This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Trulioo and Mastercard have partnered to help clients streamline onboarding while combatting fraud.

Trulioo will leverage Mastercard’s identity solutions to gain insight into identity and risk scores.

Mastercard will tap Trulioo’s global business identity verification services to enhance its Onboard Risk Check product by adding a layer of assurance to merchant and consumer onboarding solutions.

Global identity platform Truliooannounced today it has teamed up with Mastercard to help merchants streamline digital onboarding while helping them combat fraud.

Under the agreement, Trulioo will leverage Mastercard’s identity solutions to power two of its products– Person Match and Risk Intelligence. This will offer Trulioo insights into identity and risk scores through a customizable, intuitive dashboard, extending the company’s offerings beyond API-based products and further enhancing its onboarding processes.

“Trulioo is proud to partner with Mastercard and shares their dedication to industry-leading business verification and fraud prevention,”said Trulioo CEO Steve Munford.“As organizations navigate the complexities of the digital payments industry, fraud and business identity theft are constant threats. This is a pivotal milestone in our joint endeavor that will pave the way for a more secure global digital landscape.”

Mastercard will also see benefits from the strategic partnership. Trulioo’s global business identity verification services will enhance Mastercard’s Onboard Risk Check product by adding a layer of assurance to merchant and consumer onboarding solutions, helping to mitigate risk, reduce fraud, and increase trust in payments made across the globe.

“The digital economy thrives when people trust it and trust each other,” said Mastercard executive vice president, Identity Products, and Innovation Dennis Gamiello. “The ability to verify people are who they say they are instills confidence on both sides of digital interactions. Together with Trulioo, we are fueling the connections that make a vibrant digital economy possible.”

Canada-based Trulioo was founded in 2011 to help organizations navigate compliance by offering real-time verification of more than 13,000 ID documents and 700 million business entities across the globe, while checking against more than 6,000 watchlists. The company has raised $475 million.

Customer engagement company JRNI has integrated with bank technology innovator Backbase.

The integration will bring new appointment scheduling functionalities to users of Backbase’s Engagement Banking platform.

Headquartered in Amsterdam, Backbase has been a Finovate alum since 2009.

JRNI, a leader in global customer engagement for financial services, has integrated with Backbase, adding new appointment scheduling functionalities to the Backbase Engagement Banking Platform.

“We believe that the banking experience is enriched by building trust through personal connections,” Backbase general manager of ecosystems Roland Boojien said. “This partnership aims to seamlessly provide convenient personal connections in banking and wealth management, effortlessly uniting customers and trusted advisors at their preferred time and location.”

Backbase’s Engagement Banking Platform provides financial institutions (FIs) with a range of digital solutions for customer onboarding, servicing, financing origination, loyalty, and more – all from a single platform. Courtesy of the integration, financial institution customers on the platform will be able to book both virtual and in-person appointments seamlessly and securely. JRNI’s Self-Scheduling Appointment booking solution will give FIs the ability to offer an end-to-end embedded experience that begins with initial customer contact and continues through the customer’s entire journey with ongoing relationship management and support.

The Self-Scheduling Appointment booking solution will be available as an out-of-the-box add-on integrated within Backbase’s Digital Assist offering. Digital Assist provides a unified solution that helps customer-facing teams at FIs resolve customer service issues quicker, as well as upsell additional products and services easier.

“Backbase Digital Assist helps make interactions more efficient, effective, and of higher value,” JRNI CEO Phil Meer said. “JRNI’s engagement capabilities complement Backbase’s offering to drive trusted connections and relationships. Backbase shares our vision and its global platform prioritizes customer engagement as a critical pillar.”

Founded in 2008 and based in Boston, Massachusetts, JRNI offers a customer engagement platform that helps companies improve both customer acquisition and retention, as well as promote brands, drive hyper-personalization, and better engage target audiences. The company’s enterprise-grade event management platform handles scheduling, queuing, and analytics to provide customers with a personalized experience whether in-person or virtual.

Headquartered in Amsterdam, Backbase has been a Finovate alum since 2009. Most recently demoing its technology at FinovateFall 2021 in New York, the company has won Best of Show on four separate occasions. With more than 150 customers and 2,000+ employees around the world, Backbase provides a platform that enables financial institutions to offer their customers the latest fintech innovations without having to abandon their existing core banking systems.

Backbase’s JRNI announcement comes just days after the firm announced that Malaysia’s Bank Muamalat Malaysia Berhad (Bank Muamalat) had agreed to a long-term partnership designed to “revolutionize” the bank’s digital Islamic Banking offerings. Also participating in the partnership is fellow Finovate alum, Mambu.

