Boku

CNNMoney examined Zong’s competition with Boku. Link

BrightScope

Clairmail

Clairmail increased its security by using authentication from the RSA Secured Partner Program. Link

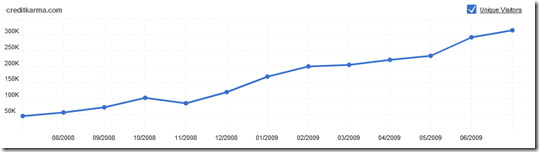

Credit Karma

The Forbes blog recommended Credit Karma as a tool to track and monitor your credit score. Link

Credit Sesame

![]()

The Forbes blog recommended Credit Sesame as a tool to track and monitor your credit score. Link

Dwolla

Dwolla updated its iPhone app to allow customers to send money via email. Link

Dynamics

American Banker discussed Dynamics’ adaptability to the mobile payment world. Link

Enloop

Small Biz Technology outlined three of Enloop’s features. Link

eToro

AlphaTrade Finance discussed eToro’s CopyTrader network. Link

Expensify

Expensify’s app was listed as Gearburn’s App of the Week. Link

Finsphere

![]()

GeekWire reviewed Finsphere’s new round of $1.75 million funding. Link

Geezeo

American Banker reported that Geezeo’s partnership with Sharetec Systems will help Geezeo reach more credit unions. Link

Guardian Analytics

The Street reported that Guardian Analytics’ Anomaly Detection & Fraud Monitoring will help financial institutions meet updated FFIEC guidelines. Link

Kony Solutions

Kony Solutions announced a partnership with Donriver for the delivery of multi-channel mobile apps. Link

Mint.com

The Quickbooks blog examined Mint.com’s PFM tool. Link

Monitise Americas

![]()

Monitise developed two banking apps designed for the iPad for NatWest and RBS. Link

PayNearMe

The Paypers interviewed Avangate and PayNearMe regarding their partnership and various future endeavors. Link

PayPal

TechCrunch speculated that eBay’s acquisition of Zong will advance PayPal’s mobile payments. Link

ProfitStars

Credit Union Times discussed ProfitStars’ partnership with Corporate One Credit Union. Link

Prosper

The Social Lending Network reviewed Prosper’s new Quick Invest feature. Link

Q2ebanking

Q2ebanking commented on the security implications of the new FFIEC guidelines. Link

RobotDough

The Motley Fool highlighted RobotDough as a powerful new tool for individual investors. Link

SilverTail Systems

ThreatMetrix

ThreatMetrix enhanced its security in anticipation of FFIEC guidelines. Link

TradeKing

Stockbrokers4u.com analyzed TradeKing’s services. Link

Xero

Xero hired a CFO onto to its team. Link

Yodlee

")

![clip_image004[4]](http://www.netbanker.com/WindowsLiveWriter/CreditKarmaProvidesFreeCreditScorestoSea_118F7/clip_image004%5B4%5D.jpg)