This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Behavioral Biometrics Specialist BioCatchRaises $30 Million in New Funding.

Gro SolutionsPartners with 4Front CU, NBKC to Ease Onboarding, Support National Rollout.

Around the web

Nordic digital lender Folkefinans choosesMambu’s SaaS core banking engine.

BBVA Compassopens up its Express Personal Loan solution to both customers and non-customers.

American Banker highlightsKasasa. Come see Kasasa’s latest tech at FinovateSpring in May.

OurCrowdexpands global operations, opens office in London.

Authy’s TwiliolaunchesFlex, a programmable contact center.

Ohio Healthcare FCU selectsDigital Onboarding to maximize member engagement rates.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Best of Show winner Tink has forged a partnership with BNP Paribas Fortis that will integrate its aggregation, PFM, and payment initiation technology into the Belgian bank’s mobile banking applications. The integration will enable the aggregation of all financial data typically available on mobile banking apps and pave the way for new offerings for customers pursuant to the EU’s new, payment services directive (PSD2).

“We are beyond excited to partner with such a forward leaning bank as BNP Paribas Fortis,” Tink CEO Daniel Kjellén said. “Our product is in great hands since we share the view on how the future of open banking will be.”

In a statement, Tink said the first stage of the partnership will include the release of a new, multi-banking app for Hello Bank! in the summer of 2018. Tink and BNP Paribas Fortis will collaborate on updating the bank’s Easy Banking mobile app by the fall.

“The partnership is proof of a retail banking market that is becoming fully transparent and customer centric, where the innovators who choose to invest early in technology will gain insights that can attract new customers and expand existing ones,” Kjellén said.

BNP Paribas Fortis CEO Max Jadot said that collaboration with “successful FinTechs” and integrating those technologies into their ecosystem was “part of the DNA” of the bank. “We strongly believe that technology and changing legislation, such as PSD2, offer exciting opportunities for banks and their clients,” Jadot said. “Clients of banks can expect increased convenience and remain at all times in control of their data.”

A subsidiary of BNP Paribas founded in 1990, BNP Paribas Fortis is the largest bank in Belgium, and is the latest bank to partner with Tink. The Swedish fintech made agreements with Nordea, Nordnet, and fellow Finovate alum Klarna in 2017, and added SEB and ABN AMRO as partners in 2016.

Tink demonstrated its technology at FinovateEurope 2017, winning Best of Show for its independent PFM app that combines aggregation and account information with payment initiation services. Last fall, the company picked up an investment of $16.5 million in a round that brought its total capital to $30.5 million. Founded in 2012 and headquartered in Stockholm, Tink earned a spot on CB Insights’ Fintech 250 list last summer. The company has 50 employees and more than 400,000 Swedish users of its app.

Our first, four-day conference in Europe is a wrap! And once again the Finovate twitter feed @Finovate was a great place for attendees and online onlookers alike to express their thoughts about our two days of live demos followed by another two days of deep dives and discussions on top fintech trends.

For those who missed it – and for those who’d love to relive the magic of #Finovate from the week that was – here’s a short sampler of the Twitter conversation from last week’s event.

We hope you have as much fun reading it as our Twitter followers – now at more than 40,000 – had in tweeting it!

And remember to follow us on Twitter @Finovate to stay up-to-date on the latest trends, hot topics, and cool companies in fintech.

TransferWiseselects Wirecard to issue a debit card alongside its digital borderless account offering.

Vipera partners with Mastercard to launch new mobile payment service, SME Pay.

Thomson Reuters teams up with MarketPsych to introduce sentiment data feed for Bitcoin.

Azimounveils new, improved money transfer service to China.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

“Banks need to ask themselves whether they are flexible and sensitive enough to adapt to the rapidly changing context.” Harrie Vollaard, Head of FinTech Ventures at Rabobank, has established several partnerships with startups, manages the Fintech investments for the Rabobank, is involved in Fintech accelerator programs around the globe, and created several spinoffs. Speaking at FinovateEurope 2018 about Creating A Digital Investment Experience To Compete In A Zero Interest Rate Environment, we chat to him about his key tips for banks who strive to create a successful digital agenda.

Finovate: What does a bank need to focus on when building a digital agenda?

