This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Brokerage infrastructure API provider DriveWealthbrought in $56.7 million in Series C funding today. The investment is more than double the Series B round of $21 million the company received in 2018. Today’s investment brings the company’s total to $100.8 million.

The round saw participation from existing investors Point72 Ventures– which led the round– as well as Raptor Group, SBI Holdings, and Route 66 Ventures. New investors Mouro Capital and Fidelity International Strategic Ventures also participated.

DriveWealth will use the funds to strengthen its technology, make strategic acquisitions, and grow the organization to scale its business.

The New York-based company offers a suite of APIs that allows its partners to embed investment experiences of U.S. securities within their own apps. Among DriveWealth’s products are tools for advisors, fractional share investing, and purchase round-up investment capabilities.

“DriveWealth saw its partners open more accounts in 2Q than E*Trade, Schwab and TD Ameritrade combined, and 3Q saw a 33% increase over 2Q,” said DriveWealth Founder and CEO Bob Cortright. “This type of activity speaks to the power of making it simple for consumers to start investing immediately. The new funding from our great investors will only help us improve our technology capabilities to democratize investing.”

Since it was founded in 2012, DriveWealth has already scaled its business to serve a range of geographies and now reaches investors in 153 countries. The company has formed partnerships with firms on six continents, including Asia, where it collaborated with Singapore-based Bambu on the launch of a white-label roboadvisory platform for U.S. wealth managers; and Africa, where the company teamed up with Sigma Securities and Trove Technologies to launch a digital U.S. equities trading product for retail investors in Nigeria.

Among DriveWealth’s clients are Hatch, Revolut, Stake, and Moneylion. The company recently partnered with Access Softek to help community banks and credit unions offer their members access to investing tools.

What is the impact of financial technology on what some might suggest is the most important “vertical” of all? With churches and other religious institutions joining other organizations in their embrace of technology, we wanted to take a look at how trends toward digitization – especially given the onset of the global health crisis – are impacting the way that faith institutions support and engage with their communities and congregations.

To learn more, we connected with Aaron Senneff, Chief Technology Officer with Pushpay. Founded in 2011 and headquartered in Redmond, Washington, Pushpay offers engagement and mobile commerce solutions, including payment solutions, to faith, non-profit, and educational organizations.

Finovate: With more than 10,500 customers and a total processing volume of $5 billion, Pushpay operates in a fascinating space within fintech: providing donor management and engagement solutions for faith communities. Can you tell us a little about the idea behind launching the company and the problem Pushpay solves for its customers?

Aaron Senneff: Pushpay was formed on the idea that church giving should be easier. When the company was founded, e-commerce through mobile devices and app was accelerating. You could order and pay for your coffee through the phone.

At the same time, churches were accepting donations via cash, check, and passing offering plates as they had done for years. Our founders saw an opportunity to use technology to help make giving easier for church members and make it much easier for church staff to track, manage, and encourage generosity through digital tools.

Today, Pushpay’s digital systems have built on the early success of digital giving, and expanded into donor development, custom mobile applications for churches and church management systems – a full complement of tools that aid churches. As our original founder was known to say, “Everything we do is driven by our purpose to bring people together by strengthening community, connection, and belonging.”

Finovate: How widely are services such as Pushpay used by churches and other religious institutions in the U.S.? Is this a rapidly growing opportunity for you?

Senneff: Many large, progressive churches use technology to their advantage today. It’s not uncommon for a church to use a wide variety of digital tools now, from streaming technology, to email marketing or CRM tools, to sophisticated custom websites. Many of those churches have added digital giving to their arsenal of tools, especially in the last five years. Particularly, large U.S. protestant churches – the so-called “mega-churches” – have significantly embraced the concept of digital giving.

The adoption of digital giving follows the adoption curve you might expect from other technologies. There are early adopters, early majority, late majority and laggards – churches span across all of these categories. While we’ve seen a lot of adoption in churches to date, we still see a number of churches and faith-based organizations using antiquated tools and processes to manage their giving. In addition, among our current customer base, the suite of tools is ever maturing, growing, and becoming more capable. There’s a great deal of opportunity to utilize those new capabilities, even for churches who adopted digital giving tools early.

Finovate: Who are Pushpay’s primary customers? Is this something that churches of varying congregation sizes can use – or is it mostly for larger institutions? Is there much geographic variation in terms of who uses Pushpay’s solutions?

