This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Tomorrow is the final day of the third quarter of 2025, which means that Wednesday marks our entrance into October. Historically, fall has been the busiest season for fintech announcements, so we’re ready to keep up with all of the new developments. Here is some of the biggest news from this week so far. We’ll continue adding news to this post throughout the week, so stay tuned!

BaaS and embedded finance

Worldpaylaunches embedded lending, banking and card issuing for platforms partners.

Payments

Citi and Dandelion collaborate to transform cross-border payments and enable near-instant payments into digital wallets across the globe.

Swift to add blockchain-based ledger to its infrastructure stack.

The UK is looking to regulate Buy Now, Pay Later lenders. Meanwhile in the US, the Consumer Financial Protection Bureau is reducing fines on previous enforcement actions. It’s a tale of two very different regulatory trends depending on which side of the Atlantic you’re on.

We’ve got the latest regtech news along with the rest of the top headlines in fintech right here in this week’s edition of the Fintech Rundown!

Payments

Ripplereports that Zand Bank and fintech platform Mamo have deployed its blockchain-enabled payments solution, the first UAE-based financial institutions to do so.

PayPallaunches its Complete Payments service in Singapore.

Albertsons Companies offers invoice-based payment for its business customers courtesy of its partnership with TreviPay.

AAA Life Insurance partners with payments network One Inc. to support digital payment processing.

Digital banking

Finovate Best of Show winner Tuumlaunches suite of Islamic Banking solutions to enable financial institutions to offer more Sharia-compliant banking products.

Fraud prevention

Money and safety app for families, Greenlight, introducesFamily Shield to help caregivers protect seniors from financial fraud.

Identity verification and fraud prevention services provider AU10TIXlaunches continuous AML risk monitoring.

MRI Software integratesNova Credit’sIncome Navigator into its fraud prevention and application qualification solution.

DeFi / crypto

Non-custodial stablecoin wallet MiniPayis now available as a standalone application on iOS devices.

Investment / wealth management

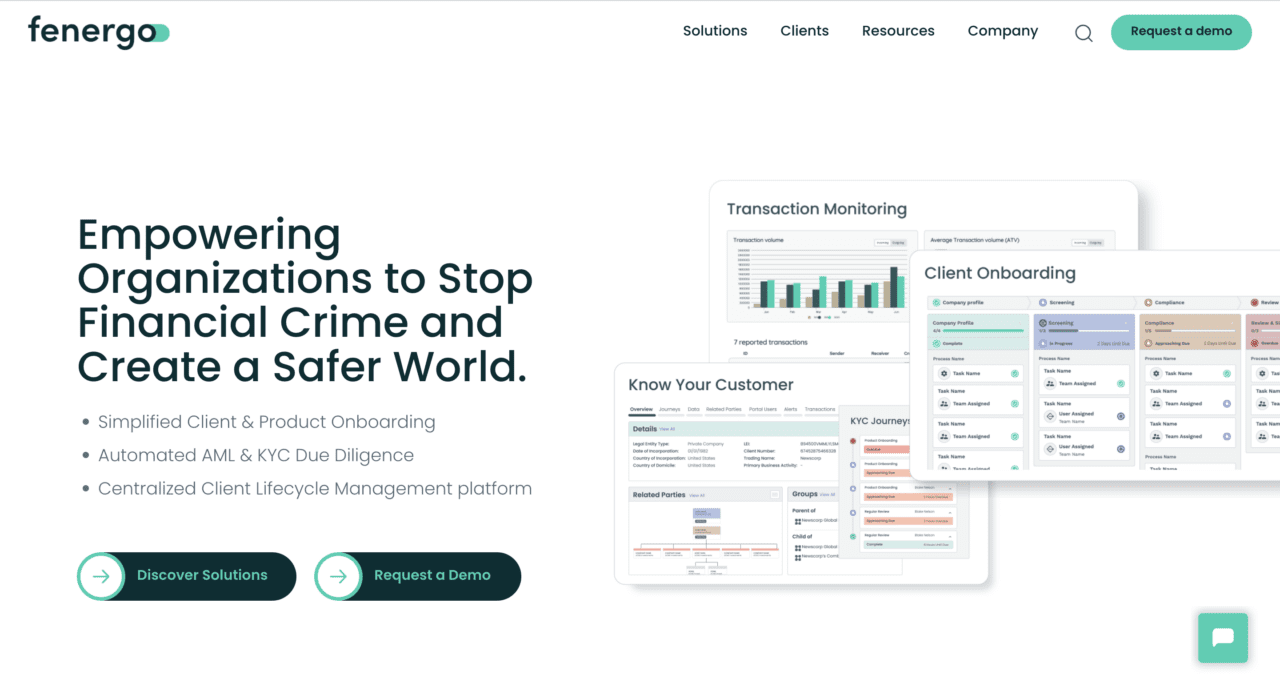

U.S. Bank Global Fund Services turns to Fenergo to digitize and streamline its investor onboarding and service experience.

