This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Will the new month bring new challenges in fintech? Or will the news cycle take a much-needed vacation as summer approaches? Stay tuned to this week’s news for updates and evolutions throughout the week.

Pinnacle Bankpartners with CorServ to implement a modern credit card program for commercial, business, and consumer customers.

Insurtech

Scott Credit Union selectsBUNDLE by Insuritas to launch its insurance agency.

Investment and wealth management

Brokerage-as-a-Service innovator DriveWealthforges new partnership with Turkish fintech Papara.

Lending

PlaidunveilsConsumer Report, a new solution that brings businesses real-time cash flow data along with credit risk insights through Plaid Check, its consumer reporting agency.

Temenos has launched Responsible Generative AI Solutions for financial services.

The GenAI tools allow bank employees to use natural language to query the engine, which will leverage banks’ data to generate unique insights and reports.

At launch, the new GenAI tools will be available within Temenos Wealth and Temenos Digital products.

Banking technology provider TemenoslaunchedResponsible Generative AI Solutions for financial services this week. The Switzerland-based company is making the solutions available as part of its AI infused banking platform, starting with its Temenos Wealth and Temenos Digital products.

Temenos’ new offering aims to change the way banks leverage their data, and the company anticipates they will ultimately improve banks’ productivity and profitability. Temenos’ new Responsible Generative AI solutions work similarly to other GenAI engines, such as ChatGPT, in that they allow bank employees to use natural language to query the engine, which will leverage banks’ data to generate unique insights and reports. Banks can use the new tools in processes ranging from managing existing accounts to brainstorming new products and mitigating financial crime.

“We all use AI in our daily lives and benefit from the personalized services and insight,” said Temenos President Product and COO Prema Varadhan. “Temenos Explainable AI offers transparent, auditable insights while our Generative AI infused platform delivers these insights instantly in an intelligent and personalized way. Temenos ensures responsible AI practices by providing explainability, security, safe deployment, and banking-specific capabilities. With our AI platform, banks can rapidly implement real-world use cases that enhance efficiency, boost profitability, and create hyper-personalized customer experiences.”

The “responsible” part of Temenos’ new tools lies in its transparency and explainability. Users and regulators will have visibility into the process and will be able to verify the results produced by the engine. The Responsible Generative AI solutions also have a permissions and access security framework to address data security and privacy concerns.

Banks can deploy the newResponsible Generative AI Solutions as standalone solutions or connect them with their existing core systems on-premise, on public or private clouds, or delivered via Temenos SaaS.

Temenos was founded in 1993 and offers solutions for retail and commercial banking, wealth management, payments, fund administrators, insurance companies, and more. The company has clients in 150 countries and offers solutions that touch 30% of the world’s banking population, equivalent to 1.2 billion people.

A few days ago, we highlighted the $25.7 million (€24.1 million) investment secured by Danish challenger bank Lunar. Also this week, we noted partnership news from Denmark-based real estate tokenization platform – and FinovateSpring alum – DigiShares.

With all this Danish fintech news, we are devoting this week’s edition of Finovate Global to the fintech scene in Denmark: a Nordic country with a population of nearly six million and a per capita GDP that’s among the top ten in the world. We’ll also highlight some of the Danish fintechs that have demonstrated their innovations on the Finovate stage.