Senneff: Pushpay serves churches of all types in the U.S. We have customers that rage from 20,000 in weekly attendance to less than 100, and every type of church in between. We have found that larger, progressive churches – the kinds of churches that might operate multiple campuses, have staff dedicated to digital technology, that have processes, systems and structures in place that support their complex and growing organizations – are often the first to adopt new technology and digital tools like Pushpay. However, we see very active interest in our tools across the spectrum of churches.

We’ve also seen an acceleration of adoption across the market as a result of COVID, as churches across the U.S. closed their doors, but still needed a way to engage their membership. The digital tools we provide can give churches a means to continue to communicate and engage with their membership, even while physical participation is on pause.

Finovate: You recently launched ChurchStaq, an end-to-end engagement solutions platform that includes a church management system. I think our readers would be especially interested to hear about the giving and donor management functionalities of the platform. Can you talk a little about this?

Senneff: ChurchStaq is a full suite of tools that enables churches to engage with their people on all levels. It includes a Church Management System – a back office system not unlike a CRM but customized for church staff – a customized mobile app that a church can deploy to their community, and a digital giving platform. These three core capabilities are combined into one product offer that work together to help churches know, grow and keep their people.

The strength of this platform isn’t the standalone donor management system or app or ChMS, but the combination of them all. A really good example of this is our suite of donor development tools. In addition to facilitating online giving, donor management system has some sophisticated reporting that allows church staff to easily identify changes in giving patterns among their community. A church might, for example, have a family that is experiencing financial distress as a result of a job loss and that is surfacing in their giving stopping or becoming more erratic.

The donor management system can easily identify those people who may be in need of care. From that point, the ChMS system can take those individuals and put them in automated workflows for the church that kick off a process of care that is designed by the church. Whether it’s assigning a staff member to call them and check in, sending them an encouraging email, or texting them with some resources, etc. They can also use the church app to push out content or push notifications to specific groups of people. The tools really work powerfully together to help churches big and small care for their people individually.

Finovate: How has COVID-19 impacted your customers? Have you seen the same eagerness to embrace new technologies as we’ve seen in among other institutions and organizations? Has Pushpay played a role in helping its customers manage the crisis?

Senneff: COVID has had a mammoth impact on U.S. churches. Many churches across the nation have been closed to physical attendance since early March. Even as they begin to re-open, we see hybrid models that combine in person and online attendance, and many church-goers and families continue to participate on-line. Digital tools like Pushpay’s have been vital for some churches. It’s allowed those who may have historically relied on physical engagements to connect with people – like written Connection Cards, booths in the lobby, new attendees meeting or classes – to replace those physical engagements with digital ones, such as invitations to give, to join groups, to interact with staff or see the churches calendar of events from a mobile app.

Many churches who were already investing in online tools actually saw attendance via viewership rise during COVID over their historic physical attendance, and the digital tools that Pushpay provides can help churches better engage with those individuals.

Finovate: What can we expect from Pushpay over the balance of 2020 and into next year?

Senneff: We continue to invest significantly in our entire product family: our digital giving platform, our church management systems, and our custom mobile apps. We’ll continue to move each of these products’ features and capabilities forward individually, but we have a significant emphasis this year and beyond on providing a seamless, full-suite solution where churches can gain a sharp 360-degree view of their people, which they can rely on to help know, grow, and keep their people.

Ant Group has set the price for its shares of its dual IPO today, and it is shaping up to be the largest public offering to-date, coming in at $34.5 billion.

The IPO will be spread equally through 1.67 billion new shares issued on Hong Kong’s Hang Seng, which is expected to raise $17.24 billion (HK$133.65 billion), and 1.67 billion new shares issued on Shanghai’s Star Market, which is expected to raise $17.23 billion (¥115 billion).

Ant will debut on November 5 on Hong Kong’s Hang Seng. The company has not disclosed a date for its planned offering on Shanghai’s Star Market.

Ant’s new valuation is anticipated to top $313 billion, up from an estimated value of $218 billion earlier this year. According to Statista, this valuation, when compared to U.S. megabanks, sits only below JP Morgan Chase, which has a market capitalization of $434 billion.

The anticipated $34.5 billion raise is a record amount, breaking the previous highest IPO set when oil company Saudi Aramco went public at $29.4 billion earlier this year. Ant’s parent company Alibaba holds the record for the second-highest IPO when it listed on the New York Stock Exchange in 2014 and raised $24 billion.

