This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Spring has sprung, March Madness is in the air, and the fintech headlines are filled with new payment solutions to enhance face-to-face commerce, new developments in the tokenized asset space, and a range of announcements on agentic AI including new tools, new partnerships, and new deployments.

Be sure to check back with Finovate’s Fintech Rundown all week long for the latest in fintech news!

Payments technology company Splititunveils its Splitit Go mobile and API-based solution that brings card-linked installment payment options to in-person commerce.

Fraud prevention and identity verification

Digital identity and compliance platform ComplyCubeunveils its expanded fraud intelligence suite.

Finix and Plaid team up to enhance bank verification and streamline money movement.

Australian fintech Vivi Moneychooses Pismo’s infrastructure to launch new AI-native financial solution on Visa’s global payment network.

Constant AI, an agentic AI firm that specialists in lending operations for credit unions, launches AI Skip-A-Pay agent, Nia.

AI platform Go AbacusunveilsThe Go1, an on-prem AI hardware solution to give banks data sovereignty. Catch Go Abacus in its Finovate debut at FinovateSpring 2026 in San Diego.

Insurtech

AI assistant for financial advisors, Zocks, introduces its new AI assistant for life insurance. See Zocks make its Finovate debut at FinovateSpring 2026 in San Diego, May 5-7.

DeFi

Q2partners with digital asset platform Stablecore to enable banks and credit unions to offer stablecoins, tokenized deposits, and other digital asset products.

TAPP Engine and KoreInside team up to bring financial stablecoins to private capital markets.

This week’s edition of Finovate Global showcases recent fintech news from Canada.

Royal Bank of Canada acquires mortgagetech Pinch Financial

The Royal Bank of Canada (RBC) has acquired Toronto-based mortgagetech Pinch Financial. Terms of the transaction were not disclosed, but the move is designed to accelerate the decisioning process for mortgage borrowers throughout the country.

“This acquisition helps us deliver on our commitment to bring the best solutions to clients on their path to home ownership,” RBC SVP of Home Equity Financing Janet Boyle said in a statement. “Pinch’s technology will help us accelerate our digital roadmap to deliver a quicker, more streamlined mortgage experience for Canadians.”

Founded in 2016, Pinch Financial offers banks, lenders, and other financial services providers a platform that allows them to verify data and automate mortgage applications. The company’s technology verifies identity, income, assets, liabilities, source of the down payment, and creditworthiness to establish whether a borrower meets the requirements—from TDS and FICO to LTV and net worth—for rate and underwriting eligibility.

RBC already plays a major role in Canada’s mortgage market. The acquisition of Pinch Financial will help the bank serve customers who prefer to apply for home loans online instead of in-person at a branch.

“We started Pinch to make mortgages more relevant and familiar for digital-first consumers—making the qualification process faster, simpler, and more transparent for borrowers,” Pinch Financial CEO Andrew Wells said. “This acquisition gives us the opportunity to bring our technology to more Canadians while being part of a team that shares our vision for innovation in financial services.”

Canada’s largest bank by market capitalization and assets—and one of the largest banks in the world—RBC serves more than 19 million clients in Canada, the US, and 27 other countries. Headquartered in Toronto, Ontario, and boasting more than 101,000 employees, RBC reported total assets of $1.9 trillion CAD as of October 31, 2025. Dave McKay is President and CEO.

Wealthsimple becomes first Canadian fintech to join SWIFT

Canadian fintech Wealthsimple has secured a big “first” and a big “second” this week. The firm became the first Canadian fintech and the second non-bank fintech in the world to become a member of the SWIFT global financial messaging network. The company is currently completing final technical integration and security certification ahead of a full launch with clients expected later this spring.

“Many Canadians rely on international wire transfers, and yet to date, the experience has been clunky and expensive. We want to fix that,” Wealthsimple VP of Payment Strategy Hanna Zaidi said. “Our SWIFT membership is going to unlock faster, simpler, and more transparent international money transfers for the more than three million Canadians who trust Wealthsimple.”

SWIFT’s international messaging network serves 11,000 financial institutions around the world, facilitating trillions of dollars in payment volume. SWIFT makes the sending and receiving of international money transfers more seamless and efficient, while also providing end-to-end tracking visibility with real-time status updates.

Wealthsimple’s SWIFT membership is part of the company’s overall strategy to lower costs and boost efficiency for money movement in Canada. Wealthsimple also announced that it will be an early adopter of the country’s pending Real-Time Rail (RTR) payment system, making its clients among the first to benefit from instant money movement between institutions.

Founded in 2014 and headquartered in Toronto, Canada, Wealthsimple offers a wide range of financial products and services, including managed investing, do-it-yourself trading, cryptocurrency, tax filing, spending, and saving. The company serves more than three million Canadians and has more than $100 billion in assets under administration. Co-founder Michael Katchen is CEO.

