This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Reset raised $6 million in seed funding from credit union customers and partners to expand its embedded earned wage access platform for credit unions and community banks.

The company positions earned wage access as a tool to deepen relationships and grow deposits, reporting that cardholders increase deposits by 27%, maintain 36% higher balances, and generate 20% more interchange revenue.

Credit unions increasingly view earned wage access as competitive infrastructure to defend primary financial relationships against digital banks and neobanks.

Embedded earned wage access platform Resetunveiled today that it has raised $6 million in seed funding. The investment, which comes from credit union customers and strategic partners in the credit union and community banking space, boosts Reset’s total funding to more than $8 million.

Reset will use the funds to expand its sales and implementation capacity, deepen product development, and accelerate existing deployments.

California-based Reset, which aims to serve credit unions and community banks, embeds its technology directly into financial institutions’ existing technology stacks to enable members to access their earned wages on a daily basis, fee-free, via a card issued by the credit union or community bank.

“When your customers lead your funding round, there is no clearer market signal,” said Reset CEO and Co-founder Matt Dicou. “These credit unions aren’t just writing a check. They’re making a decision about where they want to take their members, their institutions, and the credit union industry. They see that Chime and other neobanks are successfully recruiting people away from credit unions today. Our credit union partners already have trusted member relationships. We give them what they need to remain the primary financial home.”

Reset anticipates that the earned wage card will help financial institutions grow direct deposits, since the more a member deposits, the more real-time funds they can access. The company said that cardholders increase deposits held at their credit union by 27% and maintain checking account balances 36% higher than before switching cards.

In addition to the earned wage feature, Reset also helps credit unions generate credit interchange revenue on cardholder’s everyday spend. The company said that its cardholders generate 20% more in credit interchange revenue for their institution.

“When a credit union invests in a fintech, it sends a message: we believe in this enough to put our name on it. Reset is solving a real problem for working members, and it’s doing it in a way that makes the credit union stronger in the process,” said Stephanie Curtis, Chief Member Experience Officer at VyStar Credit Union.

Rather than viewing earned wage access as simply another product offering, many credit unions increasingly see these tools as infrastructure to defend primary financial relationships, capture direct deposits, and compete against digital banks. As neobanks continue using faster access to money as a customer acquisition tool, features like earned wage access may become table stakes rather than differentiators.

Georgia’s Own Credit Union’s investment in Reset highlights this shift from product experimentation toward competitive infrastructure. “Our members are already looking for this, and until now, they’ve had to turn to other options,” said Georgia’s Own Credit Union CTO Kevan Williamson. “Reset levels the playing field for our members. We invested because we’ve seen what it does for members’ financial stability, and because we believe credit unions should be the ones offering it.”

While many banks are still trying to create their stablecoin strategy (or decide to pursue a stablecoin strategy), some of the largest players in payments, acquiring, exchanges, and financial infrastructure are exploring a stablecoin collaboration.

CoinDesk reported that payments giants Stripe, Visa, and Mastercard are backing a stablecoin platform, while Coinbase is considering involvement. The move could challenge the dominance that Circle and Tether have on the stablecoin industry by helping standardize digital currency routing across legacy systems

What impact will this disruption have on players in the traditional space? Here are a few implications.

Stablecoin interoperability improves

As with many new enabling technologies in banking and fintech, stablecoins are quite fragmented. Even though Circle and Tether dominate issuance, moving stablecoins across wallets, exchanges, payment providers, and legacy financial infrastructure remains complex. Additionally, there is no universally accepted framework for how digital currency moves across financial infrastructure.

While both of these factors limit mainstream adoption, a consortium backed by companies such as Visa, Mastercard, Stripe, and Coinbase could help create a common framework that makes digital currency movement feel more like existing payment infrastructure.

For financial services providers in the traditional finance (TradFi) space, this common framework could help decrease integration costs, making stablecoin connectivity easier to implement. The shared framework could lower integration costs by reducing the number of connections banks and fintechs must build and maintain. A standardized ecosystem could potentially offer more consistent routing, settlement, and compliance processes. Importantly, the standardization would mean that banks would be able to act now instead of waiting for the winning standard to emerge.

Stablecoins become infrastructure instead of products

Right now, much of the conversation around stablecoins focuses on which company issues the token used for a transaction. Consumers, however, rarely care which payment rail, settlement network, or digital asset powers their transaction. Instead, they simply expect money movement to be fast, seamless, and secure.

For banks and fintechs, this may mean that owning the token itself becomes less important than controlling the infrastructure surrounding money movement. When consumers are rails agnostic, we may start to see that the companies that facilitate routing, settlement, custody, compliance, and customer experiences gain a competitive advantage over those that issue the underlying asset.

Economics of traditional payments face new pressure

Stablecoins are likely here to stay, but they will not replace cards, wires, or ACH payments. However, if major payment players like Visa and Mastercard help introduce new stablecoin infrastructure, it could create pressure on existing payment economics. For example, cross-border payments and merchant settlement could become faster and potentially less expensive.

This increased competition, even if only viable in certain use cases, could reduce margins and force traditional financial institutions to reconsider where they create value. Because both Visa and Mastercard have a stake in traditional payments, however, they are unlikely to introduce a structure that will eliminate traditional payment revenues altogether. Instead, there will likely be gradual pressure on pricing and a shift toward monetizing new infrastructure layers rather than existing friction.

Stablecoin strategy becomes harder to postpone

It is clear that stablecoins are no longer fringe, and at this point, sitting on the sidelines becomes a strategic decision. While it used to be acceptable to treat stablecoins like an optional experiment, the involvement of established financial infrastructure companies makes it mandatory to understand stablecoins. Traditional financial institutions of all sizes need to consider if they will issue stablecoins, custody them, connect to them, or simply enable customer access.