Alibaba plans to maintain its 33% share in Ant Group by having its subsidiary Zhejiang Tmall Technology purchase 730 million shares in the company.

As we reported earlier this year, Ant’s double-listing is intentionally avoiding U.S. markets. This is not only because of geopolitical tensions, but also to take advantage of new innovations in both Hong Kong and Shanghai markets, which offer weighted voting rights and offer more market-driven pricing than other domestic exchanges.

Ant was founded in 2014 and has more than 1.3 billion active annual users. Simon Hu is CEO.

Intelligent conversational chat technology is on its way to the 174,000+ members of Michigan-based United Federal Credit Union. The institution, which serves customers in neighboring Indiana and Ohio as well as in Arkansas, North Carolina, and Nevada, has teamed up with Finn AI to add the chatbot service to its suite of digital banking offerings.

United FCU will integrate the technology into its LivePerson-based live chat system, which provides credit union members with immediate assistance for routine queries. The integration will enable human agents to spend more time on complex customer services issues and allow the automated technology from Finn AI to handle everything from account access problems to forgotten passwords.

“The pandemic has increased the need for financial services companies to provide a superior customer experience,” said Finn AI CEO Jake Tyler. “United realizes the importance that digital and AI have in delivering on this promise. We look forward to partnering with them as they lay out the future of their customer service offering.”

A two-time Finovate Best of Show award winner, Finn AI leverages artificial intelligence to deliver an intelligent chatbot solution that provides optimized, out-of-the-box support for 500+ of the most commonly-requested banking queries and questions. Finn AI’s chatbot technology can interact with customers over a wide range of channels: from websites and native apps to popular messaging platforms such as WhatsApp and Facebook. With Finn AI, institutions can inexpensively expand service availability, onboard more customers faster by streamlining basic processes, improve customer engagement, and reduce handling time.

Founded in 2014, Finn AI is headquartered in Vancouver, British Columbia, Canada. Over the summer, the company announced a partnership with Genesys to add its banking chatbot to Genesys’ AppFoundry marketplace of customer experience solutions. Finn AI includes ATB Financial, Fidor Bank, and fellow multiple-time Finovate Best of Show winner MX among its customers and partners.

When it comes to taking advantage of the best that the world’s fintech has to offer, you won’t find financial services companies in Canada sleeping on the job. This week in the country’s payments space, Toronto, Ontario-based Versapay announced its acquisition of Solupay, a contactless payments company based in Ohio. We also learned that FinovateEurope alum unblu, which offers a digital conversational platform for FIs from its headquarters in Basel Switzerland, had teamed up with Calgary, Alberta-based digital technology solutions provider Celero.

By the end of the week, Canada’s largest credit education company, Borrowell, announced that it was partnering with multiple Finovate Best of Show winner MX. Borrowell, the first company in Canada to offer free credit scores via its partnership with Equifax, has launched a new bill tracking feature called Boost on its app. The company will use MX’s data cleansing technology to improve Boost’s analysis of user spending behavior to help users make better financial planning decisions.

“With MX, Borrowell is giving its customers greater clarity into how they can become more financially strong as a means to increasing credit strength,” MX Chief Customer Officer Nate Gardner said. “It is exactly this kind of innovation, partnership and money experience that MX loves to enable through our powerful data platform.”

Last week we featured an extended Q&A with Eric Rosenthal, Vice President and Managing Director for the Americas with Rapyd. If you’re interested in learning more about the fintech ecosystem in one of the most overlooked regions of the world, our conversation with Eric Rosenthal is a great place to start.

With that in mind, congratulations to Mexican challenger bank Klar, which raised $15 million in Series A funding in a round led by Prosus Ventures this week. Founded in 2019, Klar now has approximately $72 million in total debt and equity financing, and noted that the new capital will help the company build its engineering capabilities in its hubs in Berlin and Mexico.

“Klar is making credit accessible to all Mexicans, including those with no credit history,” Klar co-founder and Chief Financial Officer Daniel Autrique said. “We help people build credit by looking at how and where they spend their money, instead of being stuck with traditional credit scores that are backward looking and obsolete.” The company said that, since inception, it has issued more than 25,000 lines of credit among its 200,000 customers.

Here is our look at fintech around the world.

Sub-Saharan Africa

Stripe makes inroads in Africa with acquisition of Paystack.

A partnership between Standard Bank, Mastercard, and Google will help SMEs in Africa offer their services online as well as accept digital payments.