KPMG: Canada fintech investment “moderated” in 2025

The bad news is that investment in Canadian fintech slowed in 2025. The good news is that this moderating pace comes on the heels of record highs notched in 2024.

KPMG International recently unveiled its Pulse of Fintech H2’25 and FY25 report. The document depicts a fintech investment landscape in Canada that has returned to more historic levels, with “sustained interest in later-stage companies, platform acquisitions, and strategically important fintech subsectors such as artificial intelligence and digital assets.”

Specifically, the comparison is $2.4 billion across 113 deals in 2025 versus $9.9 billion across 161 deals in 2024. The report notes that much of the deal value in 2024 came from two sizable transactions: Nuvei’s $6.3 billion public-to-private buyout and Plusgrade’s $1 billion private equity deal. In 2025, the two largest investments in Canadian fintech were the $898 million private equity buyout of Converge Technology Solutions and Wealthsimple’s $536 million equity raise.

The report notes that investment activity in the sector picked up in the second half of 2025, especially with regard to gains in average deal value. Dubie Cunningham, a partner in KPMG Canada’s Banking and Capital Markets Practice specializing in fintech, indicated that she believed the strength in the second half of 2025 augured well for strength in 2026. “The investment appetite for Canadian fintechs will continue to grow in 2026, as investors prioritize quality, scale, and strategic fit, signaling a market that is maturing and aligning more closely with long-term value creation,” Cunningham said.

NCR Voyixagreed to sell its bank technology business in Japan to NTT Data.

An analysis of the Australian fintech sector by Deloitte Access Economics and FinTech Australia reported that the sector could grow to $71 billion in value by 2035.

Sub-Saharan Africa

Kenya and Rwanda inked an agreement that could enable digital payments companies licensed in one country to operate in the other.

South African fintech PayInc and First Capital Bank Botswana teamed up to launch instant cross-border payments.

The Fintech Times analyzed the fintech ecosystem of West African country, Burkina Faso.

Central and Eastern Europe

Part of Estonia’s Iute Group, IuteBank has begun operating as a regulated bank in Ukraine.

Earned wage access provider Express Wages has partnered with Good Hands Home Care to give employees advanced access to their earned income.

Express Wages facilitates payday advances of up to $200 a day. Money transfer options include a no-fee Visa Prepaid card, and repayment is managed systematically via the Express Wages app and company payroll platform.

Memphis, Tennessee-based Express Wages made its Finovate debut at FinovateSpring 2025 in San Diego.

“We’re proud to partner with Good Hands Home Care,” Express Wages Founder and CEO Alfred Milan said. “Caregiving is deeply meaningful and important work, and strengthening financial stability plays a big role in helping care professionals stay focused on the people and families they serve.”

Express Wages offers a platform that provides employer-integrated, on-demand pay solutions. The company’s plug-and-play technology enables companies to give their employees immediate access to a portion of their earned wages before payday. For workers who are living paycheck-to-paycheck, this early access before payday can help them avoid high-interest predatory loans, unnecessary credit card debt, and overdraft penalties.

Employees can receive up to $200 a day via Express Wages payday advance, with money transfer options including a no-fee Visa Prepaid card. Next-day ACH transfers and instant transfers to debit cards are also available, with transaction fees of $3.95 and $4.95, respectively. Repayment is automatically deducted from the employee’s next paycheck via the app and payroll platform.

Companies using Express Wages can offer the service to employees without making any changes to payroll or experiencing negative impacts on cash flow. Built to ensure both easy integration and interoperability, Express Wages requires no software installation and connects with hundreds of human resources information systems including ADP, Gusto, QuickBooks, and more in a matter of a few days.

In its partnership announcement, Express Wages noted research from a 2025 Bankrate report that indicated that more than a third of Americans had to use funds from their emergency savings in the last year, with nearly one in five Americans having no emergency savings at all. These conditions are what can make consumers vulnerable to high-interest financing products at times of financial stress. In response, a growing number of companies such as Good Hands Home Care are leveraging solutions like earned wage access to give employees greater options when it comes to managing their finances.

“At Express Wages, we focus on building tools that benefit real working lives,” Milan said. “Earned wage access is about offering greater choice and control—giving people more ways to respond when unexpected expenses hit.”

Founded in 2023 and headquartered in Memphis, Tennessee, Express Wages made its Finovate debut at FinovateSpring 2025 in San Diego. At the conference, the company showed how a new feature on its app delivers financial wellness experiences to help users improve their financial literacy.

How can banks, credit unions, and other financial institutions transform the massive volumes of data they process every day into actionable insights that can drive better decision-making, identify inefficiencies, and engage more customers? How will technologies like AI specifically help financial institutions challenged by competition from non-bank rivals, ever-evolving consumer expectations, and regulatory uncertainty?

