This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

As AI agents begin transacting on behalf of users, traditional payment and identity models fall short of providing the trust these systems require.

Prove is introducing its Verified Agent solution that links verified identity, intent, payment credentials, and consent through a cryptographically backed chain of custody for every autonomous transaction.

By replacing weak verification methods with multi-factor authentication and cryptographic proof, Prove aims to make agentic commerce safe enough to scale globally.

There has been plenty of hype around agentic commerce this fall, but many of the announcements surrounding agentic shopping and payments have leap-frogged an important issue: agent identity verification.

Digital identity company Prove is helping to solve this issue today with its new launch, the Prove Verified Agent, which aims to provide a trust and verification layer for autonomous agents acting on behalf of consumers and businesses. The new Verified Agent tool works by creating an end-to-end chain of custody that links verified identity, intent, payment credentials, and consent backed by cryptographic proof.

Agentic commerce, which could add more than $1 trillion in annual economic value, is different from the traditional four-party payment model that leverages legacy rails and identity verification. These models were not designed to allow AI agents to act on behalf of users, and agentic commerce can’t scale on traditional identity rails.

Recognizing that agentic commerce depends on verified trust between humans and machines, Prove’s leadership emphasized how identity must sit at the heart of this new ecosystem. “The vision and benefits of agentic commerce cannot be realized without trust,” said Prove CEO Rodger Desai. “Our foundational principle has always been to enable secure transactions by verifying identity and consent without friction. That approach positions Prove to lead in the agentic economy. Our platform is purpose-built for a future where bots act on our behalf, with identity that is native to every transaction and built on frontier identity principles.”

Prove’s Verified Agent offers a new trust framework that is built on the Prove Identity Graph, creating a cryptographically backed “chain of custody” for every autonomous transaction. The system begins by anchoring a verified digital identity to real-world attributes—such as phone numbers, national IDs, and payment credentials—tying each agent’s actions to a legitimate individual or business.

After tying the verified person or entity to an attribute, Prove issues signed digital credentials to authorized agents. These credentials enable agents to transact on behalf of their users, while counterparties can instantly verify their authenticity using cryptographic checks. Every identity and transaction is cross-referenced against a live registry of agent publishers, relying parties, merchants, payment networks, and CDNs to filter out unverified automation. Once verified, agents are authorized to act on behalf of a verified individual or entity, and Prove maintains the link between verified identity, intent, payment credentials, and consent.

To further protect users, Prove’s Verified Agent replaces text-based verification and one-time passwords with multi-factor authentication and session-level authorization limits, reducing phishing attempts and ensuring that each agent operates strictly within a user’s explicit consent. Additionally, every interaction is completely auditable. The interactions among agents, merchants, and users are co-signed by both user and merchant keys to provide cryptographic evidence for dispute resolution, chargeback protection, and regulatory reporting.

By creating this trust, Prove anticipates that it will enable global ecosystems to participate in the agentic economy without fear of identity violations.

Modern treasury solutions company Qolo has forged a “strategic alignment” with Huntington National Bank.

The alignment comes as the two companies unveiled a new virtual account management (VAM) platform, Connected Deposits, and follows a strategic investment Huntington made in Qolo earlier this year.

Headquartered in Fort Lauderdale, Florida, Qolo made its Finovate debut at FinovateFall 2022 in New York.

There is a wide range of challenges facing banks when it comes to treasury management these days. Interest rate uncertainty, rising regulatory scrutiny and compliance costs, working capital optimization, and technology challenges—from modernization to cybersecurity—are all issues that have made treasury management that much more difficult for CFOs, treasury managers, and their teams.

Over the summer, PwC published its 2025 Global Treasury Survey which showed how “the role of treasury continues to evolve into a more strategic, innovative and data-driven partner” that is a fundamental part of value creation for businesses. Quantitatively, the survey noted that approximately 40% of its 350 respondents—treasurers from around the world—said that they were not leveraging an in-house banking or payment centralization model. 65% of organizations queried said that they are planning to expand API use in the next few years.

This is the context in which we learn that modern treasury solutions provider Qolo has announced a “strategic alignment” with Huntington National Bank. The alignment follows a minority strategic investment the financial institution made in the Fort Lauderdale-based fintech earlier this year, and comes as the two companies announced the launch of a new virtual account management (VAM) platform, Connected Deposits, for Huntington National Bank’s commercial customers.

“Our alignment with Huntington reflects a shared vision for the future of commercial banking,” Qolo Founder and CEO Patricia Montesi said. “Treasury management is getting more complex and dynamic across almost every industry, making Virtual Account Management tools like the one Huntington is launching with Qolo increasingly essential. Together, we’ve built a solution that empowers businesses to operate with greater agility, transparency, and control.”

