I’ve complained about similar offers before, but since this arrived in my inbox this morning, I figured it’s time to revisit the issue.

———

Today’s lesson is about third-party offers, where an outside company pays to get in front of your customer base. They are relatively rare in financial services these days because banks and card issuers are wary of being tarred and feathered in social media (or the CFPB) if something goes wrong or the particular marketing permissions were later shown to be lacking.

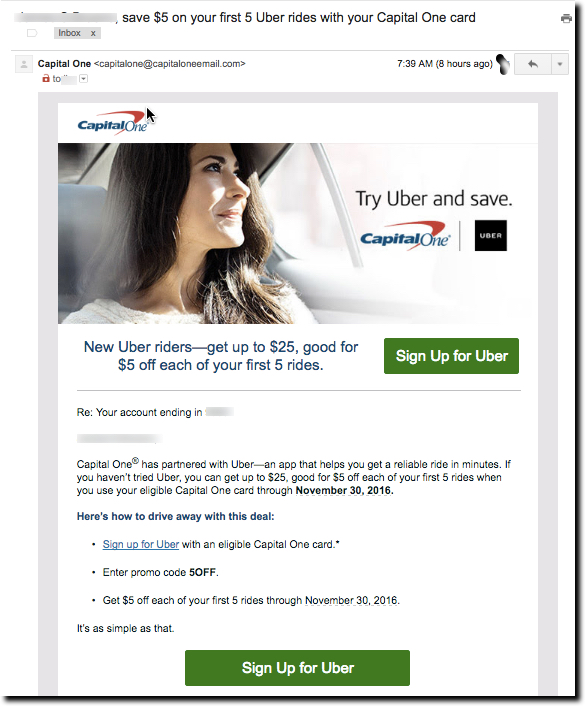

The offer in question is from Uber. It’s good for $5 off your first 5 rides and requires a Capital One card for payment. That’s a win-win. Uber gets a new customer and Capital One gets its card loaded into the Uber app for years to come.

The problem: It’s only for new Uber customers. I presume Capital One removes cardholders from the mailing who have charged an Uber to its card. But that doesn’t catch people who use another card in their Uber account.

So let’s break down what happens next. Capital One customers get this slick email (see above). They get excited to switch Uber payments over to their Capital One card to grab some $5-off rides. But then, after reading the fine print, or more likely clicking through the message and trying to sign up, cardholders find out they get zip from this deal. Now, they are not happy with Capital One or Uber. What a waste of time and brand loyalty.

Instead, why not give some smaller benefit to existing Uber customers willing to switch their payment card over to Capital One? Even just one $5 off coupon would suffice for most.

Bottom line: Capital One needs to earmark a portion of its commissions from Uber towards existing customers. If there isn’t enough revenue to do that, then it should stop making the offer.

——-

Related: At last m onth’s Finovate Fall, MX demo’d, and won Best of Show, for an automated solution called Power Switch to automatically enroll your customers’ cards into e-commerce sites such as Uber, Amazon, iTunes, and so on. Get a behind-the-scenes look at how MX produces its award-winning (six consecutive Best of Shows) at FinDEVr in Santa Clara 18/19 Oct 2016 (register here).

onth’s Finovate Fall, MX demo’d, and won Best of Show, for an automated solution called Power Switch to automatically enroll your customers’ cards into e-commerce sites such as Uber, Amazon, iTunes, and so on. Get a behind-the-scenes look at how MX produces its award-winning (six consecutive Best of Shows) at FinDEVr in Santa Clara 18/19 Oct 2016 (register here).

Here at Netbanker/OBR, we love to write about the digital future. But we know it’s even more important to address the digital now. If you don’t leverage current technology to your advantage, the future doesn’t much matter, since someone else will be running your business.

Here at Netbanker/OBR, we love to write about the digital future. But we know it’s even more important to address the digital now. If you don’t leverage current technology to your advantage, the future doesn’t much matter, since someone else will be running your business.

")