Fintech leaders, C-suite executives, and investors are facing an epic challenge: How do we adapt our customer acquisition strategies as the landscape becomes more competitive? In this article, we’ll highlight the challenges fintech companies face in customer acquisitions and the benefits of digital experience intelligence (DXI) in understanding your customer behaviors and challenges. Armed with those insights, you’ll be better able to navigate the ever-evolving fintech environment to grow your customer base and nurture your existing customers.

Want to know which of your marketing assets was most viewed by new conversions? Done!

Wondering where the common dropoff points are in your mobile app? No sweat.

Here are ten ways DXI can inform and refine customer acquisition strategies for fintech companies to acquire more of their ideal customers.

1. Identifying Acquisition Opportunities

Digital experience intelligence enables your organization to measure and analyze how users interact with your website or mobile app. Analyzing these journeys provides insight into pain points and areas of high engagement for potential customers. This initial informational process can help you tailor your product offerings and marketing outreach to engage your ideal customers.

Note: Be sure you’re targeting your ideal customers – the ones who truly need and will benefit from your products or services. Understanding who they are, and making that extra effort, will pay off with a client base that is bought in and wants your solutions to work for them.

2. Data-Driven Optimization

Leveraging insights from digital experience intelligence can help identify which marketing channels attract your target audience. In addition, user behavior analysis can measure the effectiveness of ad campaigns to optimize them across different channels.

Personalizing customer experiences is one of the most effective ways to increase engagement and conversion rates, especially during the consideration and decision-making stages. A digital experience intelligence platform like Glassbox is the easiest and most effective way to gain critical insights into how users interact with your platform.

You can then use that data to segment customers by a variety of metrics to provide more relevant, personalized digital experiences. The data gained can also be used to inform product recommendations, web content, and marketing messages, as well as cater to specific preferences, all of which can boost engagement and conversions.

4. Mobile Optimization

Nearly 40% of app uninstallations occur because people are simply not using the app. The best way to understand why customers are abandoning your app is by measuring and monitoring your customer journeys. Armed with that information, you can refine your app to ensure it’s relevant, intuitive, and user-friendly so your users are never tempted to select “Remove app.”

5. A/B Testing for Optimization

Data-driven insights are the holy grail of refining customer acquisition strategies. A/B testing enables companies to understand which versions of websites, apps, and offers perform best in attracting and converting potential customers. The insights you gain can inform continuous improvement of user experience and refine your customer acquisition strategies.

6. Proactively Addressing Customer Pain Points

Technology like Real User Monitoring (RUM) and newer iterations like Real User Experience (RUX) enable fintech companies to quickly detect and resolve technical issues.

The ability to swiftly address user experience pain points and intercept technical snags before they escalate can transform your customer’s journey from one of frustration into a smooth and responsive experience that makes them feel valued. With 80% of consumers reporting that customer experiences need to be improved, proactive engagement is your golden ticket to differentiation.

7. Unlocking More Substantial Customer Feedback with AI

Voice of the Customer (VoC) data captures customer feedback so you can gain a deeper understanding of their digital experiences. However, VoC data only represents the vocal minority—our internal analysis found that only about 4% of users provide feedback.

Fintech companies can now leverage AI to automatically compare these rated interactions to similar interactions across the entire user base. We do this at Glassbox with our Voice of the Silent (VoS) tool, which makes it easier to understand what the majority is experiencing, even when they blow off satisfaction surveys.

8. Building Customer Trust Through Transparency

Building customer trust is the most direct path to loyalty. Digital experience intelligence reveals where users hesitate to provide information or engage, which can reveal areas for improving transparency about data privacy and security measures. Addressing those concerns demonstrates your commitment to user safety, which puts you further along the path to customer trust and loyalty.

9. Clear The Biggest Hurdle: Knowing What Your Customers Want

With fintech products and services flooding the market, customers have an exhausting supply of options if you fall short of their expectations for seamless digital experiences. Understanding how they experience interactions with your website or mobile app is critical to effectively measuring, analyzing, improving, and ultimately ensuring customers feel understood and appreciated.

10. Make Customer Acquisition Everyone’s Business

Customer acquisition should be an all-encompassing, organization-wide effort – not just the job of marketing or product development. Lasting relationships are supported at multiple levels and in diverse ways, and playing that message on repeat is essential to making it stick.

Want to see what DXI actually looks like in action? Click around in Glassbox’s self-guided platform tour.

PayPal’s stablecoin, PayPal USD (PYUSD), was officially added to the Solana Blockchain last week. This shift comes after the California-based company launched on Ethereum blockchain last summer. Now, PayPal stablecoin users can send PYUSD on Ethereum or Solana when transferring out to external wallets.