While the “wait and see” approach is still a valid strategy, at this stage it is more of an active strategic decision instead of a passive delay. Financial institutions that choose not to participate should do so intentionally, taking into consideration which revenue opportunities, customer segments, and payment flows they may be willing to forgo if adoption accelerates.

Finovate’s Fintech Rundown is back with the fintech headlines you need to know as the working week begins!

We’ve got news of a funding in the consumer financing world, new products for financial wellness and credit trading, a collaboration in the money movement market and more. Be sure to check back all week long for the latest in fintech headlines.

Financial wellness

The US arm of BMO launches an new app developed by MSN Holding, DollarGPS, to help users improve their financial health.

Lending

Egyptian Buy Now, Pay Later firm Blnkraises $37 million in combined debt and equity funding.

TP ICAPunveils new credit trading and data platform, RealQ.

Credit intelligence platform OctusacquiresLevPro, a front-office software provider for public and private credit markets.

Agentic AI

Spend management software provider ExpensifylaunchesExpensify MCP, a new integration that enables AI assistants and other MCP-compatible clients to securely access Expensify data via natural language queries.

This week’s edition of Finovate Global looks at recent fintech headlines from the Eastern European nations of Bulgaria, Albania, and Hungary.

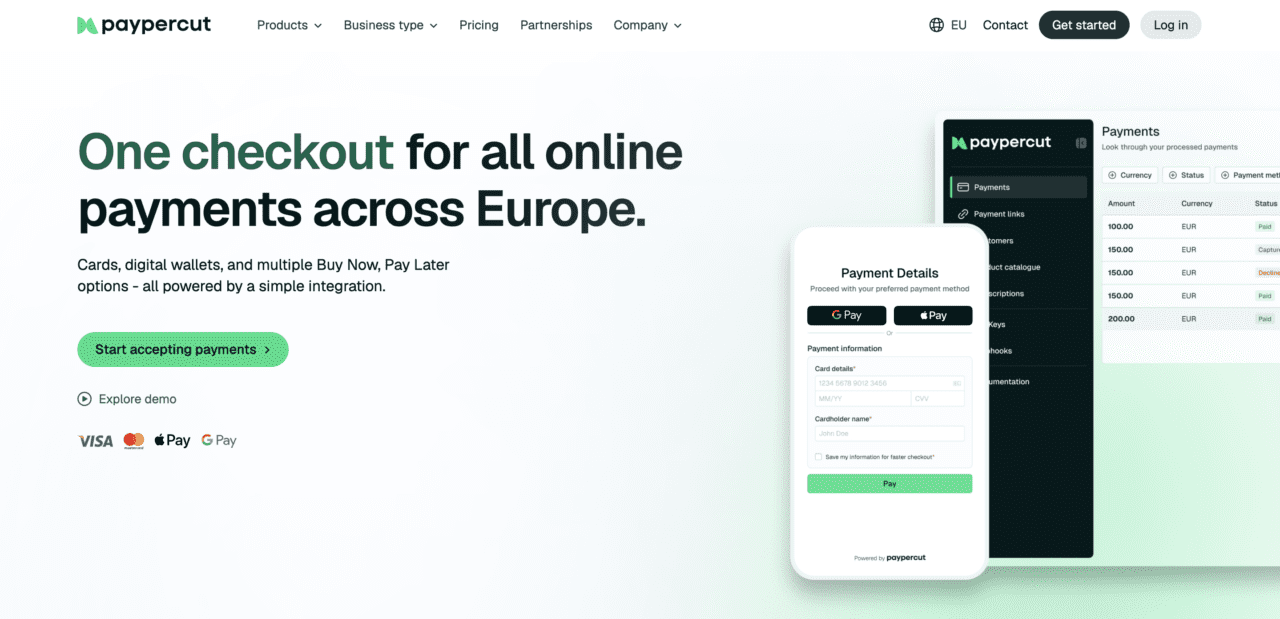

Bulgarian Fintech Paypercut Raises €5M

Paypercut, a fintech based in Sofia, Bulgaria, has secured €5 million in seed funding. The round was co-led by Concentric, Passion Capital, and Araya Ventures, and featured participation from additional investors including SMOK Ventures, Portfolio Ventures, BrightCap Ventures, BlackWood, SABAH.fund, MFG Invest, Main Set, and Matt Doka, a payment entrepreneur. Paypercut’s total funding now stands at €7 million.

Founded in response to the fragmentation of payments in Central and Eastern Europe, Paypercut has grown from a Buy Now, Pay Later aggregator into a more comprehensive payments platform. The company offers merchants access to card payments, local payment options, Buy Now Pay Later products, payment links, QR code payments, multi-currency settlement, and billing tools via a single integration. Paypercut raised €2 million in pre-seed funding in July 2025 and has onboarded more than 200 merchants in eight CEE markets since that time.

This week’s investment will help fuel Paypercut’s continued expansion across Central and Eastern Europe. The funding will also enable the firm to meet the capital requirements for an EMI license with the Central Bank of Ireland.

“CEE has always been treated as an afterthought by the payments industry, seen as too fragmented, too many local specifics, too complicated,” Paypercut Co-Founder and CEO Stoil Vasilev said. “We built Paypercut to fix that. This round gives us the resources to go further and faster: more markets, more payment options for merchants, and the infrastructure to move money in the way it should have always worked, instantly and at a fraction of the cost.”

