The decision by Canada’s Constellation Software to acquire Uruguayan technology firm – and Finovate alum – Infocorp earlier this year is a reminder of the vibrancy of the fintech ecosystems thriving in the countries to the north and south of the U.S. The acquisition was completed in June via Constellation Software’s U.S.-based subsidiary Aquila.

“We have been looking for a partner to support us as we move to our next level of experience for our clients,” InfoCorp CEO Ana Inex Echavarren said. “We are excited to join Aquila and the Constellation family as they believe in long-term relationships, and the ‘buy and hold forever’ approach supports us in our focus on long term growth with our clients.”

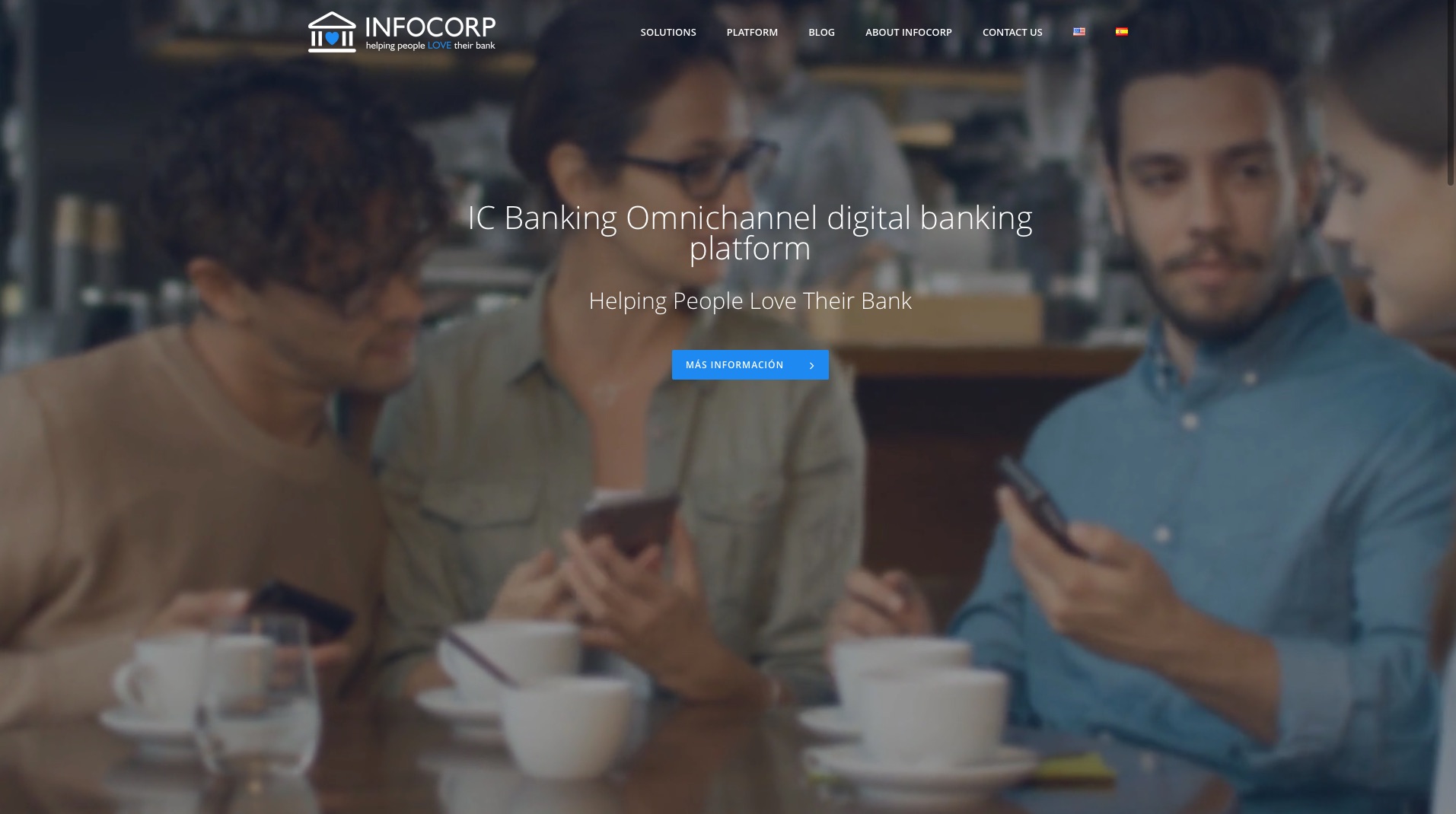

Montevideo-based InfoCorp offers its customers an omnichannel banking platform that leverages the latest advanced technologies – conversational AI, machine learning, voice recognition, and chatbots – to build solutions to better engage and serve financial services customers. With clients such as Banco Santander, Banco de Bogota, Banco Internacional, and Towerbank, the 25+ year old company made its Finovate debut in 2017, demonstrating its marketing and commercial actions orchestrator platform that enables more agile, personalized, marketing campaigns that lead to higher conversion rates and ROI.

“InfoCorp has an inspiring focus on their clients,” Aquila CEO Mike Byrne said. “To produce solutions that connect the banks with their clients is such a deep passion for the team at InfoCorp. We are really looking forward to working with the group.” Operations at InfoCorp will remain the same, post-acquisition, with Echavarren continuing as CEO and the company keeping its client portfolio and offices. InfoCorp has 250+ workers in its development and innovation centers in Santiago de Chile, Montevideo, and Colonia.

In fact, the company announced last month that it is looking to expand into both Mexico and Argentina in the wake of the acquisition, with potential expansion to Europe, Canada, and the U.S., as well. Echavarren told BNamericas that the company is currently growing at a rate of 40% to 50% a year over the past five years and is looking at investments to power Infocorp’s ability to enter bigger markets.

The fintech ecosystem in Uruguay is often overlooked compared to the fintech industries in other Latin American nations such as Mexico and Brazil – both of which Uruguay borders. With a population of approximately three and a half million, the country is the second smallest in South America and gets high marks on a number of metrics including democracy, low perception of corruption, and e-government. Uruguay is regarded as a “high-income country” by the United Nations.