“For more than 25 years, PayPal has been at the forefront of digital commerce, revolutionizing commerce by providing a trusted experience between consumers and merchants around the world. PayPal USD was created with the intent to revolutionize commerce again by providing a fast, easy, and inexpensive payment method for the next evolution of the digital economy,” said PayPal Senior Vice President of the Blockchain, Cryptocurrency, and Digital Currency Group Jose Fernandez da Ponte. “Making PYUSD available on the Solana blockchain furthers our goal of enabling a digital currency with a stable value designed for commerce and payments.”

In addition to enabling PYUSD transfers on both Ethereum and Solana, this move will have significant implications for PayPal, consumers, banks, and the crypto markets.

Impact on PayPal users

Faster transactions: Because Solana’s blockchain is known for its high-speed processing capabilities, PYUSD transactions on Solana will be much quicker, which will enhance the experience for end users.

Lower transaction costs: Solana offers low transaction fees, which will not only reduce the cost of sending and receiving PYUSD, but it will also make Solana a more attractive option for users looking to save on transaction costs.

More flexibility: Offering both Solana and Ethereum will offer users more choices for their transactions. Offering multiple blockchain allows users to choose different options based on their preferred cost and transaction speed.

Impact on Banks

Integration challenges: Traditional banks seeking to participate in the stablecoin market may need to adapt their systems to accommodate transactions that involve PayPal’s stablecoin on the Solana blockchain. These adaptations could require significant technical and regulatory challenges.

Competition: The race to stablecoin dominance has quieted among most traditional financial services providers in the U.S., but cross-border payments in all of their forms are still top-of-mind for many. As PayPal leverages the blockchain to offer faster and cheaper transactions, traditional banks may face increased competition.

Regulatory scrutiny: PayPal’s move onto Solana may attract further attention from regulators. This increased regulatory scrutiny may require financial institutions to pay more attention to their own operations and closely monitor regulatory developments to ensure that their own operations are compliant.

Impact on the Crypto market

Increased credibility: While it is not a bank, PayPal is a reputable player in the traditional financial services space. Because of its tenure and reputation in the space, the company’s adoption of Solana for its stablecoin operations offers credibility to the blockchain and crypto industries.

Boost for Solana: Solana will likely benefit from the partnership, as PayPal’s move serves as a vote of confidence for the blockchain and may lead to increased demand for Solana’s native token and may result in further adoption by other enterprises.

Shifting competition: PayPal’s selection of Solana may put pressure on Ethereum to improve its scalability and cost efficiency.

Overall, PayPal’s move is likely to enhance the efficiency and appeal of its digital currency offerings, drive broader adoption of blockchain technology, and spur innovation and competition in both the traditional financial sector and among crypto players.

PYUSD is issued and managed by Paxos Trust, a company whose products are subject to regulatory oversight by the New York State Department of Financial Services. Users can purchase PYUSD in the PayPal and Venmo wallets, as well as on crypto.com, Phantom, and Paxos. All platforms offer a fiat-to-crypto user experience.

FintechOS received a $60 million investment, boosting its total funding to over $151 million.

FintechOS will use the new funds to accelerate its global expansion.

In the announcement, FintechOS revealed it experienced 40% year-over-year revenue growth in 2023 and said it expects to break even in 2024.

Financial product management platform FintechOS recently announced it received a $60 million Series B+ investment, boosting its total funding to more than $151 million. Molten Ventures, Cipio Partners, and BlackRock led the round, while existing investors EarlyBird VC, OTB VC, and Gapminder VC also contributed.

FintechOS serves up technology that helps organizations launch and manage financial products and services without having to replace their existing core infrastructure. The company offers low-code/ no-code tools to help organizations extend the capabilities of their existing core, launch new products, improve their customer experience, and optimize back-office workflows across lending, savings, insurance, investment, and embedded finance operations.

While FintechOS will use the funds to accelerate its global expansion, the New York-based company has already made significant progress towards global growth. The company operates globally, with a presence in Europe, North America, and Asia. FintechOS is available in the U.K., the U.S., Canada, Germany, France, the Netherlands, Romania, Spain, Italy, Poland, Belgium, Australia, Singapore, and others.

“Securing this investment is a testament to the confidence our investors have in our vision and execution,” said FintechOS Co-founder and CEO Teo Blidarus. “Our rapid growth and operational improvements reflect the demand for our next-generation financial product management solutions. We are revolutionizing the financial services industry by providing technology that enables core modernization and drives innovation.”

Since Blidarus co-founded FintechOS in 2017, the company experienced 40% year-over-year revenue growth in 2023 and has seen a 170% increase in operating margins. The company expects to break even in 2024. Following its recent $15 million funding round in early 2022, FintechOS has achieved over 300% growth, expanding its client base to 50 global clients. This growth includes high-profile additions such as Société Générale, Admiral, Benenden Health, Avant Money, and Vibrant Credit Union.