In addition to its merchant payments operation, Paypercut is also developing stablecoin-based infrastructure for cross-border transfers in the region. The company will initially target high-volume corridors such as those between the Euro and the Polish Zloty (EUR-to-PLN) and the Euro and the Romanian Leu (EUR-to-RON).

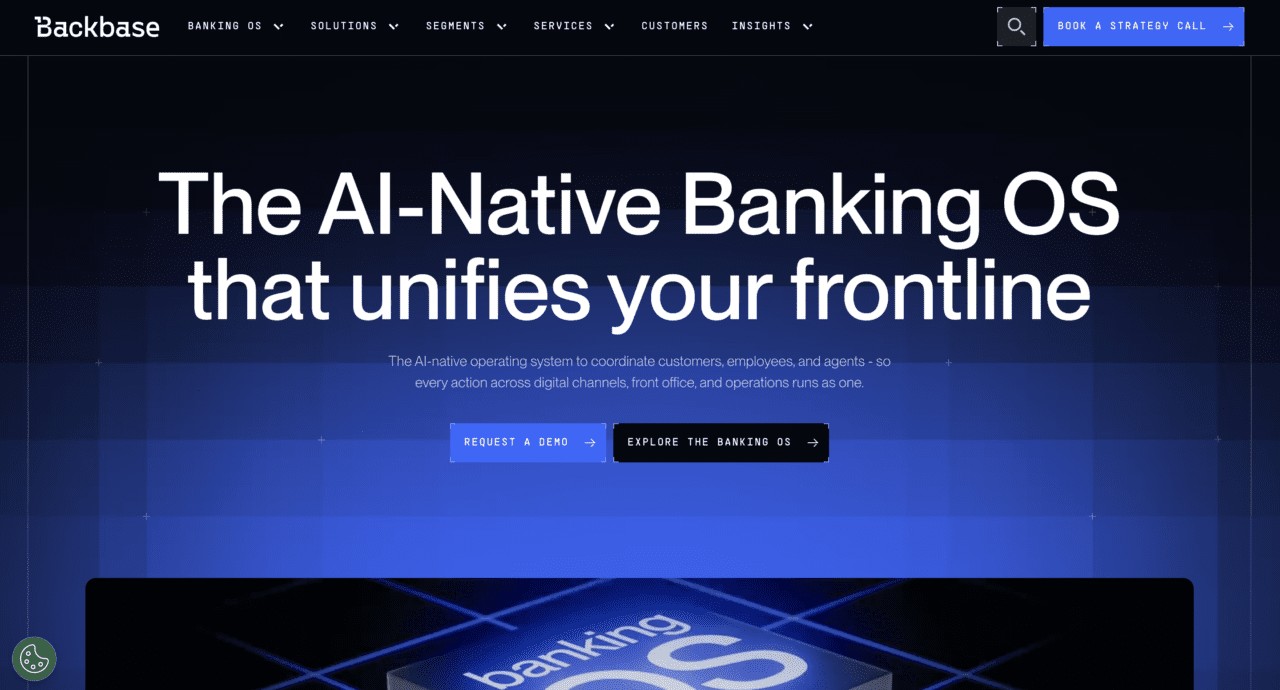

Albania’s Tirana Bank Goes Live with Backbase

Tirana Bank, named “Best Bank in Albania” in 2025 by Euromoney, has gone live with a “complete omnichannel retail banking experience” built on the Backbase AI-native Banking OS. The launch covers accounts, deposits, online loan and credit card applications, internal and outgoing transfers, card management, billpay, and financial insights. Tirana Bank will also enable Digital Assist in the employee app.

“This launch marks a significant step in our digital transformation journey, as we continue to invest in solutions that bring real, everyday value to our customers. TiBank+ is designed to deliver a seamless and intuitive banking experience, combining convenience with the trust and human connection that define our model,” Tirana Bank Chief Retail Business Officer Lila Canaj said. “Through our partnership with Backbase, we have accelerated this transformation, bringing to market a modern and scalable platform built to evolve with our customers’ needs.”

One feature that Tirana Bank anticipates its customers will appreciate is real-time spending insights, courtesy of Backbase’s personal finance management capabilities. Offering customers these insights is not a common occurrence in the region and will help Tirana Bank differentiate itself from its competitors. The institution is also going live with Apple Pay, becoming one of the few Albanian banks to offer the service via a mobile app.

“Albania is on its path to EU membership, its government has made digitalization a national priority,” Backbase Regional Vice President for South East Europe Robert Mihaljek said. “Tirana Bank looked at that moment and decided to lead it. They came to us with a clear ambition. Twelve months later, they are live with not only an MVP but a full retail APP. This is a first for Albania, and a reference for the Balkans.”

A four-time Finovate Best of Show winner, Backbase has been a Finovate alum since 2009. The Amsterdam-based fintech offers an AI-native banking operating system that converts fragmented banking operations into a unified frontline for the benefit of customers and employees alike. Founded in 2003, Backbase counts more than 150 leading banks and financial institutions around the world as users of its solutions for retail, small business, commercial, and private banking, as well as wealth management. Riddhi Dutta is CEO.

Can Crypto Make a Comeback in Hungary?

For many observers, liberal democracy was one of the big winners in the recent Hungarian election that saw the end of the Orbán regime. But could the victory of Péter Magyar and his pro-EU Tisza Party also be a good sign for crypto and digital assets in the country?

In 2025, Hungary announced an amended Crypto Act that criminalized unauthorized exchange services and established a validation regime on all crypto-to-fiat and crypto-to-crypto transactions. This incentivized some firms, such as Revolut, to withdraw from the Hungarian market entirely, while others suspended services due to regulatory uncertainty.