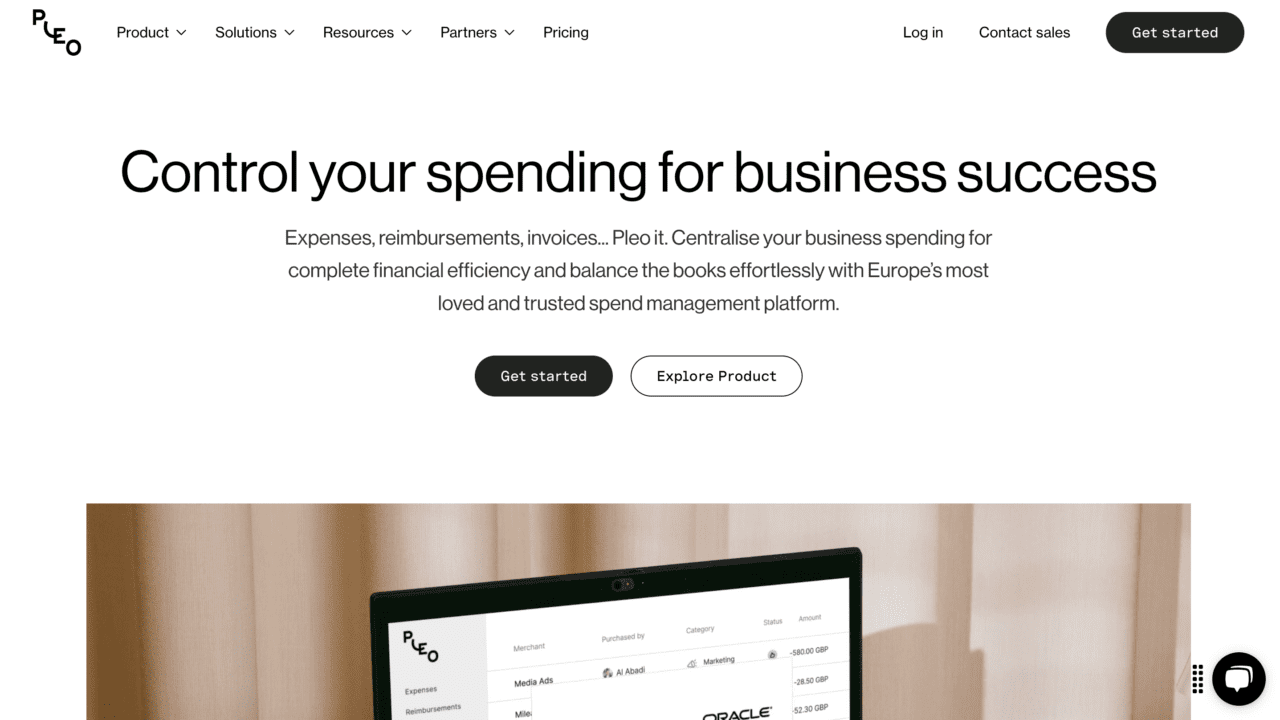

Danish fintech unicorn Pleo raises €40m in debt financing

Pleo enables companies to centralize their business spending – expenses, reimbursements, invoices, and more. Pleo also offers physical, temporary, virtual, and vendor company cards to help businesses better track and manage spending. Pleo integrates readily with common business tools such as NetSuite, Xero, and Quickbooks, making its solution a viable option for companies ranging from start-ups to enterprises. With more than 30,000 customers using its spend management platform, Pleo notes that its technology saves administrative teams 138 hours every year and has a satisfaction rate of 90%.

“We are delighted to announce our partnership with HSBC Innovation Banking. Starting at €40 million, the debt financing available to us can extend based on future requirements – which will expand our existing reach even further into more countries, enable us to increase limits and offer more currencies,” Pleo VP of Credit and Treasury Amit Kahana said. “Beyond this milestone partnership and imminent launch in the Netherlands, Pleo is expecting to see exciting developments over the coming 12 months as Pleo prepare(s) to launch in even more markets.”

Pleo initially earned its unicorn status in the summer of 2021, courtesy of a $150 million investment that drove the company’s valuation to $1.7 billion. Pleo secured an additional $200 million in funding in an extension of its Series C round in December of that year, giving the company a valuation of $4.7 billion.

Ageras raises €82m in oversubscribed private placement round

From its origins in 2012 as an online marketplace to help small businesses connect with financial professionals like accountants and bookkeepers, Denmark-based fintech Ageras has grown into a more comprehensive financial services provider, offering cloud-based accounting services to more than 300,000 small businesses in Europe.

“We want to make it easier to be a small business in an increasingly difficult administrative and regulatory landscape by offering a fully integrated platform where companies can manage their banking, accounting, and tax in one financial cockpit,” Anderson said.

The investment takes Ageras’ total equity capital to more than $231 million, according to Crunchbase. The funds will also support Ageras’ plans for new acquisitions, with Anderson admitting that there are a number of potential targets already under consideration.

Ageras operates in more than 100 countries and boasts more than a million users of its technology. Headquartered in Copenhagen, Denmark, Ageras was acquired by Investcorp, which took a minority stake in the company in 2017.

Here come Finovate’s Danish alums

Over the years, Finovate has been proud to showcase a large number of innovative fintechs from Northern Europe, including a handful from Denmark. Here are some of the Danish fintechs that have demoed their innovations on the Finovate stage.

Cardlay Payment Systems – FS24 – Cardlay Payment Systems will make its Finovate debut later this month at FinovateSpring in San Francisco. The company offers a white-label card and expense management solution, Cardlay Expense, that delivers an exceptional, real-time experience for cardholders.

Subaio – FEU22 – Subaio made its Finovate debut at FinovateEurope 2020 in Berlin, Germany, and returned to the Finovate stage two years later for FinovateEurope 2022 in London. The company helps financial companies generate new revenue streams by identifying recurring payments and insights, and delivering different use cases based on this data.

Aiia – FEU21 – Aiia demoed its technology at FinovateEurope 2021 in London. The leading open banking platform in Northern Europe, the company provides open banking services to a sizable number of financial instituitons including Lunar, Pleo, DNB, and Santander Consumer Bank. Aiia was acquired by Mastercard in 2021.

DigiShares – FS21 – DigiShares introduced itself to Finovate audiences at FinovateSpring 2021 in San Francisco. The company offers a white-label tokenization platform for real estate, bringing both automation and liquidity to the property market.

Here is our look at fintech innovation around the world.

Asia-Pacific

Vietnamese fintech startup M_Service, operator of mobile e-wallet Momo, secured $28 million (£ 19.7 million) in funding.

A new inclusive instant payment system (IIPS), Higala, launched in the Philippines.

Fintech Australia and the Thai Fintech Association signed a Memorandum of Understanding to foster fintech capabilities between the two countries.

Sub-Saharan Africa

The Central Bank of Nigeria paused account opening for new customers at four fintechs: Kuda Bank, Moniepoint, OPay, and Palmpay.

Digital financial solutions provider Payless Africa launched in Kenya.

FX and cross-border payments provider Crown Agents Bank teamed up with business platform Invest Africa.

Central and Eastern Europe

Norway-based digital identity solution provider Signicat became the first international aggregator to integrate mojeID Poland into its digital identity portfolio.