Connected Deposits is a Virtual Account Management (VAM) platform, built on Qolo’s technology, that enables real-time cash visibility, automated reconciliation, and seamless fund segregation for multi-entity businesses—all within a single parent account. The new offering is designed to help the bank’s corporate customers better manage their complex operational needs—from payments to reporting—via an API-first architecture.

Qolo anticipates that Connected Deposits will show banks how technology can enhance treasury management by reducing account maintenance costs and eliminating manual payment reconciliations. Instead, Connected Deposits, with its real-time visibility into cash positions across all entities and projects, not only enhances compliance and risk controls, but also generates new fee income opportunities for banks via modern treasury services.

“With Qolo’s technology powering Connected Deposits, we’re able to offer enhanced efficiency across complex cash management needs for our commercial clients,” Huntington’s head of national deposits, Alex Tsarnas, said. “This platform strengthens our ability to serve clients with specialized requirements while reinforcing Huntington’s commitment to innovation and client-centric solutions.”

Founded in 2018 and headquartered in Fort Lauderdale, Florida, Qolo made its Finovate debut at FinovateFall 2022 in New York. At the conference, the company demonstrated how its Companion Core provided banks with fintech functionality that worked in tandem with their current systems, enabling them to offer their customers a range of new services without the need to undergo a disruptive, wholesale core replacement.

The final week of October is always a little extra spooky, as it signals that the start of the holiday season is just days away. The week also generally brings an onslaught of company announcements, as organizations rush to publish their latest news before audiences become distracted by the holidays. Here is some of the biggest news from this week so far. We’ll continue adding news to this post throughout the week, so stay tuned!

Payments

Mastercard and CitibringCiti Flex Pay Installments to more retailers at checkout.

Worldpayunveils AI-powered 3D Secure optimization service to increase payment approvals.

PayQuickerannouncesFlex, a business-ready stablecoin alternative for global payouts.

Bold.orgpartners with Wildfire to launch first debit card rewards program for purchases on AI platforms.

PayNearMeenhancesPayXM with the rollout of AI-powered Intelligent Virtual Agent (IVA).

Modern Treasury announced its first acquisition, purchasing stablecoin and fiat payments company Beam to expand its real-time money movement capabilities.

The deal unifies fiat and stablecoin rails under Modern Treasury’s single API and will support RTP, FedNow, ACH, wires, Push-to-Card, and stablecoin payments while streamlining compliance through built-in KYC, KYB, and AML.

By combining Beam’s stablecoin technology with Modern Treasury’s scale, the company is positioning itself as a bridge between traditional and blockchain payments.

Payment operations platform Modern Treasury marked its first acquisition today. The San Francisco-based company announced this week it has purchased payments company Beam for an undisclosed amount.

Modern Treasury plans to use Beam, which offers both stablecoin and fiat payments capabilities for customers like Sling Money, to broaden its own money movement platform to include both traditional and stablecoin settlement rails.

Beam was founded in 2022 and has since processed more than $350 million in payments across the globe that have enabled small and medium-sized businesses to manage their cross-border operations. The company has raised $7 million and is backed by investors including Archetype, Castle Island Ventures, Arca, A*, and Soma.

“Instant payments and stablecoins are the future of money movement,” said Modern Treasury Co-founder and CEO Matt Marcus. “Beam has proven traction delivering real-time payments for stablecoin-native payment flows. Modern Treasury has processed hundreds of billions of dollars on our platform. Together, we’re creating the best infrastructure to move money instantly—without the delays and limitations of banks or card-first payment providers.”

Modern Treasury will support real-time payments via stablecoins, Push-to-Card, and traditional rails like RTP, FedNow, ACH, and wires. The company simplifies the application with its single API that handles compliance elements such as KYC, KYB, and AML, which allows it to replace six months of onboarding and compliance work with just a few API calls.

“Beam was founded on the belief that stablecoins can play a major role in the future of payments, but to make that real, you need scale, regulatory strength, and trusted infrastructure,” said Beam Founder and CEO Dan Mottice. “By joining forces, we’re accelerating that vision. Beam’s stablecoin and fiat orchestration capabilities will be woven directly into Modern Treasury’s platform to unlock instant pay-ins and payouts, FX efficiency, and next-generation liquidity management, all within a trusted enterprise-grade system.”

Mottice, who previously led Visa’s crypto settlement products and Visa Direct Payouts, is joining Modern Treasury as Head of Beam as part of today’s deal.

Modern Treasury’s acquisition of Beam is a great example of how stablecoins are not only becoming mainstream, but they are also becoming a key way for organizations to differentiate themselves in the enterprise payments space.

As stablecoins gain regulatory clarity and businesses demand faster, always-on settlement, Modern Treasury is positioning itself as the connective tissue between fiat and blockchain rails. Because it brings both traditional and stablecoin payments under one API and compliance framework, Modern Treasury sets itself apart in the crowded global money movement space.

This week’s edition of Finovate Global examines recent fintech news from Mexico.