Trading Technologies teams up with Cape Town-based Applied Derivatives, which will distribute the TT platform from South Africa.

Central and Eastern Europe

PayRay, a factoring company based in Lithuania, receives banking license and begins banking operations in its home country.

Lithuanian online payments firm Interpaylink partners with iDenfy to provide remote user identification.

Advapay, a digital core banking platform provider based in Estonia, teams up with U.K.-based identity verification platform Sumsub.

Middle East and Northern Africa

Cairo, Egypt-based financial wellness platform NowPay raises $2.1 million in seed funding.

Central Bank of Bahrain launches the region’s first digital fintech lab, FinHub 973.

Commercial Bank of Dubai introduces cards and accounts for low-income consumers courtesy of partnership with Now Money.

Central and Southern Asia

Indian payments processor Razorpay secures $100 million in Series D funding, earning a valuation just over one billion.

Mastercard announces partnership with Indian regtech Signzy to bring the company’s video KYC technology to its banking customers.

Indian fintech Open partners with Equitas Small Finance Bank and Visa to offer business debit card.

Latin America and the Caribbean

Brazilian payment solutions provider Ebanx announces expansion of operations into five countries in Central and South America.

Venio, a mobile app that provides financing to the unbanked, goes live in Mexico.

Chile’s third largest bank, Banco de Crédito e Inversiones (BCI), partners with Temenos to launch new corporate bank in Peru.

Asia-Pacific

The People’s Bank of China holds lottery to distribute millions in digital yuan valued at $1.5 million.

Vietnamese online payment portal AppotaPay scores payment intermediary license from State Bank of Vietnam.

PayMaya, a mobile payments platform based in the Philippines, launches new mobile payment device PayMaya One Lite, that enables acceptance of a range of digital payment types.

Nordic challenger bank Lunar announced a $47 million (€40 million) Series C funding round today, bringing its total raised to $122 million. The funds come from investment firm Chr. Augustinus Fabrikker and individual investors Klaus Oestergaard and Alan Howard.

Lunar plans to use the new funds to enter the buy now, pay later (BNPL) space. “It’s the most profitable banking landscape in the world, but also the most defensive, with least competition from the outside,” Founder and CEO Ken Villum Klausen told TechCrunch. “This means that the traditional banking customer is buying all their financial products from their bank.”

The decision to launch a BNPL tool comes after the company’s many successful launches, including paid subscriptions, consumer loans, and business bank accounts. The bank currently counts 5,000 business users and 200,000 retail banking users across the Nordic region.

Unlike established players in the BNPL market, Lunar’s BNPL tool will not rely on merchant partnerships. Instead, the bank will ask users after they make a purchase if they want to split the payment amount into installments. This model will work with both brick-and-mortar retail as well as ecommerce purchases.

Villum Klausen founded Lunar in 2015. The company’s 180 employees work in the company’s offices across Denmark, Sweden, and Norway.

In a venture round featuring Motley Fool Ventures and Ally Ventures – the strategic investment arm of Ally Financial – as well as individual angel investors, Streetshares has secured $10 million in new funding. The company said that it will use the capital, which takes the company’s total to more than $279 million, to drive future product development with an eye on serving small businesses in the post-PPP market.

“We’re seeing exciting digital adoption by banks and credit unions in response to COVID-19,” said StreetShares CEO Mark L. Rockefeller. “But equally important to us is the practical impact our technology is having in helping their customers, especially underserved business owners, get the funding they need to succeed.”

Founded in 2013 and launched a year later as an affordable digital lending alternative for veteran-owned small businesses, StreetShares unveiled its lending-as-a-service platform last year at our annual fintech conference FinovateFall. The platform enables banks to lend up to $250,000 to SMEs, and features a digital loan application, instant underwriting, loan servicing, and tracking. The company’s offering came in handy this year when the coronavirus struck and businesses across the country were shut down and starving for financial assistance. StreetShares’ technology was leveraged widely by community lenders in order to make Paycheck Protection Program funds available to SMEs.

As such, so far this year, a total of 53 financial institutions currently use the StreetShares platform. The company said that it is now expanding its platform into a suite of small business banking solutions that will be especially helpful for community banks, credit unions, and their small business clients as digital transformation initiatives continue in the wake of COVID-19.

