This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Finovate’s Fintech Rundown is back with the fintech headlines you need to know as the working week begins!

We’ve got news of a funding in the consumer financing world, new products for financial wellness and credit trading, a collaboration in the money movement market and more. Be sure to check back all week long for the latest in fintech headlines.

Financial wellness

The US arm of BMO launches an new app developed by MSN Holding, DollarGPS, to help users improve their financial health.

Lending

Egyptian Buy Now, Pay Later firm Blnkraises $37 million in combined debt and equity funding.

TP ICAPunveils new credit trading and data platform, RealQ.

Credit intelligence platform OctusacquiresLevPro, a front-office software provider for public and private credit markets.

Agentic AI

Spend management software provider ExpensifylaunchesExpensify MCP, a new integration that enables AI assistants and other MCP-compatible clients to securely access Expensify data via natural language queries.

This week’s edition of Finovate Global looks at recent fintech headlines from the Eastern European nations of Bulgaria, Albania, and Hungary.

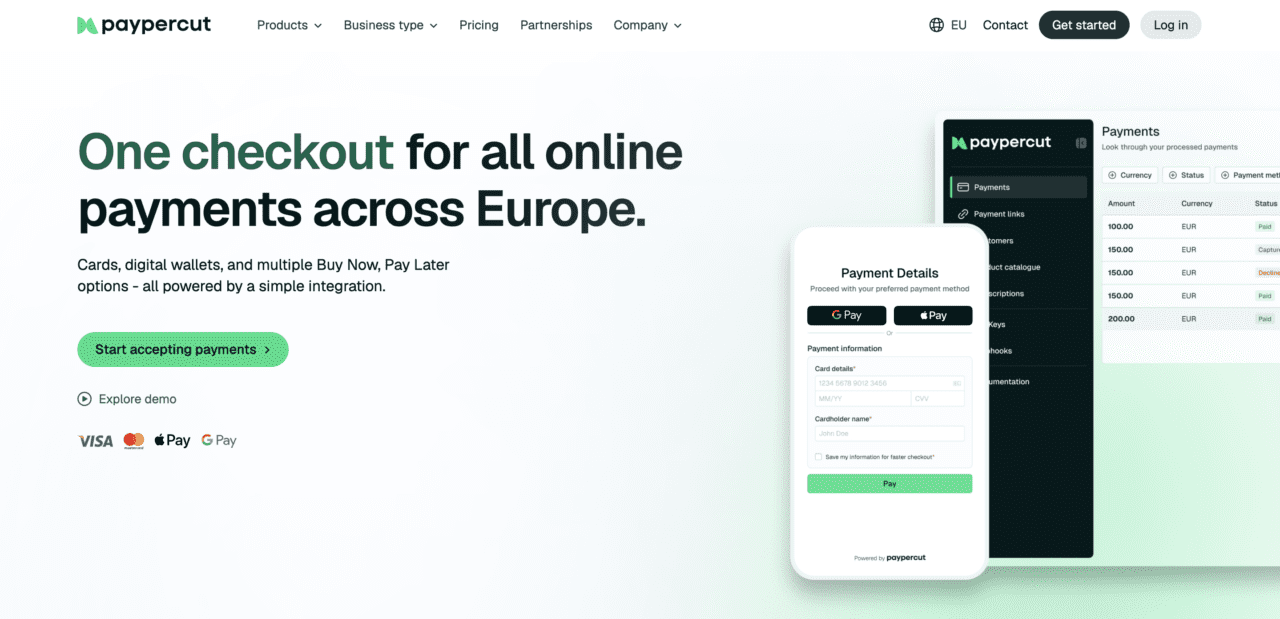

Bulgarian Fintech Paypercut Raises €5M

Paypercut, a fintech based in Sofia, Bulgaria, has secured €5 million in seed funding. The round was co-led by Concentric, Passion Capital, and Araya Ventures, and featured participation from additional investors including SMOK Ventures, Portfolio Ventures, BrightCap Ventures, BlackWood, SABAH.fund, MFG Invest, Main Set, and Matt Doka, a payment entrepreneur. Paypercut’s total funding now stands at €7 million.

Founded in response to the fragmentation of payments in Central and Eastern Europe, Paypercut has grown from a Buy Now, Pay Later aggregator into a more comprehensive payments platform. The company offers merchants access to card payments, local payment options, Buy Now Pay Later products, payment links, QR code payments, multi-currency settlement, and billing tools via a single integration. Paypercut raised €2 million in pre-seed funding in July 2025 and has onboarded more than 200 merchants in eight CEE markets since that time.

This week’s investment will help fuel Paypercut’s continued expansion across Central and Eastern Europe. The funding will also enable the firm to meet the capital requirements for an EMI license with the Central Bank of Ireland.

“CEE has always been treated as an afterthought by the payments industry, seen as too fragmented, too many local specifics, too complicated,” Paypercut Co-Founder and CEO Stoil Vasilev said. “We built Paypercut to fix that. This round gives us the resources to go further and faster: more markets, more payment options for merchants, and the infrastructure to move money in the way it should have always worked, instantly and at a fraction of the cost.”

In addition to its merchant payments operation, Paypercut is also developing stablecoin-based infrastructure for cross-border transfers in the region. The company will initially target high-volume corridors such as those between the Euro and the Polish Zloty (EUR-to-PLN) and the Euro and the Romanian Leu (EUR-to-RON).