Romanian fintech Finqware teamed up with FwF to help European companies automate financial operations.

Lithuanian fintech Softloans raised $1 million (€1 million) in pre-seed funding.

Middle East and Northern Africa

National Bank of Iraq (NBI) went live with core banking and payments technology from Temenos.

Egypt’s Bokraraised $4.6 million in pre-seed funding for its platform that offers investment products via asset backed securities.

Central and Southern Asia

Bangladesh-based Eastern Bank (EBL) teamed up with Mastercard to launch a dual currency prepaid card for medical tourists in India.

Indian cross-border payments platform BriskPE secured $5 million in seed funding.

Bank of Thailand launched QR code cross-border payments to India.

Latin America and the Caribbean

Brazil-based banking-as-a-service company QI Tech became the country’s latest unicorn after securing an extension of its $200 million Series B round from last October.

Uruguyan cross-border payment platform dLocal partnered with online English-learning platform Open English.

Brazilian fintech Nubanklaunched its new banking experience Nubank+, offering cashback, streaming video courtesy of a partnership with Max, and more.

This week’s edition of Finovate Global features the latest fintech news from Germany, where investors are backing innovations in embedded finance, payments companies are taking advantage of open banking, and the green shoots of crypto spring are growing ever more apparent.

Solaris secures funding

Germany’s embedded finance platform Solarissecured $103 million (€96 million) in a Series F round this week. The investment was led by SBI, one of Solaris’ earliest investors, with other existing investors also participating. Solaris will use the additional capital, which takes the firm’s total funding to more than $486 million (€450 million), to onboard its ADAC (Allgemeiner Deutscher Automobil-Club) credit card program, strengthen its core capital, and invest further in its platform.

“This is a significant milestone for Solaris on our path to sustainable, profitable growth,” Solaris CEO Carsten Höltkemeyer said. “The funding underlines the high level of confidence our investors have in the transformation of our company.”

In addition to the investment, the Series F also included a financial guarantee of up to $108 million (€100 million) capital equivalent.

A pioneer in the banking-as-a-service business for nearly a decade, Solaris has grown into a major banking and technology provider with more than 750 employees at ten locations in both Europe and India. The company’s BaaS solution enables businesses to embed digital banking services – including payments, lending, and identity verification – directly into their platform. In addition to making it easier for companies to launch customized financial products and services, Solaris has secured the requisite licensing – including an e-money license for both the UK and EEA – to help companies navigate the regulatory complexities of doing business across the region.

Headquartered in Berlin, Solaris realized net revenues of $140 million (€130 million) in 2022. Last fall, the company issued a study – Disrupting the value chain for financial services – How to drive revenue growth with embedded finance – that highlighted “easier access to services” as a major driver of demand for embedded financial solutions.

Micropayment partners with Tink for Pay by Bank

Berlin-based payment processor Micropayment has turned to open banking platform Tink to add Pay by Bank to its payments offering. Live in Germany, Austria, and Switzerland, Micropayment’s Pay by Bank enables consumers to initiate payments directly from their bank account to the seller’s account when purchasing goods and services. A growing preference for both merchants and consumers, account-to-account (A2A) payments provide a secure and streamlined experience for customers and lower costs for merchants.

“The DACH region is a key market for us, and Tink’s dedication to serving merchants across various industries has been invaluable,” Micropayment CSO Thomas Knoth said. “Their payment method offers consumers the speed, reliability, and security they expect, making it a seamless experience for both merchants and consumers.” In a statement, Micropayment noted that it plans to take further advantage of Tink’s pan-Europe connectivity in the future.

Founded in 2005, Micropayment is a full-service payment provider that provides its customers with software implementation, payment processing, detailed analysis, and more. The company offers nine different payment options designed specifically for e-commerce and paid content services. Micropayment customers can integrate the technology via ready-made payment windows and preconfigured shop logins, as well as white-label APIs and interfaces.

“Collaboration with Micropayment has got off to an excellent start and we are gaining traction in a highly competitive landscape, by offering merchants a payment method that offers everything a consumer has come to expect – familiarity, speed, reliability, and convenience,” Tink DACH Payments Director Thomas Gmelch said.

A Finovate alum since its Best of Show winning debut in 2014 at FinovateEurope, Tink returned to the Finovate stage three years later to earn its second Best of Show award. Most recently, the Sweden-based company announced a partnership with German modern mobility sharing services provider Deutsche Bahn. The company will deploy Tink’s Account Check solution to enable instant, secure account onboarding.

Crypto spring is alive and well in Europe as the region’s most prominent digital bank, N26, announced that its first cryptocurrency product, N26 Crypto, will be available to its customers in France. N26 began the year with the unveiling of its new Stock and ETF trading product – and the bank’s crypto solution already has been available in seven of N26’s 24 European markets. This week’s announcement adds French traders and investors to the ranks of those N26 customers who will be able to transact in nearly 200 cryptocurrencies on the N26 app.

N26 Crypto will be available to all eligible customers in France, or at least with a French or a German IBAN. All membership tiers will be able to access the technology, including customers using free accounts. There will be no additional charge for using N26 Crypto, which the bank says will offer the broadest range of cryptocurrencies for trading and investing compared to all other European banking apps.

