This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A holiday-shortened week begins with Independence Day in the US celebrated on Friday. Be sure to check with Finovate’s Fintech Rundown for the latest fintech news as the second half of 2025 gets underway in earnest!

Digital banking

Greece-based core banking vendor Natechraises $33 million in Series B funding.

Financial data network Plaid has been in the fintech headlines of late for its new partnership with data and technology company Experian, and for the launch of its Plaid Protect fraud prevention solution.

“Today we’re launching Plaid Protect: a real-time fraud intelligence system that helps detect and prevent fraud from the moment a user first interacts with your app or service,” Plaid Head of Fraud Alain Meier wrote on the company blog. “By drawing on fraud signals across a billion devices in the Plaid network, Protect goes beyond what any single company can see—surfacing fraud patterns that exist between linked bank accounts, connections to financial apps and services, and more.”

Plaid Protect is built on an adaptive, machine learning-powered risk engine that provides real-time risk scores and attributes that evolve as the user context changes—from initial contact during onboarding through account linking to ongoing user activity. Calling their fraud model Trust Index (Ti), Plaid’s first production model can access 10,000 high-signal attributes including cross-app patterns, device history, bank account risk signals, and more. The Trust Index leverages network intelligence, bank account risk, consortium feedback, and advanced identity intelligence, keying in on fraud signals that are difficult for criminals to manipulate or fake. Plaid reported that one of the solution’s early adopters found in testing that enhancing verification for just 5% of its users would have intercepted nearly 40% of first-party fraud.

Currently available in beta, Plaid Protect provides an intuitive dashboard that uses semantic search powered by natural language. This means that users can ask questions about the data in plain English (i.e., “all users who opened new accounts in the last 30 days”) instead of needing to use SQL or custom queries.

“With this new lens on fraud, companies can reduce fraud losses, dramatically improve conversion, and make smarter decisions from the very first user interaction and every step thereafter,” Meier wrote.

Plaid’s new product announcement comes days after the company reported that it had partnered with fellow Finovate alum, Experian. The two firms have entered into a strategic collaboration designed to help businesses access cashflow solutions and expand financial inclusion.

“This is just the beginning of what we believe will be a very powerful relationship with Plaid,” Group President Financial Services of Experian North America Scott Brown said. “Together, we’re helping to accelerate the adoption of cashflow insights to drive faster decisions, stronger portfolios, and new financial opportunities for consumers. We’re achieving this while delivering an experience that is transparent and provides consumers with control every step of the way.”

Courtesy of the collaboration, financial institutions can access Plaid’s secure connectivity capabilities—used by 50% of all US bank account holders—and Experian’s expertise in advanced credit analytics and decisioning from a single solution. Once a borrower agrees to share cashflow data from their bank account as part of the loan application process, Plaid’s consumer reporting agency generates a Consumer Report on their behalf. The report is delivered securely to Experian which analyzes the applicant’s data, produces a predictive Cashflow Score or set of Cashflow Attributes, and delivers it to the lender in near real time.

The report features up to two years of historical data and cashflow information from 12,000+ financial institutions. Experian reports that its Cashflow Score provides an increase of as much as 25% in predictive performance compared to scores that rely on more conventional credit data. The new offering will empower banks, credit unions, and consumer lenders to accelerate decision-making, make more accurate risk assessments, and improve borrower outcomes.

“Our work with Experian is about removing long-standing barriers, making it easier for lenders to access consumer-permissioned data and make better decisions,” Plaid Chief Operating Officer Eric Sager said. “Together, we’re building a more inclusive, intelligent, and competitive financial system.”

Founded in 2013 by Zach Perret and William Hockey and headquartered in San Francisco, Plaid introduced itself to Finovate audiences at our developers conference, FinDEVr Silicon Valley 2014. In the years since, the company has grown into a major financial data network covering more than 12,000 financial institutions in the US, Canada, UK, and Europe. With partners including Venmo and fellow Finovate alums SoFi and Betterment, Plaid works with fintechs, Fortune 500 companies, and leading banks to enable their customers to connect their financial accounts to the apps and services they count on every day.