Regtech

Risk management company EverClaunches its AI-powered risk assessment solution for marketplaces, Smart Scan.

The rage over regtech is real. In response to growing customer demands, emerging financial crime threats, and attempts by regulatory bodies to manage both of these developments, the field of regulatory compliance has never been more topical in financial services.

To this end, we interviewed banking and financial services compliance veteran Tracy Moore. Director of Thought Leadership & Regulatory Affairs at Fenergo, Moore joins the Finovate blog to provide her perspective on the regulatory environment for banks, fintechs, and financial services companies in 2025.

As part of Finovate’s commemoration of Women’s History Month, we also discuss issues of gender diversity in banking and financial services, and the role of mentorship in helping foster future leaders in the industry.

Can you tell us a little about yourself and the work you do at Fenergo?

Tracy Moore: I began my career in corporate legal training, specializing in finance and treasury transactions. My journey took me to Europe, where I transitioned into banking, spending much of my career in legal and compliance roles at global financial institutions. Upon returning to the U.S., I continued this path at a super-regional bank, gaining extensive experience in regulatory compliance and financial crime risk management.

Today, I serve as the Director of Thought Leadership & Regulatory Affairs at Fenergo, the global leader in Client Lifecycle Management (CLM) technology for financial institutions. In this role, I focus on financial crime risk management, regulatory change, and digital transformation, helping institutions solve for complex regulatory environments while enhancing operational efficiency.

I am deeply passionate about influencing industry change and driving technological advancements that make the financial sector safer and more resilient. My work involves collaborating with global regulators, financial institutions, and technology providers to develop innovative solutions that protect the industry against financial crime. I help connect regulation and technology to shape the future of compliance and risk management in today’s financial landscape.

What is it about the field of banking compliance that you find most interesting professionally?

Moore: I find it fascinating how geopolitical events shape the global financial industry, influencing not just regulatory frameworks but also presenting new challenges, such as financial crime and evolving risk landscapes. Today’s economy is so interconnected, and this means that financial institutions must constantly shift to address challenges such as sanctions, emerging threats, and evolving compliance requirements.

What truly interests me is the delicate balance financial institutions must strike meeting regulatory expectations, staying ahead of increasingly sophisticated bad actors, driving revenue growth, and ensuring safe financial services for their clients. Achieving this balance requires a combination of strategic foresight, innovation, and collaboration across the industry. Everyday has a new perspective and new challenges.

How has banking compliance changed over the course of your career in the industry?

Moore: Looking back over the past 25 years, the evolution of banking compliance has been nothing short of dramatic. When I started my career, compliance was often seen as a back-office function, more about checking boxes than driving change. Fast forward to today, and compliance has become a core pillar of financial institutions, shaping everything from risk management to customer experience.

One of the biggest shifts of course has been technology advancements. Alongside this, the sheer pace and complexity of regulatory change. Events like 9/11, the 2008 financial crisis, and major geopolitical shifts have completely reshaped the regulatory landscape. We’ve moved from more localized, paper-based processes to a hyper-digital, data-driven, and globally interconnected approach to compliance.

As a woman in this industry, I’ve also witnessed the growing role of diverse leadership in compliance and risk management. The field has evolved beyond traditional legal and audit backgrounds to welcome technologists, data analysts, and strategic thinkers, many of whom are women bringing fresh perspectives to a historically male-dominated space.

Issues (and innovation) in banking compliance have never been more top of mind. How have we arrived at this point, and is it a good thing for banks and their customers?

Moore: We’re here because the stakes have never been higher. Over the past two decades, a mix of financial crises, evolving threats, digital disruption, and geopolitical shifts has pushed compliance to the forefront. Regulators have responded with increasingly complex expectations, bringing the role of compliance into strategic planning for financial institutions.

This pressure has fuelled innovation.

AI, automation, and data analytics are transforming compliance, reducing manual processes, improving risk detection, and enhancing the customer experiences. Banks are now able to onboard clients faster, monitor activity in real time, and anticipate threats before they escalate.

For banks, it’s both a challenge and an opportunity. Compliance is tougher than ever, but those who embrace technology can gain a competitive edge. And for customers stronger compliance means better security, smoother transactions, and more trust in the system.

Seeing this shift firsthand is what lead me to make the decision to leave the traditional compliance role in banking and join Fenergo because I knew technology would be the driving force behind the future of compliance, and I wanted to be part of this transformation.

How do AI and automation create new compliance challenges for banks? In what ways can firms use these technologies to address compliance issues?

Moore: AI and automation can streamline compliance, but they also raise concerns both from regulators and banks themselves. Many institutions are skeptical, worrying about black-box decision-making, regulatory scrutiny, and potential biases.