This year at FinovateSpring 2026, we are showcasing five innovative fintechs that will demonstrate their solutions to help banks, credit unions, and other financial institutions boost productivity, manage risk, and create compelling experiences for their customers and members.

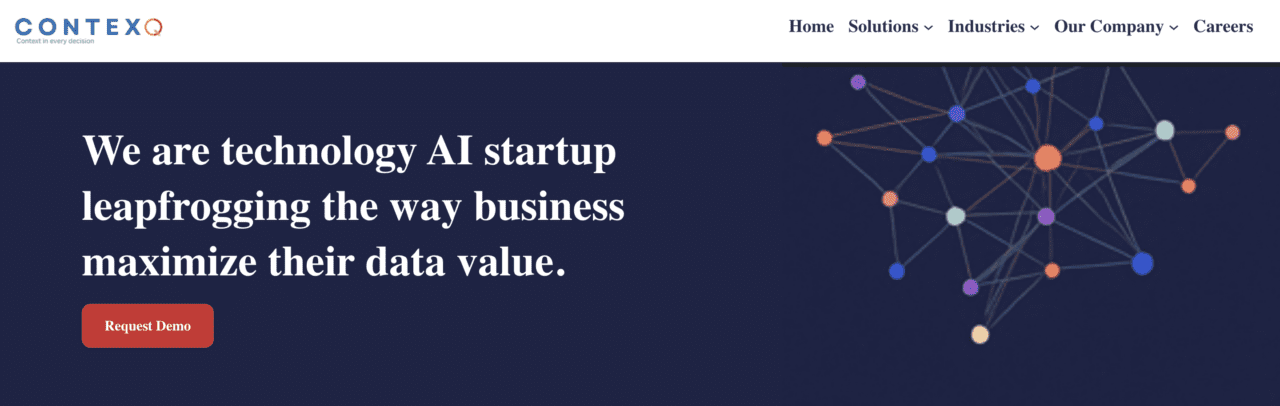

ContexQ is a forensic Graph AI that detects fraud, money laundering, and hidden beneficial ownership by seeing the relationships every other AI misses.

Headquartered in Singapore, ContexQ was founded in 2024. The company’s technology resolves fragmented identities across more than one billion entities in 12+ languages, predicts emerging fraud patterns using Graph Transformers, and unifies risk and revenue intelligence in one graph.

Finalytics.ai enables financial institutions to instantly unleash the power of AI by offering segment-of-one digital experiences for visitors informed by behavioral, transactional, and third-party data.

Founded in 2021, Finalytics.ai is headquartered in San Francisco, California.

Whatfix is an AI-native digital adoption platform that helps banks and other financial institutions accelerate system adoption, enforce compliance, and achieve measurable outcomes across mission-critical workflows.

Founded in 2013 and headquartered in San Jose, California, Whatfix offers technology that provides real-time contextual guidance powered by AI-driven ScreenSense, product analytics tied to workflow adherence and business outcomes, and mirror + AI roleplay for risk-free simulation and behavioral training.

Why banks should care

Managing risk, providing compelling personal experiences for customers, and keeping costs low are three paramount challenges for banks, credit unions, and other financial institutions in 2026. Fortunately, all three are areas where technologies such as automation, machine learning, and AI have proven their effectiveness in detecting fraud, customizing user journeys, and identifying workflow inefficiencies and bottlenecks.

Meeting these challenges by embracing fintech innovation is not only a way for banks to ensure regulatory compliance, stay ahead of fraudsters, and become more efficient—it also offers opportunities for specialization and differentiation within the field. At a time when more and more companies are adding financial services to their product mix, innovations that also help banks and credit unions stick out from the crowd are as valuable as ever.

If you are enjoying our preview of the companies demoing at FinovateSpring this year, then join us in San Diego on May 5 through May 7. Register today using this link and save 20%.

Pay by Bank infrastructure provider Token.io unveiled its Account on File feature this week.

The new feature securely recalls a user’s preferred bank and accounts and presents these as defaults for future transactions, boosting the convenience of Pay by Bank.

Token.io was founded in 2015 and made its Finovate debut the same year at FinovateSpring. Todd Clyde is CEO.

Token.iolaunched its new Account on File feature this week. Designed to boost the convenience of Pay by Bank, the new offering securely recalls a user’s preferred bank and accounts and presents them as default selections for future transactions. Token.io said that Pay by Bank will be a boon to payment service providers (PSPs) and merchants across the UK and Europe, enhancing the customer experience and increasing checkout conversion rates.

“For high-frequency transaction scenarios, such as e-commerce purchases or account top-ups, every extra step costs you customers,” Token.io Director of Product Sam French said. “With our new Account on File feature, Pay by Bank can become a one-tap experience for returning payers, driving high conversion rates for merchants, while giving consumers a secure, familiar way to pay straight from their bank accounts.”

