This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Payment automation solutions company AvidXchangeannounced this week it added $128 million to its Series F funding round. When included with the $260 million the company raised earlier this year, the oversubscribed round tops $388 million.

The round includes funds from new investors Lone Pine Capital, Schonfeld Strategic Advisors, and clients of Neuberger Berman. Existing investors, including Pivot Investment Partners, Mastercard, and Sixth Street Partners also participated.

AvidXchange will use the funds to fuel strategic growth initiatives and innovation.

“With only 40 percent of U.S. businesses automating their accounts payable processes, we continue to solve a real problem for companies that still rely on paper invoices and checks, fundamentally changing the way they pay their bills” said AvidXchange Co-founder and CEO Michael Praeger. “This has become even more evident as we see businesses implementing continuity plans and shifting to work from home models, making automation essential to support mission critical processes and keep operations running.”

AvidXchange offers solutions to help businesses manage the entire payments process– from invoice to payment– in a completely digital manner. The firm also facilitates payment fulfillment and manages supplier relationships to help companies focus on their business.

AvidXchange’s SaaS-based technology solves a huge pain point for U.S. businesses, as a full 60% of them still pay bills with paper checks.

While there is no word on an updated valuation for AvidXchange, the company was thought to be valued at $2 billion in January of this year.

Commerce monetization company Empyrannounced this week it has been acquired by its long-time partner Augeo, a loyalty and engagement firm. Financial terms of the deal were undisclosed.

Under the agreement, Empyr will rebrand as Figg, combining Augeo’s card-linking technology with Empyr’s publisher experience. Figg will benefit from Augeo’s existing 60 million users and $300 billion in transaction volume for loyalty offers.

Empyr launched in 2011 and has since raised $48.2 million in funding. The company’s API relies on data partnerships with VISA, Mastercard, and American Express to power card-linked loyalty rewards for offline businesses.

“While the timing might seem counter-intuitive, we believe there is an urgent need to bring advanced technology and more encompassing advertiser offer content to consumers seeking greater value,” said Augeo CEO David Kristal. “Some retail sectors like grocery, household essentials and health-related products are near capacity, while the travel industry, hospitality, restaurants and many local service businesses are battling to stay afloat. As things begin to improve, Figg will be uniquely positioned to connect consumers with advertisers to help accelerate commerce in the U.S. market.”

Valor Siren Ventures provided an undisclosed amount of financial support. “This is a compelling combination, to have VSV lead with new capital invigorating the operational and technology investments made by Augeo and Empyr in recent years,” added Bill Ruh, former Chairman of Empyr.

Kristal, who is also Executive Chairman of Figg, said the company chose the name Figg because it reflects its mission. “Figs define persistence and reflect the enduring quality that we felt spoke to our adaptability, sustenance and resolve,” he said.

The name also demonstrates the company’s adaptability, which is especially relevant in a time of pandemic. “Augeo was first launched during challenging times, and that experience has fortified our ability to press through adversity and grow. Today, we are looking through this current challenging time toward the “next normal.” We have a unique strategic focus around cash preservation coupled with ingenuity, adaptability and where possible, growth,” added Kristal.

What have the companies that demonstrated their latest technologies at our west coast fintech conference last spring been up to in the months since then?

We’ve moved the event later in the year in 2020 due to the public health concerns over the coronavirus pandemic. But we still wanted to check in on these innovators from our most recent spring show, and take note of their accomplishments since we last saw them on the Finovate stage. Here’s what we found:

Bringing in the Big Money

Anti-fraud solutions provider – and Best of Show winner – Arkose Labsraised $22 million in a round led by Microsoft’s VC arm, M12. The company won its first Best of Show award at our west coast conference last spring after demonstrating its authentication system.

Voca.ai, a three-time Best of Show winner, secured funding from American Express Ventures.

Digital platform banking solution provider Agorasecured $2 million in funding as it announced the opening of new headquarters in Atlanta, Georgia.