Earlier this month, ResearchAndMarkets.com published its Mexico Embedded Finance Databook Report for 2025. The 230-page report noted that the embedded finance market in Mexico is expected to reach more than $18 billion this year and top $22 billion by the end of 2030. Among the key takeaways from the report is the increasing traction of embedded credit products such as Buy Now Pay Later (BNPL), and the growth of embedded payments in mobility, food delivery, and social commerce driven by growing smartphone use and government support for digital, real-time payments options. Embedded finance solutions such as lending are enabling non-fintech businesses in Mexico to leverage APIs and BaaS to expand their offerings, the report notes. This is helping bring more financial services to underserved communities in the country. It is also creating greater competition for companies in both the lending and payments spaces.

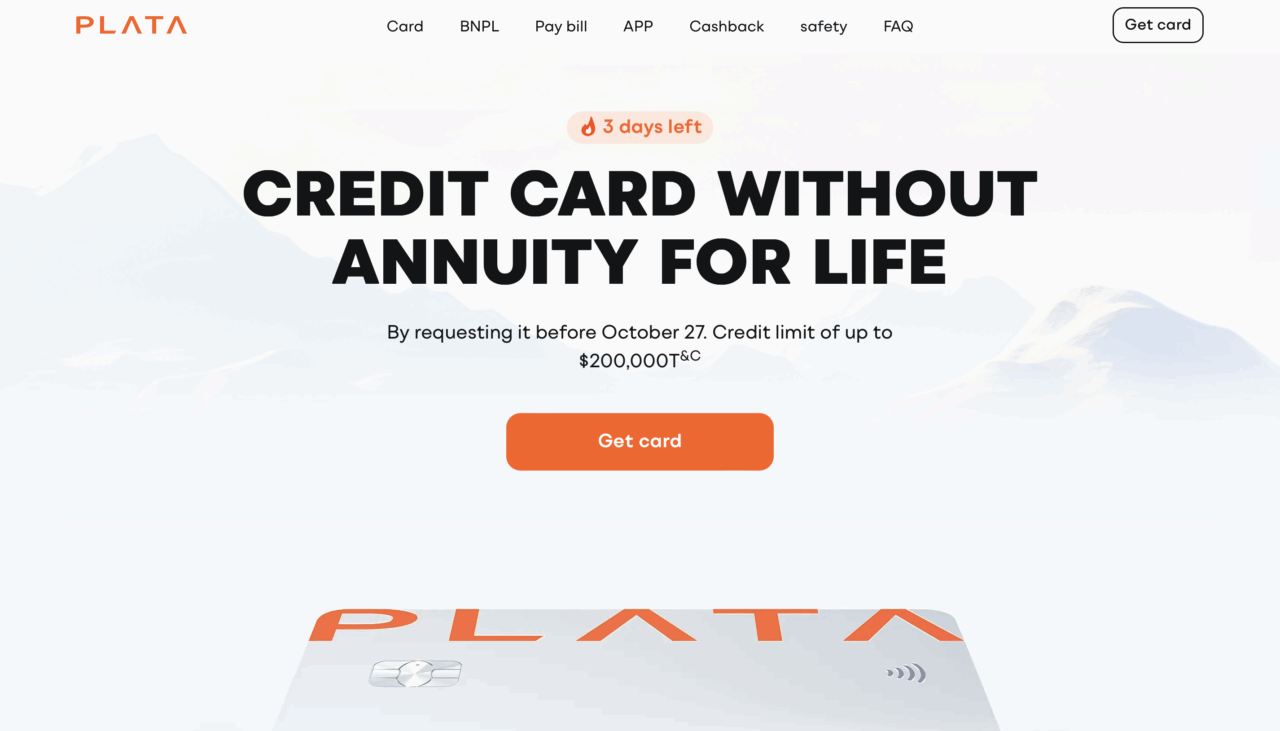

Mexican Fintech Plata Double Valuation on Latest $250 Million Fundraise

Mexican digital financial platform Plata has secured $250 million in new equity funding. The round, which includes both a primary equity raise and a secondary equity transaction, was led by Kora and featured participation from Moore Strategic Ventures, Audio Ventures, Spice Expeditions, Hedosophia, as well as several US and European family offices. The funding builds on an earlier investment by Televisa-Univision and boosts Plata’s valuation to $3.1 billion.

“The growth we have achieved in such a short time demonstrates a clear strategy and a shared conviction: build a strong institution from its foundations,” Plata CEO and Co-Founder Neri Tollardo said. “This transaction reflects investors’ confidence, the strength of our technological model, and the talent we have assembled. We set out to create a digital bank built on innovation, operational excellence, compliance, and efficiency—and today, we are seeing the results of that effort.”

Plata received its banking license in December 2024 and is waiting for authorization to begin banking operations. The company boasts its own technological and operational infrastructure, including a core banking system that enables a fully digital, branchless model with automated risk management and 24/7 personalized customer service. Over the past 30 months, Plata has topped the two million mark in terms of active credit customers, making it one of the fastest-growing digital financial platforms in Latin America. The company’s Plata Card gives users two months to pay without interest and up to 15% of cash back in real money.