Like Card on File, Account on File helps streamline the typical Pay by Bank experience, removing up to two steps. This results in fewer clicks, faster checkouts, fewer drop-offs, and more completed transactions. Account on File will enable merchants to settle faster, experience lower processing costs, and benefit from the improved cash flow that comes with account-to-account (A2A) payments.

Additionally, Token.io has put tokenization at the core of its new Account on File feature, enhancing both security and trust. Tokenization swaps sensitive account details for a non-sensitive token. This token is used to reference the user’s bank account(s) without exposing sensitive, underlying information.

Token.io’s latest offering comes at a time when Pay by Bank is becoming increasingly popular. The company’s own research indicated that 90% of PSPs offer or expect to offer Pay by Bank in the near future. Token.io’s Account on File feature is currently available through the company’s latest API.

Founded in 2015 and headquartered in London, Token.io made its Finovate debut at FinovateSpring 2015. The company most recently demoed its technology at FinovateEurope 2017. Today, Token.io is a leading A2A payment infrastructure provider with partners including three of Europe’s five largest financial institutions, as well as major payments companies such as fellow Finovate alums Mastercard and ACI Worldwide.

Payouts and treasury platform PayQuicker launched its 1099 tax reporting solution, powered by fellow Finovate alum Avalara.

The new offering helps reduce the complexity of 1099 filing while keeping companies compliant with the latest regulatory mandates.

New York-based PayQuicker made its Finovate debut at FinovateFall 2022. Avalara is an alum of Finovate’s developer conference, FinDEVr Silicon Valley 2015.

PayQuicker, a payouts and treasury platform that made its Finovate debut at FinovateFall 2022 in New York, has introduced its new 1099 tax reporting solution. Powered by agentic tax and compliance specialist—and fellow Finovate alum—Avalara, the new offering will help companies streamline and automate 1099 reporting while reducing both compliance risk and administrative burden.

“Businesses need reliable automated solutions to stay compliant without slowing down operations,” PayQuicker CFO Joe Bertalli said. “By partnering with Avalara, we’re able to provide our customers with a robust 1099 solution that reduces complexity, increases accuracy, and gives them confidence in their compliance processes.”

PayQuicker’s 1099 solution enables companies to collect W-9 and other W-series tax forms over the course of the year to help ensure accurate payee information at all times. PayQuicker’s solution also leverages real-time Taxpayer Identification Number (TIN) matching to validate data at the point of collection. This helps reduce the potential for costly backup withholding notices, penalties, and corrections at a time when regulatory requirements around tax reporting for businesses are becoming increasingly complex.

Powered by Avalara’s tax compliance technology, PayQuicker’s 1099 solution provides scalable, secure, and compliant tax reporting for businesses managing sizable numbers of payees. The solution facilitates the accurate and efficient generation, filing, and distribution of 1099 forms supported by automated federal and state filing, electronic delivery, and ongoing regulatory updates.

“PayQuicker is focused on making complex financial workflows easier for businesses,” Avalara General Manager for 1099 Reporting Queenie Lee said. “We’re excited to power their 1099 solution with Avalara’s compliance expertise, enabling customers to automate reporting and reduce risk while staying focused on growth.”

An alum of Finovate’s developer conference, FinDEVr Silicon Valley 2015, Avalara leverages an expansive library of tax content and industry integrations to serve more than 200,000 direct and indirect customers in more than 75 countries. Avalara’s purpose-built AI agents automate compliance processes from tax calculations and return filings to exemption certificate management and more. Avalara has helped companies achieve an 85% reduction in time spent managing tax returns and a 50% reduction in time spent on exemption certificate management. Scott McFarlane is Co-Founder and CEO.

Headquartered in Rochester, New York, PayQuicker made its Finovate debut at FinovateFall 2022. At the conference, PayQuicker demonstrated its Payouts OS solution which packages the company’s technology into an in-market payouts orchestration platform. Payouts OS leverages a single REST API that plugs into multiple banks and international payment rails to identify and facilitate the fastest, most cost-effective way for clients to make payouts to businesses and consumers around the world.

Embedded finance platform Array has been on a truly remarkable acquisition pace in recent weeks. The company, which won Best of Show in its Finovate debut at FinovateFall 2021 and again in its return to the Finovate stage for FinovateSpring 2022, acquired fellow Finovate alum—and fellow Best of Show winner—Penny Finance in late February. This move came just a few days after Array announced its acquisition of another Finovate alum and Best of Show winner, Chimney.

And just to show that Array’s appetites are not limited to Best of Show-winning Finovate alums, the company also announced its acquisition of paytech EarnUp less than a month ago.