With Father’s Day behind us and the first official day of summer ahead, we keeping our eye on the fintech headlines as the summer news slump approaches. Be sure to check in with Finovate’s Fintech Rundown all week long for the latest announcements in the industry.

GrailPayraises $6.7 million to make ACH payments more secure.

Fiserv and Early Warning Servicescollaborate on Paze to provide financial institutions and merchants of all sizes with a convenient digital checkout solution for consumers.

Empower Federal Credit Union tapsIlluma to launch voice authentication.

Lending

Baker Hillunveils enhancements to its platform to help financial institutions better manage commercial real estate, CECL compliance, AI-driven compliance, agricultural spreading and financial analysis.

Finastra’sFilogixboosts Gen AI capabilities to empower mortgage brokers.

Digital banking

Digital banking solution provider for small businesses, Autobooks, introducesAutobooks Capital, powered by Fundbox, integrating business lending directly within the Autobooks platform.

The dust is still settling in the wake of Circle’s “buzzy IPO” in the words of MarketWatch. We’ll see if the fintech headlines can keep up this week!

Digital banking

KAF Digital Bank goes live with Temenos SaaS to bring Islamic digital banking services to customers in Malaysia.

ABN AMRO’s payment app Tikkie has developed a full-service bank, BUUT, that caters to younger customers.

Digital bank N26unveils an updated version of its premium subscription, N26 Go.

Open banking solutions provider Salt Edgepartners with digital banking experience platform Plumery.

Farsightraises $16 million in funding, announces Series A to automate financial workflows and decision-making.

Fraud prevention and identity verification

FrankieOne launches new risk and compliance platform that offers fraud detection and identity verification.

Cybercrime consultancy We Fight Fraud partners with Salv to facilitate intelligence sharing between financial institutions in Europe.

Regtech iDenfyteams up with international hosting provider SpaceCore to bring optimized customer verification to global hosting.

The Bank of International Settlements (BIS) and the Bank of England (BoE) collaborate on testing to see if AI can spot fraudulent activity in retail payments data.

AML and CFT solutions provider AMLYZEonboards Advanzia Bank as part of its European expansion.

Veleraadds real-time account validation functionality to digital channels.

Legislation in California moves forward to give the state authority to seize unclaimed cryptocurrency assets held on exchanges after three years of inactivity.

The arrival of Daylight Savings Time in much of the West is yet another reminder that Spring is right around the corner. Here’s Finovate’s Fintech Rundown with some fintech news—including some funding and partnership news from a handful of long-time Finovate alums—to help you get caught up on the latest updates and announcements in our industry.

Worthsecures $25 million investment led by TTV Capital to drive major enterprise growth and expand workflow automation solutions.

Dwolla announces the general availability of its expanded integration with Plaid, allowing its clients to leverage Plaid’s instant account verification and real-time balance check and pay-by-bank payments.

Experian is integrating ValidMind’s AI governance and risk management tools into its Ascend Platform to help banks automate and streamline AI compliance.

The collaboration enables financial institutions to automate model validation, risk tracking, and audit readiness.

The combined solution will not only simplify AI adoption in financial services, but will also ensure compliance with key regulations like SR 11-7, E-23, SS1/23, and the EU AI Act.

Today’s environment of ever-changing regulations and technological developments in AI is making it difficult for banks to stay on top of AI compliance. To help banks manage these challenges, Experian is integrating its Ascend Platform with AI governance and risk management platform ValidMind.

Experian Ascend helps organizations make better decisions by providing them with access to extensive data and advanced analytics tools. The tool combines information from various sources, including credit and market data, and leverages AI and machine learning to offer insights to help firms better understand their customers, manage risks, and identify new opportunities.

Integrating ValidMind will help Experian automate model development and validation documentation using customizable, pre-built templates for credit, fraud, and other models. It will also enhance risk governance with robust racking, monitoring, and audit readiness features, ultimately enhancing regulatory compliance.