“FintechOS’s growth trajectory is a clear indicator of their potential,” said Cipio Partners Managing Partner Roland Dennert. “We are delighted to be part of this journey and look forward to seeing the transformative impact they will make in the financial services sector. Their commitment to modernization and innovation aligns perfectly with our investment strategy.”

As organizations struggle to adapt to changing consumer expectations and new technologies while maintaining their legacy core infrastructure, technologies such as FintechOS’ will see increasing growth. That’s because many traditional players in the space continue to operate using old computer languages such as COBOL, which was developed in 1959 and does not interface easily with modern fintech solutions.

Will the new month bring new challenges in fintech? Or will the news cycle take a much-needed vacation as summer approaches? Stay tuned to this week’s news for updates and evolutions throughout the week.

Pinnacle Bankpartners with CorServ to implement a modern credit card program for commercial, business, and consumer customers.

Insurtech

Scott Credit Union selectsBUNDLE by Insuritas to launch its insurance agency.

Investment and wealth management

Brokerage-as-a-Service innovator DriveWealthforges new partnership with Turkish fintech Papara.

Lending

PlaidunveilsConsumer Report, a new solution that brings businesses real-time cash flow data along with credit risk insights through Plaid Check, its consumer reporting agency.

Western Union is leveraging Plaid’s open banking infrastructure for money transfers in Europe.

The move is expected to benefit end users by offering a faster, more secure payments experience without negatively impacting the user experience.

Leveraging open banking payments will also create operational efficiencies for Western Union employees.

Plaidannounced this week that Western Union has selected to leverage its infrastructure to offer its customers in Europe seamless open banking payments. Western Union anticipates the move will offer its customers additional flexibility in how to send money to family and friends.

By leveraging open banking technology, funds transferred using Western Union will be faster and will have higher thresholds for safety and security without adding friction to the user experience.

“Consumers are demanding easier and simpler border-less payments without compromising on security, said Plaid Head of Europe Brian Dammeir. “Plaid is delighted to collaborate with Western Union to enable users to make larger payments, safer and faster.”

The new technology will also benefit Western Union employees by creating operational efficiencies. Plaid’s open banking technology streamlines Western Union’s internal operations and enhances its payment infrastructure by providing a common standard of funding across Europe.

“It was great working with Plaid to offer a new, easier way of doing money transfers with us,” said Western Union VP Omnichannel Marketing Bart Stence. “This collaboration shows how we at Western Union invest in innovation to provide our customers with the flexibility and trust they need.”

The question of deploying AI technology in fintech and financial services is no longer a question of “if” – or even “when.” As our recent spring fintech conference confirmed, innovators and entrepreneurs across our industry have already decided that the answer to both of those questions is “yes” and “now.”

But there are hurdles and challenges for fintechs and financial services companies as they seek to deploy AI in their products and offerings. Unlike other industries, fintechs and financial services companies operate in a high-risk environment where issues of trust, transparency, and explainability – to say nothing of regulatory oversight – are virtually existential.