What do these acquisitions mean for Array? Overall, these deals represent the company’s strategy to provide its financial institution partners with modular, embeddable tools and data that enable them to boost engagement, improve retention, and secure measurable value. Designed to complement the solutions currently offered by fintechs, financial institutions, and digital brands, Array’s embedded, invisible-by-design approach allows consumers to enjoy a wider range of financial solutions and services while still relying on the brands they know and trust.

Consider Penny Finance. Penny Finance is an online financial planning engine that enables credit unions and community banks to provide personalized education, resources, and services to their members and customers. Headquartered in Boston, Massachusetts, and founded in 2020 by CEO Crissi Cole, Penny Finance helps individuals and families pay off debt, begin investing, and build wealth—all within a unified, integrated solution. Array Founder and CEO Martin Toha said that acquiring Penny Finance will enable Array to serve consumers the same way that they experience financial challenges and responsibilities: “as part of a single, ongoing journey.”

“Penny Finance strengthens our ability to support that full picture,” Toha said, “enabling our partners to deliver more holistic, consumer-first financial experiences directly within the products people already use.”

The acquisition will empower Array to help its clients address a broader range of consumer needs and complements the company’s current credit, identity, and privacy offerings with solutions to help consumers enhance their financial wellness through better savings behavior and financial planning.

“Penny was built to give people confidence in how they spend, save, and plan—without judgment or complexity,” Penny Finance’s Cole said. “By joining Array, we can scale that mission and integrate financial education and planning tools into trusted experiences that already play a meaningful role in people’s financial lives.”

Array’s acquisition of Chimney will add the fintech’s modern financial calculators and home value tracking tools to its platform offerings. Founded in 2020 and based in Brooklyn, New York, Chimney helps more than 160 financial institutions in the US leverage real-time property data and predictive analytics to engage homeowners and grow loans. Chimney’s technology identifies high-propensity opportunities for home equity, refinancing, new mortgages, and more, enabling financial institutions to target the right customers and members at the right time with personalized offers delivered inside their banking apps and platforms. In his statement, Chimney CEO and Co-Founder Matthew Covi underscored this last point, highlighting the value of embedded finance in helping consumers get the resources they need while remaining engaged with the brands they trust.

“Traditional financial institutions are where the majority of Americans manage their finances,” Covi said. “By empowering these institutions with personalized, data-driven solutions that modernize the banking experience, we’ve realized our mission of helping millions of Americans live healthier financial lives.”

Lastly, EarnUp is a payments technology firm that helps consumers better manage debt and bills by aligning mortgage, loan, and bill payments with pay cycles. By enabling them to disaggregate large, inflexible monthly payments into smaller contributions aligned with their paychecks, EarnUp helps lower the amount of missed payments to creditors and financial stress for debtors. Headquartered in San Francisco, California, and founded in 2015, EarnUp has completed 50 million transactions with a cumulative value of $43 billion since inception. Brad Woodcox is CEO.

“EarnUp is a long-standing proven product in the home loan space, having supported millions of US mortgage borrowers through deep integrations with leading mortgage servicing platforms,” Toha said. “We hope to use this distribution and product to extend Array’s reach into the home loan payments space. This acquisition strengthens our ability to help financial services providers deliver more practical, consumer-centric experiences—especially for households managing tight margins and multiple debt obligations.”

Founded in 2020 and headquartered in New York City, Array most recently demoed its technology at FinovateSpring 2023. At the conference, the company demonstrated two of its latest financial solutions—HelloPrivacy (now Privacy Protect) and Subscription Manager—to help banks and other financial institutions generate noninterest income and boost engagement while providing customers with resources to help them stay safe online and save money. Privacy Protect helps defend users from identity theft and privacy risks by monitoring and removing personal information from the web. Subscription Manager helps users manage their subscriptions better, canceling unused subscriptions and negotiating lower rates on select subscriptions.

FinovateSpring 2026 will take place at The Sheraton San Diego on May 5-7. Register today using this link and save 20%.

Regtech Napier AI unveiled Insights AI, its new solution to help companies enhance their anti-money laundering (AML) screening processes.

The new offering will help financial crime compliance teams close key gaps in AML investigations by providing behavioral analytics and AI-enabled explanations of contributing activity.

Headquartered in London, Napier AI made its Finovate debut at FinovateEurope 2018.

AI-powered financial crime compliance solutions provider Napier AIannounced new functionality in its Transaction Monitoring solution that will help firms with their anti-money laundering (AML) screening. The new offering, Insights AI, provides behavioral analytics and natural language explanations for use in financial crime compliance, closing what Napier called “critical gaps” in anti-money laundering investigations.

