This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In our latest interview from FinovateFall 2025, Beyond the Arc CEO Steven Ramirez talks with Shruti Patel, EVP and Business CPO at US Bank, about the institution’s approach to supporting small- and mid-market businesses. The two discuss the emergence of new digital capabilities, embedded payroll and account payable solutions, as well as the role of customer experience in shaping product design.

“We are super focused on our small businesses. They are looking for very simple banking products: an easy-to-use, best-in-class operating, savings, or money market account. They’re looking for a great rewards card. And then, last but not least, small dollar loans. We excel in our small business access loans. We are number four nationally and very close in California, as well. When it comes to their lending needs, when it comes to their banking needs, we’re very much focused on how can we make the life of a small business really, really easy.”

Joining US Bank in 2023, Patel has brought leadership experience from across fintech, banking, and payments. Previously head of global partnerships and monetization at Shopify—and before that head of embedded payments and partnerships at JPMorgan Chase—Patel today oversees services for US Bank’s small business and mid-market customers across money movement and credit card solutions, as well as the bank’s full suite of digital capabilities.

With nearly 1.4 million business customers representing up to $25 million in revenue, US Bank serves its clients at every business life stage—from starting a business to managing a growing company to selling a successful venture. US Bank provides a comprehensive and integrated suite of banking and payments solutions delivered both digitally and via its trusted banking partners.

U.S. Bank partnered with Kyriba to launch Liquidity Manager, an AI-powered cash forecasting and liquidity management tool for commercial clients.

The solution offers real-time visibility, scenario planning, reconciliation, and multi-bank reporting, helping firms automate workflows and reduce operational risk.

The move signals U.S. Bank’s push into tech-forward treasury capabilities, positioning it to compete with modern finance platforms like Ramp.

U.S. Bank has teamed up with treasury solutions company Kyriba to launch a cash forecasting tool to offer businesses visibility and control over their cash and liquidity positions. The new tool, Liquidity Manager, is powered by Kyriba’s liquidity performance platform.

Leveraging Kyriba, U.S. Bank will deliver cash forecasting, scenario planning, and operational efficiencies to its mid- to large-scale commercial clients. Kyriba’s SaaS solutions empower CFOs, treasurers, and IT leaders to connect, protect, forecast, and optimize their liquidity. Founded in 2000, the company aims to help companies and banks improve their financial performance and increase operational efficiency.

“Many companies struggle to obtain a timely and accurate view of their liquidity, especially when managing multiple bank accounts across geographies and currencies,” said U.S. Bank Treasury and Payment Solutions Lead Kristy Carstensen. “This solution builds on the strengths of both U.S. Bank and Kyriba to address these challenges. By automating processes and providing actionable insights, U.S. Bank Liquidity Manager, powered by Kyriba, will empower our clients to make strategic financial decisions with confidence and ease.”

The new tool will improve firms’ cash forecasting by using historical cash flow data to predict future inflows and outflows, providing greater accuracy in daily cash position reporting and supporting more informed scenario planning. Liquidity Manager will also include cash positioning and reconciliation, cash pooling for zero-balance accounts, multi-bank balance and transaction reporting, and real-time visibility for all stakeholders. U.S. Bank expects these capabilities will help firms reduce costs through automated, centralized cash oversight and streamline workflows that minimize manual effort and operational risk.

Liquidity Manager will be available through U.S. Bank’s treasury management platform SinglePoint, which the bank updated a few weeks back. The new SinglePoint release aims to reduce manual work, deliver actionable insights, optimize common user flows, and help clients uncover operational blind spots.

“Working together, Kyriba and U.S. Bank can elevate liquidity management and cash forecasting for businesses,” said Kyriba CRO Bruno Ferreira. “By combining Kyriba’s secure, trusted AI-enabled technologies with U.S. Bank’s deep payments and banking expertise, we deliver real-time visibility across every account and region. This clarity empowers treasurers and finance teams to make confident decisions exactly when they need to, without guesswork or delays.”

