This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

See how ALTR’s programmable data security is embedded into Q2ebanking’s Q2 Trustview in order to monitor, govern, and secure FI’s sensitive data in real time.

Features

Monitor: Provides shared visibility and an immutable view of data access

Govern: Delivers real time control and breach intervention

Protect: Delivers impenetrable protection of data at rest

Why it’s great ALTR is a simpler and more effective way to protect sensitive data that works on any infrastructure from on-prem to cloud.

Presenters

Doug Wick, ALTR’s VP Product and Marketing Wick leads product and marketing at ALTR. With over 20 years of startup experience, he has broad experience managing product conception and development through to market success. LinkedIn

Lou Senko, Q2ebanking CIO/SVP With more than 20 years of experience Senko is an engineer by trade and coach by passion, building skillful development and IT teams throughout his career. LinkedIn

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

Glia enables financial institutions to engage customers online via any mode of communication, and enhances experiences via patented CoBrowsing and layered with conversational AI.

Features

Seamlessly move between modes of communication

Receive improved sales results and customer satisfaction via richer customer interactions

Deliver the best experience for customers and agents

Why it’s great By employing a digital-first approach to customer conversations, financial institutions improve customer satisfaction, reduce customer effort, and gain operational efficiencies.

Presenter

Dan Michaeli, Co-Founder and CEO Michaeli is the driving force behind Glia’s vision to combine the human touch with technology to create the best customer experiences. LinkedIn

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

Faraday offers an end-to-end AI platform built for B2C growth. Integrations, consumer data, algorithms, deployment products — it’s all built in and supported by Faraday data scientists.

Features

Streamlined AI pipeline for fast, easy implementation

Rich data, advanced analytics, powerful models, all at your fingertips

Real-time, scheduled, and ad hoc scoring capabilities

Why it’s great The Faraday AI Platform enables you to operationalize predictive consumer insights and advanced analytics in six to eight weeks, with no in-house data scientists or engineers required.

Cory Albert, Account Executive Albert has a strong background in strategic software and marketing technologies. At Faraday, he helps clients implement custom AI capabilities to exceed their goals. LinkedIn

Riley Dickie, Account Executive Dickie has worked with Faraday’s consumer finance clients for the past three years, helping them take full advantage of their customer data through AI. LinkedIn