“Our collaboration with ValidMind complements our Ascend Platform and offers our customers innovative technology to automate and accelerate their model risk management processes,” said Experian Software Solutions President Keith Little. “This partnership empowers financial institutions, insurance companies, and fintech organizations to meet regulatory challenges with confidence and agility.”

The new combined solution, which meets compliance requirements including SR 11-7, E-23, SS1/23, and the EU AI Act, integrates AI into templates to ensure that banks generate consistent, high-quality documentation organized to streamline regulatory submissions.

“This partnership is poised to establish a new industry standard for scalable, automated model risk management,” said ValidMind CEO Jonas Jacobi. “Together, we can help financial institutions reduce risk, improve efficiency, and accelerate the adoption and implementation of AI, Gen AI and statistical models.”

California-based ValidMind was founded in 2022. The company’s enterprise platform helps organizations document, validate, and govern models at scale. ValidMind also offers statistical models, AI models, and GenAI models to streamline documentation, simplify compliance, future-proof existing models, and unlock new business models in a transparent way. The company raised just over $8 million in its first funding round last year.

This week’s edition of Finovate Global looks at recent fintech headlines from Ireland.

NomuPay secures $37 million at a valuation of $200 million

Dublin, Ireland-based fintech NomuPay announced an investment of $37 million this week. The funding round, which began in September, gives the company a valuation of $200 million. The company will leverage the new capital to help accelerate the expansion of unified payment access in Asia.

“Over the past two years, we’ve grown our revenue by 100% annually and are on track to become profitable this year with an Annual Recurring Revenue (ARR) of $20 million,” NomuPay’s Faye Duncan wrote on the NomuPay website. “Our valuation has reached $200 million, and with this latest funding round, our total funding now stands at $90 million. We’re proud to support over 1,600 merchants — including Ikea — and look forward to expanding into markets like Indonesia, Japan, and Vietnam, while continuing our M&A efforts.”

Founded in 2021, NomuPay offers state-of-the-art, unified payment solutions to help businesses scale in high-growth regions in Europe, Asia, and the Middle East. The company’s uP Platform offers high-penetration alternative payment methods; real-time payout disbursements; and compliant, end-to-end marketplace funds management.

This week’s investment will help NomuPay assist international acquirers, merchants, Payment Service Providers (PSPs) and Independent Sales Organizations (ISOs) as they seek to expand in markets such as those in Asia, where differences between local regulations and a broad variety of payment methods add to both cost and complexity.

To this point, NomuPay CEO Peter Burridge noted that many organizations are stymied by the offerings of the dominant international gateway acquirers that, in some instances, provide limited access or fewer payment options. Burridge called for a more “sophisticated and less prescriptive approach.”

Experian acquires debt consolidation technology from Paylink

To help millions of consumers better manage their debts, international data and technology company Experian announced this week that it will acquire ReFi, the debt consolidation innovation from Paylink Solutions. ReFi, which specifically helps manage the “double counting” challenge in lending, will become a part of the Experian Consumer Services Marketplace.

“Our research shows that millions of consumers are stuck in a revolving debt trap, due to the systemic issue of ‘double counting’ when consumers apply for debt consolidation products,” Experian Consumer Services Managing Director Edu Castro explained. “ReFi’s innovative solutions will play a crucial role in addressing the debt challenges faced by many consumers, unlocking access to debt consolidation products that could help them save money on their debt and even pay it off sooner.”

Double counting can occur when an individual applies for a debt consolidation loan and a lender counts both the individual’s original debts and their new consolidation loan as part of the affordability assessment. Lenders “double count” because there is no guarantee that the funds from the new consolidation loan will be deployed to retire existing debt. This means that otherwise creditworthy individuals can be denied consolidation loans to help them more affordably pay off their debts.