Launching advanced treasury management tools may be U.S. Bank’s way of competing with platforms like Ramp, which are expanding beyond spend management into broader operational finance functions. Ramp, in fact, has proven that there is an appetite for this model, disclosing in a funding announcement yesterday that it is now valued at $32 billion.

By strengthening its digital treasury stack, U.S. Bank positions itself as not just a traditional banking partner, but as a technology-minded bank capable of meeting CFO-level expectations around automation, visibility, and real-time decision support.

This article is brought to you in collaboration with Gregory FCA.

AI and personalization are redefining the rules of engagement in business banking. As Executive Vice President and Chief Product Officer for Business Banking at U.S. Bank, Shruti Patel (pictured) brings a unique lens to the discussion, drawing from her deep experience in banking, payments, and fintech.

Following her appearance at FinovateFall 2025, we sat down with Shruti to discuss the evolving needs of business customers, the transformative role of AI, and the growing importance of partnerships between banks and fintech.

Tell us a little bit more about your role at U.S. Bank, your title, and what you’re responsible for.

Shruti Patel: I am the Executive Vice President, Chief Product Officer for Business Banking at U.S. Bank. In this role, I oversee services for our small business customers, ranging from $100,000 to up to $50 million in annual revenues, across banking, payments and our full suite of digital capabilities.

You spoke on the panel about the customer experience revolution. In your view, what do today’s business banking customers expect from their financial partners that they didn’t expect five or ten years ago?

Patel: We consistently hear two key expectations from our small business customers. First, they want banks to deliver best-in-class, highly sophisticated digital capabilities. Nearly 80% of small business customers, including U.S. Bank customers, have time and again told us that they’re expecting their banks to give them a one-stop shop. Many are already banking with us across our deposit products. They engage a lot with our payment products, whether this is small dollar loans, large dollar loans, or credit card solutions, or operating lines of credit.

But beyond these core services, they increasingly expect seamless, integrated digital experiences. By that, I mean not just dashboards that track transactions, but robust features like money moment insights, best-in-class accounts payable and receivable tools, and embedded payroll capabilities. To address these needs, we recently announced two exciting developments: our new accounts payable solution in partnership with Melio and Fiserv, and embedded payroll capabilities in partnership with Gusto. Both are part of our broader commitment to delivering integrated, end-to-end experiences for small business customers.

AI is everywhere in the conversation this year. Beyond the hype, how are you seeing AI deliver real value to business banking customers, whether through engagement, personalization, or entirely new experiences?

Patel: We are still in the early stages of deploying AI, but we’re already seeing strong impact across several use cases. The first is fraud monitoring and detection—security is top of mind for our business banking customers, and AI has proven valuable for fraud monitoring early detection.

The second area is customer service. While not a new application for AI, we’re using it to transcribe interactions, synthesize information, and provide our service teams with a complete view of the customer relationship. Because business owners are pressed for time, they expect seamless, efficient support from us, and AI helps ensure our teams can respond quickly and effectively.

We’ve seen a wave of innovation in areas like billpay and payroll, often driven through partnerships between banks and fintechs. Why are these types of collaborations becoming so important for small business banking?

Patel: As I mentioned earlier, small business customers are navigating an unprecedented macroeconomic environment. They’re dealing with tariff pressures and uncertainty, persistent inflation, supply chain disruptions lingering from the pandemic, and ongoing challenges in accessing capital. In this context, anything financial institutions can do to help small businesses operate more efficiently and cost-effectively is critical—not only for their success but also for deepening engagement and trust.

That’s where fintech partnerships have become so important. Business owners often tell us they feel overwhelmed by the number of software options available. They’re looking for simple, integrated solutions that support core needs like cash flow management, accounts payable and receivable, and payroll. For example, if you’re a small business with fewer than 10 employees, you want easy-to-use payroll software that just works.

With this in mind, we’ve anchored our strategy on fintech partnerships and selective acquisitions to create a one-stop shop. We launched embedded payroll capabilities with Gusto, accounts payable solutions with Fiserv in partnership with Melio, and made strategic acquisitions such as talech, a point-of-sale solution, Bento for spend management, and TravelBank, which complements our corporate card offering. Together, these investments strengthen our ability to support small businesses end-to-end.