Vollaard: There are three key areas that banks need address to build their digital agenda:

1. A clear innovation thesis and establishing the areas you want to focus on. Here are four areas that we have defined: financial cruise control, platform banking, emerging technologies as business model enablers, and data for food.

2. Open infrastructure to collaborate. To facilitate in- and out-coming datastreams as well as delivering services to third parties and incorporating external services. I envision a satellite structure of the bank’s core assets surrounded by an ecosystem of third parties and startups where the bank is still the first point of contact.

3. A company-wide digital DNA. This is the key success factor and enabler of innovation. Innovation departments running innovation projects and proof of concepts are essential, but in order to be successful you need scale. Scale can only be accomplished through the business lines and marketing department. The bank needs to look beyond the existing products and that can only be accomplished via a customer-first approach, which means a full adoption of a lean startup methodology and product development processes that facilitate iterative learning. A more Darwinian approach is also preferable; it is not the best executed project but the most adaptable organisation who survives. Banks need to ask themselves whether they are flexible and sensitive enough to adapt to the rapidly changing context.

Finovate: How does the fintech sector offer a growth opportunity for banks?

Vollaard: It offers growth in three key areas:

1. Delivering better, more transparant and cheaper services to our clients (challenger banks, personal finance management, market place lending), streamline business processes (by use of Artificial Intelligence, Blockchain), taking out risk (RegTech). The bottom line it the business model optimization; to improve cost/income ration and to increase customer satisfaction.

2. Adding additional services on top of existing banking infrastructure; services more embedded in the real life/business of the clients. A shift from product oriented to service oriented, related to the real customers needs/pains. E.g. in the value added services on top of payments. Bottom line it is business model extension fulfilling customer/client needs embedded in real life events.

3. Exploring new innovation areas; reinvent the business model of the bank. E.g. transforming your assets in to new service offerings to your clients (e.g. delivering trust services (secure login, authentication, signing services to our clients). In general it means cross industry innovations. Example: We developed an FX platform for ourselves which now can be solved as a B2B solution to other financial institutions. Bottom line it is business model innovation.

Finovate: How has Rabobank collaborated with fintechs to expand products and services for customers?

Vollaard: 90% of the collaboration with fintechs are focused incorporating their services in the service offerings of the bank or in the business processes of the banks.. E.g. Sparkholder with loanstreet; a pre-approved finance tool for SMEs.

9% of Rabobank is an extension of our services, such as Rabo&Co with FinTech Cloud Lending solutions, which is a market place lending solution for SME clients.

1% of the collaboration is related to business model innovation, such as working together with fintech Signicat delivering e-business services iDin (secure login, authentication, signing services to our clients). With our corporate investment arm Rabo Frontier Ventures we are focusing on this category.

Finovate: What are the drivers for change in digital investing?

Vollaard: The most obvious one is the customer and business need. Although this seems like a no-brainer, for the incumbents it means a transformation from a portfolio of financial products (which served the customers of the past) to financial services that fit the customer needs of today.

Another driver is the technologies that offer us opportunities we have never seen before, such as risk models/predictions based on different data sources, optimizing business processes, and new revenue streams.

Finally, there is the regulatory motivation and the harmonization of legislation across Europe to stimulate innovation and lower the thresholds to then expand.

Finovate: How can you compete in a zero interest rate environment?

Vollaard: By making investment more accessible; a mobile only investment app focused on millennials whereby the roundups from transactions are invested in ETFs. The threshold is very low to invest in and a small amount being invested on very regular bases counts up without the customer even noticing. It is completely chat-based, user friendly, design-focused and automated with low cost operation. It is a new and engaged target group.

We know the success that Betterment, Wealthfront, Nutmeg have had serving customers via insightful and user-friendly websites. Inspired by them, we introduced last year Rabo Beheerd Beleggen, which has been accepted with huge success.

Finovate: What will new technologies – like artificial intelligence and blockchain – mean for investment management?

Vollaard: The second wave of technologies impacting the financial industry will offer substantial investment opportunities and reduce costs significantly.

AI can slash down costs by 30% by reducing manual work, and blockchain/smart contracts will eliminate steps in the value chain.

Speaking at FinovateEurope 2018, Rohit Talwar – global futurist, author, and the CEO of Fast Future – discussed The Rise Of The Machines – The AI Revolution And The Road To Superintelligence. He specialises in the future of financial services and the challenges of preparing society for the disruptive impacts of exponential technologies.