ReFi provides this assurance for lenders, working with both parties to settle debts directly with existing creditors. This enables applicants for consolidation loans to be assessed solely on the basis of the consolidation loan amount. And as debt is paid off, old accounts are closed, providing convenience for customers and further bolstering confidence for lenders.

“The team who built ReFi feel tremendously privileged to already have helped thousands of people reduce their monthly outgoings and cut the amount of interest they have to pay overall,” Paylink CEO Jake Ranson said. “Becoming part of Experian will enable us to further innovate, accelerate, and grow the impact ReFi will have on delivering better outcomes for lender and borrower alike.”

Founded in 2017 and headquartered in Grantham, Lincolnshire, U.K., Paylink Solutions launched its ReFi solution in the fall of 2023. Piloted by financial wellness company Salary Finance, ReFi has saved Salary Finance customers more than £10 million in interest payments.

With its corporate headquarters in Dublin, Ireland, Experian helps businesses around the world enhance lending practices, fight fraud, and better engage their customers. A Finovate alum since 2011, Experian is a FTSE 100 Index company, publicly traded on the London Stock Exchange under the ticker EXPN.

Data privacy firm Dataships raises $7 million in Series A funding

Data privacy software company Datashipssecured $7 million in Series A funding. The round was led by Osage Venture Partners, and featured participation from Lavrock Ventures and the Urban Innovation Fund. In a statement, the company said that the funding will help “accelerate our mission to help merchants dramatically grow their marketing lists while maintaining ironclad data privacy compliance.”

Founded in 2019 and headquartered in Dublin, Dataships began as a compliance technology company and has since transitioned to compliance management. The company notes that it has helped its merchant customers realize a 10x increase in SMS opt-in rates, a 3x to 4x boost in email marketing contacts, and $112 million in additional revenue generated via 1.1 million repeat purchases. Dataships recently announced a pair of new innovations to its platform: SMS Easy Opt-in, which replaces “Reply Y” with in-checkout verification, and A/B Testing Engine that provides transparent measurement of baseline versus opt-in rates.

“We’re building Dataships to be the essential growth platform for modern e-commerce brands,” the company’s Matt Gottron noted in a blog post. “One that transforms compliance from a burden into a competitive advantage, helping merchants build larger, more engaged marketing lists that drive sustainable revenue growth.”

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Latin American payments service processor Kuady introduced its new physical prepaid Mastercard for users in Peru after launching a virtual version in September.

Onchain finance solutions provider Tokeny has teamed up with El Salvador-based Digital Asset Service Provider Ditobanx.

Visalaunched its 2025 Accelerator Program for African fintechs.

BusinessDay Nigeria examined the impact of cybercrime on Africa’s fintech and digital banking industries.

Central and Eastern Europe

Germany-based fintech unicorn N26 announced its first profitable quarter to close out 2024.

Lithuania and Romania earned praise for their growth potential in sustainable banking in a recent report from the International Sustainable Finance Centre (ISFC).

Financial Times featured German fintech Trade Republic as the firm announces it has no intention to go public at this time.

As October gets underway in earnest, Finovate’s Fintech Rundown shares news of expedited payments to help those impacted by hurricane Helene, another partnership to help new Canadians secure credit, as well as a major investment in cross-border payments and a big acquisition in the fraud prevention space.

Be sure to check back all week long for more fintech news and updates!

Experian has partnered with affordability software and payments company Paylink.

Experian will leverage Paylink’s ReFi solution, which will validate and repay consumers’ outstanding debts by consolidating them into a new loan with better terms.

ReFi will allow consumers to conduct a financial reset, while offering lenders the assurance that the new loan is affordable.

Data analytics and consumer credit reporting company Experian is broadening its services this week by expanding its debt consolidation offering. The Ireland-based company is leveraging a partnership with affordability software and payments company Paylink, which will help work around affordability restrictions with debt consolidation loans.