As you reflect on FinovateFall, what are the biggest themes or innovations you heard about that excite you about the future of business banking?

Patel: For me, the most exciting theme is personalization. I participated in a session on AI and personalization, and it reinforced that while banks and financial institutions have access to strong data, we still have a long way to go in harnessing it effectively. Accompanying customers through their end-to-end journeys and across different stages of the business lifecycle is critical.

For example, the needs of a startup are very different from those of a mature, established business. A startup might be focused on accessing small-dollar loans, while established businesses may require large operating lines to scale and expand. Small businesses need a very simple operating account with some benefits around digital transactions and money movement, but our large customers are looking for robust money movement capabilities and Treasury solutions.

The key is building personalization into these core jobs. Customers frequently ask us: “Should I be using Faster Payments or ACH?” That’s where AI can help, by serving as a product recommender that guides business owners to the right solution based on their specific needs.

As summer draws to a close, there may be a big acquisition on the horizon in the fraud and financial crime prevention space. Be sure to check in with Finovate’s Fintech Rundown all week long for the latest in fintech news.

U.S. Bank launched its Accounts Receivables platform, U.S. Bank Advanced Receivables, in partnership with Billtrust.

U.S. Bank Advanced Receivables will help businesses keep costs low and benefit from real-time visibility into cash flow and financial position.

U.S. Bank most recently demoed its technology at FinovateFall 2021 in New York.

Courtesy of a partnership with Billtrust, U.S. Bank has launched its new comprehensive accounts receivable (AR) platform. U.S. Bank Advanced Receivables will help suppliers accelerate cash flow, lower costs via automation, and provide better payment experiences.

“Suppliers face many challenges from the time they receive an order until the cash is in their account. This includes numerous manual and paper-based steps, a cumbersome credit process, billing errors, and payment delays,” U.S. Bank Global Treasury Management Head of Product Alberto Casas explained. “With U.S. Bank Advanced Receivables, businesses can transform their entire receivables process to drive down costs and gain real-time visibility into their financial position and cash flow.”

U.S. Bank Advanced Receivables combines U.S. Bank’s payment and risk management capabilities with Billtrust’s AR technology. The new offering is comprised of five core solutions – invoicing, payments, cash application, collections, and credit – each of which enhances the B2B receivables process. U.S. Bank Advanced Receivables builds on the bank’s complementary digital payment solutions, such as U.S. Bank AP Optimizer, which automates accounts payable operations from invoice receipt to payment disbursement. Together the two offerings enable companies to digitize and automate their end-to-end payment processes.

With $680 billion in assets, U.S. Bancorp is the parent company of U.S. Bank National Association. Based in Minneapolis, Minnesota, the firm serves millions of customers locally, nationally, and around the world with services including consumer banking, business banking, commercial banking, institutional banking, payments, and wealth management. Billtrust, which partnered with U.S. Bank to launch the bank’s new AR offering, is an integrated AR solutions provider whose technology is used by more than 2,400 companies worldwide. These clients range from Coca-Cola and FedEx to Staples and United Rentals.

Earlier this month, Billtrust announced that it had extended its collaboration with Visa to support its Business Payments Network (BPN). Introduced in partnership with Visa in 2018, BPN links suppliers to buyers via connectivity to their preferred bank and payables providers. Headquartered in Hamilton Township, New Jersey, and founded in 2001, Billtrust was acquired by EQT Private Equity for $1.7 billion in 2022.

U.S. Bank most recently demoed its technology at FinovateFall in 2021. At the conference, the bank demoed its U.S. Bank Card as a Service (CaaS) solution. The technology enables fintechs and other businesses to extend corporate credit digitally, and to create a custom virtual payment experience for customers via API integration.

U.S. Bank is using technology from Pagaya to help underwrite unsecured personal loans.