Cinchy won $500,000 cash prize in 2019 VentureClash competition.

ClickSWITCHraised $13 million in Series B funding.

SheerIDlanded $64 million investment in round led by CVC Growth.

Strandsagrees to be acquired by credit management solutions specialist CRIF.

YSEOPraises $9.3 million investment from NextStage.

Making Friends in High Places

BlueRush, which picked up a Best of Show win last year at our west coast conference, sealed an IndiVideo deal with Nikia Dix, and forged a strategic partnership with InfoSlips.

Best of Show winner Neener Analyticsgraduated from 2019 FIS Fintech Accelerator program.

ALTRpartnered with fellow Finovate alum Q2 to leverage blockchain technology to improve data security.

Cinchy earned a spot in the 2020 MassChallenge FinTech program.

doxo teamed up with fellow Finovate alum Plaid to bring overdraft protection to billpay.

A new partnership has broughtClickSWITCH’s account switching technology to customers of fellow Finovate alum Finastra. ClickSWITCH also announced a partnership with digital bank Current.

EVERFIcollaborates with Zelle to support youth financial literacy.

Faradayintegrated with growth marketing platform Iterable bringing AI-generated predictions to Iterable’s workflows.

Fortress Identityworked with Visa to bring biometric authentication to cardholder transactions in Latin America and the Caribbean. The company also partnered with Zenus Bank, helping the Puerto Rico-based institution securely onboard new accounts.

RightCapitalentered into a strategic partnership with the International Association of Registered Financial Consultants, and teamed up with wealth manager CircleBlack.

Terafinapartnered with Alabama’s Listerhill Credit Union and empowered small business onboarding for PlainsCapital Bank.

Earning R-E-S-P-E-C-T

Arkose Labsearned a spot in CNBC’s 2019 Upstart 100. The company’s VP of Marketing and Strategy Vanita Pandey and Senior Producer Hedda Peters win Women in Cybersecurity honors from the Cyber Defense Global Awards.

Neener Analyticswon Rising Star in India recognition in the India FinTech Forum’s IFTA 2019 awards.

Gliapicked up top honors at the CUNA Operations & Member Experience Council and Technology Council Conference Speed Rounds competition.

Invest Sou Sou was selected to participate in Halcyon Incubator for startups in the Washington, D.C. area.

GoBankingRates featuredCalcXML in its roundup of top free online financial calculators.

Cinchynamed a finalist in Connecticut Innovations’ 2019 Global Venture Challenge.

EVERFI recognized in the Deloitte 2019 Technology Fast 500.

Flybitsearned a spot in the 2020 Fintech Power 50, and was named to Digital Finance Institute’s list of Top 50 Fintech Companies in Canada for 2019. Horizn and Responsive AI also earned recognition from the Digital Finance Institute in this roundup.

Launchfire’sLemonade training platform named to 2019 Top Training Companies roster for gamification companies.

The combination of cloud banking platform Mambu and international money transfer firm TransferWise will enable Mambu customers to offer fast, inexpensive, and transparent international money transfers at the real exchange rate. Mambu will leverage TransferWise’s TransferWise for Banks solution via API, giving its clients an out-of-the-box solution that allows them to focus on building a quality user experience and expanding their offerings.

“By plugging into our API, Mambu just became the world’s number one cloud banking provider to use for international payments,” TransferWise co-founder and CEO Kristo Käärmann said. “From their first day in business, banks gain significant advantages over their competitors, benefiting from the speed and convenience of TransferWise’s services.”

Mambu CTO/CPO Ben Goldin praised TransferWise’s innovations in global money transfer and highlighted the way the partnership will enable Mambu’s customers to take advantage of opportunities around the world. “We were impressed how TransferWise has established itself around the globe spanning infrastructure platform in a highly complex regulatory environment which aligns with our aims,” Goldin said. “We aim to offer best-in-class banking services through our cloud platform and are pleased that international banking is no longer of any concern for our customers.”