“Last summer, we installed our local French Iban to be able to accelerate the deployment of the global banking offer that we want to provide to our approximately 3 million customers in France,” N26 General Manager France & Benelux, Jérémie Rosselli explained. “With this, customers can go beyond managing their money simply and intuitively on their smartphone to also invest within the N26 ecosystem,” Rosselli said.

The new offering is made possible via a partnership with Bitpanda GmbH, which manages the execution of trades as well as the custody of coins. With only €1 to get started, N26 Crypto users pay 1.5% in fees on Bitcoin and 2.5% on other cryptocurrencies. Users can upgrade to N26 Metal to take advantage of reduced transaction fees, as well as other perks.

Founded in 2013 by Valentin Stalf and Maximilian Tayenthal, N26 has eight million customers and operates in 24 different markets. The bank’s crypto product announcement follows a slew of recent headlines from the German bank. These include the launch of its Instant Savings solution in 13 new markets, and the appointment of Mayur Kamat as new Chief Product Officer.

Here is our look at fintech innovation around the world.

Central and Eastern Europe

German challenger bank N26 launched new cryptocurrency trading product N26 Crypto.

Flowpay, a Czech-based fintech that provides financing for small businesses, raised $2.3 million (€2.1 million) in seed funding.

German embedded finance platform Solaris raised $103 million (€96 million) in a Series F round led by SBI Group.

Middle East and Northern Africa

Israel-based BioCatch and Google Cloud partner to bring fraud prevention solutions to expanding markets.

UAE-based Tungsten secured a license from the FSRA to operate at the Abu Dhabi Global Market (ADGM).

Bahrain’s Eazy Financial Services joined forces with Tabby to provide BNPL services via its EazyPay POS terminals network.

Central and Southern Asia

Business Recorder’s Syed Yousuf Raza looked at how Pakistan’s banking and fintech industry is dealing with evolving fraud threats.

The Indian government signed a $23 million loan agreement with the Asian Development Bank (ADB) to enhance access to fintech education, research, and innovation at the Gujarat International Finance Tec-City.

FinTech Alliance Nepal joined the Asia FinTech Alliance.

Latin America and the Caribbean

Colombian fintech Addi secured $86 million in a combination of equity and debt financing.

Uruguayan digital payments firm dLocal anticipates record total payment volumes in 2024.

Nubank Brazil CEO Livia Chanes talked with Bloomberg News about the state of fintech in Latin America.

Asia-Pacific

Singapore-based cross-border payments company Thunes expanded its strategic partnership with Visa.

Australia’s HeirWealth integrated with Envestnet | Yodlee to bring open banking data sharing to its wealth register for high net-worth families.

HSBC and the Hong Kong Science and Technology Parks startup hub announced the first “public-private cooperation between the city’s largest innovation and technology ecosystem and leading global bank.”

Sub-Saharan Africa

Ethiopia’s Cooperative Bank of Oromia partnered with Temenos to launch its CoopApp and CoopApp Aluhuda for both conventional and Islamic digital banking experiences.

dLocal teamed up with Ebury to bring African customers optimized payment solutions.

Safaricom, a telecom based in Kenya, partnered with Onafriq to offer remittance services to Ethiopia.

This week’s edition of Finovate Global takes a look at recent fintech developments and news from Sweden. Over the years, Finovate has been proud to showcase a number of fintechs from Sweden, a country with a population of more than 10.5 million and the twelfth largest economy as measured by GDP.

Last month at FinovateEurope, we introduced Swedish embedded banking and payments company Visualizy to our audiences. Founded in 2022, the company offers a multi-bank platform that helps businesses lower costs, reduce errors, and boost security in their financial and payment operations.

Other recent Finovate alums headquartered in Sweden include StockRepublic (FinovateEurope 2023), Econans (FinovateEurope 2021), Minna Technologies (FinovateEurope 2019), and Trustly (FinovateEurope 2013. This week’s Finovate Global will include news from two older Finovate alums hailing from Sweden: Tink – which won Best of Show in its Finovate debut at FinovateEurope 2014 – and Klarna, a Finovate alum since 2012.

Klarna rolls out open banking-powered settlements in the U.K.

Swedish payments network and shopping assistant Klarnahas begun to introduce open banking-powered settlements in the U.K. This means that consumers in the U.K will be able to pay Klarna directly from their bank account rather than a debit card. It also means that the company is making good on its objective of building a payments network outside the traditional card networks.

“Open banking offers a huge opportunity for Klarna to reduce the cost of payments to society by cutting out the established card payment networks, and using up-to-date bank account data to make ever better lending decisions,” Klarna VP, Open Banking, Wilko Klaassen said. “This new launch builds on the success we have seen in 10 countries across Europe and will give U.K. open banking a major boost.”

Ease of use is one major advantage open banking settlements provide consumers. For example, there is no need to enter personal payment details into the website of retailer that the consumer might not know very well. Instead, all a consumer needs to do is click on the “Pay by bank” option. This delivers the consumer to their mobile banking app where they can complete their transaction quickly and securely.

Launching the service in the U.K. is expected to be a major boon for Klarna; approximately five million U.K. consumers currently use open banking payment each month. Outside of the U.K., Klarna’s “Pay by bank” solution is currently live in 10 countries. More than 20 million consumers each month are taking advantage of the technology.