The key challenge is explainability. Regulators need to understand how AI-driven decisions are made, so firms must prioritize transparency, clear documentation, and strong oversight.

That said, when used responsibly, AI can enhance risk detection, automate manual tasks, and improve compliance efficiency. The solution lies in communication by working with regulators to ensure AI models are interpretable, auditable, and aligned with compliance standards.

What areas of banking compliance do you think deserve more attention than they are getting?

Moore: Emerging digital assets and global regulatory alignment are two areas that need far more attention in banking compliance. The rapid rise of crypto, tokenization, and digital payments has outpaced regulatory frameworks, leaving financial institutions in a tough spot. How do you innovate while staying compliant in an environment where the rules are still being written? Without clear, consistent guidelines, banks are hesitant to fully engage, creating uncertainty for the entire industry.

At the same time, jurisdictional differences make compliance incredibly burdensome in today’s global economy. Financial crime doesn’t stop at borders, but regulations do, forcing banks to navigate a patchwork of requirements that slow down operations and increase costs. More global alignment and collaboration between regulators could ease this burden, ensuring that compliance is both effective and practical in a world where money moves faster than ever.

And lastly, the evolving nature of financial crime. Criminals are getting more sophisticated, using everything from deepfake identities to crypto mixing services to evade detection. Compliance programs need to move beyond traditional rule-based approaches and embrace real-time, predictive intelligence to stay ahead.

What are your thoughts on the progress made—or not made—toward greater gender diversity in banking in recent years? Are you optimistic about the future of women in banking, particularly in areas like compliance?

Moore: Women in banking, especially in compliance, have made progress, but not nearly enough. Too often, diversity is overlooked as a business advantage instead of recognized for the value it brings. In today’s geopolitical and financial environment, organizations need diverse perspectives to navigate risk and drive innovation, yet those perspectives are still dismissed.

Despite this, I am optimistic. Women are smart, resilient, and persistent. We continue to prove our expertise in ways that cannot be ignored. Compliance is an area where women thrive because it demands strategic thinking, problem-solving, and leadership under pressure.

Real change will happen when companies move beyond surface-level efforts and embrace diversity as a competitive advantage. Women will keep breaking barriers, whether the industry is ready or not.

Mentorship can play a key role in helping women entering financial services or launching fintechs. Did mentorship play a significant role in your early career? What message would you give to banking and financial services professionals when it comes to sharing their insights and experience as mentors?

Moore: Mentorship has been invaluable in my career. I have always sought out mentors and sponsors—both men and women—who could guide my development and challenge me to grow. Beyond that, I have chosen a personal board of directors: female professional leaders across various industries who have provided insight, support, and perspective at every stage of my journey.

For those in banking and financial services, mentorship is more than just giving advice or sharing a coffee. It is about opening doors, advocating for talent, and sharing real, honest experiences. The next generation of female leaders is watching and learning. It is up to us to make sure they feel supported, empowered, and ready to step forward.

Financial compliance software company Fenergo has teamed up with PwC.

The partnership is designed to bring AI-powered CLM and KYC solutions to more financial institutions around the world.

Fenergo made its Finovate debut at FinovateEurope 2012. PwC won Best of Show in its Finovate debut at FinovateFall 2021.

Fenergo and PwC have announced a new partnership that will help put Fenergo’s AI-powered Client Lifecycle Management (CLM) and Know Your Customer (KYC) solutions in the hands of more financial institutions. The combination of PwC’s financial crime expertise with Fenergo’s AI-powered CLM technology into a single offering will make it easier for financial institutions to digitally transform their financial crime operations.

Fenergo’s Global VP for Partnerships and Alliances Matt Edwards said that the collaboration between the two firms will “deliver an optimum target operating model for CLM.” Edwards added that the solution “empowers financial institutions to efficiently mitigate financial crime risk while driving growth and efficiency gains.”

Fenergo’s CLM helps ensure that financial services firms realize tangible benefits and return on investment from the digital transformation of their client management and compliance processes. The platform provides faster client onboarding, including streamlined onboarding for low-to-medium risk clients; improved operational efficiencies with fewer touchpoints; policy-driven accurate risk assessments aligned with regulatory requirements; and a reduced total cost of ownership thanks to advanced API integrations.

Complementing Fenergo’s CLM technology are PwC’s Target Operating Model design, end-to-end customer experience journey mapping, operational readiness, data migration, systems integration, and business change management.

PwC Partner Mark Hunter highlighted Fenergo’s technology as “uniquely positioned to serve mid-market to large multinational organizations.” Hunter praised the company’s platform for its “scale, flexibility, and advanced capabilities” that help institutions better manage complex regulatory environments and large volumes of transactions.