This also set off a confrontation with the EU, with the European Commission initiating infringement proceedings against Hungary’s validation regime, saying that it was in conflict with the EU’s MiCA framework. Interestingly, Orbán had previously been relatively pro-crypto, with his regime offering some of the lowest tax rates on crypto in Central Europe. This made Hungary—at least before 2025—an attractive jurisdiction for retail crypto investors in the region.

There are many reasons offered to explain the shift toward a more restrictive attitude in recent years—from the influence of MiCA and its mandates to the regime’s well-known preference for state control and supervision of key financial and industrial activities. But the question now is whether or not new politics will result in new policy? The correct answer, at this point, is that no one knows. What some observers have noted, however, is Magyar’s relatively more pro-EU stance on other issues and his general interest in re-aligning with European institutions more broadly. To this end, even something as straightforward as revising the country’s crypto policy to match MiCA’s mandates—and remove or revise current criminal penalties for policy violations— might be an initial positive sign toward restoring crypto’s status in Hungary.

Here is our look at fintech innovation around the world.

Central and Southern Asia

India travel fintech Scapia, which combines co-branded cards with travel booking, secured $63 million in funding in a round led by General Catalyst.

Raqami Islamic Digital Bank Limited (RIDBL) has been granted a Retail Banking License by the State Bank of Pakistan.

Via its Alipay+ gateway, Singapore’s Ant International announced the launch of cross-border mobile payment services in Latin America.

ACI Worldwide looked at the impact of real-time payments on growth in Peru, Chile, and Argentina.

Tearsheet profiled Brazilian digital financial institution Agibank.

Asia-Pacific

Singapore-based Crypto payments network Moonpay and controlling shareholder Seoryong Electronics announced a joint investment in Korean fintech Finger.

Vietnam Bank OCB selectedBackbase AI lead Chris Shayan as its Acting CEO.

African financial infrastructure company Anchor launched its Anchor MCP Server, becoming the first Nigerian fintech to make. its API documentation natively available to AI systems.

The Africa Report reported on the rise of mobile money in Ghana and how it is challenging the country’s incumbent banks.

Business Insider Africa looks at the fate of small business banking platform Brass which announced that it will be migrating its customers to Paystack Microfinance Bank.

Central and Eastern Europe

PayPalintroduced a pair of Buy Now, Pay Later products for its customers in Austria.

Ripplelaunched its RLUSD stablecoin in Turkey courtesy of partnerships with local platforms BiLira, Bitexen, and Bitlo.

Equifax UK forged a partnership with Polish credit bureau BIK to boost access to identity verification and fraud prevention technology.

Middle East and Northern Africa

Saudi Arabia-based fintech Stitch announced a pivot to focus on infrastructure and offering a financial operating system for banks.

UAE-based fintech Comfi AI secured pre-Series A funding from Yango Group’s Yango Ventures.

Cash App launched Cash App Tags, NFC-enabled, payment “accessories” that let customers pay without their phone or card.

The first of these new tags comes in the form of a wand, but the company said that other form factors will be available in the future.

While payments companies have tried and failed to move the payments form factor from cards and phones, the wands may succeed because they are visible, social, and impossible to ignore.

Cash Appannounced a new payment form factor yesterday that is so outrageous it would have dropped the jaws of payments executives in 2014 to the floor. The payments company unveiled the first release of Cash App Tags, NFC-enabled, payment “accessories” that let customers pay without their phone or card.

The pilot Cash App Tag comes in the form of a pearlescent wand, aptly called Cash App Wand. Eligible users ages 13 and up with an active Cash App Card can activate their wand by linking their wand to their Cash App Card using the Cash App on their phone. Once the wand is activated, customers can tap to pay without holding a phone or card.

The new form factors will work where Visa tap-to-pay is accepted and there are no minimum balance or activity requirements. Just like Cash App’s payment cards, Tags offer real-time transaction alerts, 24/7 fraud monitoring, and the ability to instantly lock, unlock, and deactivate them within the app.

Odds are that if you’re reading this, Cash App’s Tags aren’t marketed to your demographic. The company explicitly designed them for Gen Z customers as a new form of expression and for use in situations where phones aren’t allowed or are too cumbersome to pull out of a bag. Cash App is anticipating that users will want to collect them like Labubu dolls. In a recent survey of Gen Z consumers, the company found that 38% of this generation purchases collectibles, accessories, or limited edition items at least monthly.

“While digital wallets are invisible and physical cards are often buried in wallets, Cash App Tags are just the opposite,” said Block Hardware Lead Thomas Templeton. “We see a unique opportunity here to make payments visible and social for the first time. Early testers have told us that they’ve loved carrying the Wand and showing it off at checkout, so we believe there’s a real appetite for this among our customers”

The Cash App Wand is now available for $25 in the app, and the company plans to release limited runs of new designs in the coming weeks. “We see this as an early starting point for Cash App Tags. The number of form factors we can create is nearly limitless,” added Templeton. “From clothing to jewelry, almost any item can become a way to pay with this technology. We’re looking forward to hearing what our customers want to see next.”

I can’t decide whether I love this or hate this. Payment companies have tried for over a decade to move the payment form factor from the phone to a ring, fitness band, and even a Timex watch, but each effort has failed to gain traction. At the same time, the industry has been hyper-focused on making payments invisible, and this is the exact opposite. Perhaps moving the form factor to something as outrageous as a wand will succeed because it is visible, social, and impossible to ignore.

Digital financial services software company Finastra unveiled its new analytics solution for lenders this week, Data Insights 2.0.

Available for Finastra’s mortgage origination solution, Originate Mortgagebot, Data Insights 2.0 gives lenders a comprehensive view of the borrower journey through the application process to identify areas of friction and applicant drop-off.