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

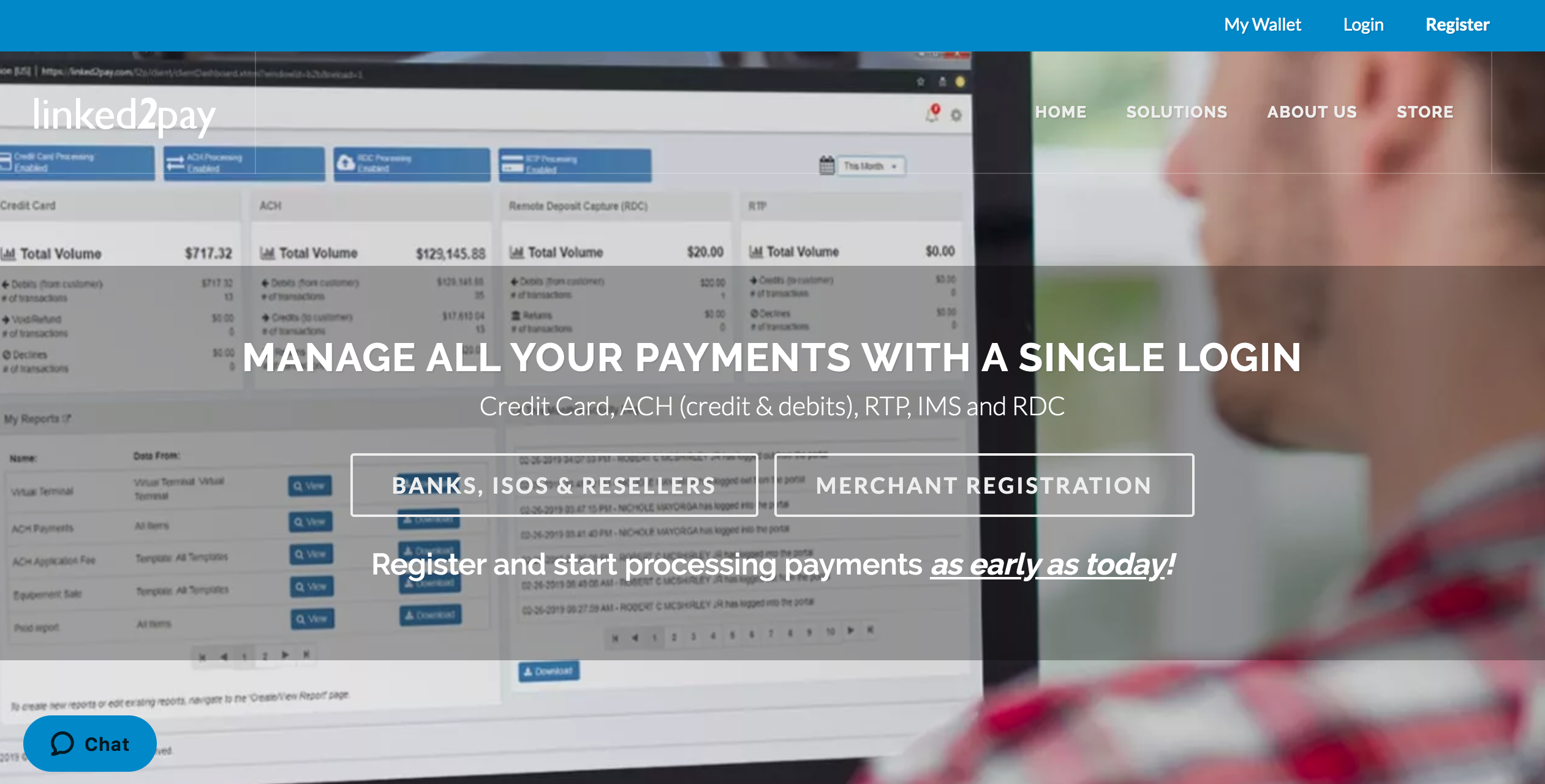

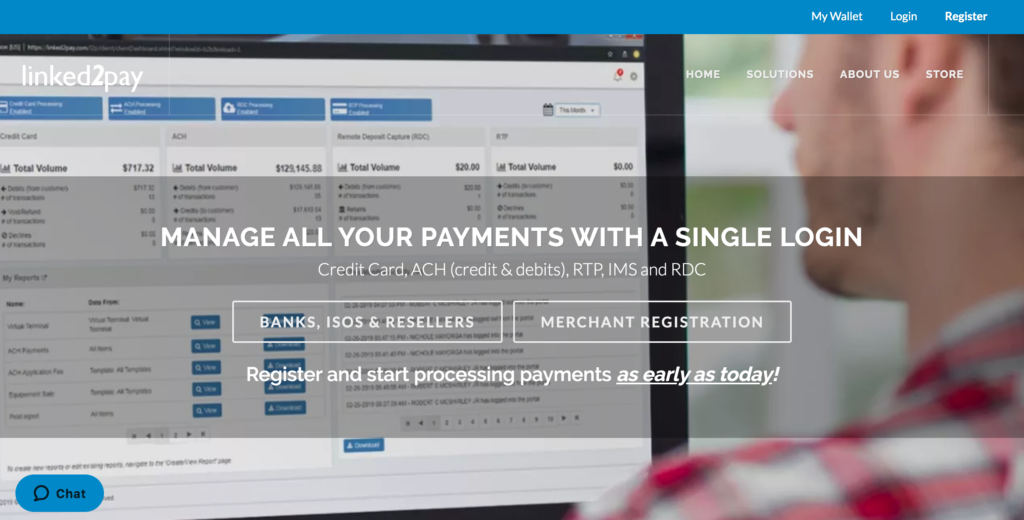

Linked2pay is an award-winning payment processing company. They will be demoing a product they invented called instant merchant settlement.