Experian reports that the number one reason consumers search for loans on its marketplace is for debt consolidation. However, lenders are unable to directly pay off customers’ debts when they take out a debt consolidation loan. This means that, during the underwriting process, lenders need to double count both the new loan and existing debts. As a result, some consumers are unable to qualify for debt consolidation loans, since the new loan is considered ‘unaffordable.’ This can result in consumers borrowing from an unlicensed lender, loan shark, or friends and family.

“The benefit of this partnership is twofold, as the ReFi solution offers a valuable tool for lenders to expand their offerings and reach a broader customer base that may have originally been overlooked,” said Experian Consumer Services Managing Director Eduardo Castro.

In today’s partnership, Experian aims to promote financial inclusion and improve access to credit using Paylink’s ReFi tool. ReFi validates and repays consumers’ outstanding debts by consolidating them into a new loan with better terms. After validating a consumer’s card, loan, and overdraft accounts, ReFi confirms balances and settlement amounts, pays creditors, and offers evidence that the accounts are closed.

“ReFi enables a financial ‘reset,’ potentially leading to significant savings and quicker debt repayment,” said Paylink CEO Jake Ranson. “It also provides lenders with assurance that the new loan is affordable and will be used to clear previous debts, helping customers achieve their financial goals. With unparalleled access to data, analytics and market insight, Experian is singularly placed to help ReFi reach thousands more people seeking to realize the opportunities access to reasonably priced credit brings.”

Experian and Paylink are not alone in trying to help consumers struggling with debt. There are a handful of other players in fintech seeking to help consumers solve their debt burdens. Finovate alums Peach, Payitoff, and Debbie, which demoed their technologies at FinovateFall last year, each bring a fresh approach to debt management and payoff. These platforms are not just about numbers; they aim to empower consumers with tools that simplify debt repayment, offering tailored strategies to help users regain financial stability.

The battle against fraud is a never-ending one. And recent fintech news headlines have helped remind us all of how broad the frontlines are. From the challenge of AI-powered deepfakes to the sad fact that many of our own bad habits continue to keep fraudsters in business, fintechs are busy developing solutions to help us get and stay at least one step ahead of the bad guys. Here are a trio of stories highlighting the latest efforts by fintechs to combat financial crime.