Finastra was formed via a merger between Finovate alum Misys and D+H in 2017. Chris Walters is CEO.

A new analytics solution offered by Finastra will help mortgage lenders convert more applications into funded loans. The new tool, Data Insights 2.0, is available for Finastra’s mortgage origination solution, Originate Mortgagebot, and gives lenders an accurate view of the borrower journey through the mortgage application process to identify where applicants tend to drop off. Data Insights 2.0 helps lenders pinpoint performance gaps to enhance their own processes, and features peer and industry benchmarking based on anonymized data from 1,000+ mortgage originators to allow them to measure their performance against the market.

“We knew we were losing applicants at specific points in the process, but we couldn’t figure out why,” United Bank VP and Mortgage Production Manager Brenda Stoerkel said. “Data Insights showed us exactly where the process was breaking down. By fixing our mobile experience and adjusting our communication timing, we saw our completion rates improve. Having the right information to make better decisions makes both our operations and our borrower experience stronger.”

Data Insights 2.0 offers real-time application exit point tracking as well as conversion analysis and geographic heat maps of application activity. The technology also provides insights into borrower demographic profiles, performance metrics for credit score distribution channels, and submission timing analysis. This will enable lenders to identify areas of friction in the application process better—including hard-to-understand forms, slow response times from the system, or a poor mobile experience—enabling them to accelerate approval timelines, enhance communication, and deliver a better experience for applicants. Data Insights 2.0 also provides peer benchmarking against industry standards to deliver a market-wide context for performance. These metrics—including applicant exit points, conversion rates, loan-to-value ratios, and more—enable lenders to move quickly from insight to action.

“Lenders have access to a considerable amount of data, but they need real insights to help them optimize their business,” Finastra Chief Product Officer for Lending Rick Foresta said. “We built Data Insights 2.0 to cut through the noise. It tells you what’s actually happening in your mortgage pipeline and what you should do about it to make it easier for people to buy homes.”

Formed via a merger between Finovate alum Misys and D+H in 2017, Finastra provides financial services software to more than 7,000 customers, including 40 of the world’s top 50 banks. Active in more than 110 countries around the world, the London-based company offers solutions for lending (LoanIQ and LaserPro), payments (Global PAYplus and Payments To Go), and universal banking (Essence), facilitating $7 trillion in transaction value daily.

As financial institutions increasingly deploy AI across customer service channels, many are wondering where they should start.

At FinovateSpring in San Diego earlier this year, I spoke withCresta Director of Customer Success Stacy Osorio about how banks, credit unions, and fintechs should think about customer experience, contact center transformation, and AI-driven automation.

One of the biggest opportunities, Osorio explained, is not simply using AI to reduce costs, but leveraging it to improve customer experiences while helping organizations better understand what is happening across customer interactions.

“Looking at customer experience through that lens, they should be thinking about the role of AI in customer experience transforming your contact center to think about ways to use AI to drive additional revenue, helping to drive that customer experience—whether that’s driving satisfaction or helping coach and innovate different ways or more automation through your AI agent,” Osorio said when discussing how financial institutions should think about AI-powered customer experience.

Osorio also noted that financial institutions should think beyond conversational AI and consider how AI can automate workflows, surface insights from customer interactions, and help human agents have better conversations.

Stacy Osorio serves as Director of Customer Success at Cresta, where she works directly with enterprise customers to help them optimize customer experiences and maximize value from AI-powered customer engagement tools.

Founded in 2017, Cresta offers an AI-powered contact center platform designed to help enterprises improve customer conversations, automate workflows, coach human agents, and better understand customer interactions. The company works with enterprise organizations across industries, including customers such as United Airlines, Cox, Acorns, and others. Cresta’s platform combines conversational intelligence, workflow automation, and AI agents to help organizations improve customer experiences while increasing operational efficiency.