A Finovate alum since 2013, TransferWise has forged partnerships with companies like Alipay to enable fund transfers to China, and brought its TransferWise for Banks technology to Canada courtesy of a partnership with EQ Bank. Founded in 2010, the U.K.-based company moves more than $5 billion every month, has more than seven million customers, and estimates that it saves its users $1.5 billion in money that would otherwise be paid in hidden fees every year.

Transferwise has raised more than $772 million in total funding. BlackRock, Lone Pine Capital, LHV Ventures, and Andreessen Horowitz are among the company’s investors.

Germany’s Mambu offers a cloud banking platform that enables users to quickly build, launch, and service loan, deposit, and other financial products. Since its inception in 2011, the company has partnered with challenger banks like N26 and, more recently, teamed up with digital consultancy Mobiquity to provide its digital banking solutions to more financial institutions and fintechs.

“Our partnership with Mambu allows us to extend our service offering to the core banking layer, next to our existing solutions and serve our clients full circle on all layers,” Mobiquity Client Strategy Partner Paul van Dommelenn said. He referred to Mambu as having “a reputation as the most successful next-generation core banking provider.”

Mambu has raised $45.4 million (€42 million) in funding. The company is an alum of both our primary Finovate conference as well as our developers conference, FinDEVr.

The coronavirus pandemic has accelerated many technology trends that were already in place. The growing reliance on digital communication is one of many examples of technologies whose value we may have taken for granted and are once again re-appreciating. This is especially true for businesses that have not kept up with innovations in digital communications that now find themselves, due to the COVID-19 crisis, furiously trying to get their digital communications game up to speed.

For companies leveraging email as their communications channel of choice – out of preference or necessity – ensuring that their message is welcome, received, and engaged is key to making the email channel worthwhile and effective.

SparkPost, which celebrated the fifth anniversary of the launch of its cloud-based solution earlier this month, is one of the companies innovating in the email delivery and analytics space. Facilitator of more than a third of all B2C and B2B email, and featuring partners like SoFi and Salary.com, SparkPost offers a platform that leverages more than a trillion, worldwide data signals to increase email engagement and inbox placement.

And as the company recently recognized, the ability of institutions and organizations to rely on the effectiveness of their communications strategies is all the more important in times of crisis. SparkPost’s John Landsman, Manager of Research Analytics, discussed the challenge in a blog post last month.

“During this dire global health emergency, organizations in virtually every industry have been communicating with their stakeholders via email and have done so with urgency and precision,” Landsman wrote. He highlighted email’s unique feature-set as a channel: the ability to quickly target specific audiences with customized content – including multi-media content – and to be able to accurately and immediately measure engagement. “In all, the email channel is perfectly suited to the rapidly evolving communication needs of a public crisis,” he noted.