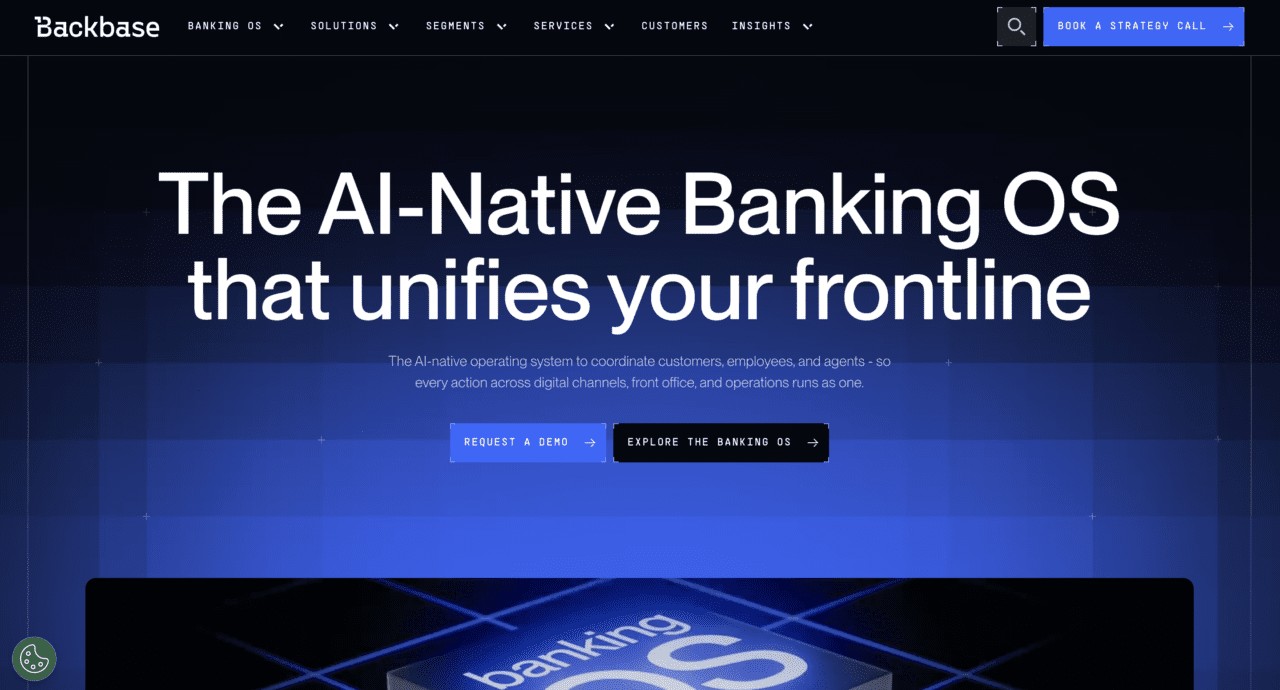

Albania’s Tirana Bank Goes Live with Backbase

Tirana Bank, named “Best Bank in Albania” in 2025 by Euromoney, has gone live with a “complete omnichannel retail banking experience” built on the Backbase AI-native Banking OS. The launch covers accounts, deposits, online loan and credit card applications, internal and outgoing transfers, card management, billpay, and financial insights. Tirana Bank will also enable Digital Assist in the employee app.

“This launch marks a significant step in our digital transformation journey, as we continue to invest in solutions that bring real, everyday value to our customers. TiBank+ is designed to deliver a seamless and intuitive banking experience, combining convenience with the trust and human connection that define our model,” Tirana Bank Chief Retail Business Officer Lila Canaj said. “Through our partnership with Backbase, we have accelerated this transformation, bringing to market a modern and scalable platform built to evolve with our customers’ needs.”

One feature that Tirana Bank anticipates its customers will appreciate is real-time spending insights, courtesy of Backbase’s personal finance management capabilities. Offering customers these insights is not a common occurrence in the region and will help Tirana Bank differentiate itself from its competitors. The institution is also going live with Apple Pay, becoming one of the few Albanian banks to offer the service via a mobile app.

“Albania is on its path to EU membership, its government has made digitalization a national priority,” Backbase Regional Vice President for South East Europe Robert Mihaljek said. “Tirana Bank looked at that moment and decided to lead it. They came to us with a clear ambition. Twelve months later, they are live with not only an MVP but a full retail APP. This is a first for Albania, and a reference for the Balkans.”

A four-time Finovate Best of Show winner, Backbase has been a Finovate alum since 2009. The Amsterdam-based fintech offers an AI-native banking operating system that converts fragmented banking operations into a unified frontline for the benefit of customers and employees alike. Founded in 2003, Backbase counts more than 150 leading banks and financial institutions around the world as users of its solutions for retail, small business, commercial, and private banking, as well as wealth management. Riddhi Dutta is CEO.

Can Crypto Make a Comeback in Hungary?

For many observers, liberal democracy was one of the big winners in the recent Hungarian election that saw the end of the Orbán regime. But could the victory of Péter Magyar and his pro-EU Tisza Party also be a good sign for crypto and digital assets in the country?

In 2025, Hungary announced an amended Crypto Act that criminalized unauthorized exchange services and established a validation regime on all crypto-to-fiat and crypto-to-crypto transactions. This incentivized some firms, such as Revolut, to withdraw from the Hungarian market entirely, while others suspended services due to regulatory uncertainty.

This also set off a confrontation with the EU, with the European Commission initiating infringement proceedings against Hungary’s validation regime, saying that it was in conflict with the EU’s MiCA framework. Interestingly, Orbán had previously been relatively pro-crypto, with his regime offering some of the lowest tax rates on crypto in Central Europe. This made Hungary—at least before 2025—an attractive jurisdiction for retail crypto investors in the region.

There are many reasons offered to explain the shift toward a more restrictive attitude in recent years—from the influence of MiCA and its mandates to the regime’s well-known preference for state control and supervision of key financial and industrial activities. But the question now is whether or not new politics will result in new policy? The correct answer, at this point, is that no one knows. What some observers have noted, however, is Magyar’s relatively more pro-EU stance on other issues and his general interest in re-aligning with European institutions more broadly. To this end, even something as straightforward as revising the country’s crypto policy to match MiCA’s mandates—and remove or revise current criminal penalties for policy violations— might be an initial positive sign toward restoring crypto’s status in Hungary.

Here is our look at fintech innovation around the world.

Central and Southern Asia

India travel fintech Scapia, which combines co-branded cards with travel booking, secured $63 million in funding in a round led by General Catalyst.

Raqami Islamic Digital Bank Limited (RIDBL) has been granted a Retail Banking License by the State Bank of Pakistan.

Via its Alipay+ gateway, Singapore’s Ant International announced the launch of cross-border mobile payment services in Latin America.

ACI Worldwide looked at the impact of real-time payments on growth in Peru, Chile, and Argentina.

Tearsheet profiled Brazilian digital financial institution Agibank.

Asia-Pacific

Singapore-based Crypto payments network Moonpay and controlling shareholder Seoryong Electronics announced a joint investment in Korean fintech Finger.

Vietnam Bank OCB selectedBackbase AI lead Chris Shayan as its Acting CEO.

African financial infrastructure company Anchor launched its Anchor MCP Server, becoming the first Nigerian fintech to make. its API documentation natively available to AI systems.

The Africa Report reported on the rise of mobile money in Ghana and how it is challenging the country’s incumbent banks.

Business Insider Africa looks at the fate of small business banking platform Brass which announced that it will be migrating its customers to Paystack Microfinance Bank.

Central and Eastern Europe

PayPalintroduced a pair of Buy Now, Pay Later products for its customers in Austria.

Ripplelaunched its RLUSD stablecoin in Turkey courtesy of partnerships with local platforms BiLira, Bitexen, and Bitlo.