Pagaya’s AI model generates underwriting recommendations and completes a secondary credit decisioning review of borrowers who were originally rejected.

The partnership, which has the potential to expand U.S. Bank’s borrower pool, has already led to the approval of more than 2,000 personal loans over the past few months.

U.S. Bank announced today it has tapped alternative underwriting solutions company Pagaya to help more borrowers qualify for loans.

U.S. Bank initiated the partnership to help more clients access personal loans, which often pose more risk for lenders because they are unsecured. Pagaya leverages AI to complete a secondary credit decisioning review of borrowers who are initially rejected. If Pagaya approves the borrower, U.S. Bank will originate and service the loan.

Key to the solution is Pagaya’s AI model that analyzes thousands of data points to generate tailored underwriting recommendations. Because the model uses more data than a traditional regression model, U.S. Bank can more efficiently find applicants who are responsible borrowers, but who don’t fit into the bank’s FICO score cutoff.

As interest rates remain high, banks will continue to face challenges in managing their lending operations. When higher interest rates lead to increased borrowing costs, some customers are unable to afford previously attainable loans. Also contributing to the smaller borrower pool, banks have become more selective in their lending practices by focusing on borrowers with strong credit profiles and stable financial histories.

“We know that we have many clients who don’t fall within our traditional credit parameters,” said U.S. Bank Head of Consumer Lending Partnerships Mike Shepard. “By expanding access to responsible credit solutions, we are giving clients access to funds when they need it the most, through their existing and trusted banking relationship with us.”

Ultimately, using Pagaya helps U.S. Bank extend loans to more clients by delivering credit to individuals who would otherwise be rejected. Since U.S. Bank began working with Pagaya for underwriting a few months ago, the bank has been able to approve more than 2,000 clients for personal loans.

New York-based Pagaya was founded in 2016 and has raised $1.6 billion in combined debt and equity across ten funding rounds. The company went public via a SPAC merger in 2021 and currently trades on the NASDAQ under the ticker PGY with a market capitalization of $8.95 million.

“We share U.S. Bank’s commitment to increasing access to life-changing financial products and services,” said Pagaya Chief Growth Officer Leslie Gillin. “With Pagaya’s integrated and seamlessly embedded lending technology, our lending partners can expand and deepen their client relationships to a more diverse group of borrowers.”

U.S. Bank launched a new suite of embedded payments solutions within Microsoft Dynamics 365.

The collaboration embeds U.S. Bank payment capabilities across Microsoft platforms.

U.S. Bank said it plans to embed additional payment capabilities within platforms such as Microsoft Teams and Microsoft Power Platform.

U.S. Bank’s collaboration with Microsoft announced earlier this year has borne fruit: the bank has introduced a new suite of embedded payments solutions within Microsoft Dynamics 365. The integration embeds U.S. Bank payment capabilities across Microsoft platforms. It also makes U.S. Bank among the first financial institutions to take advantage of the opportunity of directly integrating into the popular enterprise resource planning (ERP) and finance solution.

Among the solutions available to businesses using Microsoft Dynamics 365 is the U.S. Bank AP Optimizer. Available directly from their business application, the technology gives treasury management teams the ability to automate invoice processing for both business and consumer payment disbursement within Microsoft Dynamics 365. This will facilitate automated accounts payable workflows, including matching and reconciliation.

“We are committed to meeting clients wherever they are in their digital journey, bringing payments to businesses in a way that’s instant, embedded and connected to the technology they use every day,” U.S. Bank vice chair and head of Payment Services Shailesh Kotwal said. “Our integration with Microsoft – which businesses rely on daily to serve their customers – opens new possibilities for U.S. Bank clients to improve efficiencies and enable faster payments.”

According to U.S. Bank, this week’s news is only the beginning. The bank announced that it has plans to embed additional payment tools within Microsoft platforms such as Microsoft Teams and Microsoft Power Platform.