“We’re seeing years of digital adoption by banks condensed into weeks,” said Ollen Douglass, Managing Director of Motley Fool Ventures. “Beginning with PPP, and now on to a full-suite of products, we believe StreetShares is positioned perfectly to power banks in their digital transformations.”

StreetShares is headquartered in Reston, Virginia. Read our profile of the company from last summer as StreetShares was stepping up to help bring needed financing to SMEs at the onset of the COVID-19 crisis.

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

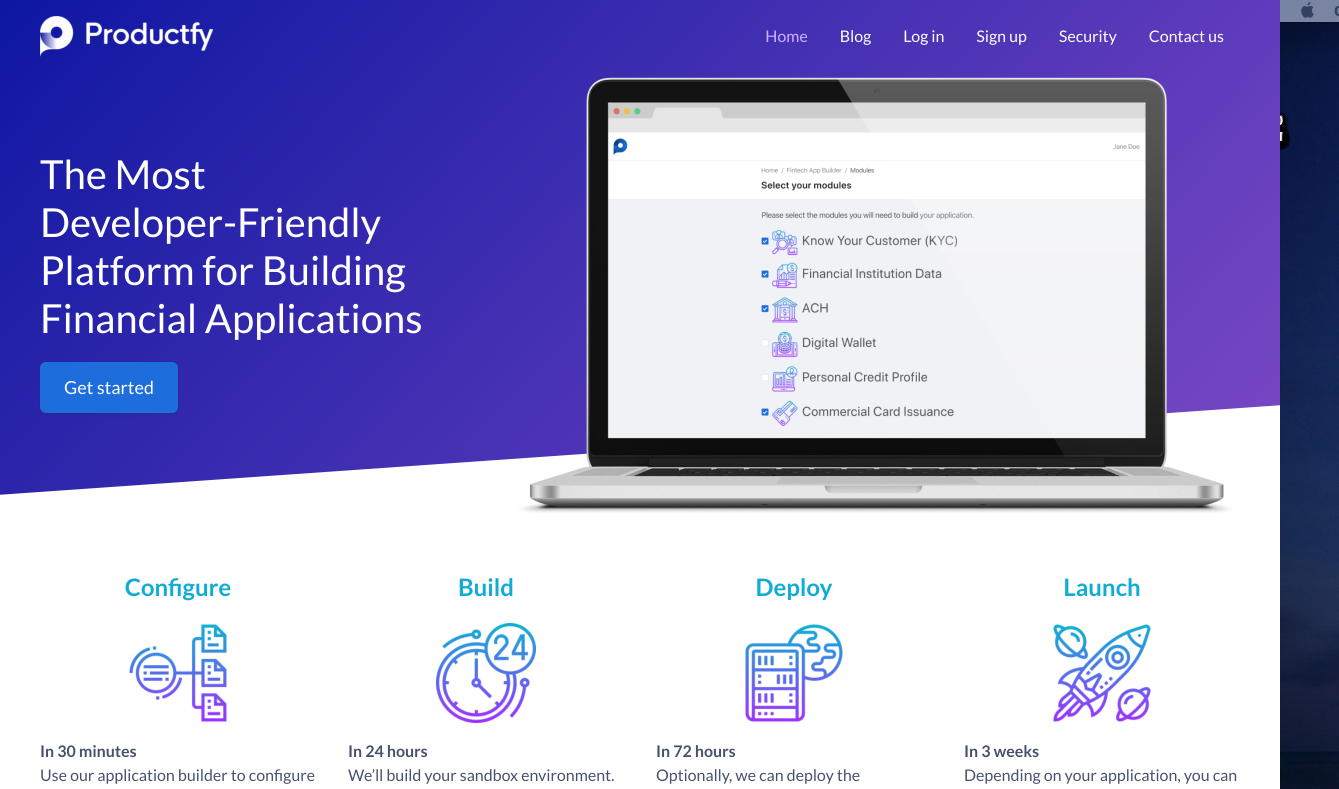

Productfy makes it fast, scalable, and seamless to launch new financial products to market. With a unified platform and a single line of code per feature, companies can go live in weeks.

Features

Fintech tools in a box with embedded module, compliance, and elastic banking infrastructure

Accelerate time to market without spending time and money on undifferentiated features

Developer friendly

Why it’s great Productfy’s solution entails both developer friendly embedded fintech features and white glove support to enable fintechs to navigate the regulatory process with financial data and bank partners.