Equifax UK forged a partnership with Polish credit bureau BIK to boost access to identity verification and fraud prevention technology.

Middle East and Northern Africa

Saudi Arabia-based fintech Stitch announced a pivot to focus on infrastructure and offering a financial operating system for banks.

UAE-based fintech Comfi AI secured pre-Series A funding from Yango Group’s Yango Ventures.

If you’re in the US, you may be pouring an extra cup of caffeine after an activity-filled long weekend. While you were away, however, the rest of the fintech world kept moving. This week, we’ll continue to add more announcements as the week progresses.

Payments

Marqetaexpands account and money movement offering in Europe, building on strong regional momentum.

This week’s edition of Finovate Global reviews recent fintech news and headlines from Thailand.

DV8 Public Company to Acquire Rakkar Digital

Pending regulatory approvals, DV8 Public Company has announced plans to acquire Rakkar Digital, a digital asset custody provider, and invest up to $3 million (THB100 million) in the firm. DV8 has inked a share sale and purchase agreement to buy Rakkar’s ordinary shares from its existing shareholders. The transaction marks DV8’s latest entry into regulated digital asset operations. The company invested in Korean digital asset treasury platform Bitplanet in 2025.

Rakkar Digital was established in 2022 as a joint project between SCBX, the parent company of Siam Commercial Bank, and Fireblocks, a global digital asset infrastructure provider. Headquartered in Singapore, Rakkar Digital provides institutional-grade digital asset and cryptocurrency custodian services and has more than $700 million in assets under custody. In a statement, DV8 noted that Rakkar Digital’s regulatory standing, operational framework, and trust among institutional customers made the company a wise acquisition and will help DV8 compete in Asia’s rapidly growing digital asset ecosystem.

Founded in 1978, DV8 Public Company is a media and advertising agency based in Bangkok, Thailand. Formerly known as Demeter Corporation Public Company Limited, the company rebranded in 2020 and is currently transforming itself into a builder of regulated digital asset infrastructure. DV8 announced this pivot last summer, appointing Thai business leader Chatchaval Jiaravanon as its new Chairman and raising approximately $7.4 million (THB 241 million) in funding.

Mastercard and Krungthai Complete Agentic Transaction in Thailand

Mastercard announced that it has completed a pilot project in Thailand to deliver its first authenticated agentic transaction in partnership with Krungthai Card Public Company Limited (KTC). The project featured Mastercard Agent Pay and was initiated by AI agents in a secure, transparent pilot environment with full consumer control. The transaction used tokenized credentials, authenticated by Mastercard Payment Passkeys, to provide customer verification and data protection.

“AI-driven innovation in payments marks a significant step forward for the financial industry,” Krungthai Card President and CEO Pittaya Vorapanyasakul said. “Our collaboration with Mastercard reflects our strategic commitment to integrating agentic commerce into KTC’s ecosystem—enabling smarter, more secure, and intuitive experiences for consumers. This milestone reinforces our role in advancing payment innovation in Thailand.”

The pilot project demonstrated how AI can complete everyday tasks for consumers safely and efficiently. In this instance, an AI agent booked transportation from Suvarnabhumi airport to Central Chidlom via global mobility provider Elife. Both the booking and the agentic transaction were facilitated by the AI agent, which was connected to Elife’s services network.

Thailand is the latest country where Mastercard has tested its innovations in agentic commerce. So far in 2026, the company has completed authenticated agentic transactions in Australia, New Zealand, Singapore, Malaysia, India, South Korea, Taiwan, and Hong Kong.

“Thailand continues to be one of the region’s most attractive travel destinations, and its dynamic travel environment provides an ideal, real-world testbed for agentic commerce,” Mastercard Country Manager for Thailand and Myanmar Winnie Wong said. “Through this collaboration with Krungthai Card (KTC), Mastercard’s first partner in Thailand to test agentic AI transactions, consumer-authorized AI agents can help make travel experiences more seamless, while embedding trust, authentication, and security directly into payments.”

KTC is a major Thai financial services provider that specializes in credit cards, personal loans, and other payment services. Founded in 1996, the company is headquartered in Bangkok.

Wise Secures Licenses for Wallet and Card Services in Thailand

International money transfer innovator Wise (formerly TransferWise) has obtained five licenses that will enable the firm to offer banking and financial services in Thailand. The UK-based company is the first non-bank to secure five licenses in the country: an electronic money service license, an electronic fund transfer license, an authorized money transfer agent license, an authorized electronic money business operator license (also known as an FX e-Money License), and a foreign business license.

These licenses reflect the relatively complex nature of Thailand as a market for international payments. However, the effort is likely to prove worthwhile. Thailand one of the most internationally connected economies in Southeast Asia, and the APAC region is an especially important one for Wise, accounting for 20% of the fintech’s global revenue.

“Thailand’s cross-border payments market has long been dominated by traditional banks, and Wise is bringing a faster, more transparent alternative,” Wise Head of Banking and Expansion for APAC SK Saraogi said. “With these licenses, customers will soon be able to manage money seamlessly whether they are sending it abroad or using it locally. Beyond Thailand, we see strong demand for our products across APAC and will continue to increase our regulatory footprint to bring our products to even more customers.”

A Finovate alum since 2013, Wise is an international fintech specializing in global money movement and management. Launched in 2011 as “TransferWise” by Kristo Käärmann and Taavet Hinrikus and headquartered in the UK, Wise supported more than 15 million individuals and businesses with its fund transfer services in fiscal 2025. The company processes £9 billion in cross-border transactions every month, saving customers around £1.5 billion a year.

Here is our look at fintech innovation around the world.

Asia-Pacific

Mastercardcompleted a pilot project that delivered the first authenticated agentic transaction in Thailand with Krungthai Card Public Company Limited.

Australian Payments Plus agreed to sell its payments app Beem to Bolt Group.

StraitsX and KBank established real-time payments between Singapore and Thailand.

Sub-Saharan Africa

African fintech Moniepoint acquired Sumac Microfinance Bank, accelerating its entry into the Kenyan market.

Paytech Flutterwave announced plans to establish a regional hub in Anambra, in the southeast part of Nigeria, to help target small businesses.

The Fintech Times reviewed Ghana’s fintech ecosystem.

Payment orchestration platform MoneyHash inked a new partnership with Bahrain-based Eazy Financial Services.

The Times of Israel looked at the current state of fintech investment in Israel.

Central and Southern Asia

Indian lending platform KreditBee achieved a valuation of $1.5 billion after raising $280 million in new funding.