“We believe Plata represents the new standard for digital banking in emerging markets,” Kora Co-Founder Nitin Saigal said. “In a very short time, the company has demonstrated impressive execution, combining technological innovation with a clear vision for financial inclusion. We are excited to continue strengthening our partnership and to support Plata in this new phase of growth.”

Revolut obtains Mexican banking license; SumUp goes live

This week we learned that two Finovate alums—Revolut and SumUp—are actively exploring opportunities in Mexico. Revolut announced this week that it has received final regulatory approval to initiate banking operations in Mexico. The authorization came from the National Banking and Securities Commission (CNBV), with approval of the Bank of Mexico. Now a Multiple Banking Institution in Mexico, Revolut is the first independent digital bank to directly apply for and complete the full licensing and approval process in the country.

“We are exceptionally proud of our team and the bank we have built here in Mexico,” Revolut Bank S.A., Institución de Banca Múltiple CEO Juan Miguel Guerra said. “We are very grateful to the authorities for this vote of confidence and their commitment to fostering competition in the industry, and we are confident that our offering will benefit millions of people across the country.”

Revolut is a digital banking and financial services platform that offers a wide range of solutions, including multi-currency accounts with real-time exchange rates; stock, cryptocurrency, commodity, and ETF investing and trading; as well as business accounts, corporate cards, and expense management tools. Founded in 2015, Revolut serves as a financial services “super app” for more than 65 million customers around the world.

Meanwhile, payments platform SumUp announced its official launch in Mexico this week. The company has introduced its SumUp Go card reader to the Mexican market, enabling merchants to accept payments anytime, anywhere, with no monthly fixed costs. The card reader is compatible with all major credit and debit cards and features both exceptional battery life and unlimited 4G cellular connectivity due to its built-in SIM.

“Expanding into Mexico marks a pivotal step in SumUp’s strategic growth across Latin America,” SumUp North America CEO Andrew Helms said. “We see remarkable potential in the region and recognize a strong demand for accessible, user-friendly payment solutions that streamline business operations. At SumUp, our mission is to simplify business for our merchants and we’re delighted to bring this commitment to Mexico.”

Founded in 2012, SumUp counts more than four million merchants in 37 markets as users of its payment processing solutions and business management tools. These include mobile card readers and point-of-sale (POS) systems, as well as solutions for sales tracking and inventory management, customer loyalty programs, and financial reporting and analytics.

Revolut has been a Finovate alum since its debut at FinovateEurope 2015. SumUp won Best of Show in its Finovate debut at FinovateEurope 2013. Both companies are headquartered in London.

Here is our look at fintech innovation around the world.

Middle East and Northern Africa

Oman’s BankDhofar launched its new braille debit card.

The Cooperative Bank of Oromia, a regional bank based in Ethiopia, partnered with digital transformation company JMR Infotech to go live with Oracle Financial Services Crime and Compliance Studio.

Saudi National Bank subsidiary Samba Bank unveiled its new fraud detection system powered by BPC’s SmartVista Fraud Management.

Central and Southern Asia

Mongolian fintech AND Global raised $21.4 million in Series B funding in a round led by the International Finance Corporation and AEON Financial Service.

Karandaaz Pakistan and Walee Financial Services forged a strategic partnership to launch Pakistan’s first Shariah-compliant, digital asset financing solution for female entrepreneurs.

Three of Japan’s largest banks—MUFG Bank, Sumitomo Mitsuio Banking Corp, and Mizuho Bank—announced plans to collaborate on the launch of a unified stablemcoin.

Tracxn’s recently released Southeast Asia FinTech Reportnoted that fintech startups in the region raised $839 million in the first nine months of 2025, a decline from previous years.

African all-in-one financial platform Moniepoint secured more than $200 million in Series C funding.

Sanlam teamed up with TymeBank to build a co-branded fintech super app for consumers in South Africa.

Capitec Bank partnered with accounting software company Stub to provide South African small and micro-sized businesses with direct access to their transactional data.

Central and Eastern Europe

German fintech Aifinyo AG announced that it was converting its balance sheet to bitcoin, becoming the first German firm to adopt a full bitcoin treasury model.

SoftPOS solutions company MineSec inked a Memorandum of Understanding (MoU with Turkish digital payments company Paymore.

Latvian fintech Eleving Group raised €275 million ($319.5 million) via a public bond issue.

Splitit and DXC Technology are partnering to bring AI-powered, card-linked installment payments to banks using DXC’s Hogan core banking platform, enabling personalized BNPL functionality directly from existing cards and accounts.

The collaboration will help banks reclaim BNPL market share by eliminating friction while giving institutions the flexibility to originate installment loans on their own books or through Splitit.