A UK-based multinational assurance, advisory, and tax services provider, PwC counts more than 85% of the Global Fortune 500 companies as its clients. PwC maintains offices in 152 countries and reported gross revenues of more than $55 billion for the year ending 30 June 2024. The company participated in Finovate’s developer conference, FinDEVr SiliconValley 2016, and won Best of Show at FinovateFall 2021 for a demonstration of Customer Link, its customer data platform that helps institutions build better, more personalized experiences.

Dublin, Ireland-based Fenergo made its Finovate debut at FinovateEurope 2012. The company offers simplified client and product onboarding, automated AML and KYC due diligence, and a centralized CLM platform that helps financial institutions, asset management, and fintechs manage customers throughout the entire client lifecycle.

Fenergo’s partnership news with PwC comes a few days after the company announced the launch of its all-in-one KYC, onboarding, and trade request management platform for businesses in the energy and commodities sector. The new Trader Request Portal combines KYC, onboarding, and trade request management capabilities.

Fresh from FinovateFall in New York, we’ve got a raft of fintech news to share and catch up on. Be sure to check Finovate’s Fintech Rundown all week long for the latest in industry news, announcements, and headlines.

This week’s edition of Finovate Globalhighlights recent fintech headlines from Ireland.

Dublin-based regtech Fenergo has inked a partnership with Caribbean-based PROVEN Bank. The financial institution will leverage Fenergo’s transaction monitoring solution to enhance and streamline its anti-money laundering (AML) compliance operations.

PROVEN Bank Deputy Chief Executive Officer Nikita Kissoon underscored increasing regulatory pressure on financial institutions as one of the reasons the bank sought the partnership with Fenergo. Kissoon praised the company’s “excellent reputation for expertise in both AML regulations and cutting-edge compliance technology,” and said that enhanced AML compliance “aligns with our commitment to combat financial crime and remain future-proofed against fast-evolving regulatory changes across our offshore locations.”

Fenergo’s technology will help boost operational efficiency for the Caribbean-based financial institution. PROVEN Bank will benefit from the automation of multiple manual AML processes, which will reduce the number of false positives and free up compliance resources to focus on more complex situations and higher-risk customers. The bank will begin deploying the technology at its Cayman Islands location and subsequently expand the solution to its offices in St. Lucia and its affiliate company, PROVEN Wealth, based in Jamaica.

The partnership is especially timely. The Cayman Islands, where PROVEN Bank is based, was only recently removed from the Financial Action Task force’s AML grey list and the European Union’s black list earlier this year.

Fenergo Chief Strategy Officer Stella Clarke pointed out that banks like PROVEN that operate in multiple jurisdictions often struggle to keep up with local regulations with regards to AML. “Our transaction monitoring solutions offers PROVEN Bank the flexibility to seamlessly adapt to fast-evolving regulatory environments, while empowering it to more effectively cross-sell services to existing customers based on rich data insights,” Clarke said.

Fenergo made its Finovate debut 12 years ago at FinovateEurope in London. The company has raised more than $760 million in funding, and includes TLG Capital and Bridgepoint among its investors. Fenergo’s partnership news comes at the same time that the firm announced that it had formed an alliance with Deloitte Ireland to help deliver Fenergo’s CLM solutions to financial institutions throughout EMEA.