Clear away the vendor hype and desperate “me too” announcements from across the sector, and the evidence is starting to mount that financial services is exploring serious applications of artificial intelligence (AI). The technology is being deployed in everything from complex internal reconciliations, risk identification, and fraud detection through to customer service chatbots, robo trading, and targeted marketing based on deep customer profiling. Furthermore, in the fast-paced world of fintech start-ups, we are seeing AI-powered hedge funds and advisory firms, personal finance managers, and a host of sites that offer us the potential to streamline traditionally slow and expensive processes for everything from invoice financing to personal insurance.

So, now the game is on, where can we see it evolving to in the coming years? One area is in real-time fraud detection for banking and credit card transactions – spotting and preventing situations that might otherwise take us weeks to resolve. At another level, investors and regulators could eventually be able to monitor the behaviour of fund managers and personal advisors. These systems would examine transactional behaviour, personal spending patterns, and social media activity to detect the potential for insider trading, market manipulation, and misuse of client funds.

For individuals, the aggregation of our personal data with that of millions of other people will allow our intelligent finance advisors to recommend cheaper alternatives for goods and services we buy regularly. The next step would be to aggregate our purchasing to secure discounts from key suppliers. Indeed, we might authorize these advanced comparison tools to switch our purchases, insurances, and even savings on a continuous basis to whoever is offering us the best deal.

Taking this a stage further, new opportunities might arise for those who have a detailed understanding of our lifestyles from travel, to dining, and clothing purchases and link this to our personal financial management. Such sites might be authorised to trade unused airmiles and store loyalty points on our behalf, negotiate entertainment discounts for us, accept paid adverts to our social networks, and rent out our driveway as a parking space. Such systems would then invest any cash surpluses earned on a moment by moment basis using our preferred risk profile as a guide.

The next evolution might to employ a personal AI clone or “digital twin”. These applications would build a detailed understanding of our lifestyles and be authorized to buy, save, sell, or trade on our behalf. Depending on the level of authorization, they might undertake credit card purchases, bank transactions, and bill payments, complete loan or mortgage applications, and even make impulse buys. The system might report back on every transaction or simply deliver an end of day voice or video mail to update on the day’s activities.

The list of potential applications is literally limitless. From streamlining and reducing the cost of activities that are currently an expensive hassle, through to finding new ways of making our finances go further, AI seems increasingly likely to become a vital part of the financial ecosystem. While many of the new AI ventures will go the way of most start-ups and fade away, some will survive. Furthermore, the best ideas are likely to be adopted by more established players as they seek to transform themselves into more customer centric enterprises. The hope is that successive waves of AI innovation will help us make far better use of all the assets at our disposal – not just our cash.

Amazon made headlines around the banking/fintech world this week following a WSJ story Monday about a rumored collaboration with Chase Bank and/or Capital One. The click-bait title, Next Up for Amazon: Checking Accounts (apparently revised from the title embedded in the hyperlink, “Are You Ready for an Amazon-branded Checking”) made it go viral in the United States, at least with news organizations.

The facts were less exciting than the headline. Apparently the ecommerce giant issued an RFP last year seeking suppliers of a “hybrid” checking account aimed at younger and unbanked customers (it’s unclear whether that is a single segment “young and underbanked” or two segments, “young” and/or “underbanked”). And there was no indication that any new product was coming now, or ever.

There is one thing missing in the 100+ stories that appeared in the wake of the WSJ piece:

Amazon already is a bank in everything but the name

Here’s a list of its current financial and payment offerings:

Amazon Pay: Used by 33 million to pay for goods at non-Amazon sites

Amazon Gift Cards: Available at brick & mortar retailers all over the country (I’ve bought more of those than all other gift cards combined)

Amazon Store Card, with financing option on qualified purchases: Issued by Synchrony Bank

Amazon Cash, a virtual debit card which allows cash deposits to the Amazon Pay wallet

Amazon Rewards Visa Signature Card, an affinity card issued by Chase Bank (also Amazon Prime Rewards card; see also March 13 update below)

Amazon Prime Reload, which pays a 2% bonus for cash deposits into Amazon Pay

Amazon.com Corporate Credit Line: A way for businesses to pay for Amazon purchases via monthly consolidated billing, underwritten by Synchrony Bank

