within five months of its August launch.

Calling American consumers “too reliant on traditional banks,” N26 U.S. CEO Nicolas Kopp suggested that the wave of new U.S. customers was just the beginning. “We’re incredibly proud to have reached a quarter-million U.S. customers in our first five months and we’re just getting started. We have big plans to offer millions of future N26 users a feature-rich, easy-to-use banking experience.”

The challenger bank, which launched in the U.S. last year courtesy of a partnership with Axos Bank, offers its new U.S.-based customers a regulated, FDIC-insured account, a Visa debit card, and basic spending management tools like account activity display, daily spending limits, and automatic transaction categorization. In December, N26 introduced its Perks program for U.S. customers, giving them cashback rewards and discounts for purchases made on their N26 debit card.

N26 gives its customers the ability to open accounts in less than five minutes, transfer money to friends instantly with MoneyBeam, and leverage a tool called Spaces to open sub-accounts to manage savings goals. The accounts have no hidden fees, and accountholders have access to a network of more than 55,000 surcharge-free ATMs. Customers who sign up for direct deposit can access their pay up to two days early.

Gains in the U.S. notwithstanding, N26 points to Europe as the source of most of the growth in its customer base – which reached 3.5 million last summer and now stands at five million. N26 co-founder and CEO Valenti Stalf heralded the five million customer milestone, but suggested the achievement is only a step on the journey the company has set out for itself when it was founded in 2013. “(We) have not forgotten our original mission – to challenge an industry that is ripe for change,” Stalf said. “N26 has proved that banking can be simple and intuitive through the use of technology.”

N26 has raised more than $680 million in funding, with $470 million of the challenger bank’s equity capital coming last year.