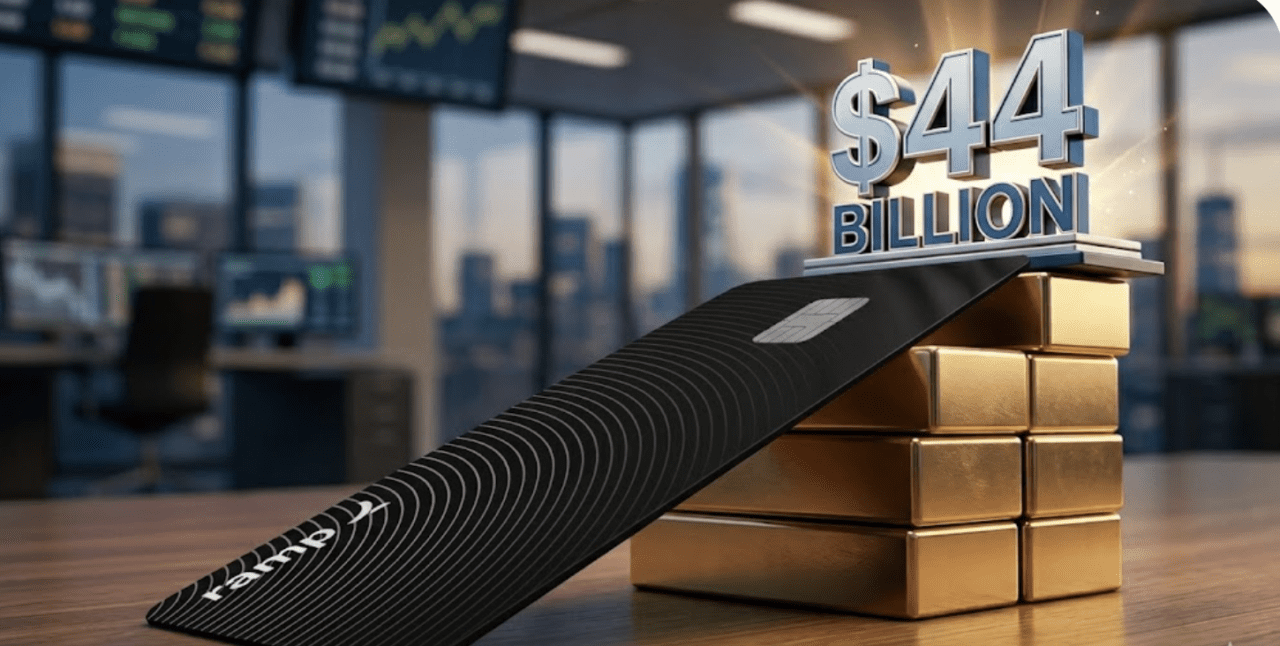

Ramp raised $750 million at a $44 billion valuation as it expands beyond corporate cards and expense management.

The company is betting AI token spend will become a major business cost category requiring new financial infrastructure.

Ramp launched Stack, an AI-native accounting platform, as it pushes deeper into automation, accounting, and enterprise finance.

Corporate card and expense management platform Ramp is on a roll this week. In addition to launchingStack, an AI-native platform for accountants, the New York-based company also raised $750 million at a $44 billion valuation.

The $750 million boosts the company’s total funds to $3.75 billion, following its most recent raise of $300 million in November of last year. Investors in this week’s round include new contributors Goldman Sachs Alternatives, D.E. Shaw & Co., Morgan Stanley Investment Management, Generation Investment Management, Insight Partners, and BroadLight Capital, as well as previous investors Founders Fund, Lightspeed Venture Partners, D1 Capital Partners, T. Rowe Price, General Catalyst, Alpha Wave Global, 137 Ventures, Thrive Capital, Coatue, Sands Capital, Khosla Ventures, 1789 Capital, Avenir Growth, BoxGroup, 8VC, Pinegrove Venture Partners, Definition Capital, and Stripes.

The investment comes as Ramp positions itself as financial infrastructure for AI spending by expanding into managing one of the fastest-growing costs in business: tokens.

“For 500 years, business ran on two pillars of spend: people and vendors. In the last 24 months, a third arrived—intelligence, paid by the token and invisible to every system we’ve built to manage cost. Ramp is the infrastructure for the third pillar,” said Ramp Co-Founder and CEO Eric Glyman.

As businesses embed AI into workflows, employees and agents are generating growing volumes of token-based costs across models, copilots, and automated workflows. Ramp is betting companies will increasingly need tools to monitor, control, and optimize those costs just as they do traditional employee and vendor spending.

The round also comes days after Ramp launched Stack, a tool that allows customers to use agents to do reconciliations, update schedules, post journal entries, and create flux analyses. This creates value for accountants, as it has pre-built integrations that connect to every system their clients use, offers a full audit trail on every action, and provides an underlying model that handles a wide range of accounting tasks.

Some analysts claim that Ramp is overvalued at $44 billion, as it well exceeds competitor Brex’s valuation of $5.15 billion when it was acquired by Capital One earlier this year. It also exceeds PayPal’s valuation of nearly $38 billion.

However, Ramp is defending its value based on its past platform growth and current trajectory. In the past few months alone, Ramp has launched more than 70 products and major features. In addition to token spend management and Stack, the company released budget tools, procurement agents, accounting agents, and customized tools for startups. Also, Ramp closed two acquisitions and announced geographical expansions into the UK and Europe.

“We’re growing as fast as we were three years ago, at roughly twenty times the size,” said Glyman. “And that’s because finance is going through the biggest structural change since the spreadsheet. Every company needs infrastructure to navigate an AI economy, from a CFO in London to an accounting firm in Wichita. While we’re growing fast, we still only serve a fraction of the market. There’s a lot more work to do.”

Whether Ramp’s valuation proves justified remains to be seen. But the company’s recent product launches and messaging suggest it is attempting something larger than expense management. Rather than positioning itself as a corporate card company, Ramp is betting that businesses entering an AI economy will need new financial infrastructure to manage not only employees and vendors, but also increasingly autonomous systems and the costs they generate.

The recent crisis involving Bilt, a fintech that specializes in rent-payment rewards, is almost a perfect storm of the challenges faced by fintechs, banks, regulators, and their customers when it comes to third-party partnerships and their discontents.

This week, the Consumer Financial Protection Bureau (CFPB) reported that it had met with Bilt to discuss the issues surrounding the flawed transition process when its partnership with Wells Fargo ended in February of this year. The two companies had been working together since 2022 to offer the Bilt Mastercard. When the partnership ended, Bilt struggled to efficiently move customers into its new Bilt 2.0 structure. Customer complaints were rampant: rent and mortgage payments were returned, delayed, or debited without reaching intended recipients. Card declines were reported amid general confusion about the new arrangement. Massachusetts Senator Elizabeth Warren, who took an early interest in the problem, said that there had been a 1,300% spike in CFPB complaints due to the problems of the Bilt transition.

The CFPB’s statement today expresses confidence in the steps Bilt is taking to remedy the situation, including “reimbursing fees for more than 500 newly identified customers from its outreach following discussions with the CFPB.” The agency also noted that it would “continue monitoring Bilt’s efforts until it is satisfied that full redress will be provided and will share another update at such time.”

What are some of the biggest takeaways from Bilt’s breakup with Wells Fargo and its complaint-ridden transition process?