The new functionality comes courtesy of an innovation partnership between Napier AI and the UK Financial Conduct Authority (FCA), with the company leveraging the FCA’s Supercharged Sandbox to test new models and strategies. The goal was to provide financial crime compliance teams with a tool that would surface clear, AI-enabled explanations of customer behavior beyond the initial alert. These insights would be available directly within transaction monitoring tasks, highlighting behavioral patterns and illuminating potential new or emerging risks during the investigation. This is because, for most compliance teams, the challenge is less total alert volume and more about investigation inefficiency. To this end, Insights AI identifies relevant behavioral patterns, explains contributing activity in context, reduces the amount of time spent on manual data analysis, and enables compliance teams to focus on more complex issues during the investigation process.

Napier Chief Data Scientist Janet Bastiman underscored the value of the relationship between the company and the FCA. “Participating in the FCA Supercharged Sandbox allowed us to design and run new approaches to testing AI models for anti-money laundering,” Bastiman said. “One of the biggest historical challenges in tackling complex money laundering typologies is the disconnected nature of the data required for pattern analysis along the complete lifecycle of customer behavior or transaction flows.”

Under the name “Project Theseus,” the technology was tested for pattern mining and fluid dynamics as part of the FCA Supercharged Sandbox Showcase. This involved the deployment of frequency-based AI algorithms on large-scale synthetic financial data sets to identify money laundering typologies more effectively than traditional rules-based systems—while using significantly less computing power. The tested AML transaction monitoring models now form part of the Napier AI Continuum platform and support the company’s newly announced Insights AI feature.

“The embedding of Insights AI into our Transaction Monitoring solution is all about ensuring the incredible data science behind the scenes is surfaced in a way that puts power into the hands of AML analysts, to make the best possible human-in-the-loop decisions for the alerts,” Napier AI Chief Product Officer Will Monk said. “We lead with a compliance-first approach to AI in AML by partnering closely with the FCA so we can ensure our product aligns with regulatory guidance and meets policy goals around reducing the impact of economic crime on the UK.”

Founded in 2015, Napier AI made its Finovate debut at FinovateEurope 2018 in London. At the conference, the company demonstrated how its customer screening and transaction monitoring enhancement software enables firms to enhance their AML and client screening processes. The company’s technology helps reduce false positives by up to 80% while significantly lowering operational risk and cost.

Napier AI began the year with the launch of MV Shield—Powered by Napier AI. The fruit of a partnership between Napier AI and banking technology provider Mutual Vision, MV Shield is a compliance-as-a-service (CaaS) solution built specifically for building societies and credit unions in the UK and Canada. MV Shield provides an alternative to standard AML systems, aligning its controls, reporting, and risk models to the specific needs of membership-based financial institutions.

With St. Patrick’s Day at the beginning of the week and the first day of spring at the end, it feels as if we are truly leaving winter behind us. Cacti are blooming here in the desert southwest and the fintech news —from new offerings in wealth management to the latest innovations in agentic AI—is flowing. Be sure to check back here at Finovate’s Fintech Rundown all week long for updates.

Digital banking

BankDhofarlaunchesNeo Corporate Internet Banking (Neo CIB), its next-generation digital banking platform.

DNERO, a neobank that caters to Latino customers, readies for a March 24 launch.

Digital asset wealth management platform Abraannounces plans to go public via SPAC merger with New Providence Acquisition Corp at a valuation of $750 million.

Sokinlaunches stablecoin capabilities to provide hybrid finance platform unifying digital assets and fiat.

Agentic AI

Lithuanian fintech Chaseit.aiintroduces AI agents to automate loan servicing and call center communications.

Integrated financial management platform for freelancers and gig economy workers, Finom, launches its embedded interest account.

Iwocaintroduces free financial health resources, including its Credit Compass, for small businesses in the UK.

Lending and Credit

Experian launches its AI-powered Experian Virtual Assistant (EVA) to deliver real-time, personalized financial insights and recommendations on financial products such as credit cards, loans, and insurance.

Ocrolusaccelerates automated conditioning for mortgage lenders with full lifecycle management.

Back end technology

FMSI and Applipartner to help credit union branches drive member revenue.

This week’s edition of Finovate Global looks at recent fintech headlines from Scotland.

AutoRek Launches RegToolKit

Automated reconciliation and financial control solutions provider AutoRek has launched its AutoRek RegToolKit. The new offering will help financial services companies simplify, track, and demonstrate their compliance with complex regulations.

AutoRek RegToolKit maps client products and services against regulatory requirements to ensure that companies can become compliant as well as prove their compliance with regulatory authorities. The solution features an applicability matrix across regulatory requirements, business risks, and mitigating controls, providing a comprehensive overview for all legal entities and product lines and reducing the audit burden. AutoRek RegToolKit uses an in-built breach register to identify compliance breaches, assign ownership, and track the process through to remediation, avoiding reliance on both spreadsheets and manual audits. The new offering complements the company’s data management, reconciliation, and reporting platform providing a consolidated data, governance, and oversight solution.