Features

Provides merchants their funds instantly upon batch out

Offers liquidity

Is cutting edge technology

Why it’s great Merchants receive their funds instantly upon batch out, 24/7/365.

Presenters

Kyle Taylor, COO Taylor has been with Linked2pay since the beginning. Primarily, he has a key role in managing all of the in-house programming and business development. LinkedIn

Madison McShirley, Operations McShirley started at Linked2pay earlier this year. Her role at the company is centered around assisting in the daily operations. LinkedIn

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

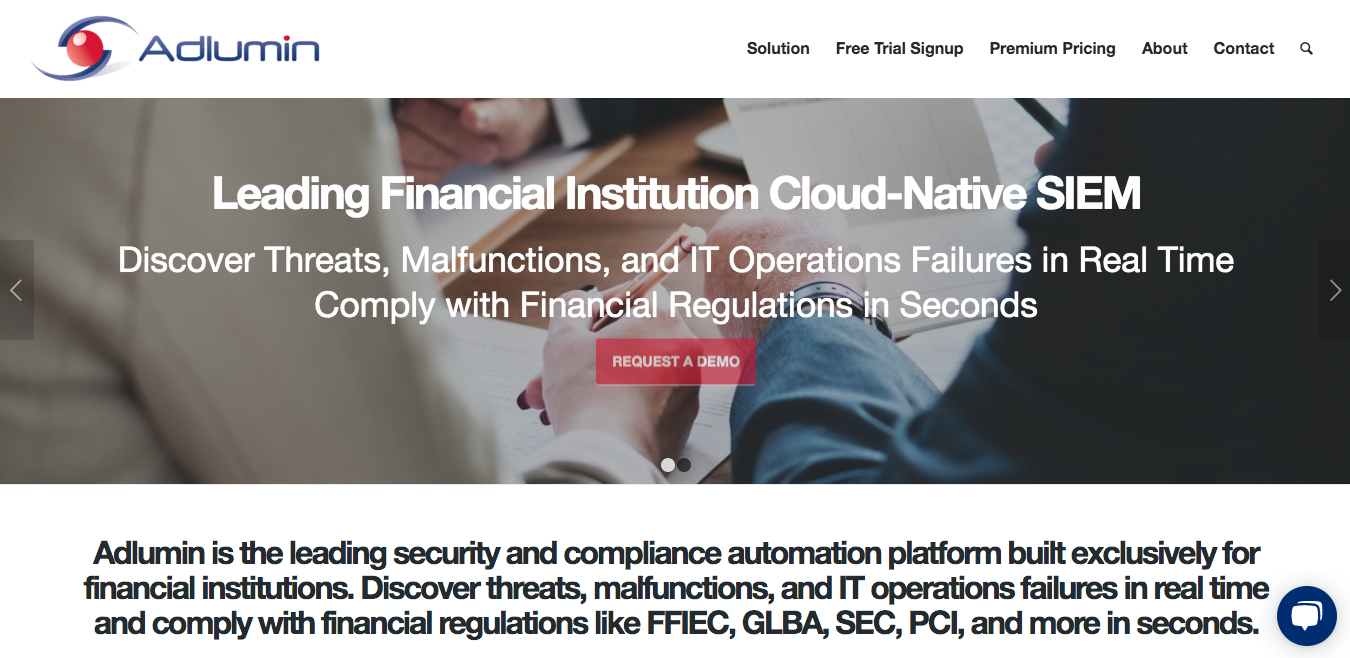

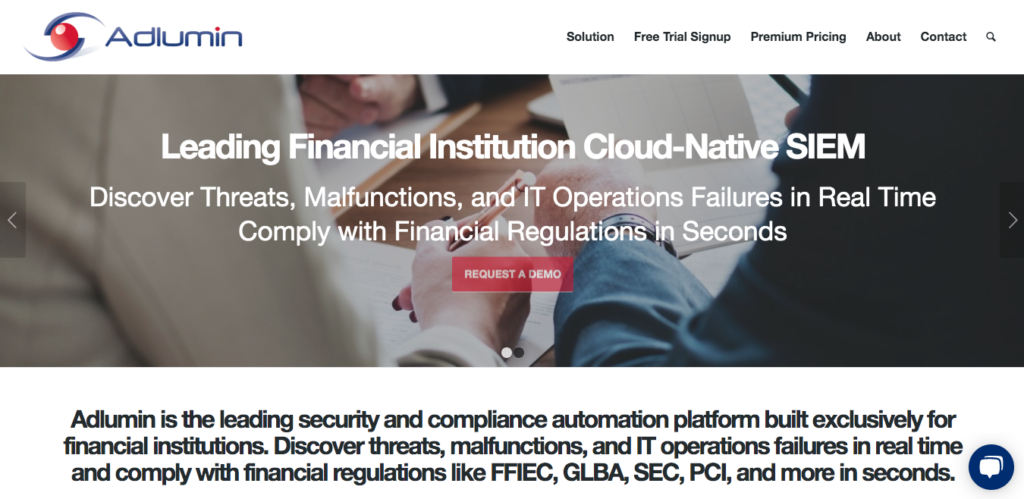

Adlumin delivers a cost efficient, easy-to-use, and simple-to-integrate, cloud-native security and compliance automation platform built exclusively for the financial services market.

Features

Automated regulatory reporting for requirements like FFIEC CAT, ACET, etc.

Security and compliance automation for the core banking ecosystem

Storage and encryption options for every standard

Why it’s great Adlumin was built exclusively for the financial industry, meeting their highly specialized compliance and technology requirements.

Presenter

Robert Johnston, President and Chief Executive Johnston is the President and Chief Executive of Adlumin, a cybersecurity technology firm focused on delivering cloud-native security and compliance automation technology. LinkedIn

FICO and risk investigation solutions provider Arachnys partner to help FIs improve their client onboarding and record management processes.

Bill.comcelebrates grand opening of new Houston office.

Finicityships new Verification of Income and Employment (VOIE) solution using TXVerify technology.

SecureKeycollaborates with Digital Bazaar to streamline organizational identity proofing.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Canadian identity innovator Truliooannounced today it brought in $53 million (CAD $70 million). The round was led by Goldman Sachs Growth Equity and saw participation from Citi Ventures, Santander InnoVentures and American Express Ventures. Trulioo’s total funding how stands at $73 million (CAD $96.6 million).

The Trulioo team will use the funds to build its presence in new markets, as well as boost its workforce from 130 to 200 people who staff the company’s Vancouver, San Francisco, and Dublin offices.