A merger between CityPay and Chhito Paisa is expected to bolster Nepal’s fintech sector.

Glaas, an India-based embedded credit infrastructure company, raised $5 million in funding from Devesh Sachdev, who joined the company as co-founder and managing director.

Latin America and the Caribbean

Stablecoin issuer and infrastructure company Balboa Corporation launched in Panama.

This week’s edition of Finovate Global highlights recent fintech headlines from Saharan and sub-Saharan Africa.

Circle and Sasai Fintech team up to boost adoption of USDC

Digital asset platform Circle announced a new partnership between one of its affiliates and Sasai Fintech, a business of Cassava Technologies. The partnership is designed to boost adoption of Circle’s USDC stablecoin and expand internet-native financial infrastructure across Africa.

“Africa’s digital economy is entering a new era, propelled by entrepreneurship, a mobile-first generation, and the acceleration of intra-regional trade,” Cassava Technologies Founder and Executive Chairman Strive Masiyiwa said. “By integrating with the trusted and widely adopted USDC network, we can drive financial inclusion and open transformative opportunities for businesses and consumers alike.”

Stablecoin adoption in Africa is accelerating due to increases in the number of mobile-first consumers, the growth of cross-border commerce, and the overall expansion of the digital economy. USDC is a fully-reserved, transparent payment stablecoin redeemable 1:1 for US dollars. The stablecoin has been used to power programmable payments and financial applications around the world. This week’s partnership announcement between Circle and Sasai Fintech calls for further exploration into practical applications for USDC. The two companies will also investigate ways that Circle’s full stack platform can lower costs, friction, and settlement time for Sasai’s enterprise and retail customers.

“Emerging markets are at the forefront of stablecoin adoption, and Africa represents a significant opportunity for internet-native innovation,” Circle Co-Founder, Chairman, and CEO Jeremy Allaire said. “Working with Cassava, we can extend the benefits of USDC and on-chain infrastructure into high-growth payment corridors to deliver always-on global connectivity.”

Sasai Fintech is a pan-African digital payment solutions provider. Headquartered in Johannesburg, South Africa, and founded in 2021, Sasai Fintech has enabled more than 250 million wallets and more than 85,000 POS terminals. A division of Cassava Technologies, Sasai Fintech has 20+ enterprise partners and is active in 30+ cross-border markets.

IFC Partners with Cashi to expand digital payments infrastructure

International Finance Corporation (IFC) has teamed up with digital payment infrastructure company Cashi. The fintech offers a digital payment platform that allows users to send and receive money via mobile phones, point-of-sale devices, and SMS-based tools. Cashi’s platform links users with banks, telecoms, and other financial institutions in a single interoperable ecosystem that makes everyday transactions easier in an economy that still relies heavily on cash and faces significant obstacles to accessing comprehensive banking services.

“IFC’s upstream support allows us to adapt our proven, crisis-tested platform to the realities of central Africa,” Cashi CEO Tarneem Saeed said. “This partnership enables us to work closely with regulators and ecosystem partners, build trust with local merchants, and deliver practical financial tools that people can use in their daily lives, even in low-connectivity environments.”

Cashi’s platform helps address and alleviate digital infrastructure bottlenecks in economies that are cash-dependent and underbanked. The company offers a range of financial products and services that enable businesses and individuals to send, receive, and spend money. Cashi offers instant settlement, reliable uptime, and dedicated support for both merchants and users. Founded in 2022 and headquartered in Khartoum, Sudan, Cashi operates as part of Alsoug.com, the country’s largest digital classifieds and marketplace.

Financial infrastructure startup Littlefish raises $9.4 million

A South African fintech infrastructure startup, littlefish, has scored $9.4 million in Series A funding. The round was led by Partech, and featured participation from TLcom Capital, Flourish Ventures, and Proparco. The investment is the latest fundraising for the company since its 2021 seed round, and the firm expects to use the new capital to grow its team, advance product development, and enter new markets such as Kenya, Tanzania, Uganda, Botswana, Zimbabwe, and Zambia.

“This raise is a validation of our belief that the best way to serve Africa’s small businesses is to work with the institutions they already trust, not around them,” Brandon Roberts, Co-Founder and CEO of littlefish, said. “We’ve proven the model in South Africa, and this capital gives us the runway to deepen those relationships and bring what we’ve built to millions more merchants across the continent. The little guys deserve world-class financial infrastructure, too, and we’re building it.”

Littlefish offers a merchant operating system that empowers banks to deliver fintech products and services to small businesses by integrating payments, POS software, CRMs, APIs, and more into a unified layer. This enables banks and other financial institutions to offer modern, digital services to merchants without disrupting their existing relationships with customers. Littlefish helps banks deliver more services to their business customers more efficiently, and gives small businesses the opportunity to gradually modernize and digitize their operations.

Littlefish counts institutions such as Standard Bank, First National Bank, and Absa among its clients. The company was co-founded in 2021 by Roberts and Miod Davith Kahwa.

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Mexico-based digital commerce platform, Clip, introducedTap to Pay functionality on the iPhone.

Mastercardexecuted a series of live, end-to-end agentic payment transactions across Latin America and the Caribbean.

Cross-border payments technology company Reap obtained a Money Transmitter Registry in Mexico.

Asia-Pacific

Singapore-based fintech Fingular unveiled Shariah-first digital financing brand in Malaysia, Tazee.

Enterprise on-chain settlement infrastructure company Capital Layer forged a distribution partnership with Taiwan-based domestic system integrator Stark Technology Inc.

Vienamese police dismantle fraudulent cryptocurrency scheme that cost investors billions of dollars.

Sub-Saharan Africa

Operating system for African banks and merchants, Littlefish, raised $9.5 million in Series A funding.

Western Union partnered with Sasai Fintech to bring digital remittance access to South African consumers.

Mastercard is acquiring stablecoin infrastructure provider BVNK for up to $1.8 billion to bridge fiat and on-chain payments within a single network.

The deal positions Mastercard to connect cards, bank rails, stablecoins, and tokenized deposits to create a unified, multi-rail payments ecosystem.

While competitor Visa relies on a partnership-led approach to stablecoin integration, Mastercard is seeking to own the infrastructure layer outright.

Mastercard is making a move to own the rails that bridge stablecoins and fiat this week. The payments giant is acquiring stablecoin infrastructure provider BVNK for up to $1.8 billion, including $300 million in contingent payments.

The announcement comes at a time when the current stablecoin market capitalization exceeds $316 billion, a figure that is up 2.5x from 2023. It also comes as users across the globe are increasingly open to holding stablecoins. In a recent survey of over 4,000 stablecoin and crypto holders, BVNK found that 56% of participants expressed plans to acquire more stablecoins within the next 12 months.