Amazon Lending: Which has originated $3B to smaller merchants since 2011 (cited by Bloomberg, sourced to CB Insights)

Credit Card Marketplace: Hadn’t seen that before, includes Amazon co-branded cards along with Discover and American Express

Gift Card marketplace: Hundreds of prepaid gift cards from other retailers along with restaurants, travel, and entertainment providers

Amazon Currency Converter: For purchasing on Amazon.com in local currency

Amazon Allowance: Tool for parents to enable their kids to pay directly (link was broken so not sure the status)

Shop with Points: A number of major banking rewards programs can shop directly at Amazon with their bank-provided points including Citibank, American Express, Chase and Discover

Alexa: Supports banking and payments info (aka skills) from a number of financial institutions including Capital One, US Bank, and American Express

Teen accounts: Amazon allows teens to set up separate logins and make purchases from an allowance amount and/or request approval directly from parents (Source: Business Intelligence).

(Update 29 March 2018) Recent news reports imply that Amazon may be looking at creating additional teen payment options, potentially in partnership with banks

The only major retail banking service missing, a stand-alone debit card (although you can already link a debit card to your Amazon account). Which I’m guessing is the core of the RFP mentioned by the Wall Street Journal.

Update (13 Mar 2018): Bloomberg reports that Amazon is planning on launching a small business co-branded card with Chase, the issuer of Amazon’s consumer card.

Bottom line: Amazon is already deeply involved in banking and payments, as are most major retailers. Gift cards, co-branded credit cards, and SMB credit products are already being used by millions of consumers. Adding a debit card and/or “hybrid checking account” isn’t going to make them any more menacing as a competitor. The prime concern for banks is whether Amazon can move payment volume from bank-issued credit cards, where the industry enjoys healthy profit margins, to debit/ACH with narrow-to-non-existent margins.

Author: Jim Bruene (@netbanker) is Founder & Advisor at Finovate as well as Principal of BUX Certified, a financial services user-experience accreditation program.