Trulioo’s team is 130 employees strong

“Today, families, businesses and entire economies are being powered by the global shift towards a truly digital economy, which is exciting but also opens up new forms of risk,” said Stephen Ufford, Trulioo CEO and founder. “We’re committed to leveraging technology to help our customers fight financial crime, money laundering and election fraud. I’d like to thank our investors for their trust in the work we are doing and for enabling us to push forward our solutions that transcend boundaries and channels, and which facilitate trusted transactions from anywhere, instantly.”

Trulioo’s API allows organizations to instantly verify identities of more than five billion consumers (more than two thirds of the global population) and more than 250 million businesses across 195 countries. The company’s GlobalGateway database offers an online electronic identity verification (eIDV) service that helps businesses comply with AML and KYC rules, as well as a range of international electronic identity verification requirements.

Trulioo, which will demo its technology at FinovateFall next week in New York, provides electronic identification technology that has the potential to positively impact people in developing nations who may not have much of an online record to prove their identity. This underrepresented group can now potentially open a bank account, apply for a loan, or conduct other financial activity that was previously out of reach.

Earlier this year, Trulioo’s Head of Growth, Anatoly Kvitnitsky,demonstrated GlobalGateway’s instant onboarding with EmbedID at FinovateSpring. EmbedID enables businesses to query Trulioo’s GlobalGateway API and instantly verify customers in multiple markets by embedding a snippet of code to their website.

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

InterGen Data’sDAVID – Digital Advice Via Demographics is a web platform (browser and/or widget) that is an artificial intelligence/ machine learning-driven experience which shows its users the financial impact of their upcoming Life Events. By using InterGen Data’s platform you will be able to help your advisors become contextually relevant to their clients and attract new customers, improve client engagement, and mitigate customer attrition.