“Firms are required to not only control their data, but also evidence that their processes align with regulatory rules,” AutoRek Chief Product, Technology, and Operations Officer Jim Sadler said. “RegToolKit takes the complexity out of compliance by mapping rules to controls, tracking non-conformity, and providing a complete audit trail. Combined with our reconciliation platform, it allows firms to achieve full end-to-end financial control and compliance.”

Founded in 1994, AutoRek made its Finovate debut at FinovateEurope 2023. At the conference, the Glasgow, Scotland-based regtech demonstrated how its intuitive, configurable dashboards help firms manage the pain points in the reconciliation process. The company’s machine learning-based technology monitors the performance of reconciliations, disaggregating and categorizing outstanding balances, highlighting escalation points, and more. AutoRek helps institutions transition away from spreadsheets and manual processes toward greater control and efficiency.

FreeAgent Integrates with Sodium Software, Active | UK

Edinburgh, Scotland-based fintech FreeAgent has announced a handful of integrations in recent days. First, the company reported that it had integrated with cloud-first workpapers and accounts platform Active | UK. Active works with core accounting systems to boost accuracy and standardize workflows. The partnership will enable users to automatically import data from FreeAgent into Active Workpapers, reducing the potential for human error and enabling faster, more consistent reporting.

Second, just this week FreeAgent reported that it has integrated with accounting practice management platform Sodium Software. The partnership is designed to help accounting professionals and teams in the UK streamline CRM, proposals, workflows, invoicing, and more. Connecting FreeAgent accounts to Sodium will enable accountants and teams to sync client data instantly and directly monitor the status of clients. In a LinkedIn post, FreeAgent added that further functionality, including automated billing and bookkeeping insights, is “coming soon.”

Founded in 2001, Active | UK is celebrating its 25th year as a technology partner for accounting firms. A division of Active by Business Australia, Active | UK helps companies standardize processes and workflows to ensure that all team members are working in the same way. Active | UK offers automated accounting workflows to seamlessly populate and sync data, and an intuitive Excel split pane that gives users greater control and transparency over figures and calculations.

Officially in public beta, Sodium Software was launched in late 2025 as a practice management platform for UK accountants. While seeing practice management as “the foundation,” the company has noted that its roadmap extends beyond this to include AML, payments, accounts production, and more. Sodium Software recently unveiled new features including unlimited custom fields, pricing tiers, and the ability to make both client and bulk updates.

FreeAgent made its Finovate debut at FinovateEurope 2013 in London. Founded in 2007, the company today has more than 200,000 small businesses, accountants, and bookkeepers using its accounting software

Insurtech Wrisk Acquires Atto, formerly DirectID

Here’s some M&A news from last month that slipped under our radar: Independent embedded insurtech platform for the automotive OEM sector Wrisk has acquired real-time financial intelligence platform Atto. Terms of the transaction were not disclosed.

Atto enables companies to make context-aware credit and risk decisions within live customer journeys. Leveraging open banking to securely access and analyze transaction-level data, Atto’s technology transforms it into actionable insights that can be embedded into regulated, enterprise-grade customer experiences. Wrisk, which partners with automotive OEMs to embed insurance directly into the consumer journey, will use Atto’s financial intelligence solution to offer greater flexibility in how financing and protection products are designed and delivered.

The acquisition will also enable Atto to take advantage of Wrisk’s OEM relationships, delivery capability, and regulated operating framework to deploy its capabilities across a broader range of markets and use cases.

“Atto has built a credible financial intelligence and credit scoring platform with real-world enterprise use,” Wrisk Chief Executive Officer Nimesh Patel said. “Joining Wrisk allows us to combine that intelligence with a delivery layer that serves brands and other partners at scale.”

Edinburgh, Scotland-based Atto rebranded from DirectID in 2024. DirectID was launched in 2016 as the flagship product of James Varga’s The ID Company (which itself was a rebrand of Varga’s miiCard, a digital verification company and Finovate alum founded in 2011).

“Joining Wrisk represents a natural next phase in Atto’s growth,” Atto Strategic Programme Advisor Rob Knight said. “We have proven the value of open banking-driven credit intelligence with enterprise clients, and Wrisk brings the regulated operating framework and delivery capability required to deploy that intelligence at scale. Together we can embed credit decisioning, affordability, and actionable insights directly into live finance and protection journeys.”

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

We Are Tech Africa profiled Algerian fintech platform Gifty, which offers a single app for shopping, billpay, mobile top-ups, and digital gift cards.

MENA-based fintech Network International and ADCB Egypt went live with FICO Falcon Fraud Manager.

The Times of Israel looked at how momentum from 2025 will drive the Israeli fintech industry in 2026.