Presenter

Duy Vo, CEO & Founder Vo started Productfy after seeing the convergence of two huge macro trends: mass adoption of higher abstraction platforms and financial services moving to the edge of service providers. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

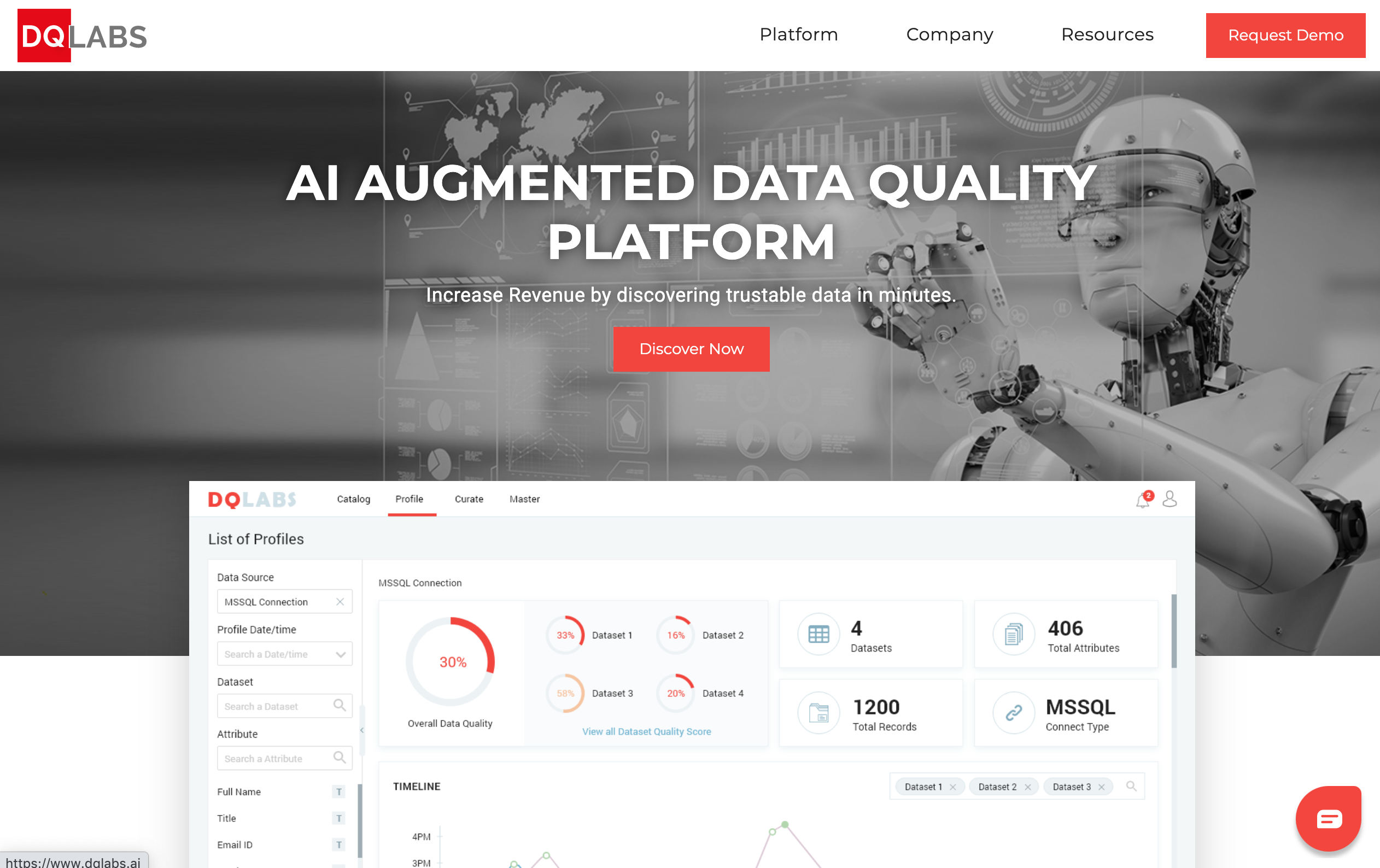

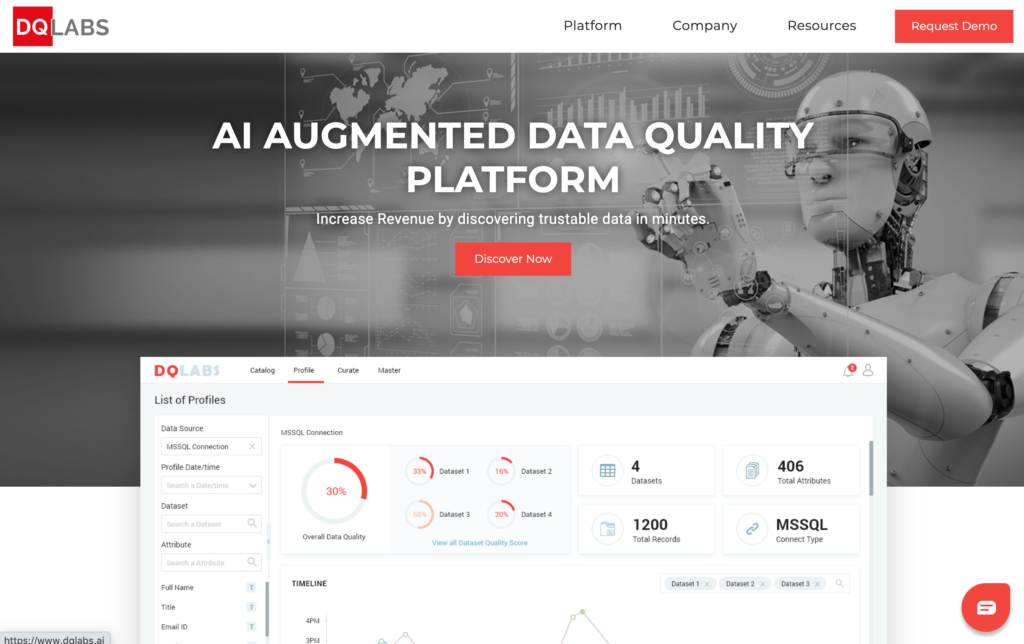

DQLabs is an artificial intelligence/ machine learning (AI/ML) augmented data quality platform that provides a simple way for organizations to handle issues around data quality, governance, curation, and master data management effectively.

Features

Discover trustable, high quality data in minutes using AI/ML

View a unified platform for data management needs

Conduct data ingestion, catalog, profiling, curation, governance, and MDM – all done in a few clicks

Why it’s great DQLabs’ AI augmented data quality platform gives organizations the ability to manage data smarter and leverage an immediate ROI in weeks, rather than months.

Presenter

Raj Joseph, CEO & President Joseph is a thought leader and visionary in the field of modern data management and augmented analytics and has two decades of experience around data science, AI/ML and enterprise data solutions. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

Glia is a digital customer service platform that connects financial institutions to their customers using chat, voice, video, co-browsing, and AI.

Features

Seamlessly move between modes of communication

Receive improved sales results and customer satisfaction via richer customer interactions

Deliver the best experience for customers and agents

Why it’s great By employing a digital-first approach to customer conversations, financial institutions improve customer satisfaction, reduce customer effort, and gain operational efficiencies.

Presenter