“Embedded payments can deliver powerful, new ways for businesses to streamline processes, enhance visibility, deliver better experiences, and reduce risk,” Microsoft Corporate Vice President for Worldwide Financial Services Bill Borden said. “We are excited to build on our work with U.S. Bank, delivering integrated, easy-to-use digital payments capabilities to our customers through Microsoft Dynamics 365 with additional embedded solutions to come.”

The two companies have been working together closely since February, when U.S. Bank announced a “substantial investment” in the modernization of its technology by choosing Microsoft Azure at its primary cloud provider for applications. The move will give customers more tools and more options when it comes to accessing banking services and provides U.S. Bank with opportunities to grow via new partnerships and what the bank sees as an “ever-evolving financial services marketplace.”

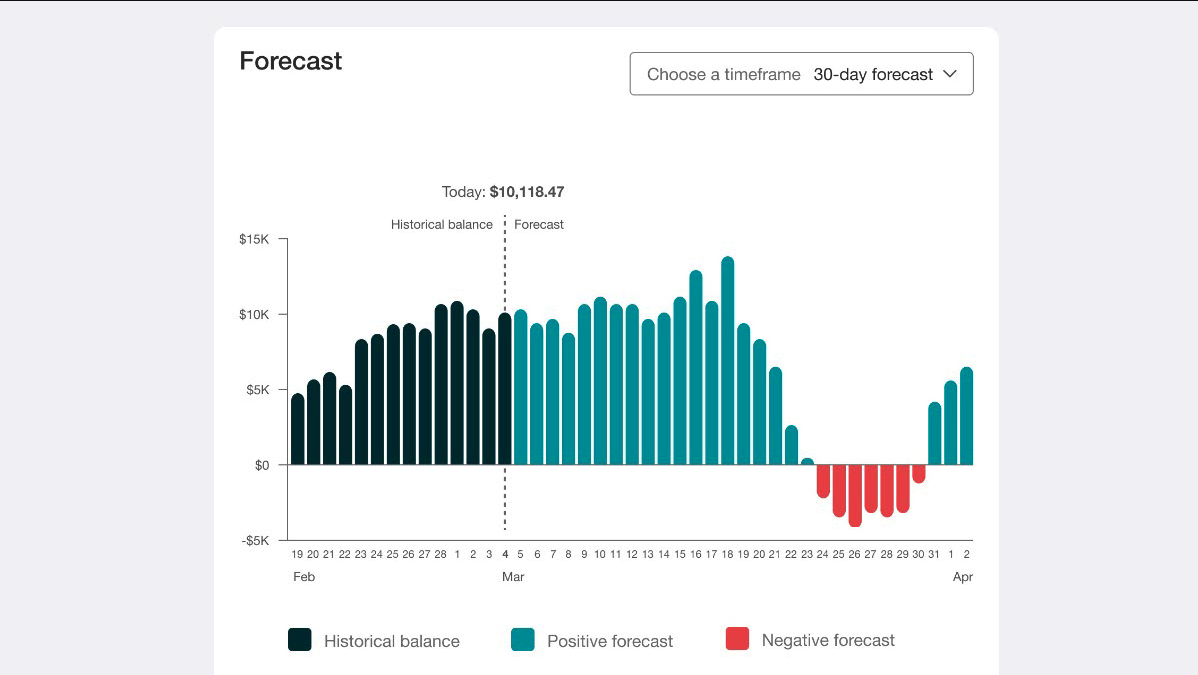

U.S. Bank’s collaboration news comes just one month after the bank introduced a new cash flow prediction tool for small businesses. The solution gives SME owners a 90-day forecast of cash flow and enables them to factor in external client data along with data from their own U.S. Bank accounts to provide more comprehensive cash flow insights.

U.S. Bank most recently demoed its technology last September at FinovateFall 2021. At the conference, the Minneapolis, Minnesota-based bank demoed its Card-as-a-Service (CaaS) solution. The offering enables fintechs, partners, and clients to digitally extend corporate credit, and to leverage API integration to create a custom virtual payment experience in their own ecosystem. Spending limits, tokenization, and encryption are all features of U.S. Bank’s CaaS solution.