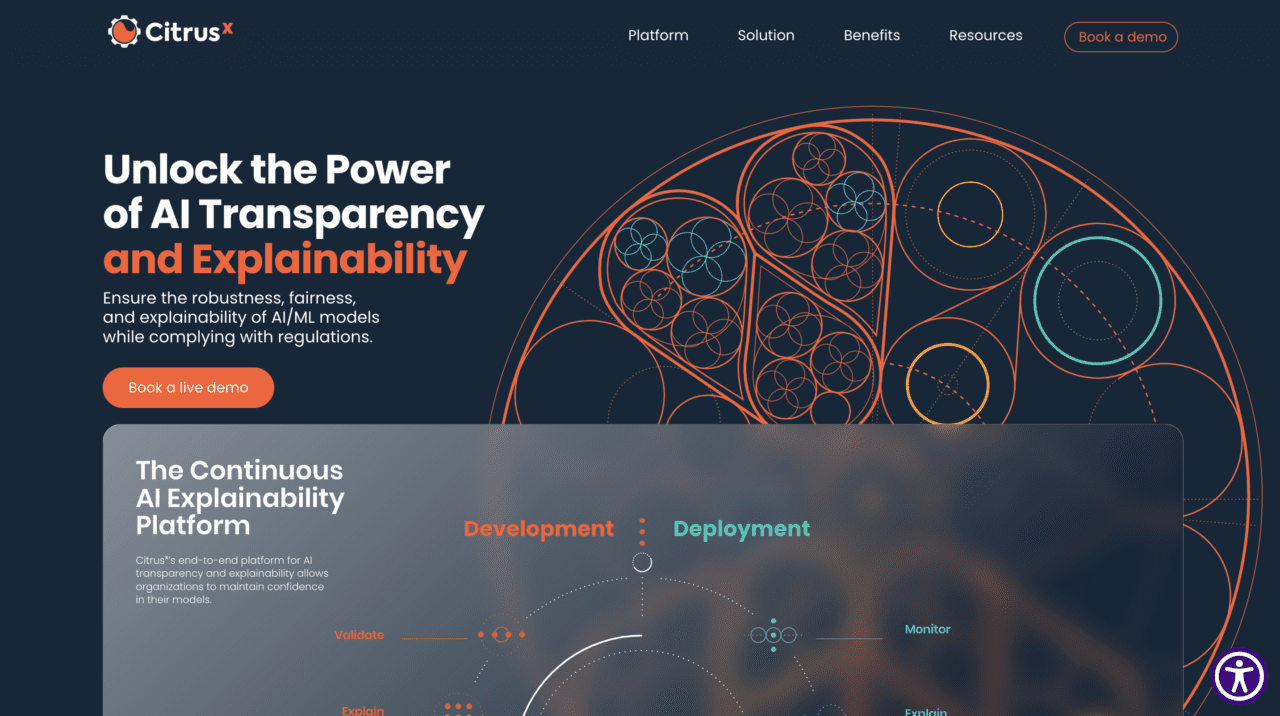

Earlier this year at FinovateEurope in London, Israel-based Citrusxdemoed its platform that enables all stakeholders in the AI pipeline to remain in the loop and benefit from 100% transparency in their models.

We caught up with Citrusx’s VP of Business Development Michal Berdugo (pictured) to talk about the company, how it helps businesses effectively deploy AI technology, and what we can expect from the company in the near future.

What problem does Citrusx solve and who does it solve it for?

Michal Berdugo: In today’s data-driven world, everyone wants to adopt AI for various use cases, but they often face many roadblocks. In high-risk industries, the primary obstacles are a lack of understanding and trust. When key decision-makers can’t trust their AI systems it can lead to potential reputational and regulatory damages.

Citrusx comes in to help financial institutions and other organizations in highly regulated industries speed up their time to production while ensuring their models are accurate, robust, explainable, fair, and comply with regulatory requirements.

How does Citrusx solve this problem better than other companies or solutions?

Berdugo: High-risk sectors such as banks, loan providers, and credit unions, face unique challenges in adopting AI solutions. The lengthy production timelines and the inherent opacity of AI systems leave these companies vulnerable to liability issues. Without transparency, they are unable to fully understand or explain AI-driven decisions, heightening their exposure to legal and regulatory risks.

Citrusx’s patent-pending technology delivers real-time insights, accurate explanations, and critical validation measurements throughout the development cycle and offers proprietary monitoring and prediction methods, making it model-agnostic and resilient to feature correlation problems. Citrusx empowers businesses to build trust and deploy AI responsibly, unlocking its full potential.

Who are Citrusx’s primary customers? How do you reach them?

Berdugo: Citrusx attracts risk leaders and data science leaders who are actively seeking innovative solutions. These forward-thinkers are constantly on the lookout for ways to mitigate risks and maintain compliance with regulations. Peer recommendations validate Citrusx’s effectiveness, while articles featuring insights about us and thought leadership also spark interest.

When these leaders search for cutting-edge tools, Citrusx naturally emerges as a preferred option. Additionally, understanding the unique challenges in high-risk industries such as finance and insurance allows us to effectively address their specific pain points. To explore how Citrusx can benefit your organization, reach out to us directly via our website and book a demo.

Can you tell us about a favorite implementation or deployment of your technology?

Berdugo: One of the Big Five banks in Canada approached us because they wanted to deploy an AI model, but finding a way to make it explainable while complying with regulations was a challenge. When models become more complex, understanding their decision-making processes and fostering accountability and trust in the outcomes becomes difficult. Additionally, without any transparency of the rationale of the model, it can cause vulnerabilities and biases to slip through the cracks, which could lead to reputational and regulatory damages.

To help them combat these issues and build a robust, explainable, and fair model, we provided them with a framework to explain the inner workings of their model accurately. Using proprietary explainability methods, we gave them the tools to see the model’s results on a global and local level, yielding a full report of each sample in their dataset.

With our help, the bank achieved a deeper level of understanding of their model, giving them the trust to finally put them in deployment! All stakeholders, including those who are non-technical, were able to understand the model’s decisions, allowing them to approve it faster with confidence.

Instead of taking six to nine months to deploy their model, we cut the time in half. We also gave them the assurance that their models remained compliant with regulations.