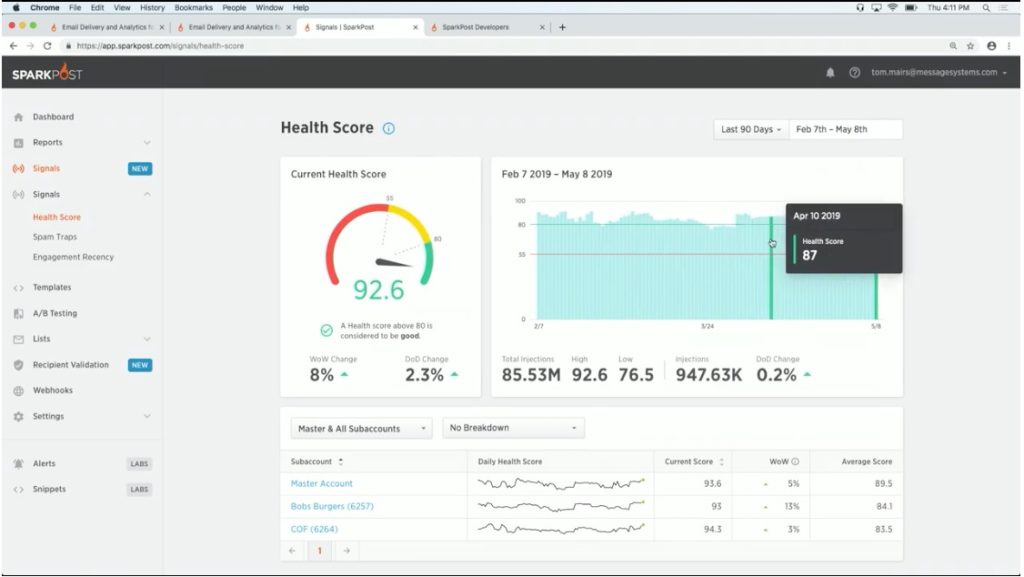

SparkPost’s Health Score gives companies deep insight into what factors are shaping email engagement rates.

Landsman referenced the surge in traffic on its own platform as an example of the explosion in email activity in recent months. Weekly volumes climbed from 3,600 campaigns in mid-February to 40,000+ campaigns a month later. The activity review also showed differences in read rates by sector (Transportation at the top; Financial institutions somewhere in the middle; Credit cards at the bottom). In a companion post, the SparkPost VP of Customer Success shared a set of best practices for companies looking to optimize their email communication strategy during a crisis. “While crisis communications are stressful to produce,” she wrote, “you can make a huge difference in how your company is perceived by sending valuable and relevant information during a tough time.”

The COVID crisis comes as SparkPost looks back on the work the company has done since launching its cloud solution and emerging from its previous incarnation as on-premises, enterprise-grade email server, Message Systems. Today the company has 6,000 customers and facilitates almost 40% of the world’s commercial email to the tune of 6+ trillion emails a year. And perhaps most critically, SparkPost’s platform gives them access to a robust collection of email intelligence data. This is what enabled the company to combine email delivery and email analytics in a new offering, Signals. This product leverages email intelligence data and machine learning models to anticipate potential recipient engagement issues before the emails are sent.

SparkPost’s Tom Mairs demonstrating Signals at FinovateSpring last May.

The anniversary also marks a significant shift at the top as SparkPost founder George Schlossnagle transitions from Chief Technical Officer to Chief Evangelist to make way for CPO Charlie Reverte’s promotion to CTO. “This amazing team has given me time to reflect on both what I enjoy and where I can add the most value,” Schlossnagle wrote at the company blog earlier this month. “I’m very excited to announce Charlie as our new CTO.”

SparkPost has raised more than $93 million in equity funding from investors including NewSpring Capital, LLR Partners, and Hercules Capital. Headquartered in Columbia, Maryland, the company demonstrated the Signals feature of its platform at FinovateSpring (this year, FinovateWest) last May.

The new strategic partnership between CuneXus and TransUnion, announced this week, will empower financial institutions to offer highly relevant financing offers to their customers. The collaboration matches CuneXus’ Perpetual Loan Approval platform with TransUnion’s vast data assets to deliver relevant brand experiences to consumers quickly, securely, and via the digital channels they increasingly prefer.

“We are thrilled to have found a partner with a long history of customer advocacy to enhance our application-free lending solution,” CuneXus president and CEO Dave Buerger said. “If the CuneXus platform is the engine, TransUnion’s wealth of data and knowledge is the rocket fuel.”

“The CuneXus solution allows lenders to harness the power of today’s most sophisticated data assets, like trended credit data, and operationalizes that data for maximum consumer impact,” senior director of credit unions for TransUnion Sean Flynn explained. “In addition, our combined solutions will enable lenders to deploy prescreen strategies that have been optimized based on our companies’ combined expertise and many years of evaluating best practices in consumer lending.”