U.S. Bank introduced a new tool to give small business owners the ability to see a 90-day forecast of their cash flow.

The new offering is the latest innovation from U.S. Bank’s Business Essential suite of banking and payments solutions.

U.S. Bank made its Finovate debut last year at FinovateFall 2021. At the conference, the bank demoed its Cards-as-a-Service (CaaS) technology.

U.S. Bank unveiled a new solution to enable small business owners to see a 90-day forecast of their cash flow. The tool allows users to leverage external data from their clients along with their own U.S. Bank accounts to provide more comprehensive insights. The offering is designed to address what U.S. Bank Chief Digital Officer Irv Henderson called “a top concern for today’s business owners.”

“Giving our clients the ability to forecast their cash flow outlook, including, in the future, the capability to consider various scenarios, will provide them with vital information to make smart decisions for today and the future,” Henderson said.

U.S. Bank’s new cash flow tool gives users a 90-day historical view along with its forecast of account balances up to 90 days ahead. The bank plans to introduce additional functionality to enable users to build “what if” scenarios and observe the impact of those scenarios on future cash flow.

The tool is currently available to clients of U.S. Bank from their online dashboard. Part of U.S. Bank’s Business Essentials suite of banking and payments solutions, the cash flow tool is the bank’s latest effort to “bring together digital capabilities and the power of data” to provide small businesses with actionable insights, according to Henderson.

U.S. Bank made its Finovate debut a year ago at our all-digital FinovateFall 2021 conference. At the event, the Minneapolis, Minnesota-based bank demonstrated its Card-as-a-Service (CaaS) technology that enables companies to extend corporate credit digitally. With the touch of a button, virtual cards -with precise spend limits, tokenization, and encryption – can be pushed to users’ mobile wallets in real time. The Card-as-a-Service solution also gives businesses the ability, via API integration, to build custom virtual payment experiences in their ecosystem.

The parent company of U.S. Bank National Association, U.S. Bancorp serves millions of customers through a range of businesses including consumer and business banking, payment services, corporate and commercial banking, wealth management, and investment services. The institution has $591 billion in assets as of June 2022.

Clients that use U.S. Bank’s prepaid Focus Card for payroll can offer their employees access to their wages as they earn them, thanks to a new partnership between U.S. Bank and Payactiv.

Employees will not only benefit from early access to their wages, but will also have access to Payactiv’s other financial wellness tools.

“We’re proud to be on the leading edge, developing a solution that helps our business clients provide additional convenient options for their employee payroll,” said U.S. Bank Payment Services Vice Chair Shailesh Kotwal.

U.S. Bank is partnering with financial wellness company Payactiv this week. Under the agreement, U.S. Bank will leverage Payactiv’s earned wage access (EWA) tools.

U.S. Bank’s commercial clients that use U.S. Bank’s prepaid Focus Card for payroll can enable their employees to access a portion of the wages they’ve already earned. Employees can access their funds on their U.S. Bank Focus Card, via an instant deposit into their checking account, or other payment options.

In addition to benefitting from early payouts, employees will have access to other financial wellness services such as savings and bill management tools, financial education, and a discounts marketplace.

“The future of payments is one where companies may soon say goodbye to the traditional, biweekly payroll,” said U.S. Bank Payment Services Vice Chair Shailesh Kotwal. “Employers recognize that providing employees on-demand access to earned wages improves employee satisfaction and recruiting efforts. We’re proud to be on the leading edge, developing a solution that helps our business clients provide additional convenient options for their employee payroll.”

Payactiv was founded in 2011 to help companies send their employees their wages as they earn them, as opposed to bi-weekly. “We provide timely access to liquidity – so a single mother can pay for daycare between paychecks and a healthcare worker can cover an unexpected car expense,” explained company CEO Safwan Shah.

California-based Payactiv has raised $134 million in funding and earned a Best of Show award for its 2016 demo. In 2020, the Consumer Financial Protection Bureau (CFPB) approved Payactiv’s EWA program as exempt from the federal Truth in Lending Act and Regulation Z rules governing creditors. “Employers can take comfort in knowing that PayActiv continues to be the leader in responsible EWA for employees,” Shah said at the time.