What in your background gave you the confidence to tackle this challenge?

Berdugo: Based on my experience, I gained an understanding of the significant gap companies in the financial sector are facing. While organizations want to keep pace, they are falling behind because of regulations. On top of that, there is a lack of transparency and trust in their models. At Citrusx, we had the confidence to take on this problem because we onboarded a global bank as our first main customer. With our combined backgrounds in the financial sector, government, and AI/ML development, we had the tools to build the best solution for our clients and potential clients.

Above: Citrusx’s Michal Berdugo and Dagan Eshar, VP of Research and Development

What is the fintech ecosystem in Israel like? What is the relationship between fintechs, banks, and traditional financial services companies in the country?

Berdugo: Israel’s fintech ecosystem is thriving, boasting a high number of startups creating innovative financial solutions for a relatively small population. There are roughly 550 fintech startups in Israel, and 20 of those companies are valued at over $1 billion. This makes Israel a major player in fintech on a global scale.

The relationship between fintechs, banks, and traditional financial institutions in Israel is evolving. There’s both competition and collaboration. Banks are partnering with fintechs to improve their digital offerings and reach new customers, while fintechs benefit from the banks’ established infrastructure and customer base. This symbiotic relationship helps both sectors grow and provide better financial services in Israel.

You demoed at FinovateEurope earlier this year. How was your experience?

Berdugo: The experience was great, as it was the first conference we participated in since launching from stealth. We were excited to share more about our product and the crowd was incredibly receptive. We gained many interesting insights about what different stakeholders in the AI pipeline are focused on in the coming quarters. The Finovate team was also very helpful and gave us great feedback in preparation for the demo.

What are your goals for Citrusx? What can we expect to hear from you in the months to come?

Berdugo: We are signing new clients and working on growing and expanding our product and team in the coming year. We are working toward a time when Citrusx’s solutions will be a standard practice.

The conversation continues with Finovate VP and host of the Finovate Podcast Greg Palmer!

In recent episodes of the Finovate Podcast, Greg Palmer has discussed a number of key topics in fintech and financial services. These topics include the current state of venture capital funding, the opportunities presented by new technologies like AI and faster payments, and a look at the current challenges faced by credit unions. Catch up on the latest from Greg and the Finovate Podcast below!

Greg Palmer sits down with Pete Cherecwich, President of Asset Servicing at Northern Trust, to discuss the new technologies available to financial institutions and how FIs can push their tech stack forward.

Greg Palmer and Bain Capital Venture Partner Sarah Hinkfuss talk about the current state of venture capital funding and the best opportunities for investment in fintech.

Greg Palmer interviews Jean Pesme, Global Director of Finance at the World Bank, to discuss the impact of fast payments on the world economy, including the role of the World Bank’s Project FASTT.

Greg Palmer talks with Brian Lee, CEO of Landings Credit Union, on the role of emerging technologies in helping credit unions better serve their members and grow deposits.

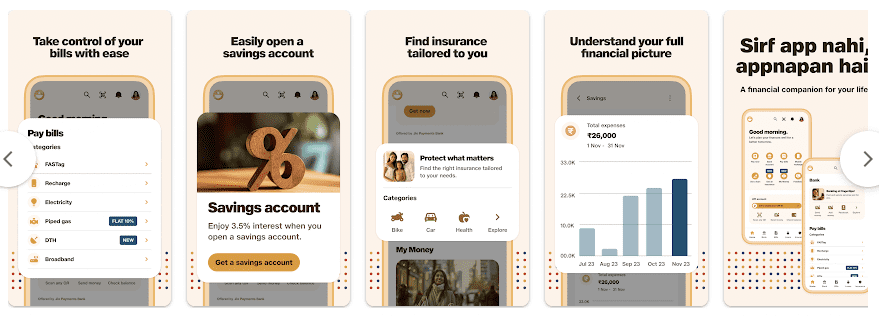

Jio Financial Services parent Reliance Group launched its own financial super app, JioFinance.

JioFinance serves as a single place where users can conduct digital payments, apply for loans, and purchase insurance.

Jio Financial partnered with Blackrock last year and is expected to enter the wealth management space in the future.

TechCrunch unveiled this morning that Jio Financial Services parent and multi-sector conglomerate Reliance Group launched its own financial super app, JioFinance.

Jio Financial’s new JioFinance app launched today in the Google Play store and aims to serve as a single place where users can conduct digital payments, apply for loans, and purchase insurance. The bank accounts are held with Reliance-owned Jio Payments Bank, which was granted a banking license by the Reserve Bank of India in 2015.