CuneXus demonstrated its cplXpress lending and marketing automation platform at FinovateSpring in 2018. Named Best Consumer Lending Company in the 2020 FinTech Breakthrough Awards in March, CuneXus also announced a partnership with independent GAP program provider Frost Financial Services. That agreement will integrate Frost Financial’s auto loan protection products into CuneXus perpetual loan automation platform.

Founded in 2008 and headquartered in Santa Rosa, California, CuneXus began this year with an announcement that the company had topped 2019 projections with a 40% year-over-year gain in consumer reach and now has more than 120 financial institution partners. The company has raised $6.7 million in funding from investors including CMFG Ventures.

A Finovate alum since 2016, TransUnion is a global data and insights company that serves as one of the three major credit reporting agencies. Founded in 1968 and based in Chicago, Illinois, TransUnion collects and aggregates financial data on more than one billion consumers in 30+ countries around the world. The company is publicly traded on the NYSE under the ticker symbol TRU, and has a market capitalization of $13 billion.

Since the U.S. government launched the Paycheck Protection Program (PPP) to help keep small businesses afloat as they grapple with the economic effects of COVID-19, the program has received plenty of criticism.

Banks were vastly underprepared and under-informed about the program, which made them ill-equipped to support their customers. Adding to headaches, small business applicants were often left wondering if their application was approved and if and when they would receive funds.

Now on April 16, the program’s $349 billion has dried up. In some ways, this is a sign of success. Small businesses across the U.S. have been granted access to funds that otherwise they would now have via PPP loans. So where did the $349 billion go?

We checked in with data aggregation site covidloantracker.com which offers the following stats:

11,300+ small businesses have applied for loans

4% of small businesses have received their PPP funds

Average loan size was $216,000

The median PPP loan size is $98,500

Average payment speed is 8.2 days

The banks who distributed these loans primarily consisted of small, regional banks, which issued 76% of the funds. JP Morgan Chase paid out 10% and Wells Fargo and Bank of America each distributed 1%.

While small businesses from all 50 states received funds, more than half (54%) of the PPP fund recipients hail from Texas, while 21% came from Georgia, 30% from California, 18% from Wisconsin, and 16% from Illinois.

As for what’s next, Congress is currently working on adding more funds to the program. The cash should be available to small businesses “soon.”

When Movenannounced a transition away from being a provider of consumer banking services and toward business partnerships, few questioned the company’s capacity to win with enterprise customers. Founded in 2010 by Brett King, Moven has secured partnerships with financial institutions around the world, including Westpac in New Zealand, BCA in Indonesia, TD Bank in Canada, and, most recently, STC Pay in Saudi Arabia.

But there was some question as to what would happen with Moven’s customer accounts, which the company announced it would close by April 30, 2020.

We now have our answer: Moven will transition its customers to San Francisco, California-based Varo Money, which is in the process of securing its status as a challenger bank in the U.S.

“Moven has been a pioneer in the digital banking space and a long-time inspiration,” Varo Money CEO Colin Walsh said. “We are excited to welcome their customers and deliver on the types of technology and features they have grown to love.”

Moven CEO Marek Forysiak said the decision to choose Varo stemmed in part from compatibility with the company’s commitment to fostering financial wellness. The two companies are also looking into ways that Varo can leverage not just Moven’s former customers but also the business’ current and future digital banking technology as Varo continues on the path toward full bankhood.

“We are excited to partner with Varo ahead of their official national charter,” Walsh said. “Our patented financial wellness technology aligns with Varo’s efforts to help everyday Americans gain access to better financial insights and opportunities.”

Founded in 2015, Varo Money offers a mobile banking app, products such as a high-yield savings account, and services including early direct deposit. Available on both iOS and Android platforms, and charging no fees, Varo Money earned regulatory approval from the FDIC in February, insuring the firm’s deposits and giving Varo a major boost in its effort to become a full-fledged bank. To this point, the company has leveraged its partnership with Bancorp as its custodian; Bancorp is slated to transfer those customer deposits to Varo this quarter.