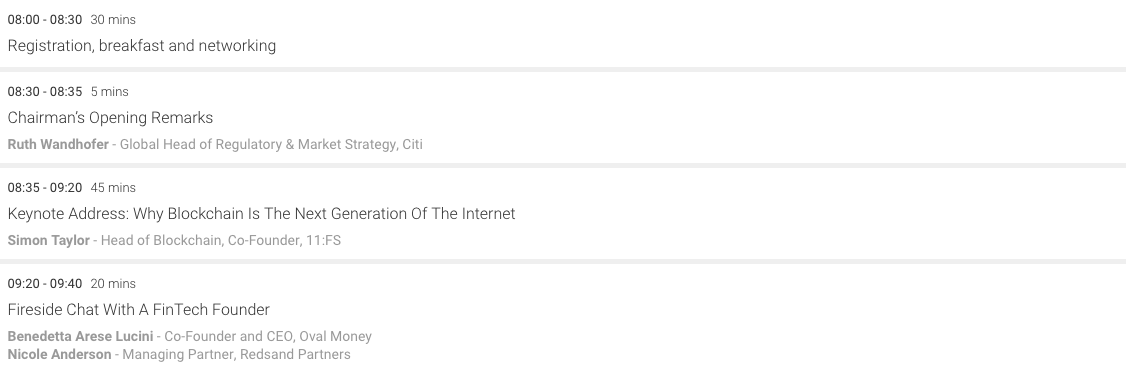

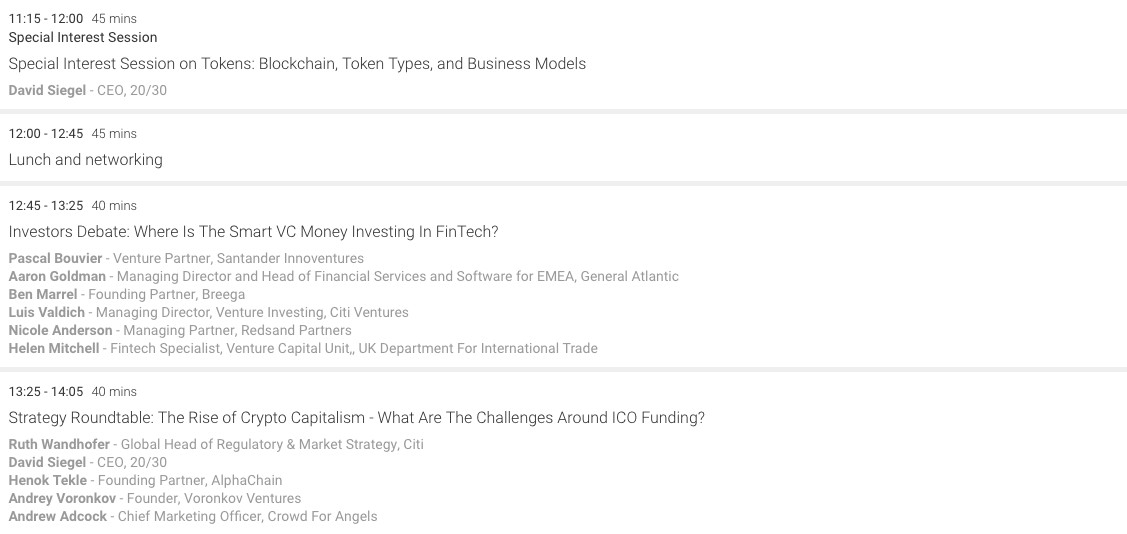

The days have flown by and it’s hard to believe we’ve arrived at the final day of FinovateEurope! We have a lot of content in store today and can’t wait to get started.

We’re at ExCel London and tickets are still available at the registration desk. If you missed the first part of the show, catch up by searching #Finovate on Twitter.

Here’s an overview of today’s agenda. For a detailed look, check out the event website.

From 10:10 to 12:00 our four-track summit panel discussions and fireside chats will cover four topics:

Payments

Digital Lending

New Tech

Special Interest

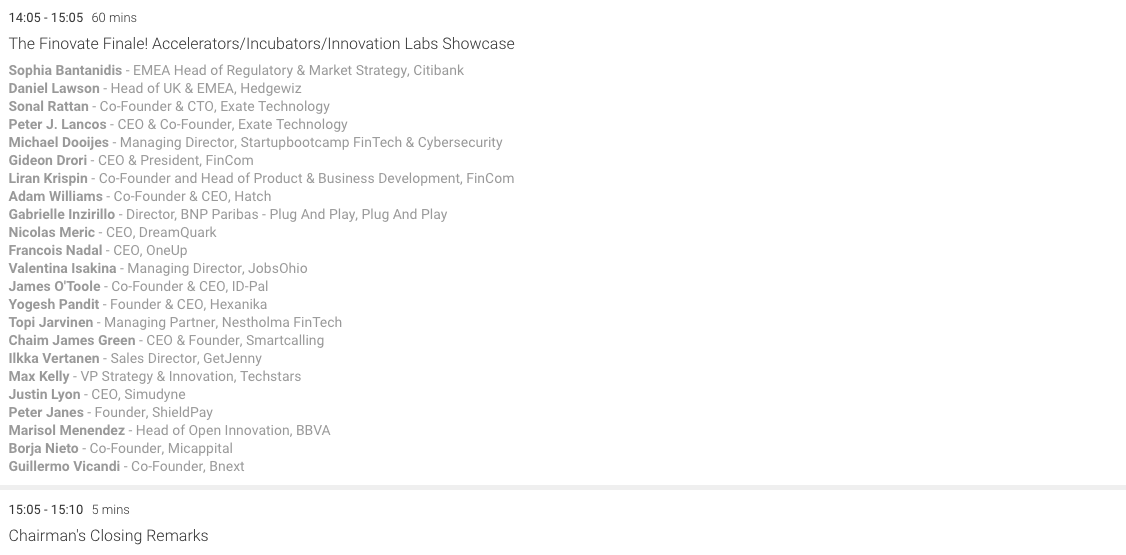

And that’s a wrap! Thanks to all of the presenters for braving the stage with their live demos, to all of the speakers and panel hosts, and of course to our audience– we couldn’t do this without you.

Demo videos will be available on Finovate.com in a couple of weeks and you can find panel discussions as well as bonus content and interviews on our YouTube channel. Until we see you again next year, tune into the Finovate blog for the latest in fintech news.