This increased utility of stablecoins is creating a need in the traditional financial space as users require a bridge between fiat and stablecoins. As a result, banks and fintechs need to offer their customers payment options enabled by stablecoins and tokenized deposits.

Mastercard anticipates that acquiring BVNK’s stablecoin infrastructure will allow it to become the bridge between fiat and stablecoins. The company will connect stablecoin rails to its own network to offer consumers the accessibility and interoperability they have come to expect in the traditional finance realm.

“We expect that most financial institutions and fintechs will in time provide digital currency services, be it with stablecoins or tokenized deposits. We want to support them and their customers with a best-in-class, highly compliant, interoperable offering that brings the benefits of tokenized money to the real world,” said Mastercard Chief Product Officer Jorn Lambert. “This acquisition reinforces what we have always done, using innovation and technology to power economies and empower people. Adding on-chain rails to our network will support speed and programmability for virtually every type of transaction.”

Mastercard isn’t the first traditional card network making a move to establish a foothold in the stablecoin space. Visa has formed partnerships with Circle and Bridge to support USDC payments and enable on-chain settlement flows. Mastercard, however, is taking things a step further. Instead of relying on a partnership-led approach, the network giant is acquiring the stablecoin infrastructure outright. Bringing the infrastructure in-house will allow Mastercard to connect traditional finance, on-chain assets, and enterprise payment flows within a single network.

BVNK was founded in 2021 and currently processes over $25 billion each year on behalf of enterprises and payment service providers. The UK-based company leverages stablecoins to enable businesses to move value instantly across borders and networks. Through its partnerships with global licensing bodies and Tier 1 banks, BVNK serves clients such as Worldpay, Deel, and dLocal.

“This partnership is about complementary strengths: Mastercard brings 200+ countries and territories, institutional trust and settlement rails. BVNK brings proven stablecoin infrastructure, deep expertise and an enterprise customer base,” said BVNK Co-founder and CEO Jesse Hemson-Struthers in a post on LinkedIn. “More trust attracts more users. More users attract more businesses. More businesses attract more developers. And suddenly, moving money on stablecoin rails becomes as routine as moving money on traditional rails—accessible to everyone.”

Once the acquisition is finalized later this year, Mastercard will be able to offer a single network to connect cards, bank rails, stablecoins, and tokenized deposits. The new, multi-rail approach will let customers choose the solutions that work best for them without tying them down to a single platform.

“This deal brings together complementary capabilities to define and deliver the future of money,” said Hemson-Struthers. “Together, we’re able to deliver an unprecedented infrastructure for digital currency-based financial services.”

Mastercard is launching a Virtual C-Suite for small business customers this week, introducing agentic AI agents that act as digital executives to provide strategic insights and decision-making support.

The new Virtual C‑Suite is a set of agentic AI-powered tools that are specifically focused on small and medium-sized businesses, which represent roughly 90% of enterprises across the globe and more than half of global employment. By introducing AI agents that mimic executive roles such as CFO, Mastercard is aiming to close the gap between the resources available to large enterprises and those accessible to small businesses.

Mastercard is using its vast experience in payments, data, and security to bring a deeper understanding of how a customer’s money moves. Virtual C-Suite brings intelligence into small businesses’ accounting systems, business software, and banking applications to analyze business performance, identify risks and opportunities, predict likely outcomes, and recommend actions. The tool relies on insights from the billions of transactions processed on Mastercard’s network annually, combined with a business’ financial activity to provide relevant, trusted recommendations on how businesses pay, get paid, and manage working capital.

“Small businesses are the cornerstones of communities, but it’s easy for owners to lose sight of the passions that inspired them when they’re buried in spreadsheets and stretched across multiple roles,” said Mastercard Global Head of Small and Medium Enterprises Mark Barnett. “We hear these pressures from entrepreneurs every day. With Virtual C-Suite, we are bringing the innovative technology, quality data at scale, and strategic expertise usually available to large enterprises to small business owners. Our goal is to turn operational complexity into clarity—helping entrepreneurs regain time, make smarter decisions, and translate their ambition into measurable growth.”

After integrating the new tool, business users and their teams will have access to dashboards and natural language conversational platforms through which they can ask agents direct questions about their accounts, trends, or recommended actions.

Virtual C-Suite will initially launch with a Virtual CFO capability. Mastercard will make additional executive-function roles over time, delivered through financial institutions, accounting platforms, and software providers.

The launch is part of Mastercard’s broader push into agentic AI. The company’s Virtual C-Suite is an advancement beyond basic analytical capabilities, recommending and executing actions across the commerce lifecycle. The new offering highlights how payments networks are adding value by bringing AI intelligence layers to small businesses, combining transaction data with agentic AI to deliver financial insights that traditionally required dedicated finance teams.

Virtual C-Suite’s small business focus is among a series of Mastercard’s recent initiatives aimed at SMEs. In 2024, the company introduced Biz360, a platform designed to help entrepreneurs consolidate and manage the digital tools they rely on to run their operations. Mastercard also rolled out Small Business Navigator to connect business owners with productivity services and remote talent resources, and introduced an SME credit card with built-in cybersecurity protections to help small businesses defend against growing digital threats.

Welcome to March! Women’s History Month, Holi (the Hindu “Festival of Colors”), the start of spring, St. Patrick’s Day, Eid al-Fith, Cesar Chavez Day … there’s a lot to celebrate and look forward to over the next few weeks.

Here on Finovate’s Fintech Rundown, we’re looking forward to the rush of industry news and announcements that typical comes with the seasonal thaw.

Payments

Private equity firm Incore Invest completes its acquisition of CoreOrchestration AB from Worldline.

Appleis in conversation with banks in India to bring Apple Pay to the country later this year.

The Hong Kong Monetary Authority (HKMA), the Shanghai Data Bureau (SDB), and the National Technology Innovation Center for Blockchain ink a Memorandum of Understanding between Shanghai and Hong Kong to apply blockchain technology to develop a cross-border platform to facilitate trade finance.

2026 begins in earnest today as the first full working week of the year gets underway. Be sure to check in with Finovate’s Fintech Rundown over the next few days to get you up and running with the latest in fintech news and announcements!

Universal Exchange (UEX) Bitgetopens its TradFi trading suite to all users.

TradeStationunveils the upcoming launch of TITAN X, its next generation of its flagship trading platform designed for active traders.

Crypto and DeFi

Telcoin, a digital asset bank that just won final charter approval from the Nebraska Department of Banking and Finance, launches its eUSD stablecoin.