Tink adds to U.K. leadership team

Speaking of open banking, Swedish open banking platform Tink announced this week that it is bolstering its leadership ranks. The company – which won Best of Show in its Finovate debut at FinovateEurope in 2014 – has appointed Ian Morrin as Head of Payments & Platforms, Andrew Boyajian as Head of Products for Payments & CX, and Jack Spiers as Banking and Lending Director.

Of the three new hires, Jack Spiers may ring a bell with Finovate audiences. Spiers was a recent speaker at FinovateEurope, where he provided a Special Address on “Transforming Lending in the Cost of Living Crisis.” In his presentation, Spiers – whose ten years of fintech experience include tenures at both Klarna and Clearpay – discussed how traditional methods are falling short in their ability to accurately assess creditworthiness. Instead, he pointed to new research from Tink that showed how data-enriched affordability checks can do better.

The new hires come just days after Tink announced a partnership with German railway company Deutsche Bahn. Via the new agreement, Tink will offer Deutsche Bahn customers optimized direct debit setups. This will enable customers to use Deutsche Bahn’s modern mobility-sharing systems, which are run by Deutsche Bahn subsidiary DB Connect. The railway company will also leverage Tink’s Account Check technology for its car-sharing and bike-sharing networks, Flinkster and Call a Bike.

Founded in 2012 and headquartered in Stockholm, Sweden, Tink most recently demoed its technology at FinovateEurope 2019. A two-time Finovate Best of Show winner, Tink was acquired by Visa in 2022 for $2 billion.

Swedish Central Bank looks to defend cash

If the Swedish Central Bank is for cash, then who can be against it?

That’s one of the questions the nation’s central bank is asking in the wake of 2023 survey that indicated that half of the survey’s respondents had run into circumstances in which they wanted to pay with cash, but merchant would not accept it. According to a report issued by Sweden’s Riksbank that is based on those results, this number was only 37% a year ago.

The report indicates that the supply of cash services in Sweden is decreasing and has been since at least 2016. Cash services refer to those locations for cash withdrawals, deposits of daily takings, as well as over-the-counter payments. This decline has slowed somewhat in the past five years, as new regulations have insisted that banks share the responsibility of providing cash services with other non-bank institutions. But the downward trend is clear.

“Payments must work for everyone, Riksbank governor and chairman of the executive board Erik Thedéen said in a press release. “In the longer term, all payments may be digital – but until then, cash plays an important role. We need legislation to ensure that cash can be used to pay. Banks must also ensure that more customers have access to payment accounts.”

To this end, in addition to calling for further research and study, the Swedish central bank proposed, for example, that banks should ensure that cash can be transferred to and from retail outlets at reasonable prices. At present, only one private company does this. Another proposal suggests that banks be obligated to accept banknote and coin deposits from private individuals. As noted above, there is not a current requirement for banks to do so.

These changes, along with others to help more individuals secure payment accounts, are likely to help Sweden increase financial inclusion as the country continues the rapid digitalization of its payment market. There will be no retreat from this drive for “faster, smoother, and more efficient payments.” But ensuring the availability and utility of cash, at least in the meantime, will both support that transition as well as ensure fewer Swedes are left behind on the way.

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

U.K.-based fintech Unlimit secured a license from the Bank of Tanzania to do operate as a payments service provider (PSP) in the country.

African fintech PalmPay launched a pair of new products in Nigeria: Unlimited Free Transfer and Target Savings.

Mastercard and South African fintech SAVA teamed up to bring innovative payment options – including digital bank accounts and accounting integration tools – to small, medium, and micro enterprises (SMMEs).

Central and Eastern Europe

Berlin, Germany-based brokerage-as-a-service platform lemon.markets launched this week in partnership with Deutsche Bank, BNP Paribas, and Tradegate.

The Hungarian Ministry of the Economy has suggested new rules to codify the use of digital assets in the country.

German fintech Naro emerged from stealth this week with $3 million in pre-seed funding.

Middle East and Northern Africa

Israel-based fintech Nayaz shared its plans for expansion in Latin America following its acquisition of Brazil’s VMtecnologia.

Dunes Financial, headquartered in the UAE, agreed to acquire the technology assets of Be Mobile Africa.

The Financial Brand profiled former Bank Leumi CEO Rakefet Russak-Aminoach.

Central and Southern Asia

India’s UPI linked with Nepal’s largest payment network, Fonepay.

Writing in IBA.org, Sahar Iqbal assessed the current fintech landscape of Pakistan.

Courtesy of a partnership with Mastercard, India’s IndusInd Bank will launch an tokenizable wearable solution called Indus PayWear.

Latin America and the Caribbean

Aquis Technologies secured a contract to support the operation of the Central Bank of Colombia, Banco de la República.

Mexican challenger bank Fondeadora turned to MeaWallet for tokenization services.

Banco do Brasil teamed up with Giesecke+Devrient (G+D) to test offline payments for its CBDC project.

Asia-Pacific

Bank Muamalat Malaysia Berhad (Bank Muamalat) forged a multi-year collaboration with Google Cloud en route to its transformation into a digital Islamic bank.

Philippines-based Metropolitan Bank & Trust (Metrobank) partnered with Temenos to enhance its wealth management offerings.

Australian regulators are looking to regulate Buy Now Pay Later products under the nation’s Credit Act.