Named one of the 9 Best Checking Accounts for April 2020 by NerdWallet, Varo has raised more than $178 million in funding from investors such as Warburg Pincus and The Rise Fund. The company has an estimated valuation of $418 million.

What is the state of fintech as we move toward the second half of 2020? As expectations struggle to catch up with the worldwide public health challenge of the coronavirus pandemic, Finovate will dedicate a week to examining where fintech is right now and where it’s going over the balance of this historic year.

With a focus on the latest trends in payments, fraud and cybercrime prevention technology, bankingtech, and wealthtech, Finovate Fintech Halftime Review will kick off on June 22 and run through June 26. The digital-exclusive, five-day event will feature webinars, videos, white papers, eMagazines, and more – with each day dedicated to a key theme driving fintech today. Login and join us from the comfort of your home – or your home/office. The Finovate Fintech Halftime Review is a great opportunity to get a deep dive into the content that matters to you most.

Finovate Podcast Examines Fintech in the Age of COVID-19

Feeling isolated and anxious while sheltering-in-place? Listen in on some of the most insightful conversations about fintech and the economic challenge of the coronavirus pandemic on the Finovate Podcast.

In his most recent episodes, host Greg Palmer continues his Fintech in Extraordinary Times series, examining the impact of the public health crisis on technology and financial services. Check out his interview with Brett King, founder of Moven, and host of the Breaking Banks podcast; as well as his conversation with fintech expert and former Special Assistant to President Obama, Adrienne Harris.

Here is our weekly roundup of news from our Finovate alums.

Ethocaannounces extension of its partnership with Microsoft to give the company’s customers access to their digital purchase receipts.

ACI Worldwidepartners with High Payment Solutions (Hi-Pay) to build the first payments gateway service in Mongolia.

Salt Edgebrings PSD2 and open banking solutions to Roundups’ donation platform.

Avaloqintegrates the ACTICO Compliance Suite to help clients prevent financial crime.

Worldline partners with Meniga to boost digital customer engagement with Meniga’s personalized banking features.

Lendio and TouchBistro partner to help restaurants access PPP loan funds faster.

Glance NetworkslaunchesGlance for Financial Services, a co-browse, screenshare, and video tool.

Finantixcloses acquisition of Swiss data analytics company InCube Group.

Minna Technologieslaunches subscription management pilot for RBI’s Tatra banka.

Bankjoyinks partnerships with four credit unions in Minnesota, Oklahoma, and Nebraska with a combined $724 million in assets and more than 65,000 members.

Hong Kong Jockey Club customers look toDaon’sIdentityX platform for mobile login services.

Tinkpartners with Kivra to facilitate payment of bills and invoices.

Hyundai Card partners with Personetics to deliver financial insights and advice to credit card users.

BlueRushappoints Andrew Osmak as new Chief Revenue Officer.

EnveilreleasesZeroReveal Machine Learning, an encrypted machine learning product.

4Front Credit Union to offerPlinqit to help members save money and stay engaged.

Finovate Alumni Features and Profiles

Arxan Joins Two Firms to Form New Company – Application security company Arxan Technologies announced yesterday that it has joined forces with two other industry firms, CollabNet VersionOne and XebiaLabs, to form a new entity, Digital.ai.

Apiax on Why 2020 is Turning Out to Be the Year for Regtech – News from regtech companies has been flowing in 2020. Not only that, we saw significantly more regtech companies at FinovateEurope earlier this year than we have at previous events.

Onfido Raises $100 Million Because “Identity is Broken” – Digital identity verification platform Onfido reeled in $100 million in a round led by TPG Growth this week. The London-based company’s total investment now sits at just over $182 million.

How to Underwrite Loans When Everyone is a Higher Risk – COVID-19 has rewritten so many rules about the economy. It is now more difficult than ever to underwrite risk and ultimately understand if a consumer will pay back their loan.