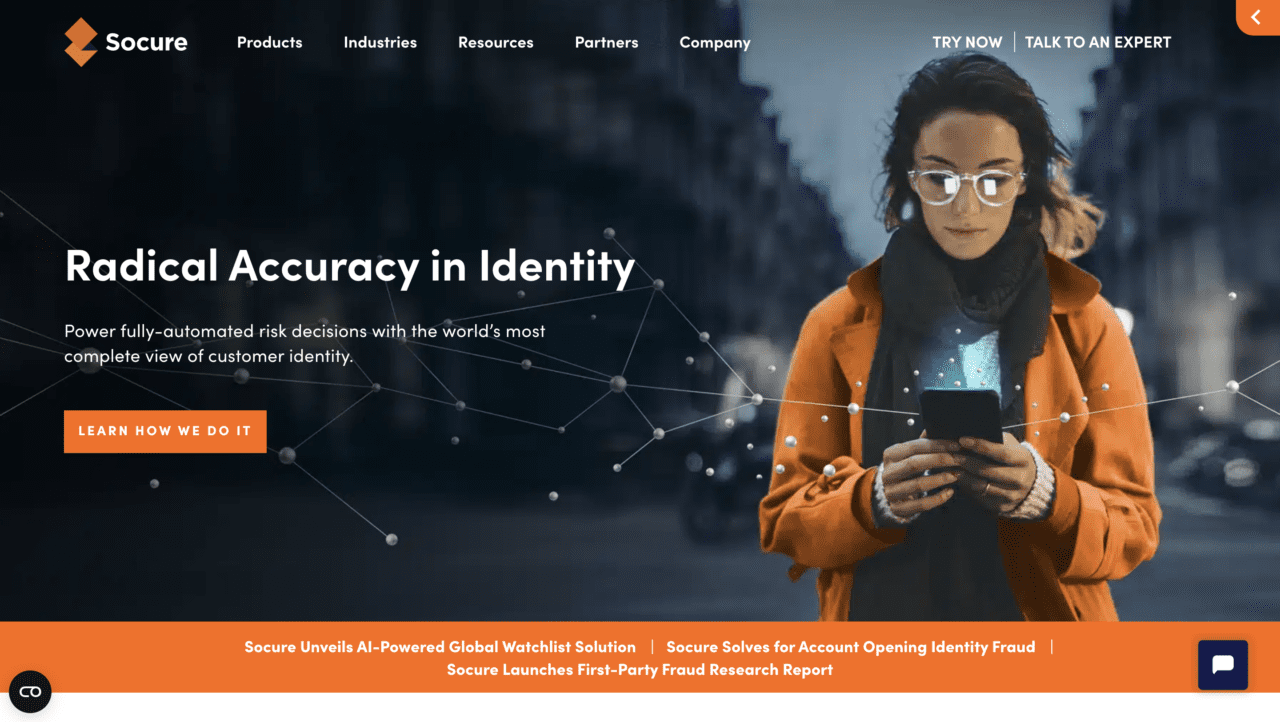

Digital identity verification innovator Socure has unveiled its Selfie Reverification solution. The new capability provides a way to validate return consumers online in less than two seconds with just a selfie. The technology matches incoming selfies with previously verified ID headshots, and features a true match rate of 99.9%. Built on the company’s Document Verification (DocV) solution, Selfie Reverification also detects signs of deepfaking, and readily identifies age discrepancies between the photo and the credential.

“Identity verification isn’t a one-time event. As consumers interact with an online service over time, their risk profile can change. That’s why it’s important to determine you are still who you say you are, without going through the full verification process again,” explained Socure Chief Product and Analytics Officer Pablo Abreu.

Selfie Reverification prompts the user to take a selfie, and sends real-time feedback on positioning, angle, and lighting. Once taken, the selfie undergoes a Level 2 NIST PAD compliant liveness check to prevent spoofing, as well as Socure’s injection attack detection process which makes sure that a fraudster has not injected a false or altered credential into the session. Lastly, the selfie is compared against a set of hundreds of thousands of curated deepfake samples created by more than 20 different AI generators.

The technology leverages biometric analytics to evaluate more than 80 facial features, from eye distance and nose width to jawline contours and emotional expression, to create a facial map and ensure an accurate match. Use cases for Selfie Reverification include preventing account takeover, securing high-risk transactions, streamlining account recovery and re-verification/re-validation, and more.

Founded in 2012 and headquartered in Incline Village, Nevada, Socure most recently demoed its technology on the Finovate stage at FinovateFall 2017. Today, the company has more than 2,500 customers, including four of the top five banks, the top credit bureau, and 400+ fintechs. Businesses ranging from Capital One and SoFi to DraftKings and the State of California rely on Socure’s technology for accurate identity verification and fraud prevention. Johnny Ayers is Socure’s founder and CEO.