The week begins with big news on the payment cards front as Capital One announces plans to acquireDiscover Financial Services in an all-stock deal valued at $35 billion. Check out what else is going on in fintech and financial services in our latest fintech weekly news rundown!

Embedded finance

German embedded finance platform Moniteraises $6.5 million (€6 million) in funding.

Quaint Oak Bank selectsFinzly to modernize payments and enable its embedded banking practice.

Gorham Savings Bank partners with CorServ to implement modern commercial credit card program.

REPAYenhances accounts payable integration for Sage Intacct.

REPAYpartners with Maxyfi to modernize the collection of payments.

FXC Intelligence signs a data and intelligence partnership with dLocal to support its expansion into the remittance segment of the cross-border payments industry.

Nigerian digital bank FairMoneyis considering acquiringUmba, digital bank with operations in Nigeria and Kenya, in an all stock deal valued at $20 million.

Crypto

Revolut announces plans to open an advanced cryptocurrency exchange.

RockWallet to onboard former Wyre users after acquisition of its customer base.

Velexaintroduces Fractional Bonds, democratizing investment in high-quality bonds.

TIFINreceives $10 million from SEI to power the future of wealth through artificial intelligence.

Open banking

Data intelligence platform Bud Financial is partnering with open banking company Fintech Galaxy to strengthen the open banking scene in the MENA region.

Insurtech

Insurtech Myloselected by 1-800Accountant as digital insurance partner.

FinovateEurope 2024 will have its fair share of local talent demoing live on the Finovate stage on 27 February in London. And while we’re looking forward to the return of FinovateEurope 2023 Best of Show winner NayaOne, we’re also excited to meet a whole bunch of U.K.-based fintechs that are making their Finovate debuts:

FinovateEurope 2024 will also feature one of our most geographically diverse lineups to date. Companies from 15 different countries plus the U.K. will be on hand in just a few weeks to demo their latest fintech innovations at our annual European fintech conference.

See for yourself! Here’s a look at the range of countries our demoing companies are coming from:

This week’s Fintech Rundown features partnership and expansion news from a handful of Finovate alums, as well as some interesting fundings in the cryptocurrency and charitable giving space.

This week in Finovate Global we take a look at some recent fintech developments in Mexico.

First up is news that Grupo Financiero Banorte has launched Mexico’s first fully digital bank, bineo. The company noted that it hopes to add 2.8 million new customers in the next five years.

“The launch of bineo is a great milestone in the history of Grupo Financiero Banorte that will allow us to meet all needs: those who prefer a human-digital combination and those who seek 100% digital banking, with the financial security that has always characterized the institution,” Grupo Financiero Banorte chairman Carlos Hank Gonzalez said.

Bimeo offers a pair of accounts for customers. The bimeo Total Account allows for unlimited deposits. The Light Account has a monthly cap of 3,000 UDIS (investment units), which equals approximately 24,000 Mexican pesos.

Account holders will have access to both a digital and a physical debit card that includes a feature that enables them to allocate their savings toward specific goals. Card holders can use their physical card at more than 10,000 Banorte ATMs. Additionally, in a nod to sustainability, the physical card consists of biodegradable materials.

The new digital bank also offers financing products for bineo account holders. Customers will be able to apply for digital loans in amounts ranging from 5,000 to 200,000 MXN. Repayment terms range from six to 24 months. The bank also pledges competitive rates and instant access to funds once loans are approved.

“We imagine a bank that puts people at the centre, and we created it!” bineo CEO Victor Moya said. “We think in a different way of managing finances, where personalization is the heart of what we do. Bineo will offer new products and services based on customer needs so as not to confine them to a product designed by us.”

Pago en Quincenas with Kueski Pay is the name of the new payment option. It enables payment for purchases in biweekly installments, helping make shopping on Amazon more affordable to many Mexican consumers. The option also helps deal with the fact that less than a third of the adult population in Mexico has a credit card. By leveraging Kueski Pay, one of Mexico’s most popular buy now, pay later platforms, Amazon Mexico helps expand purchase financing beyond both credit as well as debit cards.

“Our agreement with Amazon demonstrates the need Mexicans have for more flexible , secure, and inclusive payment alternatives,” Kueski Pay SVP of Sales Lisset May said. “Kueski Pay enables merchants to deliver more innovative shopping experiences and help Mexican consumers live their personal finances with more excitement.”

Kueski Pay has provided nearly 15 million loans to date. The company notes that 1 in 4 of Mexico’s most relevant merchants offer the payment option. Customers who opt for Pago en Quincenas with Kueski Pay can choose from plans of up to four interest-free biweekly payments as part of an introductory offer, or as many as 12 biweekly payments. Payments can be made by linked bank account, debit card, or cash at participating networks. A one-time application must be completed during the Amazon checkout process the first time a customer chooses the Kueski Pay option.

Finovate has been happy to host a handful of fintechs from Mexico over the years. Some of our Mexico-based alums include:

Nufi

Founded in 2020 and headquartered in Monterrey, Nuevo Leon, Mexico, Nufi made its Finovate debut at FinovateFall 2021 in New York. The company demoed its Fintech Legos offering, a set of modular building blocks that enable firms to build their own financial solutions. At the conference, Nufi showed how its Fintech Legos could be used to build a modular, adaptable KYC process that could be deployed by any company.