DXC’s bank clients will be able to embed installment capabilities within their own traditional banking infrastructure, helping them modernize, retain customer relationships, and compete on flexibility and user experience.

Georgia-based BNPL solutions provider Splititannounced it is collaborating with DXC Technology (DXC) to help banks compete on BNPL.

DXC Technology and Splitit have joined forces to bring card-linked installment payments to banks using DXC’s Hogan core banking platform. The integration enables banks to offer personalized, AI-powered installment plans at checkout or post-purchase, both online and in person, using cards and accounts customers already trust.

Hogan supports more than 300 million accounts across 40+ major banks with $5 trillion in deposits. By partnering with Splitit, banks can compete directly with BNPL providers while avoiding the friction of new account openings and serving customers who prefer to pay with debit. The collaboration aims to help banks reclaim market share lost to traditional BNPL players and deliver the flexibility today’s consumers expect.

“For decades, Hogan has been the backbone of the world’s largest banks. This partnership with Splitit shows how that foundation can now be used to create new revenue streams at the point of sale,” said DXC Global Head and General Manager of Financial Services Sandeep Bhanote. “By normalizing installment capabilities across existing accounts, we’re enabling issuers to modernize their offerings without replacing their core—and empowering consumers with flexible payments that use the cards they already trust.”

The benefits of the partnership extend beyond simply providing more payment options for end users. Banks will be able to deploy branded installment offers that appear natively at checkout or within the bank’s online banking portal. Additionally, partnering with Splitit will help DXC offer its bank clients the choice to originate the installments directly on their books or to have Splitit originate the installments.

“BNPL players have disintermediated banks by offering transactional lending at the merchant checkout. This partnership resets the playing field,” said Splitit CEO Nandan Sheth. “Together with DXC, we’re empowering banks to compete head-on with BNPL providers by bringing installments directly into existing bank accounts or issued debit cards. With DXC’s access to over 300 million bank accounts through its core banking platform, our joint technology gives financial institutions a seamless, low-lift way to automatically deliver installment functionality to existing customers. This innovation enables banks to maintain greater control of their customer relationships and attract new younger customers.”

Splitit was founded in 2012, went public in 2019, and went private again in 2023 after it was acquired by Motive Partners. The company seeks to simplify flexible payments, launching a partner program called the Agentic Commerce Partner Program earlier this month. The new initiative will allow autonomous shopping agents to make payments using card-linked installments.

While BNPL has fallen off the list of top trends in the past few years, its use has not dropped. The installment payment solution market is set to grow from $2.23 billion in 2024 to $3.44 billion by 2031, with 72% of merchants saying that they prefer card-linked installments for their simplicity and reach.

By embedding installment functionality into existing cards and core systems, DXC can help banks compete on flexibility without sacrificing customer relationships to third-party fintechs. As BNPL grows, the next wave of BNPL innovation isn’t about new entrants, but about how legacy infrastructure adapts to meet changing consumer expectations.

Deepfake detection company Neural Defend and India’s Zee News have teamed up to launch the country’s first AI-powered, deepfake verification system for news media.

The partnership will enable Zee News consumers to upload suspicious videos, audio clips, or images and have Neural Defend’s technology determine within seconds whether or not the material has been artificially manipulated.

Founded in 2024 and headquartered in San Francisco, California, Neural Defend made its Finovate debut at FinovateEurope 2025 in London. Piyush Verma is CEO.

Deepfake detection specialist Neural Defend has teamed up with Mumbai-based Zee News to launch India’s first deepfake verification system for news media—powered by AI. The new solution empowers individuals with direct access to advanced verification technology, enabling them to authenticate videos, images, and audio files in real time.

“Our goal was to ensure deepfake detection is fast, accurate, and simple for every citizen,” ZMCL Chief Technology Officer Vijayant Kumar said. “By integrating Neural Defend’s advanced AI with Zee News’ platforms, we’ve created a solution that can detect even the most sophisticated manipulations within seconds. This is not only an innovation for today, but a future-proof safeguard for tomorrow’s information ecosystem.”

The partnership will enable individuals to upload suspicious videos, images, or audio clips and have Neural Defend’s technology analyze the files and confirm their authenticity—or identify the files as artificially manipulated—within seconds. At a time when the average viewer is struggling to differentiate increasingly sophisticated manipulated content, including video, from non-manipulated content, the collaboration between Neural Defend and Zee News gives media consumers new tools to help them “separate fact from fiction in an age where misinformation spreads fast,” said ZMCL Marketing Head Anindya Khare.

“While Gen Z and younger viewers are particularly vulnerable to being misled by fake videos and audio, this initiative ensures a safe and credible space for everyone,” Khare added. “For advertisers and partners, it creates the most reliable environment to engage with audiences—where advanced technology and authenticity come together. This is the future of brand-safe and responsible media.”