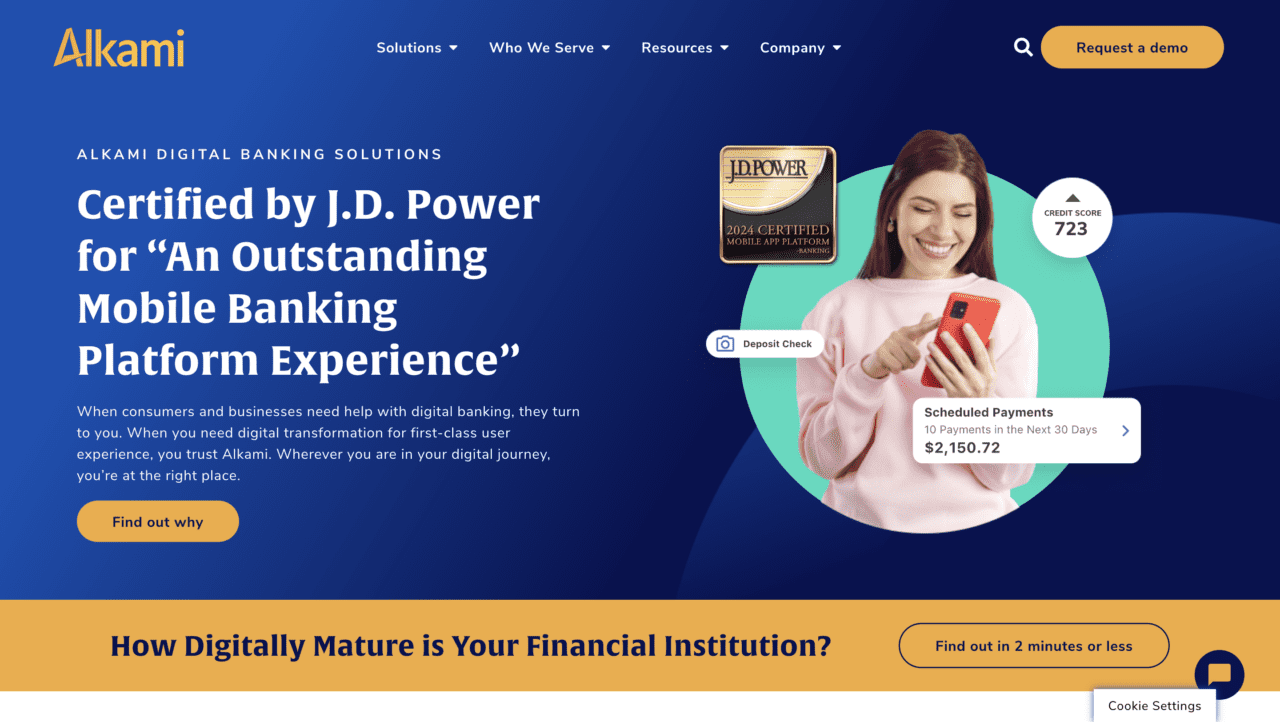

Digital banking solution provider Alkami has added credential stuffing protection to the challenge-response authentication process for its digital banking platform. The new functionality automatically checks for human behavior in the background, but does not require visual puzzles or any additional time spent by the user.

“This enhancement in Alkami’s platform has given us the ability to provide an additional layer of security for our account holders,” Quontic Bank SVP of Digital Banking Grace Pace said. “The secure and seamless login experience has contributed to reducing potential fraudulent activities, offering our customers greater peace of mind without added complexity.”

Credential stuffing refers to a type of cyberattack in which a hacker uses credentials obtained through data breaches or purchased from the dark web in order to attempt to access another service. A typical case of credential stuffing, for example, could involve a hacker using the credentials from a breach at a retail store to attempt to log into a bank’s website.

Credential stuffing is a common attack in part because it takes advantage of the tendency of individuals to reuse usernames and passwords. But its commonality takes nothing away from the damage these attacks do. One estimate determined that credential stuffing costs businesses $6 million a year on average, to say nothing of the negative reputational impact that often accompanies it.

The addition of credential stuffing protection is the latest example of Alkami’s layered approach to fraud detection and prevention in digital banking. “Alkami continues to evolve its platform as the security threats change for our customers, and we’re proud to integrate credential stuffing as part of our standard solution for everyone,” Alkami Director of Product Management Brad Cranford said. “Our goal is to help our customers manage security while providing the best experiences for their account holders.”

Headquartered in Plano, Texas, Alkami made its Finovate debut in 2009 as “IThryv.” Alex Shootman is CEO.

Data and technology company Experian is adding behavioral analytics to its fraud detection capabilities courtesy of a newly announced acquisition of NeuroID.

More specifically, Experian is looking to bolster its defenses against AI-generated fraud threats. With their ability to apply fraud detection strategies to key vulnerabilities such as origination and account management, insights from behavioral analytics can help mitigate fraud in real time and defend users against a range of malevolent actions including identity theft, account takeover, bot attacks, and fraud rings.