Why it’s great By leveraging artificial intelligence and machine learning, companies can now deliver personalized experiences, be predictive, and move from a reactive to a proactive business model.

Presenter

Robert Kirk, President and CEO Kirk is a seasoned industry executive who is responsible for the vision, development, establishment, and growth of InterGen Data’s Life Stage / Life Event predictive technology to the BFSI industries. LinkedIn

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

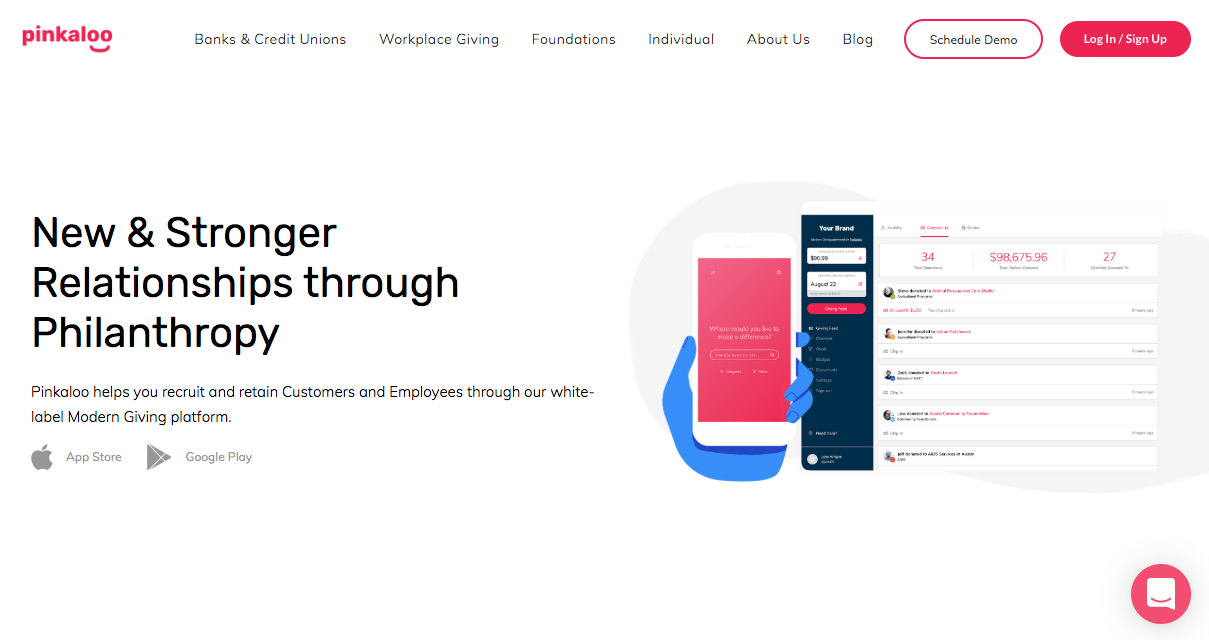

Pinkaloo helps financial institutions attract and retain customers and increase deposits and fees by powering their customers’ charitable giving.

Features

Win new customers, new deposits, and new fees

Help customers budget, discover great charities, and collaborate

Offer round-ups and incentives to drive key KPIs

Why it’s great Customers switch banks 2.5x more than before. Eighty one percent of millennials expect a commitment to good corporate citizenship. Pinkaloo’s white-label Modern Giving provides FIs with a solution to both.