In its look at fintech in Uruguay, Contxto highlighted a baker’s dozen of companies that are not only growing regionally, but moving closer to expansion worldwide. The feature divides the country’s fintech industry into five components: payments, exchange, open banking, investments, and what it calls “fintech enterprise services (FES).” This primarily involves providing fintech solutions to online financial services companies.

Here is our look at fintech around the world.

Sub-Saharan Africa

- A partnership with Standard Chartered Bank will enable Airtel Africa to build its fintech business and help support financial inclusion.

- South African digital banking platform provider Ukheshe earns finalist spot in the 2020 Ecobank Fintech Challenge.

- ThisDayLive features VC investor Ameya Upadhyay on the challenge of startup development in Africa.

Central and Eastern Europe

- Fintech Futures takes a look at financial inclusion in Russia.

- Poland’s mPay teams up with iDenfy to bring biometric facial recognition and other identity verification technologies to its mobile payments platform.

- Romania’s PayByFace brings its biometric facial recognition technology to Up Romania cardholders, enabling biometric purchases as participating stores and restaurants.

Middle East and Northern Africa

- CIH Bank of Morocco partners with Finastra for a remote implementation of the company’s Fusion Corporate Channels and Fusion Trade Innovation systems.

- Cairo, Egypt-based payments-as-a-service fintech Paymob raises $3.5 million in funding.

- National Bank of Oman enables cardless ATM transactions.

Central and Southern Asia

- MEDICI featured Indian regtech startup Signzy in its RegTech Top 21 Startups for 2020 roster. Signzy is the only Indian regtech to make the list.

- Reserve Bank of India announces offline digital payments pilot project.

- JCB International and PJSCB Orient Finans initiate merchant acquiring operations in Uzbekistan.

Latin America and the Caribbean

- Mexican lending platform Creze raises $12 million.

- Rapyd partners with PayMyTuition to boost the company’s ability to accept bank transfer-based payments from countries in Latin America and the Asia Pacific region.

- WorldRemit teams up with a pair of Mexican neobanks, albo and Klar.

Asia-Pacific

- Ayoconnect, a billpay network based in Indonesia, raises $5 million in pre-Series B funding.

- Southeast Asian fintech TrueMoney teams up with cross-border payments firm Thunes to expand its remittance business.

- Vietnamese digital banking platform Timo announces new partnership with Viet Capital Bank.