Currencycloud and Derivative Path to Bring FX to Community Banks – A new strategic partnership between Currencycloud and cloud-based FX trading platform Derivative Path will make it easier for community and regional banks to offer a variety of FX and interest rate derivative trading options to their customers.

Kyckr Deepens Relationship with Citi – Regtech company Kyckr, which first partnered with its client Citigroup in 2016, has extended its relationship with the bank.

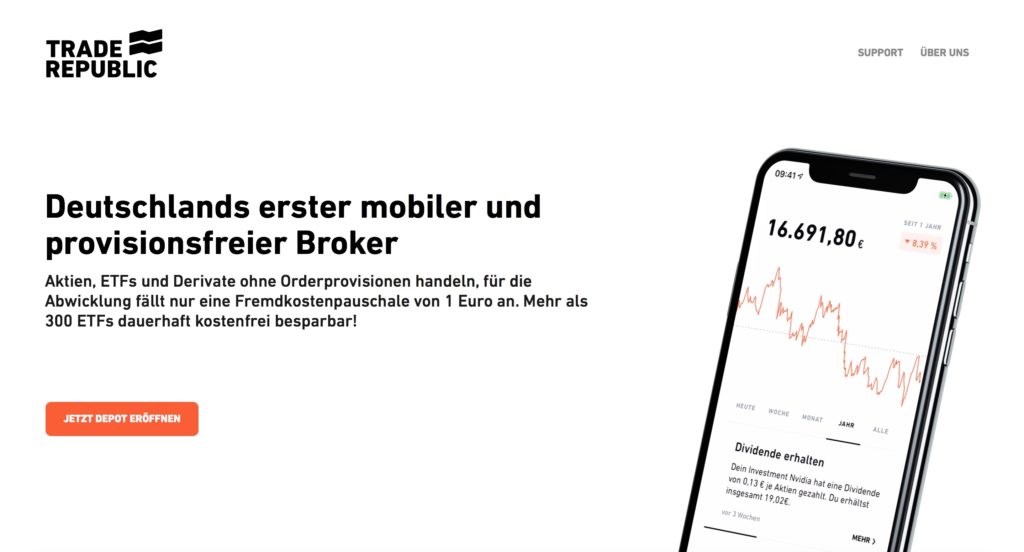

While mobile trading and investing app Robinhood rallies from a rough March toward a rumored $200+ million funding round, the company many are calling its European equivalent is making headlines of its own on the other side of the pond.

Berlin-based Trade Republic, which offers a mobile app that enables users to buy and sell stocks, ETFs, and other assets without having to pay a commission, announced that it has raised $67.4 million (€62 million) in new funding. The Series B round was led by Accel and Founders Fund, and will help the five-year old company build out its platform ahead of a formal launch later this year.

“About 85% of assets of European households are in bank accounts with mostly zero or negative interest rates,” Trade Republic co-founder Christian Hecker explained. “Our app enables people to invest their money safely, quickly, and transparently. By doing so, we are democratizing access to capital markets.”

With more than 150,000 users since its May launch last year, Trade Republic’s app is currently managing nearly one billion euros in assets.

Israel’s First Digital Bank Chooses Core Platform

The first digital bank in the country has no official name as of yet and, of course, no physical branches. But courtesy of a partnership with Tata Consultancy Services, the Bank With No Name has found its core platform in the form of the Banking Service Bureau, powered by TCS BaNCS.

“We have achieved a key milestone in the Israeli financial services industry by being onboarded on to TCS’ Banking Services Bureau,” bank chairman Shouky Oren said. “This approach will reduce the cost of banking for the average citizen and foster the development of innovative and differentiated services.”

The bank is slated to open in 2021 and will offer a wide range of services including deposits and loans, credit, account management, and securities trading. The firm will be the first company to receive a new banking license in Israel in more than 40 years.

Here is our weekly look at fintech around the world.

Central and Southern Asia

Indian SME and micro-enterprise lender Aye Finance raises $23.8 million in debt funding.