Presenters

Gideon Taub, Founder & CEO Taub started his career on Wall St. before spending 10 years helping to build Videology, a VC-funded ad-tech product. He founded Pinkaloo to solve a personal problem he faced in managing his giving. LinkedIn

Daniel Gardner, COO Gardner spent 5 years at JP Morgan before transitioning into product and operations roles at tech startups. His passion for Pinkaloo stems from wanting to bring more data and transparency to giving. LinkedIn

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

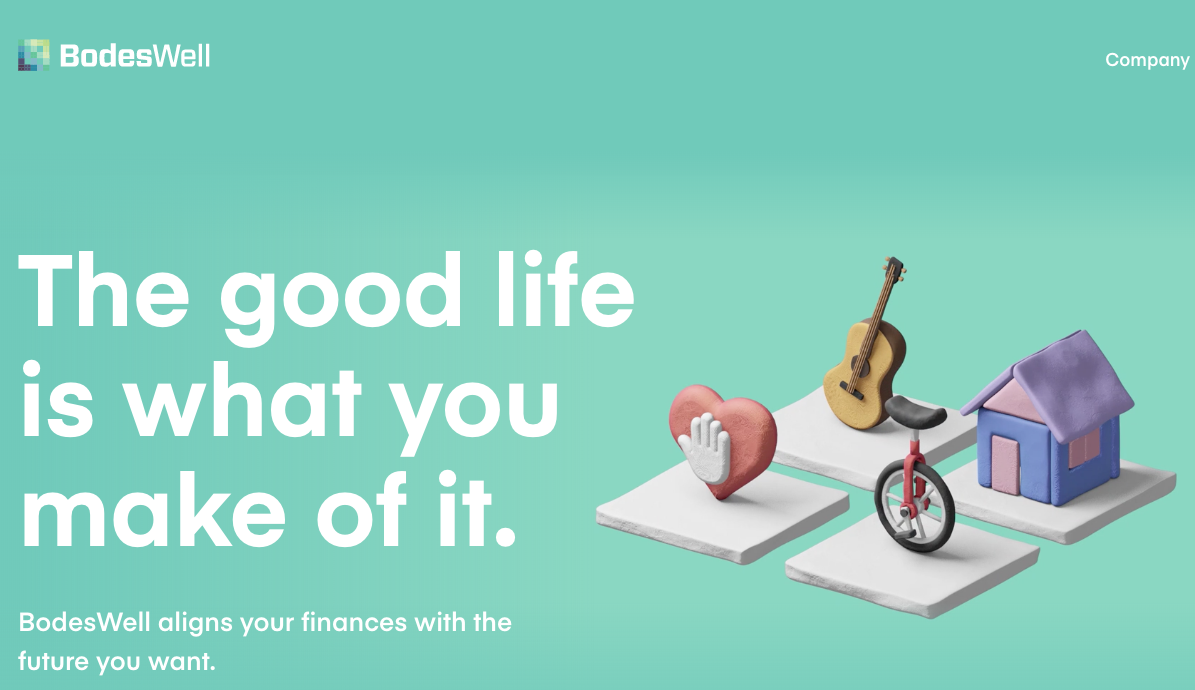

BodesWell aligns your finances with the future you want. The company’s one-page platform combines the user’s financial transactions data with models of the future in an easy, intuitive experience.

Features

Offers a simple, intuitive experience

Provides powerful analytical models and guidance

Brings the consumer confidence from knowing they’ve got a plan

Why it’s great BodesWell is built to integrate in a co-branded partnership model with your bank, insurance company, or investment firm.

Presenters

Matthew Bellows, Co-Founder and CEO Bellows is the co-founder of BodesWell. This is his third greenfield startup – he sold the first to CBS. He raised $50 million for the second startup from Google and Battery Ventures. He and his family live in Cambridge, MA. LinkedIn

Bernie Bernstein, Co-Founder and CTO Bernstein is the co-founder and CTO of BodesWell. Previously, he was CTO at Time Out Group, VP Engineering at Trip Advisor, and a Senior Engineer at Apple. Bernie and his family live in Newton, MA. Linked

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

Datanomers is fintech/AI. The company’s Financial Risk Profiler, deployed at banks, reduces defaults by 5% to 15%. The Customer Insight Manager is unique; it alerts banks to customer attrition – proactively so that they can retain them.

Features

Assists in meeting incremental growth targets by preventing attrition of premium customers

Identifies key customer insight: what’s uppermost in their mind

Does all this in real-time

Why it’s great Customer Insight Manager (CIM)– is the world’s most advanced AI, Natural Language Understanding solution that identifies premium customers at risk of leaving- stopping customer attrition in its tracks.