As the number of women representing start-ups at FinovateEurope 2018 is at its highest since conception, we gather some of the leading ladies in fintech to discuss how the industry has evolved, what practical steps can be taken to move keep moving forward and why male colleagues and peers need to get involved too.

The panel:

Julie Muhn, Senior Research Analyst, Finovate

Magdalena Kron, Head of Rise London & VP Open Innovation, Barclays Bank

The midway point of FinovateEurope falls on a notable holiday– International Women’s Day. This combination makes it the perfect time to celebrate all of the women who have graced the Finovate stage over the past two days.

Out of our 68 demoing companies, 21 were represented by women presenters– that’s 31%. This figure is 35% higher than at FinovateEurope last year, when 23% of the presenting companies were represented by a woman on stage. And it’s 55% higher than at FinovateEurope 2016, when 20% of the companies featured a woman on stage; more than 2x higher than FinovateEurope 2015, where 15% of the companies had female speakers; and a huge leap from our first event in 2007 with zero (seenote 1).

These numbers spell out definitive progress. And with this in mind let’s celebrate women in fintech today– and every day, recognize how far we’ve come, and make an effort to foster a more inclusive environment within our industry.

Editor’s Note: While sadly it’s true that no women were on stage during the 20 demos of the first Finovate. One company, iPay Technologies, was founded by Dana Bowers, but she chose not to speak that day. And Finovate might not even exist if it wasn’t for Melanie Flanagan, then Marketing Manager at Yodlee (also co-founded by a woman), who was the first person to agree to demo. Finally, Susan Hawkins, then SVP at Metavante,was instrumental in getting both her company and Monitise on stage. So there you have it, woman called the shots for at least 20% of Finovate v1.0’s content, even if they ended up delegating the on-stage pitching to men. Thanks Melanie, Dana and Susan! — Jim Bruene, Founder

Best of Show winner ClinclaunchesSpotlight, the first self-service training program for conversational AI.

Cloud Lending Solutionsrecognized as a Top 10 Best Performing Salesforce Solution Provider for 2017 by Insight Success Magazine.

Ohpen Angelique Schouten named Chief Commercial Officer; Lydia van de Voort appointed to U.K. CEO post.

Auto financing offers from Santander Consumer USA now available on the AutoGravity app.

Pushforwins public vote at inaugural Dublin Innovation Jam.

Members Heritage Credit Union launches member-owned insurance agency in partnership with Insuritas.

Lendiointroduces new franchise in Gainesville-Ocala Florida region.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

If there is one theme that unites all of our FinovateEurope Best of Show winners this year, that theme may be summed up in one word: data. As Finovate senior research analyst Julie Muhn pointed out during a recent conversation, the ability to leverage data to create more meaningful, more personalized, more secure experiences for consumers of financial services underlies much of the innovation that we see not just on the Finovate stage, but across fintech writ large, as well.

In this way, financial technology is turning the old adage – it’s not what you know, it’s who you know – on its head. The connections between us and the things we do, the places we go, the transactions we make, are in many ways the Holy Grail for companies that are constantly seeking out better ways to serve us. And for those companies that do win our trust and gain access to what we know and do, the rewards could not be greater.

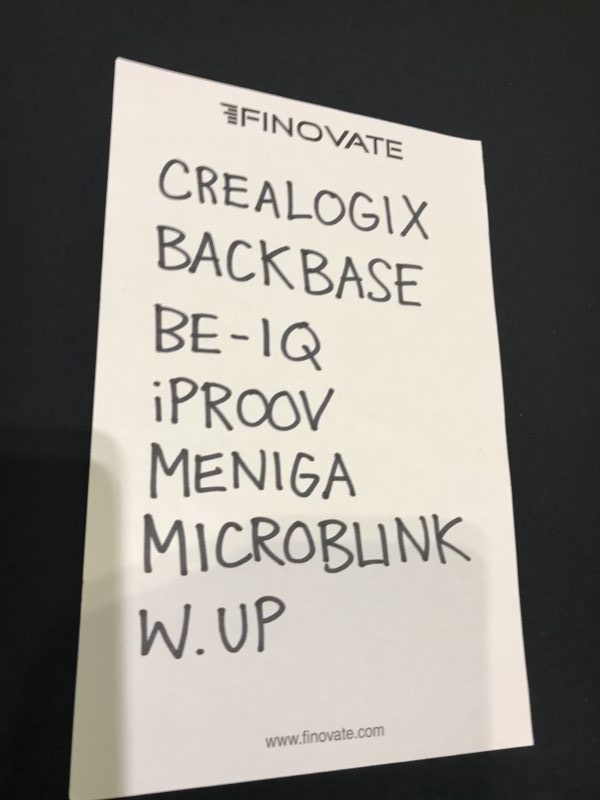

With this in mind, we present to you a small sample of those companies that may be best positioned to take advantage of this Golden Age of Data: the Best of Show winners of FinovateEurope 2018.