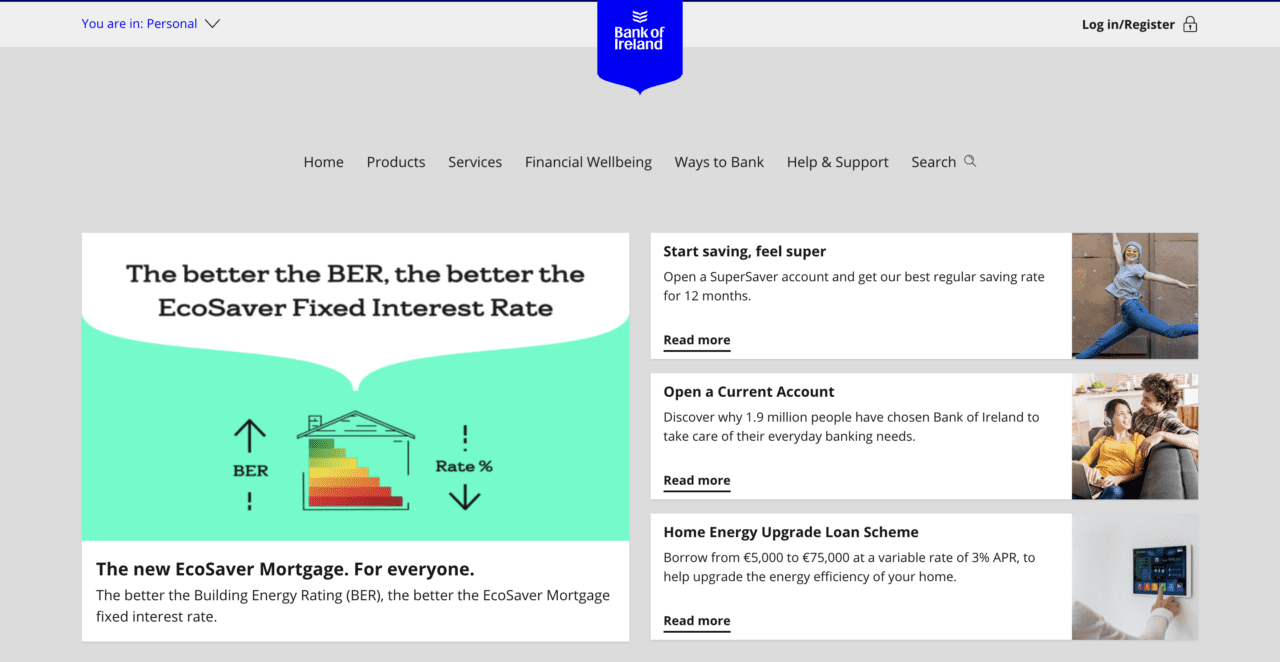

The Bank of Ireland wants you!

If you are a technology specialist looking to drive fintech innovation in the Republic, that is.

The Bank of Ireland just announced that it is recruiting for 100 technology roles in a variety of digital projects, including fighting fraud and advanced data analytics. The Bank is specifically looking for talent with experience in data, delivery management, engineering, resilience and cybersecurity. Open banking, cloud computing, APIs, and AI are also among the areas of emphasis.

“We continue to invest in our talent, technology, and infrastructure to ensure customers have the very best banking services,” Bank of Ireland Group Chief Operating Officer Ciarán Coyle said, “We’re currently progressing a range of innovative digital projects across the Group and we want to recruit talented specialists who can enhance the banking experience for our customers.”

The bank’s search for tech talent comes as the institution has increased its investment in financial technology. After making more than 60 enhancements to its mobile banking app, including biometrics and fraud monitoring, the bank saw an 18% year-on-year increase in active digital users. The bank announced the largest single investment in ATMs in the last decade earlier this year, as well as an investment of €15 million on new fraud prevention technology.

“We are looking for the very best talent to join our technology team as we continue to deliver improvements for customers and colleagues across the organization,” Coyle said.

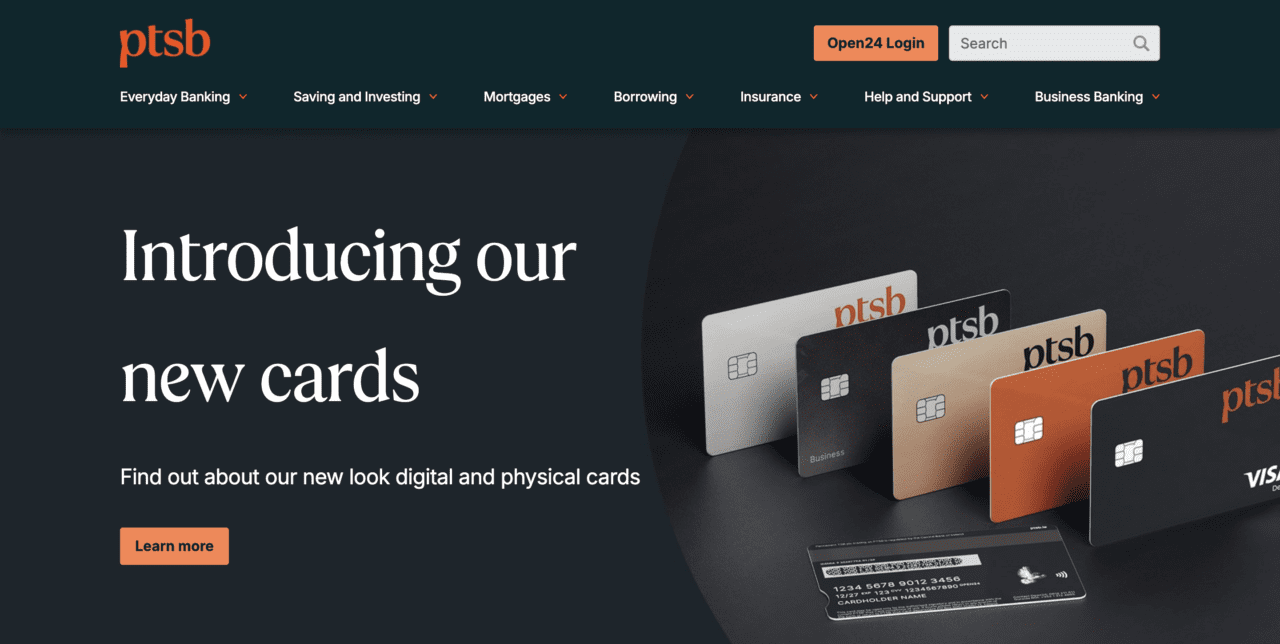

Ireland’s PTSB has extended its agreement with Worldpay, giving the bank’s customers access to an additional range of services from the company, including e-commerce and ePOS. PTSB will also gain access to Worldpay DCC, a dynamic currency conversion solution that allows cardholders to pay in the currency of their choice.