U.S. Bank has agreed to acquire San Francisco, California-based expense and travel management company TravelBank. Financial terms of the transaction were not disclosed, but one outlet, Skift, has said that the deal was valued at $200 million.

“We are focused on giving businesses more confidence, control, and convenience in managing payments and expenses,” U.S. Bank Vice Chair of Payment Services Shailesh Kotwal said. “TravelBank will help us accelerate these efforts.”

Founded in 2016, TravelBank offers an all-in-one solution for expense and travel management. Relying on a single platform, reporting model, and subscription price, TravelBank helps employees and businesses control and track expenses, automate traditionally manual processes, streamline both approvals and reporting, and remain compliant. With more than 20,000 customers, TravelBank claims to have reduced business travel spending by its clients by 30% on average, while simultaneously boosting employee morale with a user-friendly design and a travel rewards program. Ahead of this week’s acquisition, the company had raised $35 million in funding from investors including Dreamers VC and DCM Ventures.

“We created TravelBank to provide a single experience for expense reporting and travel management,” co-founder and CEO of TravelBank Duke Chung explained. “Our combined offering with U.S. Bank will be the most comprehensive expense, travel, and payment management solution in the industry.”

Skift further reported that Chung will “move over to the bank” post-acquisition, while TravelBank will continue to support its existing clients.

The acquisition is the fruit of a partnership between the two companies that extends back to September of 2020. In the fall of last year, U.S. Bank integrated TravelBank’s travel and expense management platform into its U.S. Bank Instant Card. The collaboration enabled program administrators to issue Instant Cards directly from their expense management platforms.

With nearly 70,000 employees and $567 billon in assets, U.S. Bancorp is the parent company of U.S. Bank National Association. Headquartered in Minneapolis, the bank serves millions of customers, both in the U.S. and around the world, with a variety of services including consumer and business banking, payments, corporate and commercial banking, wealth management, and investments.

U.S. Bank demonstrated its Card-as-a-Service (CaaS) solution at FinovateFall 2021 in September. The technology enables companies to leverage API integration to extend corporate credit digitally and create a custom virtual payment experience in their ecosystem.

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

U.S. BankCard as a Service (CaaS) empowers fintech partners or clients to extend corporate credit digitally and create a custom virtual payment experience in their ecosystem through API integration.

Features

Offers precise spend limits, tokenization, and encryption

Cards can be pushed to users’ mobile wallets in real time, with a touch of a button

Provides extensive controls around card security and fraud

Why it’s great U.S. Bank serves millions of customers around the world and is known for creating innovative ways for customers to bank how, when, and where they prefer.

Presenters

Jon Zimmermann, VP Product Development Zimmermann is a Vice President and Group Product Manager within the Corporate Payment Systems division of U.S. Bank. He is responsible for the U.S. Bank Instant Card and Card as a Service products. LinkedIn

Alex Hornbuckle, VP Product Development Hornbuckle is a Vice President and Senior Product Manager within the Corporate Payment Systems division of U.S. Bank. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

Join U.S. Bank and learn how to create and send virtual corporate cards in real time for immediate use.

Features

Provision a virtual corporate card in real time

Define card limit and expiration date

Push to a mobile wallet for secure payments

Why it’s great Learn how easy it is to extend corporate spending to the people who need it in real time, with full control and transparency using virtual cards and a mobile wallet.

Presenters

Laretha Hulse, VP Product Development Hulse is Vice President of Product Development for U.S. Bank Corporate Payment Systems. She led the design and launch of the first commercial mobile app and continues to champion mobile and digital payment solutions. She has over 15 years experience in the commercial payment industry working in the aviation, healthcare, payables, and travel verticals. LinkedIn

Jon Zimmermann, VP Zimmermann is a vice president and group product manager within the Corporate Payment Systems division of U.S. Bank. He is responsible for the U.S. Bank Instant Card and Card as a Service products. LinkedIn