“Introducing JioFinance, for your fast and secure UPI payments, seamless bill payments, and timely reminders,” the app description reads. “Enjoy instant rewards and benefits on all UPI transactions. Instant account opening in a few minutes, with zero balance feature, interest rate as high as 3.5% and a digital passbook, with Jio Payments Bank. Take control of your finances with easy tracking and analysis of your spends in a few clicks. Pay bills, track expenses, and save money with the JioFinance app!”

Today’s launch comes after Jio Financial formed a partnership with Blackrock in 2023 to add wealth management offerings to its existing insurance and lending offerings. Also in 2023, Jio Financial announced it was leveraging alternative data to enhance its personalization efforts.

Unlike the U.S., India has a growing scene of true super apps players. Reliance’s competitors in the space include Tata Group and Paytm. Tata Group’s Tata Neu aims to integrate a range of services from e-commerce and finance to travel and health under one platform. And Paytm, which originally launched as a mobile wallet and payment app, has expanded into a super app by adding banking, financial services, and e-commerce functionalities.

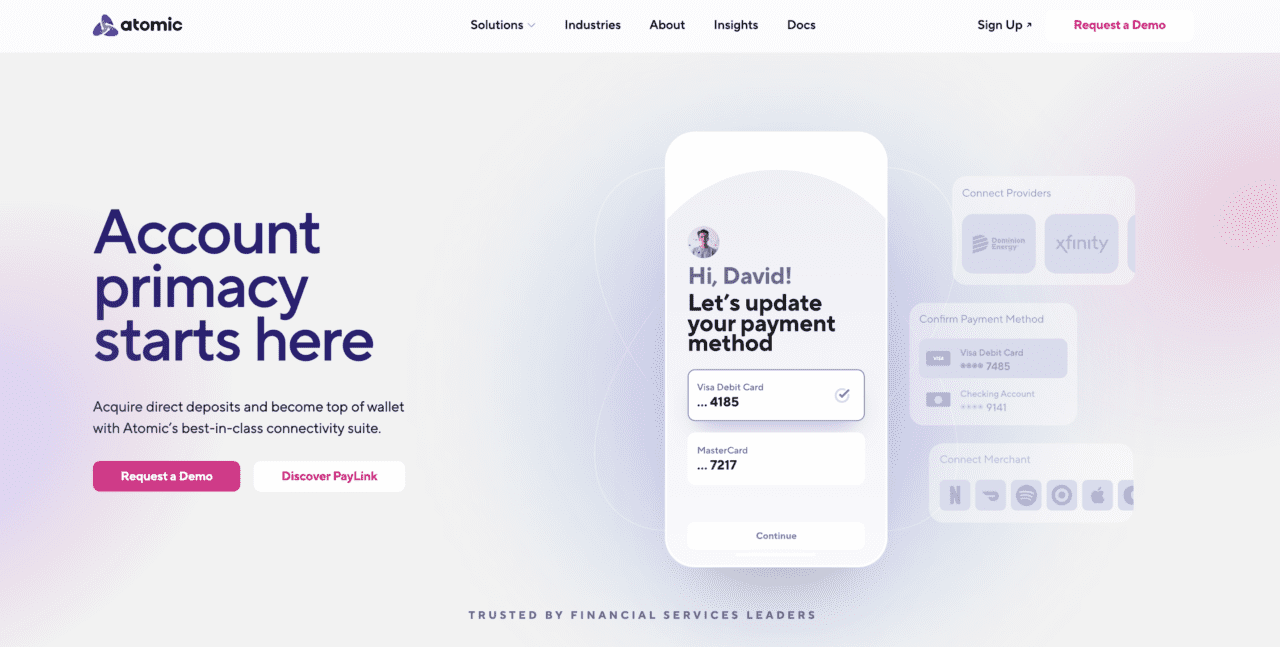

The new offering for financial institutions enables users to monitor recurring payments and make real-time changes from within their banking app.

Atomic most recently demoed its technology earlier this month at FinovateSpring in San Francisco.

Payroll connectivity innovator Atomicunveiled its latest offering: PayLink Manage. The new solution is an actionable subscription management tool for financial institutions that enables users to monitor recurring payments and make real-time changes from within their banking app.

“By integrating PayLink Manage, banks can not only improve their service offerings and increase engagement, but also can solidify themselves as the primary banking relationship,” Atomic CEO and Co-Founder Jordan Wright said. “When banks help their account holders with innovative insights that are actionable, everybody wins.”

PayLink centralizes and automates oversight and control of recurring payments. Users can connect, view, and track a variety of payment types from subscriptions and bills to streaming services and mortgage payments. PayLink Manage also enables users to make real-time changes to their subscriptions directly within the banking app. Additionally, courtesy of Atomic’s direct connectivity, financial institutions can gain insights into usage data, itemized receipts, and other key subscription information. This facilitates deeper analysis, driving more personalized guidance that helps users save money.