Dan Michaeli, CEO & Co-Founder Michaeli is the driving force behind Glia’s vision to combine the human touch with technology to create the best customer experiences. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

CoCoNet’s fully digital onboarding software for corporate customers optimizes common processes, making them up to 66% faster and more efficient.

Features

Mapping of complex structures with many individuals and permissions

Convenient digital legitimation and signature processes

Integrated customer analytics for process improvements

Why it’s great Unlike other onboarding solutions developed for retail customers, CoCoNet’s solution is only developed for corporate customers to fulfill the specific and complex needs of this niche.

Presenters

Björn Hassing, CEO Hassing is responsible for innovation, technology, marketing, and sales. He’s been a member of the board since January 2017. He started in 2005 as an IT Architect. LinkedIn

Dennis Rochel, MD & Head of Innovations Rochel started in 2013 as Mobile Development Architect at CoCoNet. He also studied computer science and IT security. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

ArnexaBinbox is the world’s first secure messaging platform that is phishing-free.

Features

Zero phishing engenders greater trust and engagement amongst users

End-to-end encryption

Simple APIs for easy sending and receiving of messages

Why it’s great Arnexa Binbox achieves zero phishing without content scanning and analyzing sender attributes. It uses unique signals that enable it to sift phishing messages cleanly, easily, and correctly.

Presenter

Sridhar Ramakrishnan, CEO & Founder Ramakrishnan is a long-time entrepreneur having worked in several startups. He serves on the board of CA Jump$tart, an organization dedicated to youth financial literacy. LinkedIn