Mumbai-based Zee News is one of the leading Hindi news channels in India with more than 52 million viewers. The company is owned by Indian media conglomerate Essel Group and is the flagship channel of Zee Media Corporation. Zee News is publicly traded on the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE), and has a market capitalization of $75 million.

Founded in 2024 and headquartered in San Francisco, California, Neural Defend made its Finovate debut at FinovateEurope 2025 in London. At the conference, the company demonstrated its agentic AI-powered deepfake detection solution that can be integrated into any video, audio, or image verification platform to offer real-time identity verification to EKYC firms, verification companies, banks, payments service providers, fintechs, and more. Neural Defend’s technology leverages proprietary, multi-layered AI to spot even subtle alterations and manipulations with precision. The solution also boosts security for video and audio calls by instantly detecting and mitigating deepfakes in real time.

What is supplier enablement and why does it offer businesses a way to optimize vendor payments to maximize cash flow or another business outcome? How does the revolution in data management help businesses deal with the challenge of important data that is sequestered in accounting systems? And, finally, what role do automation and AI have in opening up access to that data?

Last month at FinovateFall, I interviewed Peter Zhou, Co-Founder and CEO of Rutter. Founded in 2021 and headquartered in New York City, the company offers a unified API to help companies add accounting, commerce, and payment integrations into their B2B product workflows. A trusted integration partner for companies such as Airwallex, Mercury, and Ramp, Rutter empowers businesses to build and launch products in lending, expense management, AP/AR automation, and more.

“In the same way that companies like Plaid offer a unified API for banking data, Rutter aims to be the unified API for small business financial data. Our core systems of record that we are unifying for companies are commerce, payments, accounting, and ads data … We basically help them provide customer-facing integrations into those systems of record that their customers use.”

Rutter introduced its Supplier Enablement solution earlier this year. The new offering leverages unified ERP and payment intelligence to help businesses unlock card revenue. Supplier Enablement allows Rutter to provide support for fetching vendor data from 30+ additional mid-market and enterprise ERPs, a new intelligent file import workflow, advanced OCR enrichment that uses bill attachments to improve vendor match, and integration of Visa card acceptance data to enhance vendor scoring.

Peter Zhou is a graduate of Yale University, with both Bachelor’s and Master of Science degrees in Computer Science. Before co-founding Rutter, Zhou was a software engineer with San Francisco, California-based professional services company Atrium.

Finzly launched Agentic Galaxy, a new addition to its Galaxy suite that embeds deployable AI agents into the core of payments and operations.

The platform’s built-in AI modules automate payment processing, enhance compliance through human-in-the-loop oversight, and reduce complexity by integrating intelligence natively rather than bolting it on.

Finzly’s move reflects the broader rise of agentic and generative AI, as financial institutions adopt the same kind of intelligent automation and personalization transforming consumer shopping experiences.

Banking-as-a-Service provider Finzly announced it is adding to its Galaxy suite. The North Carolina-based company is launchingAgentic Galaxy to offer deployable AI agents that help banks bring ideas to market faster, simplify their operations, and deliver seamless customer experiences.

The new tool will leverage Finzly’s suite of specialized AI modules that offer payment processing intelligence, automate workflows, and enhance user experiences. Agentic Galaxy’s AI-powered agents help streamline operations and enable financial institutions to offer new services that integrate human-in-the-loop oversight, ensuring compliance. And because the AI agents are integrated into the product instead of being bolted on, there is less complexity and it is easier for firms to measure efficiency gains.

“Finzly’s approach to agentic AI goes beyond surface-level automation—it focuses on how intelligence can live deep within the core of payments and operations and enable new forms of modernization,” said Datos Insights Strategic Advisor, Commercial Banking & Payments Practice Gilles Ubaghs. “These are the kind of capabilities that help banks move from a defensive and reactive positioning to a more proactive form of continuous evolution.”

The AI agents can help complete tasks, resolve exceptions, and make informed decisions faster. “With agentic AI built into payments and operations,” explained Finzly Founder and CEO Booshan Rengachari, “banks can operate at speed with confidence, maintain strong governance, and focus on delivering exceptional customer experiences.”

The new tool is designed for firms looking to replace legacy systems. Agentic Galaxy offers an intelligent payment-processing core that supports multiple rails. The platform can also help non-banks in search of smarter, faster payment operations and virtual accounts.

Finzly’s flagship offering, Finzly OS, enables clients to launch a modern bank from scratch. The company’s API connects to all US payment rails, including Fed ACH, Fedwire, RTP, SWIFT, and FedNow. Founded in 2012 under the name SwapsTech, Finzly is a two-time Best of Show winner and has built its reputation on unifying payment systems and digital banking capabilities into a single, intelligent operating system for financial institutions.