PTSB Head of Personal Banking at PTSB Jeff Harbourne said that the ability to offer “a best-in-class merchant services solution” was key to the bank’s “ambition of becoming Ireland’s best personal and business bank.” Harbourne added, “By partnering with Worldpay, we’re offering a competitive advanced payments solution to our existing and new customers that enables them to grow their businesses and accept payment across all channels.”

With more than 1.2 million customers, PTSB has a presence in 98 locations throughout Ireland. Founded in 1816, the financial institution rebranded from Permanent TSB last fall following its acquisition of a sizable portion of Ulster Bank, including the firm’s Retail, SME, and Asset Finance businesses.

A Finovate alum since 2015, WorldPay today is a major payments technology and solutions company that processes more than 40 billion transactions across 146 countries and 135 currencies. Headquartered in Cincinnati, Ohio, and founded in 1971, WorldPay announced an extension of its strategic partnership with fellow Finovate alum ACI Worldwide in July, and inked a new partnership with another Finovate alum, American Express, in May.

Here is our look at fintech innovation around the world.

Latin America and the Caribbean

Colombian payment orchestration platform Yuno teamed up with Medellin-based financial services app Nequi.

Mexico City-based cryptocurrency exchange Bitso partnered with blockchain company Coincover for its non-custodial disaster recovery service.

Peruvian investment and asset management arm of Credicorp, Credicorp Capital, went live with Temenos’Multifonds accounting and investor servicing solution.

Financial Times profiled Kim Beom-su, founder of Kakao and one of the richest men in South Korea, who was recently arrested on stock manipulation charges.

Digital identity verification provider ADVANCE.AI signed an agreement with the Credit Information Corporation (CIC) to become the newest credit bureau in the Philippines. Read more about fintech in the Philippines in last week’s edition of Finovate Global.

Estonian payments and e-commerce solution provider Montonio introduced its new CEO Johan Nord.

Payments infrastructure company Kevin has been blocked from serving new clients by the Bank of Lithuania, which has also appointed a “temporary representative to oversee” the firm’s activities.

Middle East and Northern Africa

Singapore’s Prytek bought a controlling stake in Israeli fintech Tip Ranks, giving the company a valuation of $200 million.

This week’s edition of Finovate Global highlights recent fintech news from India.

A strategic partnership between financial software applications and marketplace company Finastra and Tech Mahindra, announced today, will help corporate banks accelerate their digital transformation journeys. Specifically, the partnership will make Tech Mahindra the exclusive global implementation partner for Finastra’s Cash Management platform. Tech Mahindra will also become the preferred partner for Finastra’s Trade Innovation and Corporate Channels solutions in the U.S., Canada, and Europe.

“This is an important partnership that aligns closely with our commitment to helping our customers navigate today’s challenges and embrace much needed digitalization,” Finastra CEO Simon Paris said. “The broad portfolio of services and deep experience offered by Tech Mahindra are a valuable complement to our modern and open software. With this combination, we look forward to propelling the digital transformation of even more banks and financial institutions around the world.”

The partnership will enable the two companies to offer a variety of cross-functional solutions across digital advisory, system integration, integrated infrastructure, and cloud services. These solutions will help corporate and institutional banks streamline and digitalize their operations. Financial institutions will further benefit from faster time to value for customers courtesy of faster implementations and upgrades.

“This partnership brings together two global leaders in digital transformation and financial services applications to help corporate banks scale at speed,” said Tech Mahindra CEO and Managing Director Mohit Joshi. “We believe our joint efforts will redefine the way banks digitize to improve their profit margins.”

Founded in 1986, Tech Mahindra is an international IT services and consulting company, headquartered in Pune, India. Part of the Mahindra Group, Tech Mahindra has more than 147,000 employees in 90+ countries serving 1,100+ clients. The firm offers solutions and expertise in verticals ranging from banking, insurance, and telecommunications, to media, entertainment, and retail. The first Indian company to earn the Sustainable Markets Initiative’s Terra Carta Seal, Tech Mahindra is publicly traded on India’s National Stock Exchange (NSE) and has a market capitalization of $17.8 billion (₹1.5 trillion).

The product of a union between Finovate alum Misys and D+H in 2017, Finastra offers software and solutions for financial institutions across lending, payments, treasury and capital markets, as well as retail, digital, and commercial banking. The company’s technology for banks helps them develop their direct banking relationships and to grow through new channels such as Banking-as-a-Service and embedded finance. More than 8,000 institutions – including 45 of the world’s top 50 banks – rely on Finastra’s technology.