Partnerships are hard, breaking up can be harder

For all the understandable concern about making fintech/bank partnerships work, there is relatively little discussion about what fintechs should do—or need to do—when a partnership is ending to ensure that the transition does not negatively impact customers or damage relationships with other partners.

Arguably, this is the biggest single takeaway from the Bilt breakup and transition: whether it is because of a regulatory decision, a business challenge, or a bank failure, when transitions out of these partnerships go poorly, the negative impacts tend to fall disproportionately on consumers. There is also some question about who bears the responsibility of protecting customer data and funds during transitions. As such, when these events occur, they can have an industry-wide impact on consumer trust toward fintechs and can blunt innovation by making new technologies and services seem risky to end users and potential partners.

The human touch helps in a crisis

Even though there were reportedly issues with customers accessing live customer support due to “high volumes,” the fact that many Bilt customers were steered toward AI chatbots to resolve issues was a operational and, potentially reputational, mistake.

On the operational level, many customers reported that AI chatbots were unable to answer their questions or provide basic information, let alone resolve specific complaints. Reputationally, this can leave an impression that a firm does not care about effectively triaging customer problems, even if it is understandably not able to solve some problems immediately.

This is also a reminder that human agents that can respond with authentic empathy to confused and frustrated customers are still valuable at a time of increasingly agentic customer care.

Regulatory clarity requires regulatory authority

The lack of regulatory clarity about the ultimate responsibility for safeguarding consumer data and capital during transitions like the one involving Bilt and Wells Fargo is a real problem.

But this lack of clarity is compounded when the disposition of the regulatory body itself is difficult to discern. In its statement, the CFPB underscored its preference for a “collaborative process” rather than what is called a “protracted investigation, followed by a public enforcement action, which could be litigated for years before consumers get any redress.” This, plus a swipe at the Biden-era CFPB director Rohit Chopra, suggests that the CFPB prefers to pursue a less confrontational approach when it comes to holding companies accountable when their actions harm consumers.

This is perhaps better than no approach at all. Recall that the Trump Administration in February 2025 launched a near-shutdown of the CFPB, stopping all enforcement actions, halting new and ongoing investigations, and even locking staff out of buildings. Many of the administration’s actions have been put on hold by a federal court judge ruling in 2025, and oral arguments on a lawsuit challenging the administration’s actions against the CFPB were heard this February. In the meantime, a slimmed-down CFPB has changed its mission to focus on what it calls issues of “clear consumer harm, particularly fraud affecting servicemembers and veterans.”

How well this approach will serve the consumers harmed by the next failed fintech/bank partnership remains to be seen.

Digital banking provider Bankjoy announced that its personal finance platform JoyCompass is now deployed with 30 community financial institutions.

Embedded directly into users’ digital banking experience, JoyCompass is designed to help boost financial wellness while giving community financial institutions valuable data to help them deepen client engagement.

Bankjoy made its Finovate debut at FinovateFall 2016 and most recently demoed its technology at FinovateFall 2023. Michael Duncan is Founder and CEO.

A year after digital banking provider Bankjoyintroduced its next-generation personal finance platform, JoyCompass, the solution continues to see broad adoption by community banks and credit unions. Designed to help community financial institutions (CFIs) boost growth via client engagement, JoyCompass is embedded into users’ digital banking experience, supporting financial wellness while providing CFIs with data that helps them increase client engagement and total relationship value. Today, Bankjoy announced that a total of 30 CFIs are now using the platform, including Ellafi, CommunityWide, Advantage Plus, Statewide, Lewis Clark, OU FCU, and SIU CU, among others.

“Community financial institutions have a unique opportunity to differentiate themselves through digital banking experiences that are personal, proactive, and impactful. JoyCompass is helping our clients do exactly that,” Bankjoy Co-Founder and CEO Michael Duncan said.

Bankjoy noted that members using JoyCompass’ spending analysis functionality experienced retention gains of nearly 10% (93% vs 83.8%). Members who created a goal using JoyCompass saw retention gains of nearly 15% (98.5% vs 83.8%), and members who created a budget using JoyCompass experienced retention gains of more than 16% (100% vs 83.8%). These statistics, the company noted, mean deeper relationships with members and reduced churn.

“We were looking for different ways to help our members manage their finances,” said Dillon Tardiff, VP of Marketing and Digital Products at Ellafi Credit Union. “Having JoyCompass within our digital banking, powered by our own data, is just phenomenal. Having it right there is so easy, it helps members track goals and make progress on whatever matters most, whether paying off debt, saving for maternity leave, or other life events.”

Bankjoy’s offering comes as financial literacy continues to be a problem for many consumers. According to a report from Accenture, 40% of customers admit to lacking basic financial knowledge, with 88% of Gen Z and Millennial consumers saying they would like to expand their financial literacy. Additionally, 72% of customers value personalization in their banking options even as many community financial institutions remain unable to offer highly personalized experiences.

In response to this, Bankjoy’s JoyCompass offers a comprehensive financial wellness platform that features personalized education tools, a financial health scoring system, and gamification strategies to make challenging financial concepts and ideas easier to understand.

“JoyCompass enables growth by delivering on the original mission that made community banking special through the branch, now accomplished digitally: building meaningful, personal relationships and helping people succeed financially,” Duncan said when the solution was launched in May 2025. “JoyCompass solves the engagement challenge through gamified financial wellness tools that members actually want to use, delivering value for users and critical data for financial institutions. It creates a virtuous cycle that benefits both the client and the institution.”