This launch comes at a time when generative and agentic AI are reshaping how value is created across financial services. A recent report from Adobe for Business highlighted that traffic from Gen AI-powered tools to retail sites spiked by 4,700% year-over-year by July 2025, and that AI-driven visits are now far more engaged than traditional ones. Finzly’s new tool in its Agentic Galaxy suite aligns with this shift because it embeds AI agents into the payments and operations core, which enables banks and fintechs to act with the same agility and intention that consumer brands are exercising when they plug AI into discovery, recommendation, and checkout flows.

Generative AI-powered shopping has been gaining steam in the latter half of this year and is shaping up to be one of the top trends as we move into 2026. The availability and convenience of Gen AI tools are shifting consumers’ shopping habits away from traditional browser-based shopping as these new tools become more deeply embedded in the shopping experience.

Adobe for Business published a report earlier this year that shows momentum in the use of generative AI-powered chat services. The report, which surveyed more than 5,000 US individuals, aimed to complement a study conducted during the 2024 holiday shopping season that examined consumers’ usage of Gen AI-powered chat services and browsers.

There are six standout findings from the report that exemplify the shift in consumers’ habits.

Generative AI traffic to retail sites exploded

Adobe found that the first surge during the 2024 holiday season reached a growth of 1,300% year-over-year. Following this, the recent data shows that traffic from Gen AI-powered chat tools and browsers has continued to accelerate, reaching a 4,700% year-over-year increase as of July 2025. AI-driven visits now represent a meaningful and fast-growing share of retail shopping and research activity.

Over one-third of US consumers have used AI for shopping

According to Adobe’s 5,000-person survey, 38% of consumers have used generative AI at some point during their shopping process, while 52% plan to do so this year. Shoppers are most commonly using it for product research (53%), recommendations (40%), finding deals (36%), creating shopping lists (30%), and gift ideas (30%).

AI shoppers are more engaged and informed

Consumers that arrive at a website from AI-powered sources spend 32% more time per visit, view 10% more pages, and have a 27% lower bounce rate than those coming from traditional sources such as search, social media, and email. Shoppers using Gen AI also report an increase in satisfaction, with 85% of users saying that AI improved their shopping experience and 73% now rely on it as their primary product research tool. Overall, shoppers using Gen AI tools are more engaged than shoppers using traditional ecommerce methods.

Conversions still lag

While consumers are increasingly using Gen AI tools for browsing, many stop there and fail to actually make the purchase. In fact, Adobe’s study showed that AI-driven traffic is still 23% less likely to convert than traditional traffic. This figure has actually shown a bit of improvement over the past few months. The study showed that conversion rates were 49% lower in January 2025 and 38% lower in April 2025. This suggests that consumers increasingly trust AI-powered recommendations enough to complete purchases directly.

Revenue-per-visit from AI sources is catching up to non-AI visits

When it comes down to dollar figures, it turns out that Gen AI-powered shopping isn’t as valuable, though that is quickly changing. Adobe’s study found that AI-driven revenue-per-visit rose 84% from January 2025 to July 2025. While AI-driven visits were worth 97% less than non-AI visits in July 2024, they were only 27% less than a non-AI visit a year later. This indicates shoppers are moving from using AI purely for research to actually buying through AI-driven paths.

Mobile is fueling AI-driven shopping growth

According to the study, in July 2025, 26% of AI-driven retail traffic came from mobile. This is up by 8 percentage points from 18% six months earlier. Adobe expects mobile AI use to further close the conversion gap, given consumers’ tendency toward more impulse-driven shopping on phones.

All of these statistics paint a picture of what we can expect to happen to ecommerce in the next few years. As consumers increasingly turn to their preferred Gen AI tool when they start their shopping journey, we’re witnessing the early stages of a new kind of marketplace. In ecommerce 2.0, we’ll see discovery, recommendation, and payment converge within a single interface. Competition in this new frontier will no longer be about who owns the checkout. Rather, it will centralize around who owns the conversation that leads there. As the 2025 holiday shopping season picks up, expect to see fintechs, retailers, and payment providers racing to claim their spot in the Gen AI shopping ecosystem.

Netherlands-based digital banking experience platform Plumery introduced its Cashback Management capability this week.

The solution will help financial institutions build and launch their own cashback programs in weeks, providing real-time, personalized rewards that boost customer engagement and loyalty.

Founded in 2016, Plumery made its Finovate debut at FinovateEurope 2025 in London. Ben Goldin is Founder and CEO.

Digital banking experience platform Plumerylaunched its Cashback Management capability this week. The new offering will empower institutions to build and run personalized, real-time rewards in weeks. The cashback management capability helps firms boost engagement, NPS, and revenue.

Many financial institutions would like to offer cashback—insofar as cashback is one of the most universally recognized and appreciated loyalty schemes. Yet many legacy core systems are unable to provide it, leaving some institutions stuck with outdated rewards programs that lack both personalization and real-time responsiveness. To help institutions manage this challenge, Plumery’s Cashback Management enables them to launch modern cashback programs—from instant or scheduled credits to AI-driven reward groups—while maintaining control of compliance, costs, and the customer experience.