Kast, a financial platform built on stablecoin rails, expands global payouts to 11 new local currencies including GBP, EUR, and CAD, as well as a multiple currencies in the Asia Pacific region.

This week’s edition of Finovate Globallooks at recent fintech headlines from South Africa.

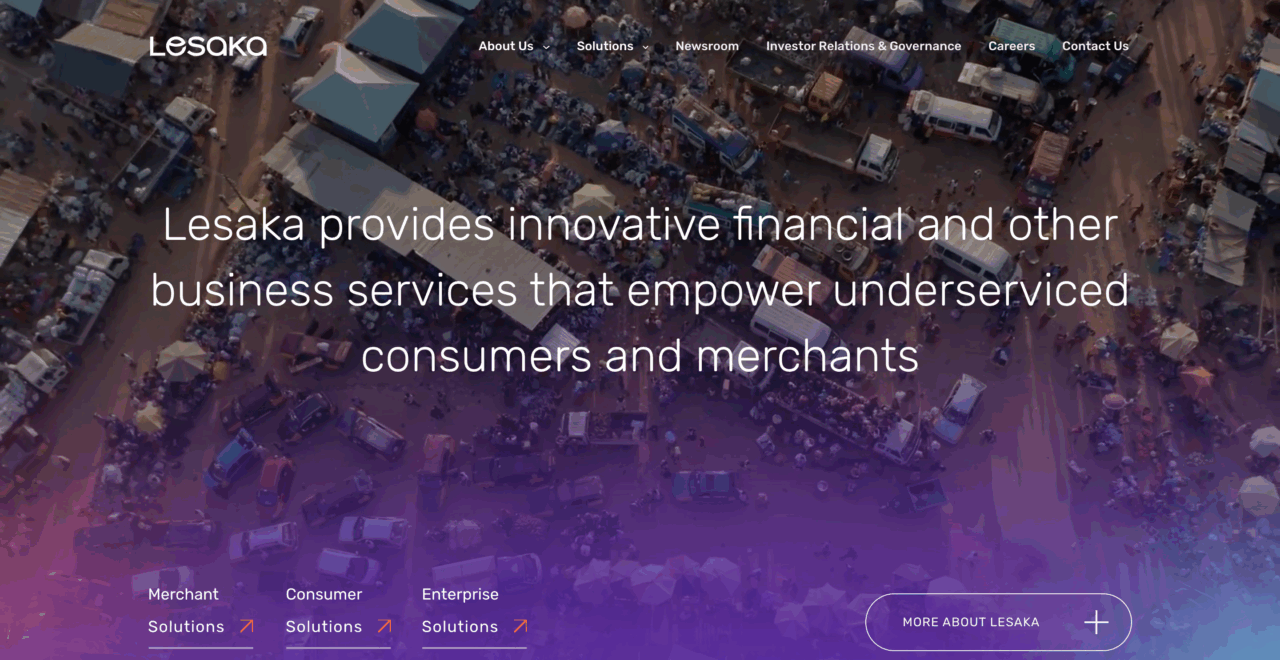

Lesaka Technologies to Acquire Bank Zero

Lesaka Technologies, a fintech that provides low-cost financial services to underbanked South Africans, has secured approval from the Competition Commission to acquire Bank Zero. An app-only bank co-founded by Michael Jordaan in 2018 and publicly launched three years later, Bank Zero today has more than 40,000 funded accounts and deposits of more than $22 million. The financial institution offers personal and business banking solutions to both underbanked and tech-first customers.

Initially announced in July, the acquisition is valued at $60 million. The transaction consists of a combination of newly issued shares in Lesaka and up to $5 million in cash. Post-transaction, Jordaan will remain as Bank Zero’s chairman, and co-founder Yatin Narsai will continue to serve as CEO. Bank Zero’s entire management team will also remain in place.

Lesaka anticipates that the acquisition will fortify its balance sheet, enhance lending performance, and reduce the firm’s dependence on bank debt. The fintech suggested that the move could lower its gross debt by $57 million.

“The acquisition of Bank Zero is a transformative event in Lesaka’s journey, enabling us to better serve our consumers, merchants, and enterprise clients, by embedding a trusted, well-engineered neobank capability into our fintech platform,” Lesaka Chairman Ali Mazanderani said. “I am delighted to welcome the Bank Zero team to Lesaka as partners.”

Lesaka Technologies offers banking, lending, and insurance products to consumers and cash management, billpay, business funding, and card acquiring solutions to retail merchants in both the formal and informal sectors. Founded in 1997, the company is headquartered in Johannesburg, South Africa.

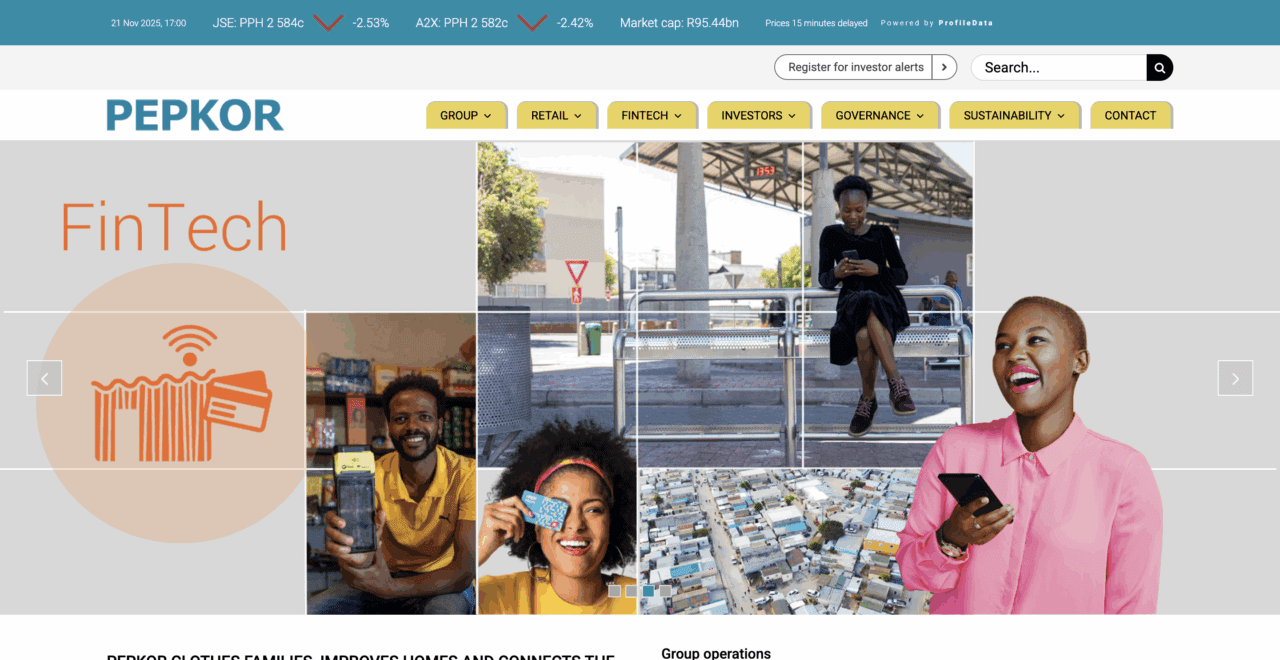

South African Retailer Explores New Banking Venture

One of South Africa’s largest discount retail groups may be getting into the banking business.