Backbase for its Customer OS, the next generation of the Backbase Digital Banking Platform, which is laser-focused on providing customer-first journeys. Video.

Be-IQ for its holistic and gamified approach to risk profiling and financial well-being that accounts for the very contradictions that make us human: our behaviors. Video.

CREALOGIX for its customer banking platform, Gravity, which is breaking new ground with its intuitive and user-friendly, self-service insights application. Video.

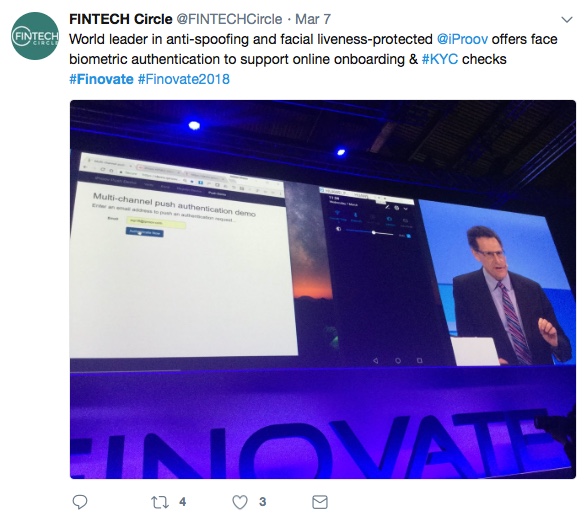

iProov for its liveness-protected, facial biometric authentication technology which is fully-automated for fast, easy and ultra-secure mobile and PC on-boarding. Video.

Meniga for its digital banking solution that helps banks around the world use data to personalize digital channels and drive customer engagement. Video.

Microblink for BlinkReceipt, its SDK for real-time extraction of all purchase data from retail receipts and OCR technology which eliminates typing from mobile apps. Video.

W.UP for its digital banking sales and engagement solution that uses pre-built customer insights to build relevant, personalized, and timely interactions with clients. Video.

Please join us in thanking our sponsors and partners who help us make FinovateEurope a huge success year in and year out. And be sure to stay tuned for coverage of our new extended format on Thursday and Friday as we take deep dives into some of the most pressing issues and fascinating trends in fintech today. For more information about the keynote addresses, panel discussions, and fireside chats coming up on Days Three and Four, our full agenda is available on our FinovateEurope 2018 page.

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The seven companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2018 conferences are below: FinovateEurope 2015 FinovateSpring 2015 FinovateFall 2015 FinovateEurope 2016 FinovateSpring 2016 FinovateFall 2016 FinovateAsia 2016 FinovateEurope 2017 FinovateSpring 2017 FinovateFall 2017 FinovateAsia 2017 FinovateMiddleEast 2018

“Banks need to ask themselves whether they are flexible and sensitive enough to adapt to the rapidly changing context.” Harrie Vollaard, Head of FinTech Ventures at Rabobank, has established several partnerships with startups, manages the Fintech investments for the Rabobank, is involved in Fintech accelerator programs around the globe, and created several spinoffs. Speaking at FinovateEurope 2018 about

“Banks need to ask themselves whether they are flexible and sensitive enough to adapt to the rapidly changing context.” Harrie Vollaard, Head of FinTech Ventures at Rabobank, has established several partnerships with startups, manages the Fintech investments for the Rabobank, is involved in Fintech accelerator programs around the globe, and created several spinoffs. Speaking at FinovateEurope 2018 about

Speaking at

Speaking at ![What’s the Fuss? Amazon Already Offers Full Suite of Banking Services [Updated]](https://finovate.com/wp-content/uploads/2018/03/amazon-banking-product-line.jpg)