The Reserve Bank of India (RBI) has been making fintech, financial, and economic news of late. On the fintech side, the RBI has granted cross-border payment licenses to three fintechs: BillDesk, Amazon Pay, and Adyen. These licenses will enable these companies to operate as cross-border payment aggregators and, ultimately, to offer their customers payment services for both imports and exports.

The RBI has been actively encouraging many fintechs to secure payment aggregator licenses; more than 20 companies have been granted PA licenses to date. In many of these instances, the RBI has suggested that companies interested in cross-border payments in particular apply for these licenses. Another firm that recently secured its PA license for cross-border payments for import and export from the RBI is Cashfree Payments.

In order to secure PA licenses, fintechs must register under the Financial Intelligence Unit-India (FIU-IND) in order to become authorized to process transactions. Fintechs must also maintain a minimum net worth of Rs 15 Cr ($1.8 million) during application, a sum that will increase to Rs 25 Cr ($2.9 million) after March 2026.

Speaking of payments, the RBI is now a part of Project Nexus. The first project from the payments sector of the Bank for International Settlements (BIS), the project seeks to connect the Faster Payment Systems of four Association of Southeast Asian Nations (ASEAN) countries – Malaysia, the Philippines, Singapore, and Thailand – and India. While India’s RBI has collaborated with a number of other countries via its Unified Payments Interface (UPI) to support bilateral payments, RBI’s participation in Project Nexus is the first time the bank has officially joined a multilateral project of this scope.

Additional countries are expected to be added over time. The project will help small and medium-sized businesses in India make faster, less expensive, and more reliable cross-border payments. To this end, the project will also make it easier for Indian banks to offer cross-border payment services to a broader range of countries. Speed and greater transparency are also among the benefits highlighted by observers.

Are you a fan of CBDCs? This week, the RBI reported that its central bank digital currency (CBDC) pilot has five million users and 420,000 participating merchants as of June 30. According to Reuters, transactions in the digital rupee are running at a pace of 100,000 a day, significantly below lofty expectations and hopes of one million transactions a day by 2023. It has also been pointed out that the digital rupee may suffer from competition with the country’s popular faster payments system, UPI.

Nevertheless, the digital rupee may be getting a bit of a boost courtesy of cryptocurrency exchange Bybit, which launched digital rupee payments on its platform this week. According to Cointelegraph, the digital rupee will be available as a wallet-based payment option, along with the exchange’s payment options in rupees via bank transfer, third-parties such as Paytm, and India’s Unified Payments Interface (UPI).

“By incorporating the eRupee payment, Bybit aims to elevate the payment experience for INR (Indian rupee) users, fostering trust and reliability in every transaction,” said Bybit sales and marketing director Joan Han. “Furthermore, this initiative is expected to attract a wider pool of merchants to the platform, driving business growth and expanding the reach of Bybit’s services within the market.”

Founded in 2018, Bybit is the second-largest cryptocurrency exchange by trading volume in the world, with more than 37 million users.

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

Faye, an insurtech startup based in Israel, raised $31 million in Series B funding.

Egyptian B2B platform Cartona secured $8.1 million in a Series A extension round led by Algebra Ventures.

Israel-based financial crime detection company ThetaRayacquired screening company Screena.

Central and Southern Asia

Bangladesh-based fintech Nagad teamed up with Huawei Technologies.

The Reserve Bank of India approved cross-border payment licenses for BillDesk, Amazon Pay, and Adyen.

Texas-based migration fintech Vesti announced an expansion to Bangladesh, India, and Pakistan.

Latin America and the Caribbean

Caribbean-based PROVEN Bank partnered with Ireland’s Fenergo to enhance its transaction monitoring and AML operations.

Mexican fintech platform for the underbanked and microbusinesses Aviva raised $5.5 million in funding.

Rippleteamed up with the National Federation of Associations of Central Bank Servers (Fenasbac) to promote fintech innovation in Brazil.

Asia-Pacific

ADVANCE.AI launched its KYB business intelligence service to enhance its operations in Singapore and Malaysia.

The summer fintech news slowdown is coming soon, but it hasn’t taken hold yet. Fintech news picked up last week, with multiple funding rounds and product announcements. Stay tuned to read this week’s news as we post updates and evolutions.

Embedded finance

Cross-border payments platform PingPongunveils its embedded lending solution.

Will the new month bring new challenges in fintech? Or will the news cycle take a much-needed vacation as summer approaches? Stay tuned to this week’s news for updates and evolutions throughout the week.

Pinnacle Bankpartners with CorServ to implement a modern credit card program for commercial, business, and consumer customers.

Insurtech

Scott Credit Union selectsBUNDLE by Insuritas to launch its insurance agency.