Pepkor Holdings operates more than 5,800 stores across a wide number of brands including PEP, Ackermans, and Tekkie Town. A subsidiary of Steinhoff International, Pepkor is reportedly looking to launch a new banking venture—informally referred to as “Pep Bank”—that will leverage the company’s market reach to offer zero-fee banking to millions of consumers with lower incomes. The company is said to be in conversation with Investec, seeking a partner to support the new bank’s regulatory, operational, and financial infrastructure.

There has been no public commentary from Pepkor on the initiative, and press reports assert that the talks are in “early stages.” Further, the launch of a new bank would require approvals from the South African Reserve Bank (SARB) and the National Credit Regulator, and no such engagement has been reported to date.

Speaking of launching banking operations in South Africa, Revolut announced that it has officially begun the process of securing a banking license in the country. The company has confirmed that it submitted a Section 12 application under the country’s Banks Act, the first step in becoming a licensed bank in South Africa. Revolut first signaled its intention to launch a bank in South Africa in September, highlighting the country as a “key growth market” with increasing rates of digital adoption and an openness to innovative financial products and services.

“Becoming a licensed bank will allow us to bring a full suite of products to the market and ensure we become the go-to financial app for millions of South Africans,” Revolut South Africa CEO Jacques Meyer said.

As a sign of the company’s growing engagement with the South African market, Revolut has appointed Dr. Gaby Magomola as Chairman of Revolut South Africa. A pioneer in the history of banking in South Africa, Dr. Magomola has served in senior executive roles at Citibank, Barclays Bank, First National Bank, and African Bank. He most recently served as Deputy Chairman of the Development Bank of Southern Africa (DBSA).

“Dr. Magomola’s experience is invaluable as we deepen our commitment to the South African market,” Meyer said. “His strategic counsel will be critical in navigating the local regulatory environment, ensuring we build a locally relevant service that addresses the financial needs of all customers in South Africa.”

Revolut’s presence in South Africa would bring significant additional competition to the country’s digital bank industry, which consists of TymeBank, Discovery Bank, and Bank Zero, which has been acquired by Lesaka Technologies, as we noted in this week’s column. Already one of the largest digital banks in the world, Revolut has said its expansion in South Africa is part of the company’s goal to grow its customer base from 65 million to 100 million by 2027. Revolut also seeks to be active in 30 markets by 2030.

Here is our look at fintech innovation around the world.

Asia-Pacific

Japan’s largest trust bank, Sumitomo Mitsui Trust Bank, selected SCSK Corporation and OneSpan to enhance security for its mobile banking operations.

Australian superannuation fund Brighter Super partnered with Napier AI to enhance its compliance infrastructure.

Is Jack back? South China Morning Post featured Alibaba Group Holding founder Jack Ma’s return to the campus of Ant Group.

Sub-Saharan Africa

South African fintech Lesaka Technologies received approval to acquire Bank Zero in a deal valued at $60 million.

Revoluthas applied for a banking license in South Africa.

South Africa’s Discovery Bank announced new crypto trading offering.

Central and Eastern Europe

Lithuanian regtech iDenfy unveiled its new solution that conduct instant license checks during the KYC process.

The European Payments Initiative (EPI) announced that Wero for e-commerce is now live in Germany.

Mastercardintroduced open loop transit payments in Azerbaijan.

Middle East and Northern Africa

Crypto payments company MoonPay expanded its partnership with Israel-based Zengo Wallet. The firm’s venture arm, MoonPay Ventures, also announced a strategic investment in the self-custodial crypto wallet.

First Abu Dhabi Bank teamed up with Thunes to enable global mobile wallet payouts.

Yuze Digital, a AI-powered fintech platform for freelancers and independent businesses, launched its pilot in India.

Pakistani fintech Abhi partnered with UAE-based digital platform Numou to help SMEs access financial services.

Indian fintech Yubi raised $46.4 million to enhance its debt marketplace, collection systems, and AI capabilities.

Latin America and the Caribbean

Uruguay-based cross-border payment platform dLocal partnered with global payouts orchestration company PayQuicker to help the firm serve more merchants in emerging markets.

Latin American accounts receivable management and collections automation platform Moonflow acquired Mexican fintech Kobro.

Dutch insurtech RISK has acquired Amsterdam-based savings app Dyme. Terms of the transaction were not disclosed. The deal will enable Dyme to boost its presence in the Netherlands as well as enter the German market. Courtesy of the agreement, both Dyme’s brand and management team will remain intact.

“From being featured on Dragon’s Den to becoming one of the largest finance apps in Europe and reaching profitability, our mission has always been the same: helping people take control of their money,” Dyme noted on its LinkedIn Page. “This step opens up some great opportunities for Dyme and its customers: expand the product, especially with great insurance packages and service, reach millions more people through the RISK ecosystem, and take Dyme international, beginning with Germany.”

Dyme currently has more than 600,000 consumers who have linked their bank accounts to the Dyme platform. The company’s app serves as a personal financial assistant to help users lower costs, and uses smart algorithms to automate subscription cancellations and provide financial guidance. Dyme announced its first profitable quarter in 2024, and has said that it has helped users save more than €40 million since inception. The acquisition will combine RISK’s market expertise and technological platforms with Dyme’s user-friendly financial solutions that enable users to easily manage their expenses, budgets, and more.

RISK offers an advanced IT platform, SureBase, that assists financial advisors, online labels, and insurers in product comparison and distribution. SureBase, according to RISK CEO Harm Vollmuller, will serve a key base for the new synergy between RISK and Dyme. “By combining that with our platforms and market knowledge, we can reach people at a time when financial breaking space is more important than ever,” Vollmuller said.