Central and Southern Asia

State Bank of India forged a strategic partnership with Japan’s MUFG to bolster financial collaboration between India and Japan.

Santander teamed up with Visa to test agentic payments in markets in Latin America.

DriveWealthannounced a partnership with Latin American neobank Banco Ualá to help it launch a new stock investing service for customers in Mexico.

Jamaica Observers profiled financial wellness app Quatta which goes live this month.

Asia-Pacific

Mizuho Financial Group choseFIS’Balance Sheet Manager to help it navigate new regulatory reporting requirements in Japan.

Indonesia-based digital credit unicorn Kredivo acquired Vietnamese digital bank Timo.

Mastercardannounced a collaboration between its money movement platform, Mastercard Move, and Bank of Shanghai.

Sub-Saharan Africa

UK-based international credit information and risk management service provider Creditinfo announced its entry into the Uganda market.

African Islamic neobank Nyla partnered with Mambu as it goes live in Ghana and readies for West African expansion.

Nigerian fintech Thrifto launched a platform to help digitize traditional group savings scheme such as Ajo and Esusu,

Central and Eastern Europe

Commerzbank and Berlin, Germany’s Hawkannounced a collaboration to leverage AI to optimize internal banking processes such as fighting money laundering.

Berlin-based AAZZURforged a partnership with Estonian electronic money institution Wallester.

Romanian P2P lending platform Fagura secured investment from Bravva Angels, named “FinTech of the Year” at 2026 Romanian Startup Awards.

Have you been keeping up with the conversations on the Finovate Podcast?

Podcast host and Finovate VP Greg Palmer has interviewed an interesting range of guests in the first few months of 2026. From Best of Show winners to venture capitalists to fintech founders, Palmer’s podcast guests provide great insights into some of the most compelling innovations and the most important trends in our industry. Below are some of the conversations Greg has hosted so far this year.

Greg Palmer interviews FinovateEurope Best of Show winner Tweezr on updating legacy systems through LLMs and AI.

In this podcast conversation Greg Palmer sits down with Matt Ober, Managing Partner at Social Leverage, for a perspective on fintech investment trends in 2026.

Finovate podcast host Greg Palmer interviews Joel Blake, OBE, founder and CEO of GFA Exchange on the challenge and reward of democratizing access to finance.

Agentic AI infrastructure company Lyzr AI has raised $14.5 million in Series A+ funding. The round was led by Accenture and gives the company a valuation of $250 million.

This week’s investment follows Lyzr AI’s successful $8 million Series A round in October.

Headquartered in Jersey City, New Jersey, Lyzr AI made its Finovate debut at FinovateFall 2025 in New York.

Agentic AI infrastructure platform Lyzr AI has secured $14.5 million in a Series A+ round led by Accenture. The investment gives the Jersey City, New Jersey-based startup a valuation of $250 million, and comes less than a year after the company’s $8 million Series A round in October. In a statement on its LinkedIn page, Lyzr AI noted that the investment will help it further develop its “foundational technology platform to power the post-generative AI landscape.”

“Enterprise AI adoption is accelerating,” the company’s note continued. “But not the kind that lives in slide decks and conference rooms. The kind that passes 300-question technical audits. The kind that runs inside a customer’s own VPC. The kind that survives VAPT and red teaming before it ever touches production. That is the standard Lyzr was built for.”

Lyzr’s platform enables companies to build, design, and deploy AI agents that can complete tasks, interact with enterprise tools and data sources, and automate workflows including customer onboarding, loan servicing and origination, regulatory monitoring, claims processing, and more. With more than 100 production-ready AI agents available, Lyzr’s technology streamlines processes for banking, insurance, human resources, marketing, and sales, and is used by companies including AWS, Hitachi, NTT Data, and Nvidia.

“The true strength of Lyzr’s enterprise platform lies in the compounding value of our ecosystem,” the company wrote. “We have built an architecture designed to drive mutual growth and strategic alignment across the board, delivering measurable success for our customers, consulting partners, hyperscalers, and LLM providers alike.”

Founded in 2023, Lyzr made its Finovate debut at FinovateFall 2025 in New York. At the conference, the company demonstrated how its Lyzr Studio enables customers to build agents, knowledge graphs, responsible AI guardrails, and agent evaluation in a single location. The builder-focused platform offers businesses an open source framework with embedded Safe & Responsible AI guardrails.

Lyzr’s fundraising announcement comes just days after the company announced a strategic partnership with business AI transformation and enterprise integration firm Pronix Inc. The two companies will work together to help accelerate the adoption of agentic AI by businesses, combining Lyzr’s technology with Pronix’s expertise in digital transformation and modernization. Lyzr also recently announced that it is working with data infrastructure and agentic AI company GWC Data.AI, which joined Lyzr’s Partner Accelerator for Lyzr (PAL) program in late February.