“PayLink leverages Atomic’s proven technology, which has already facilitated millions of secure connections across financial platforms,” Atomic Chief Product Officer Andrea Martone said. “With this launch, we are extending our trusted, robust connectivity framework to subscription management, providing financial institutions with a tool to enhance customer engagement and improve retention by helping people take action to improve their financial outcomes.”

Headquartered in Salt Lake City, Utah, Atomic made its most recent Finovate appearance earlier this month at FinovateSpring in San Francisco. At the conference, the company demoed its subscription management technology, which leverages its access to payroll, HRIS systems, and merchants to support a range of financial services, including direct deposit switching, income and employment verification, and more. Founded in 2019, Atomic has raised more than $68 million in funding from investors, including ATX Venture Partners and Portage Ventures.

FinovateSpring was a whirlwind of meeting new people, learning about new ideas, as well as seeing familiar faces and hearing new perspectives on old concepts. The show wrapped up last Thursday in San Francisco and I have a treasure trove of thoughts to share.

Before I explain the top five things I saw and heard at FinovateSpring this year, I’ll start with a disclaimer. Because of on stage and behind-the-camera speaking obligations, I only managed to watch about half of the content. Many of my takeaways stem from conversations I had–both on and off stage. One of my favorite things about Finovate is the seasoned and diverse base of attendees who are willing to openly answer questions.

That said, here are my top five takeaways from the event:

GenAI is everywhere

On stage: Many of the live demos centered around genAI. Each company emphasized that they were using a large language model (LLM) with guardrails to create a responsible, generative AI to save time and create efficiencies.

On the networking floor: While conversations surrounding genAI were generally positive, some people were more bearish on the topic, expressing concerns that human-in-the-loop does not offer enough accountability and that AI needs to be responsibly integrated into workplace organizational structures so that we do not eliminate all lower level employees. I learned that everyone has an opinion on the matter, but nobody can offer any accurate prediction on future applications of AI in financial services.

Third party risk management in BaaS

On stage: With all of the drama in the BaaS space, there was a lot to talk about when it comes to third party risk management. Much of the discussion centered around properly vetting third party providers, creating open and transparent communication between third parties and the bank, and having a clear exit plan for when the third party ceases operation.

On the networking floor: A lot of folks were talking about the Synapse bankruptcy case and the potential implications its collapse may have on For Benefit Of (FBO) accounts and BaaS in general. While some said that the FBO model is risky, others said that the issue lies in middleman providers such as Synapse, Unit, and Treasury Prime, and that BaaS will remain unharmed.

Future of regulatory constraints

On stage: Many speakers and panelists brought up the topic of regulation, as multiple fintech subsectors of fintech are dealing with volatile regulatory environments. During the panels and presentations, most speakers shared a positive outlook on the regulatory environment in the U.S.

On the networking floor: Similar to the speakers, many folks I spoke with on the networking floor had positive things to say about the U.S. regulatory environment. Even when discussing consent orders related to BaaS, the emphasis of these discussions centered around future proofing third party relationships and maintaining open communication with regulatory bodies.

Scenario planning

On stage: During my fireside chat with Brian Solis, the digital anthropologist and futurist emphasized the importance of scenario planning. He stressed that both banks and fintechs will have the most opportunities for success in today’s fast-paced, ever-changing environment if they are diligent about scenario planning. This is especially true in a highly regulated industry and when AI is taking over much of the heavy lifting.

On the networking floor: While none of my conversations centered around scenario planning, a handful of folks brought up the importance of planning as a general way to mitigate risk when it comes to leveraging new technologies, forming new partnerships, and remaining customer centric.

Embedded finance

On stage: I had the opportunity to host a panel discussion on embedded finance on the second day of the conference. Our 30 minute conversation highlighted the prevalence of embedded finance across the fintech sector. The panel participants also reviewed tips on maintaining third party partnerships and emphasized that, while the customer always belongs to the bank, the relationship is more likely to get watered down when leveraging third party technology.

Off stage: Embedded finance was present everywhere I looked. It is clear that, despite some risks and regulatory concerns, banks and fintechs will continue to leverage embedded finance.

Honorable meow-ntion: J.P. Meowgan

My favorite session at every Finovate event is the Analyst All Stars, which features three or four analysts offering their seven-minute presentations on a top fintech theme. During his presentation, Ian Benton, Senior Analyst at Javelin Strategy & Research who gave a presentation on small business banking used an illustration of a cat he named Mr. Munchies who needed to visit J.P. Meogan to get a loan for his small business.