The new Cashback Management offering features ready-to-use cashback journeys for transaction processing, rules engine, settlement, customer user experience, and analytics. The technology’s AI module reviews purchase history and category preferences to create monthly cashback groups based on spending habits—all fully configurable to ensure regulatory compliance. And as a SaaS-first, API-driven solution, Plumery’s Cashback Management integrates with core infrastructures, card processors, and KYC/AML providers to ensure that institutions can modernize and enhance their rewards offerings over time.

“Financial institutions tell us they want to increase engagement with cashback and rewards but are blocked by legacy infrastructure,” Plumery Founder and CEO Ben Goldin said. “Our Cashback Management capability changes this. With pre-built APIs, configurable rules, and an AI personalization module all designed to be transparent, compliant, and under the institution’s full control, banks and other financial institutions can move from design to live cashback in weeks. That means stronger retention, higher spend per customer, and new revenue opportunities from merchant-funded offers—and without the vendor lock-in.”

Plumery’s Cashback Management news comes days after the company reported that it had been included as a Sample Vendor in the 2025 Gartner Market Guide for Digital Banking Platforms. Plumery also announced earlier this month that it was expanding its digital banking platform to support credit unions in Canada. The company partnered with Aequilibrium, a digital transformation consultancy and implementation services firm based in Vancouver, British Columbia, to help ensure that its platform meets the specific needs of Canadian credit union members.

“Canadian institutions have a rare opportunity to modernize on their own terms, rather than being tied to outdated systems,” Goldin said. “Our platform provides an immediate, future-ready option that puts control back in the hands of credit unions.”

Founded in 2016 and headquartered in the Netherlands, Plumery made its Finovate debut at FinovateEurope 2025 in London. At the conference, the company demonstrated its Super App Accelerator, which enables financial institutions to build and launch their own comprehensive Super App in weeks rather than years.

To learn more about Plumery, check out my interview with Ben Goldin from earlier this year.

SaaS cloud banking platform Mambu announced the launch of its composable banking approach for credit unions in North America.

The initiative will help credit unions move beyond monolithic, legacy systems and embrace a modern composable banking infrastructure that supports innovation.

Mambu also announced that it has extended its partnership with Indonesian digital bank Krom for five years.

SaaS cloud banking platform Mambu finds itself in the fintech headlines twice in a week’s time. The Europe-based fintech announced today the launch of its composable banking approach for North American-based credit unions. The initiative is designed to enable credit unions to evolve beyond legacy core systems, modernize their infrastructures, and provide their members with a more compelling digital experience. The launch news comes just days after Mambu announced that it was extending its partnership with Indonesian digital bank Krom (PT Krom Bank Indonesia).

An innovator in the field of composable banking—which relies on modular, interchangeable components rather than singular, monolithic systems—Mambu is looking to help credit unions transition from legacy systems and embrace a more modern infrastructure that promotes speed, offers flexibility, and supports innovation. In a statement, the company noted that its composable banking approach also facilitates new options when it comes to deployment, including speedboat deployment, dual core, and staged migrations. These deployment strategies enable credit unions to continue to innovate while maintaining control over the pace of the institution’s transformation.

“Credit unions are under immense pressure to keep pace with member expectations, all while operating on legacy systems that many feel hold them back,” Mambu VP of Credit Unions Amber Harsin said. “Composability is not a strategy of patching or layering complexity onto legacy systems to force integration; it’s about forging a clean, digital-first foundation that allows credit unions to scale, innovate, and serve their communities better.”

Mambu also recently announced that it has extended its partnership with Indonesian digital bank Krom (PT Krom Bank Indonesia) for five years. The collaboration between Mambu and Krom enabled the latter to launch its digital banking app in 2024.

“Mambu has proven to be a powerful partner from day one,” Krom Bank President Director Anton Hermawan said. “Our renewed partnership is a key step in Krom’s long-term strategy to build a scalable, innovative, and inclusive digital bank for Indonesians. With Mambu’s cloud-native core and the flexibility it provides, we’ve been able to launch high-impact products faster, stay compliant, and deliver a seamless experience to our customers.”

Krom’s relationship with Mambu goes back to the spring of 2022, when the digital bank selected the company as its core banking partner. Today, Krom Bank is one of the fastest-growing digital banks in Indonesia and has targeted both profitability and more than 20 million accounts on its books by 2030.

“Krom Bank is a standout example of what’s possible when bold vision meets modern technology,” Mambu Managing Director, Head of APAC Sales, David Becker said. “Its rapid growth and strong financial performance are a testament to how a cloud-native, composable core like Mambu can support scale and agility in even the most complex markets.”

Founded in 2011, Mambu most recently demoed its technology at FinovateEurope 2022 (in partnership with Persistent Systems). The European fintech has more than 260 customers around the world, 114 million end users, and its technology handles 200 million API calls per day. Fernando Zandona is CEO.