Sr. Pago

Mexico City-based fintech Sr. Pago was founded in 2010 and made its Finovate debut at FinovateFall 2014. At the conference, the company’s CEO and co-founder Pablo Gonzalez Vargas demoed the Sr. Pago Card + Reader, which help small businesses and individuals accept card payments for services and have those payments loaded onto the recipient’s Mastercard. The company was acquired by Mexico-based online lending platform Konfío in 2021.

Prestadero

Also headquartered in Mexico City, Prestadero made its Finovate debut in 2013 at FinovateSpring. Founded in 2011, Prestadero was the first fully legally compliant and operational P2P lending platform in Mexico. At FinovateSpring, the company demonstrated how its proprietary management software enabled Prestadero to parse out declined loans in seconds and offer rates for approved loans in less than a minute.

Kuspit

Founded in 2010 and based in Mexico City, Kuspit is a regulated broker/dealer in Mexico. The company targets retail investors with little investing experience and offers an investing community in which learning, sharing, and investing “dynamically integrate with one another.” Making its Finovate debut in 2012 at FinovateSpring, the company showed how it uses visualization to help investors understand the relationship between risk and return.

Here is our look at fintech innovation around the world.

Central and Southern Asia

Regulators in India ordered digital payments provider Paytm to cease much of its business operations due to non-compliance issues.

Mastercard and SadaPay extended their partnership to support the financial needs of SMEs and freelancers in Pakistan.

Indian private sector bank Karnataka Bank teamed up with financial services platform Northern Arc Capital.

U.S. President Joe Biden and Chinese President Xi Jinping are meeting in California this week. With that in mind, Finovate Global turns to China for the latest fintech news from the world’s second most populous country.

For context, the People’s Bank of China (PBOC) released its Fintech Development Plan for 2022-2025 almost two years ago. In its analysis of the PBOC’s Plan, China Briefing noted that the country had “much to gain” from innovation in fintech and financial services. In large part this was because of China’s “insufficient supply of inclusive finance, especially in rural areas.” The country reached a consumer fintech adoption rate of 87% in 2019. And, again, further fintech adoption in rural areas could cause this rate to quickly climb even higher.

What obstacles confront China’s fintech sector? China Briefing suggests that “unbalanced application of intelligent technology” is among the issues to be resolved – or at least better managed. The report references the so-called “Matthew Effect” in which stronger positions become stronger and weaker positions become weaker to describe the one of China’s bigger challenges when it comes to innovation in financial services.

Read the report from China Briefing to learn more about how China plans to “leapfrog improvement of the fintech sector”.

China’s JD.com launched its enhanced authentication solution for imported goods in the region, JD Smart Check. The new process is part of the company’s cross-border e-commerce platform, JD Worldwide.

JD Smart Check has three main focuses: improving quality inspections for cosmetic products, leveraging blockchain technology to enhance anti-counterfeiting activity, and providing on-demand authenticity inspections for products shipped by direct mail. New X-ray fluorescence analysis to provides fast, on-site assessment of cosmetics and personal care products at JD’s logistic centers. With regards to anti-counterfeiting efforts, the company leverages serialized tracking codes, supply chain monitoring, and product inspection videos to ensure accurate scrutiny of inventories. Lastly, JD Worldwide will be able to better serve direct mail shoppers by adding reports from authoritative centers to its product inspection services.

China’s largest retailer by revenue, JD.com serves nearly 600 million customers. The company operates the largest fulfillment infrastructure for any Chinese e-commerce firm.

Ant Group has forged a partnership with Payments Network Malaysia (PayNet). The partnership will enable travelers from eight nations – representing eight different supported digital wallets – to use PayNet’s DuitNow QR in Malaysia.

The DuitNow QR network consists of more than 1.8 million merchant touchpoints throughout Malaysia. The eight supported wallets are Alipay (China), AlipayHK (Hong Kong SAR), HelloMoney by AUB (Philippines), Hipay (Mongolia), MPay (Macau SAR), Naver Pay (Japan), Toss Pay (South Korea) and True Money (Thailand). Group CEO of PayNet Farhan Ahmad said that the cross-border digital payments collaboration with Ant Group signified “a new Silk Road emerging” that will be “powered by cross-border payment functionality.”

The Ant Group/PayNet partnership comes as a recent report commissioned by Alipay indicates that increases in average consumer spending over the past few years will help accelerate intra-Asia cross-border travel and payments. The companies noted that the partnership extends “beyond connectivity” to include joint marketing efforts that will boost merchant and brand visibility in digital wallets.

Here is our look at fintech innovation around the world.

Philippines-based digital bank Tonik has entered the insurance business. The neobank announced a new strategic partnership this week with life insurance company Sun Life Grepa Financial, Inc. (Sun Life Grepa).

The partnership will enable Tonik to offer its customers Payhinga, a credit life and disability insurance product. Payhinga gives policyholders access to life and disability insurance with coverage of up to 120% of the loan amount. Further, policyholders can use a two-month payment holiday to reschedule upcoming loan payments in the event of financial difficulty.

“The partnership with Sun Life Grepa will significantly expand our suite of products, and insurance is a highly sought-after addition our customers have been requesting,” Tonik Country President Long Pineda said.