Bankjoy made its Finovate debut at FinovateFall 2016 and most recently demoed its technology at FinovateFall 2023, where it showed how its platform is helping neobank Panacea Financial deliver financial services for medical professionals. Founded in 2015 and headquartered in Royal Oak, Michigan, Bankjoy also recently announced that four Corelation-core credit unions have renewed their partnerships with the fintech over the past three months. Bankjoy was recognized as the first Corelation Certified partner in 2021.

Financial crime innovator AMLYZE announced this week that fellow Lithuanian company WALLETTO has selected it to strengthen its anti-money laundering (AML) and counter-financial terrorism (CFT) capabilities.

AMLYZE was founded in 2019 to help fight financial crime with a range of SaaS-based products that cover real-time and retrospective transaction monitoring, customer risk assessment, AML/CFT investigations, sanctions, PEP, and adverse media screening.

WALLETTO will integrate AMLYZE’s AML/CFT platform to help reinforce its compliance framework. WALLETTO will leverage the full AMLYZE product suite, including Transaction Monitoring, Customer Risk Assessment, AML Investigations, Customer Screening, and Payment Screening.

“At WALLETTO, maintaining the highest standards of compliance, security, and operational resilience is a fundamental part of our long-term growth strategy,” said WALLETTO Member of the Management Board Migle Soltysiak.

WALLETTO was founded in 2017 to offer solutions for card issuance, acquiring, and electronic payments such as SEPA and SWIFT services. The company is an e-money institution (EMI) regulated by the Bank of Lithuania and holds partnerships with Visa and Mastercard to help businesses scale their payments services without having to worry about compliance.

For AMLYZE, which demoed at FinovateEurope 2024, partnering with WALLETTO will help it expand into the Baltic region. “Welcoming WALLETTO to our client portfolio is a particularly meaningful milestone for us,” said AMLYZE CEO and Co-Founder Gabrielius Erikas Bilkštys. “WALLETTO is one of the largest fintechs in Lithuania, and this partnership reflects our commitment to the Baltic market, which we consider our home. We are proud to be the compliance partner of choice for leading institutions in this region and to continue growing our portfolio of clients served here.”

The partnership comes as compliance infrastructure is becoming not only a regulatory requirement but also a competitive differentiator. As fintechs expand internationally, launch additional payment capabilities, and face more regulatory scrutiny, demand is growing for specialized platforms capable of managing complex financial crime workflows. For AMLYZE, landing one of Lithuania’s largest fintechs shows that newer compliance providers can increasingly compete for traditional financial institutions rather than only smaller customers.

Concentrix Corporation and Napier AI are teaming up to help companies enhance their anti-money laundering and counter-terrorism financing operations.

Integrating Napier AI’s compliance platform into Concentrix’s network of financial crime capabilities will enable businesses to boost their fraud prevention efforts with banking-grade, AI-powered solutions.

Napier AI made its Finovate debut at FinovateEurope 2018. The London-based financial crime prevention specialist was founded in 2015. Greg Watson is CEO.

The collaboration adds Napier AI’s compliance platform to Concentrix’s network of financial crime and regulatory technology capabilities, leveraging intelligent transformation, data, and operational excellence to enable companies to transform their fraud prevention and financial crime operations with banking-grade, AI-powered AML and sanctions screening capabilities. The partnership will help companies detect and stop financial crime with greater accuracy and speed, reduce the risk of false negatives, lower the number and frequency of false positives, use automation and intelligent workflows to streamline compliance processes, and enhance regulatory reporting and audit readiness.

“Nobody should have to choose between effective compliance and business growth,” Napier AI Head of Asia Pacific Ron Mullins said. “By partnering with Concentrix, we’re combining cutting-edge AI technology with global scale and transformation expertise to help organizations across ANZ rethink how they approach financial crime—making compliance smarter, faster, and more trusted.”

Designed for banks and credit unions, the collaboration will also benefit Tranche 2-impacted firms such as real estate agents, accountants, legal practitioners, and other professional service providers. These entities are expected to be subject to AML and counter-terrorist financing (CTF) regulations once Tranche 2 of Australia’s Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) reforms is fully implemented. Tranche 1 of the framework, which focuses on traditional financial institutions like banks, credit unions, and money transfer services, was implemented in 2006.

“Financial crime compliance is at a pivotal moment in ANZ, where institutions must balance increasing regulatory demands with the need to deliver seamless customer experiences,” Concentrix GVP of Growth for ANZ Dhiraj Kumar said. “Our collaboration with Napier AI enhances our broader ecosystem of capabilities, strengthening our ability to deliver intelligent, tech-powered solutions that help clients stay ahead of financial crime while driving operational efficiency and innovation.”

A global technology company, Concentrix Corporation helps more than 2,000 clients solve business challenges via a combination of unique data and insights, deep industry expertise, and advanced technology solutions. An intelligent transformation partner and member of the Fortune 500, Concentrix serves companies in verticals ranging from banking and financial services to healthcare, e-commerce, energy, transportation, and more. The firm recently unveiled its immersive experience center, iX360: a hands-on environment that gives clients the opportunity to see technology in action and understand how it supports customer and operational needs.

Napier AI made its Finovate debut at FinovateEurope 2018. At the conference, the company demonstrated its customer screening and transaction monitoring enhancement software, which boosts the performance of legacy AML and client screening solutions. The company’s flagship solution, the Napier AI Continuum platform, integrates multiple compliance solutions into a single dashboard and provides cloud-native, API-first architecture to ensure low-latency performance without disruption during transaction spikes. Founded in 2015, Napier AI today is trusted by more than 100 institutions around the world, with clients including Banco do Brasil, NVIDIA, and State Street. Greg Watson is CEO.