“This new facility is a testament to the trust and confidence Brand New Day Bank has placed in Factris and our vision for SME financing,” Factris CEO Brian Reaves said. “As we continue to scale across Europe, this partnership ensures we can meet the increasing demand for alternative financing and provide SMEs with the liquidity they need to thrive.”

Founded in 2017 and headquartered in Amsterdam, North Holland, Factris specializes in invoice factoring for small and medium-sized enterprises. The company offers selective factoring to enable companies to decide which specific invoices to factor, fund availability within 24 hours of invoice submission, credit insurance to protect against customer non-payment or bankruptcy, and debtor management for collections and account receivables.

Brand New Day Bank is a Netherlands-based digital-first, challenger bank and fintech that began operating in 2010. The financial institution serves both individuals and small-to-medium sized businesses with savings accounts, investment and pension products, tax-advantaged savings and investment solutions, and annuity payment services. Brand New Day Bank has more than €8 billion in assets.

Digital banking experience platform Plumeryannounced a suite of new features and integrations designed especially for credit unions in Canada. These new capabilities will give these institutions the ability to provide personalized, compliant, and modern digital banking experiences for their members.

The Amsterdam-based fintech leveraged a collaboration with Aequilibrium, a digital services and technology consultancy headquartered in Vancouver, British Columbia, to make sure its Canadian-ready platform is built based on the way that Canadian credit union members prefer to bank. This includes not just hyper-personalized, mobile-first, and intuitive digital journeys, but also support for everyday payments and transfers including billpay and Interact e-Transfers, and Canadian savings and lending products like GICs.

Plumery’s move comes as Canadian banks and credit unions face a range of challenges including evolving customer expectations, fintech competition, and the pressure to modernize their legacy systems. More immediately, Canadian credit unions are scrambling in the wake of Central 1 Credit Union’s announcement that it will wind down its digital banking platform Forge (formerly MemberDirect). More than 170 credit unions across Canada had been relying on the technology.

“With Forge winding down, Canadian institutions have a rare opportunity to modernize on their own terms, rather than being tied to outdated systems,” Plumery CEO and Founder Ben Goldin said. “Our platform provides an immediate, future-ready option that puts control back in the hands of credit unions. By working with Aequilibrium, we are combining global banking innovation with local expertise to deliver experiences that meet the unique needs of Canadian credit unions’ members.”

Founded in 2016, Plumery enables financial institutions to offer unique mobile and online experiences on top of either their modern or legacy core banking platforms up to 80% faster. Plumery’s technology features foundations that are pre-integrated into its digital banking journeys that accelerate app development and shorten time-to-market while maintaining complete control over both design and functionality.

India’s Bank of Baroda launched its eRUPI Person-to-Person (P2P) gifting solution.

TBC Uzbekistan extended financial services to non-residents.

Indian fintech Kiwi unveiled its interest-backed EMI on UPI.

Latin America and the Caribbean

Brazilian digital banking giant Nubank has applied for a US national bank charter.

Unlimit announced securing Principal Membership with Mastercard and Visa in Peru.

Brazi-based proptech Lastro raised $15 million in Series A funding in a round led by Prosus Ventures.

Asia-Pacific

Cambodian MSME-focused bank Chief Bank teamed up with payment solutions provider BPC to launch its new Chief Mobile 3.0 mobile app.

The People’s Bank of China opened a digital yuan operation center in Shanghai.

The Hong Kong Monetary Authority (HKMA) and the Hong Kong Science and Technology Parks Corporation (HKSTP) launched IADS Developer Hackathon to promote bank-fintech collaboration.

Mastercard Commerce Media has launched to leverage consumer-permissioned transaction data, giving 25,000 advertiser partners smarter targeting and delivering up to 22x ROAS across industries like retail, travel, and dining.

Mastercard’s partnerships with Citi, American Airlines, Microsoft, and WPP will expand scale, reach, and brand integration.

Retail media networks are surging, with spending projected to hit nearly $100 billion by 2028. Chase Media Solutions, which launched in 2024, is an example of how financial institutions are monetizing first-party data to serve personalized offers.

Mastercard announced that it will begin leveraging consumer-permissioned data via its new digital media network, Mastercard Commerce Media. The new media network will give Mastercard’s 25,000 advertiser partners access to transaction data from the 500 million enrolled consumers in order to power smarter, personalized commerce.

Through Mastercard’s proprietary Offers platform, advertisers can deliver tailored campaigns, such as cashback, discounts, and incentives, to audiences defined by their business goals. Using insights from consumer-permissioned data, Mastercard identifies the right customers and delivers relevant advertising content. Consumers can then activate offers on their enrolled card and complete the purchase, with Mastercard directly attributing the transaction to the campaign.

Beyond traditional cashback, Mastercard Commerce Media helps publishers strengthen brand loyalty by enabling programs where consumers earn rewards in a brand’s own cash currency, giving shoppers more purchasing power and brands deeper engagement. Looking ahead, Mastercard plans to expand distribution to new channels and deepen integrations across its broader services portfolio beginning in 2026.

Mastercard processed more than 160 billion transactions in 2024, and its new media network will deliver proprietary insights from transactions like these processed by Mastercard. Mastercard Commerce Media currently delivers a return on ad spend (ROAS) of up to 22 times for advertisers across retail, travel, entertainment, dining, and more.

“We understand how to connect advertisers to consumers and consumers to the products, services and experiences they value,” said Mastercard Chief Services Officer Craig Vosburg. “Mastercard Commerce Media is a natural extension of the trusted connections we’re known for and the work we already do across our unique suite of services. That means we’re not just well-positioned to bring a full-scale commerce media network to life—we’re best-positioned.”

Mastercard Commerce Media is launching in partnership with Citi, which will help the program grow faster, reach more users, and deliver more value. Mastercard already has ongoing ties with Citi, which will give Mastercard’s media network a head start in leveraging Citi’s infrastructure, customer base, and channels. Mastercard is also partnering with American Airlines, Microsoft, and WPP, which will help extend its footprint and connection to brands in the traditional media space.

As the use of consumer-permissioned data gains popularity across fintech subsectors, so too has the adoption of retail media networks. These networks allow institutions to monetize their first-party data by connecting brands with highly targeted audiences through trusted digital channels.

According to eMarketer, retail media networks will expand in the coming years. The firm estimates that retail media network spending will reach nearly $100 billion through 2028, reflecting both advertiser demand and consumer engagement with personalized content. An early trailblazer in the space is Chase Media Solutions, which launched in 2024 to leverage its transaction and cardholder data to serve personalized offers and marketing to its 80 million customers.