The Philippines’ first, digital-only neobank, Tonik offers loan, deposit, and payment products to consumers via its digital banking platform. The bank teamed up with FC Home Center, launching its Shop Installment Loan with the retailer in August. In June, Tonik announced that it had reached the one million customer milestone. Greg Krasnov (CEO) founded Tonik in 2020.

Speaking of digital banks based in the Philippines, UNO Digital Bank is teaming up with Collabera Digital. A digital engineering services provider, Collabera Digital will help the bank develop and integrate a mini app within superapp GCash.

Collabera Digital provided the strategy to address key issues such as AML and KYC, and built an integrated API platform. The leading superapp in the Philippines, GCash provides a wide range of financial services including money transfer, billpay, savings, investments, insurance, lending, and more. UNO Digital Bank’s integration into GCash will boost access to financial services to individuals across the socio-economic spectrum. The integration also supports the growth of the digital economy via services like mobile banking and digital wallets.

“Our partnership with GCash is significant in scaling and increasing our customer reach,” founder and CEO of UNO Digital Bank Manish Bhai said. “As a greenfield bank, built independently of a larger traditional institution, we have to be innovative in identifying opportunities to grow and expand. GCash, with their 90+ million users and active thrust towards financial inclusion, is a great partner leading to a win-win proposition for both the entities.”

UNO Digital Bank was founded in 2021 and is headquartered in Taguig, a city in the Manila metropolitan area. The institution had total assets of $29 million (PHP 1.78 billion) as of end of year 2022.

What are fintechs in the Philippines doing for small businesses? Merchant fintech platform yufinannounced a series of partnerships this week designed to bring new services to Philippines-based merchants. The new additions to yufin’s partnership ecosystem include wholesaler Lots for Less, delivery firm Transportify, and streaming content company Vivamax.

Shubhrendu Khoche, President and co-founder of yufin Philippines, noted that the new partnerships will drive greater digital adoption by businesses throughout the value chain. “As the financial growth engine for small merchants, these new partnerships will create more reasons for digital payment for our small merchants, their shoppers, and suppliers,” Khoche explained.

Founded in 2021, yufin aims to raise the income of 10 million households at least by 50% in the next five years. The company’s partnership ecosystem helps turn small, corner shops into preferred banking and credit hubs for their customers. With a goal of partnering rather than competing with local banks, yufin offers assisted digital financial services that enable underserved communities to leverage technology to improve financial outcomes.

Here is our look at fintech innovation around the world.

Sub-Saharan Africa

South Africa’s Lipa Payments secured full SDK certification for Tap to Phone from both Visa and Mastercard.

Kenyan fintech and mobility solutions company Data Integrated won approval to operate as a Payment Service Provider from the country’s central bank.

Stitch, a business payments company based in South Africa, raised $25 million in Series A funding.

Central and Eastern Europe

German B2B Buy Now Pay Later payments provider Mondu registered with the Financial Conduct Authority (FCA).

Polish fintech Verestro integrated the Quicko Wallet money transfer service within the Slack application.

Cloover, a climate-based fintech based in Germany, raised €7 million in pre-seed funding.

Middle East and Northern Africa

ACI Worldwideforged a partnership with MENA-based payments and BaaS enabler NymCard.

Temenos unveiled a new solution, based on Generative AI, that automatically classifies customers’ banking transactions.

The new offering will help banks offer more personalized insights and recommendations to their customers.

Temenos’ Generative AI solution is part of the company’s strategic AI roadmap. Other use cases for the technology include chatbots and guiding customer journeys.

How will financial services companies take advantage of Generative AI? One way, courtesy of a new solution from Temenos, will be to leverage the technology to automatically classify customers’ banking transactions. This functionality will make it easier for banks to offer personalized insights and recommendations to their customers.

While traditional AI and machine learning technologies have been deployed by financial services firms in a variety of contexts, generative AI and Large Language Models (LLMs) offer these companies the ability to enhance both operations and customer experiences even further. This is due to the fact that Generative AI and LLMs outperform traditional AI and machine learning approaches when it comes to understanding language, images, sound, video, and code – and then leveraging these inputs into a variety of solutions for customers.

Temenos’s new Generative AI-based offering enables banks to automatically classify and label customer transactions. The technology has a high degree of accuracy and operates in multiple languages. The automatic customer transaction capability has a number of use cases including cashflow prediction, customer attrition analysis, next best product, and more.

“We have continually invested in embedding Explainable AI and ML capabilities into our banking platform and making available all products through an easy-to-use interface or APIs,” Temenos President of Product and COO Prema Varadhan said. Varadhan referred to the new offering as part of the company’s strategic AI roadmap and underscored the value of transparency and explainability when it comes to deploying AI.

Temenos has deployed explainable AI in a wide variety of use cases ranging from wealth management, AML, credit scoring, smart money management, collection optimization, and more. However, transaction classification is the first instance of leveraging Generative AI in a Temenos product. The company said in a statement that it plans to extend the technology to chatbots and customer interfaces, as well as in guiding customer journeys and responding to customer queries.

A Finovate alum since 2013, Temenos was founded in 1993 and is headquartered in Geneva, Switzerland. The company serves 3,000 customers and its open platform enables more than 1.2 billion individuals to conduct their daily banking activities. Two-thirds of the top 1,000 banks in the world and more than 70 challenger banks in 150+ countries use Temenos’ technology. Max Chuard is CEO.