Investment and wealth management

Brokerage-as-a-Service innovator DriveWealthforges new partnership with Turkish fintech Papara.

Lending

PlaidunveilsConsumer Report, a new solution that brings businesses real-time cash flow data along with credit risk insights through Plaid Check, its consumer reporting agency.

Irish regtech Fenergo has agreed to be acquired by a pair of private equity firms, Astorg of Paris and Bridgepoint of London. The deal, which involved selling a majority take worth $600 million, values Fenergo at $1.1 billion (€900m), and will give the company additional capacity to “make strategic acquisitions and stay ahead of the competition.”

“We are delighted that Astorg and Bridgepoint have chosen to invest in our company, providing us with the financial strength required to pursue our ambitious high-growth strategy,” Fenergo founder and CEO Marc Murphy said. “Both Astorg and Bridgepoint have enormous experience and credibility in our sector, something I am keen to leverage over the coming years. Ultimately, we only exist to serve the needs of our customers. We are looking forward to partnering with them in the next phase of our development.”

Founded in 2009 and headquartered in Dublin, Fenergo made its Finovate debut three years later, demonstrating its innovative client onboarding and account opening management solution. Since then, Fenergo has established itself as a major player in the space, partnering with 32 of the world’s top 50 financial institutions, as well as technology companies like IBM, PwC, and Luxoft. The company says its technology has provided clients with 82% reduction in onboarding times, 34% savings in audit costs, and 7x ROI in four years or less.

Fenergo began the year with the launch of its KYC & Onboarding for Salesforce solution, connecting its client lifecycle management (CLM) technology and regulatory intelligence with Salesforce’s CRM. The integration makes it easier for banks and other financial institutions to enhance the customer experience by providing a more seamless onboarding process.

“In today’s highly challenging business environment, there is no margin for error in delivering exceptional, digital, and joined-up customer experiences,” Murphy explained when the new offering was launched. “Automation is key so that customers can be onboarded without unnecessary manual intervention in the back-end processes. Salesforce is the launchpad for automated onboarding while Fenergo ensures compliance by design through API-powered multi-channel orchestration.”

Fenergo was awarded top honors in the Client Lifecycle Management Solution category at the Ninth Annual WealthBriefing European Awards this month, echoing the recognition the company received at the beginning of the year from Asian Private Banker. So far in 2021, Fenergo has forged partnerships with Anglo-Gulf Trade Bank and Mizuho Americas.

Revolut has added a new feature to its Revolut Junior app for youth aged seven to seventeen that will help parents teach the value of saving to their children. Goals enables both parents and child users to set and track financial savings objectives, and leverages the app’s other main features – Allowances and Tasks – to provide a more comprehensive financial wellness solution that works for kids and their parents.

Available to Revolut’s Premium and Metal customers, the new option can be used by parents to create financial savings goals and monitor their child’s progress as savings accrue. Kids can set their own savings goals as well, which can be supervised via the parent’s app. Goals can be funded directly by parents or by child users via their Allowances or by completing assigned tasks and chores.

“Goals, along with payments, allowances, and tasks, was one of our customers’ top requested and valued features,” Revolut Head of Premium Product Felix Jamestin said in a statement. “(We’re) excited to be building a product that is making saving fun and easy for both kids and parents.”

Revolut launched its Revolut Junior app earlier this year, and now boasts more than 200,000 children signed up for the program. Currently available in the EEA and the U.S., Revolut plans to offer the solution in Singapore, Japan, and Australia “in the near future.”

Alumni News Updates

LendingClub sheds P2P lending en route to bank rebirth: You would be forgiven for thinking the first rule of a company called “LendingClub” is to lend money. But LendingClub’s pivot away from its origins as an innovator in the P2P space 14 years ago continues as it announces that it will shut down its retail P2P platform as of the end of the year. The move comes more than a year after LendingClub shuttered its small business lending arm, and is widely understood to be a path-clearing effort en route to LendingClub incarnation as a bank.

Fenergo, IBM partner to bring AI to customer onboarding: A new integration between IBM Watson, the IBM Cloud, and Fenergo’s client lifestyle management technology will improve the efficiency of the onboarding process for financial institutions. IBM Customer Lifecycle Management with Fenergo combines Fenergo’s leadership in customer journey and digital transformation with IBM’s AI-enabled, AML and KYC solutions to provide better personalization, risk assessment, and regulatory compliance.

Eigen Technologies hires its first CFO: London-based NLP technology innovator Eigen Technologies has selected Spyros Karageorgis as its first Chief Financial Officer. Karageorgis comes to Eigen after tenures as CFO and COO at image recognition company Cortexica Vision Systems, and as CFO at SaaS e-commerce platform Venda. Karageorgis is one of two new members of Eigen’s C-suite: the company also announced new Chief Revenue Officer Tony Ehrens.