Presenters

Deepak Dube, Founder and CEO Dube is a Ph.D. Previously, he was a Bell Labs researcher for 19 years, served on the faculty at NYU, and was CTO at IPsoft. He holds patents and speaks on AI and ML. He led a team to invent the world-renowned cognitive agent Amelia. LinkedIn

Meeta Pandey, VP Business Development Pandey, Ph.D., is a dynamic business leader with a diverse background ranging from being ex-faculty at Monmouth University, to consulting for financial firms, to building a business with world-class teams. LinkedIn

A look at the companies demoing live at FinovateMiddleEast on November 20 and 21, 2019 in Dubai. Register today and save your spot.

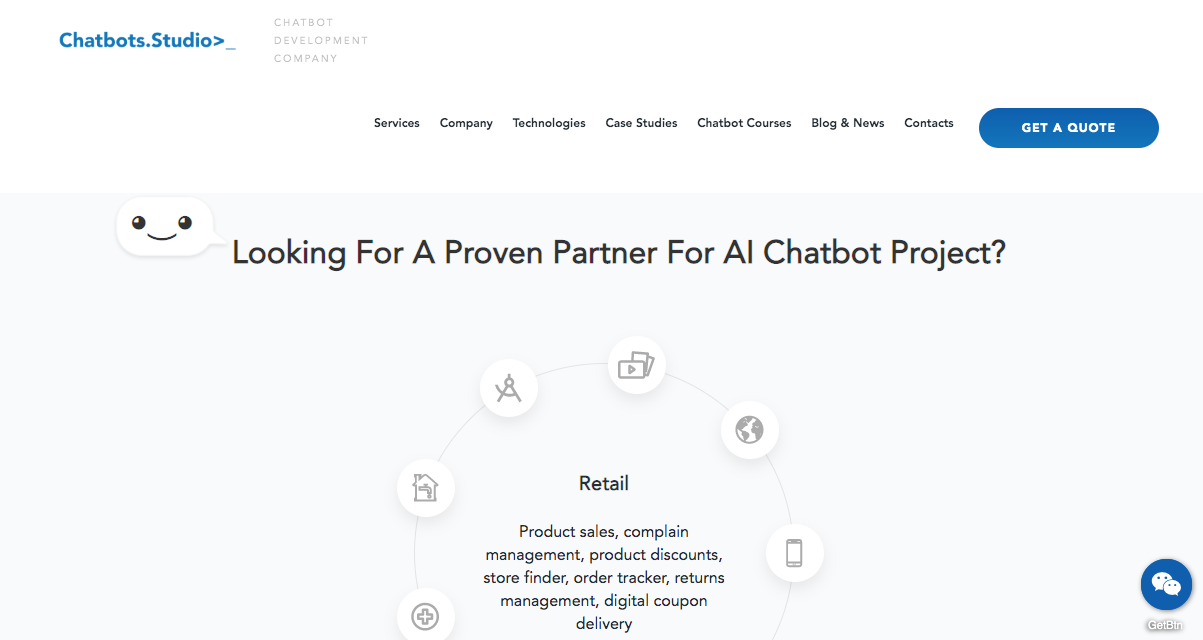

Chatbots.Studio’sBot Commerce Platform helps to connect merchants, customers, CRM, and payment providers. The platform allows SMEs to create a chatbot for different messengers and accept payments instantly.

Features

Cloud marketplace of commercial bot templates

One-click payments via Apple/GPay

Why it’s great Chatbots.Studio solves the problem of digitalization and communications with customers in smartphones for SMEs.

Presenters

Max Popov, Co-Founder & CTO at Chatbots.Studio Popov is co-founder and CTO of Chatbots.Studio. He has more than 15 years of experience in banking and fintech as Head of CRM, Cloud Technologies, and CTO. LinkedIn

Egor Avetisov, Head of Innovations at Privatbank Avetisov has more than 12 years of experience in banking and technology. He is responsible for the implementation of new technologies and collaboration with big tech companies. LinkedIn