“Our acquisition of NeuroID highlights our commitment to provide our clients with world-class data, analytics, and insights to prevent fraud,” said President of Experian’s North American Identity & Fraud business, Robert Boxberger. “Together with NeuroID, we’re excited to build new blended offerings that detect risk but also empower businesses to confidently navigate the online landscape and trust in their transactions.” He added, “In today’s highly competitive and digital-first world, the use of behavioral analytics is now vital for innovating for the future of fighting fraud.”

NeuroID’s solutions are now available via CrossCore on the Experian Ascend Technology platform. The integration will enable platform users to use a single service provider to monitor and analyze real-time digital activity.

“NeuroID unlocks a new view into a user’s riskiness based on behavioral interactions,” NeuroID CEO Jack Alton said. “This view arms companies with a proactive, first line of defense to detect sophisticated fraud rings and bot attacks. By joining forces with Experian, we’re looking forward to helping companies confidently navigate this new era with solutions that enable more secure and frictionless experiences.”

A Finovate alum since 2011, Experian most recently demoed its technology at FinovateFall in New York in 2018. Headquartered in Dublin, Ireland, the company employs more than 22,000 people, including more than 9,000 technologists and product developers, working in 32 countries.

Are you an innovative fintech with new technology that’s ready for prime time? Join us in New York next month for FinovateFall and take advantage of the opportunity to showcase your solution before an audience of 2,000+ decision-makers.

We’re midway through August, and while everyone attempts to sneak in their final summer vacation days, the fintech news continues on. While we’ve seen a handful of acquisition news headlines so far this summer, I expect things to tick up slightly this fall. Stay tuned throughout the week to read the latest news this week as we post updates and evolutions.

Experian launched Cashflow Attributes, a tool to offer lenders more data about underserved consumers.

Cashflow Attributes offers lenders visibility into more than 900 consumer attributes that reflect consumers’ cashflow and affordability.

Lenders can use the insights to aid in their underwriting decisions, drive more personalized experiences, and help improve financial management tools.

Information services company ExperianunveiledCashflow Attributes yesterday, a new solution that leverages open banking to help underserved consumers access fair and affordable credit.

Cashflow Attributes uses more than 900 income, cashflow, and affordability attributes to allow lenders to integrate applicants’ banking data into the decision-making process. Experian expects the new solution will help some of the 106 million U.S. consumers who are considered credit invisible, unscoreable by conventional credit scores, or have a subprime or below credit score and are therefore unable to secure credit at mainstream rates. Credit Attributes layers traditional credit report data with cashflow insights to create a more detailed view of a consumer’s financial health and creditworthiness.

“Supporting financial inclusion and creating an equitable path to credit is ingrained in our DNA,” said Experian Financial and Marketing Services Group President Scott Brown. “We believe banking information holds untapped potential and that our new Cashflow Attributes represent an exciting step forward that can easily be integrated into lending decisions. As we look ahead, we will continue to leverage our core credit data, new data elements and our analytics expertise to unlock new opportunities for both consumers and businesses.”

To use Cashflow Attributes, lenders first provide Experian with depersonalized transaction information from their existing customers or from customers at other banks, as long as they have consumer-permissioned account access. Experian uses its categorization model to analyze and categorize the consumer transaction data and sends the lender the transaction categories and predictive attributes. Lenders can use these categories and attributes to aid in their underwriting decisions, drive more personalized experiences, and help improve financial management tools.

Founded in 1980 and originally known for its consumer credit reporting, Experian has extensive access to data and has added fraud prevention offerings, identity theft protection, credit building tools, and a loan comparison marketplace. On the commercial side, Experian provides a range of services for small businesses, including business credit reporting, marketing products and services, debt collection tools, and more. The company is headquartered in Dublin, Ireland, and is listed on the London Stock Exchange under the ticker EXPN and has a market capitalization of $39.5 billion.