A partnership between Mastercard and Askari Bank Pakistan will help the commercial and retail bank expand its product portfolio.

Traxcn and IBS Intelligence report that India’s fintech industry saw a 40% gain in funding over the first quarter of 2020 compared to 2019.

GooglePay’s Nearby Spot feature, which helps users find essential stores and shelters in their area, goes live in India.

Latin America and the Caribbean

Sao Paulo, Brazil readies for the launch of a new digital challenger bank, Elas, dedicated to serving female entrepreneurs.

Coronavirus concerns have put the breaks on Mexico’s ability to license new fintechs.

Criptolago enables Venezuela’s oil-based stablecoin, PTR, to be transactable via text message.

Asia-Pacific

Japanese fintech Paidy raises additional funding from Itochu Corporation for its Series C round.

Vietnam-based microlender Finhay secures investment from Acorns co-founder Jeffrey Cruttenden and Thien Viet Securities.

Koinworks, one of Indonesia’s biggest P2P lenders, raises $20 million in debt and equity.

Sub-Saharan Africa

Flash, a fintech based in the Democratic Republic of Congo, introduces a new payment offering, Flash Money, in partnership with Visa.

PagaSystems and Nigerian fintech SystemSpecs join forces to boost electronic payments in Nigeria.

South Africa’s new fintech innovation hub goes live.

Central and Eastern Europe

Hamburg, Germany’s Deposit Solutions expands its partnership with Deutsche Bank.

NAGA, a German fintech that enables social trading and investing in stocks, cryptocurrencies, FX and other assets, announces profitability.

Born2Invest features venture investor and founder of iTLEADERS Yegor Klopenko on the challenge COVID-19 presents to Russian fintech.

Middle East and Northern Africa

Commercial Bank, based in Qatar, introduces new payroll service to help companies support employees’ digital international money transfers.

Mohamed Okasha, co-founder of Egyptian fintech Fawry, to launch $25 million fintech fund.

Qatar Development Bank (QDB) launches fintech incubator and accelerator programs.

Application security company Arxan Technologiesannounced yesterday that it has joined forces with two other industry firms, CollabNet VersionOne and XebiaLabs, to form a new entity, Digital.ai. Financial terms were not disclosed.

The three businesses will combine their expertise– business agility, software delivery, and application security– into a single platform. Overall, Digital.ai seeks to aid companies pursuing digital transformation to deliver digital experiences that customers trust.

“Digital.ai enables enterprises to focus on business outcomes instead of outputs, unifying value creation, delivery, and protection practices to drive efficiencies and create engaging, secure digital experiences that customers value and trust,” said Digital.ai CEO Ashok Reddy. “Now more than ever, it is critical that organizations leverage the power of business agility to optimize processes and make decisions rooted in customer centricity. Doing so will result in higher quality, more secure products that are delivered faster and drive stronger customer and employee engagement.”

Arxan’s approach to security is to protect apps “from the inside out.” The company protects the app’s binary code, JavaScript, and cryptographic keys to guard common entry points from fraudster attacks.

Digital.ai serves companies across multiple sectors including automotive, finance, digital media, gaming, insurance, medical devices, and more. The company’s customers include ABN AMRO Bank, KeyBank, KLM/Air France, Siemens, and Toyota.

Today’s news comes almost 20 years after Arxan’s launch. The San Francisco-based company was founded in 2001 by Hoi Chang and Mikhail Atallah. Since then, Joe Sander has taken the role as CEO.

In a round led by Bain Capital Tech Opportunities, behavioral biometric innovator BioCatch has secured a major $145 million investment. The Series C round featured participation from new and existing investors including Industry Ventures and American Express Ventures, and boosts the company’s total capital to more than $186 million.

BioCatch chairman and CEO Howard Edelstein put the company’s news and recent accomplishments in the context of the challenges brought about by the COVID-19 global pandemic. “The current environment has spawned a large increase in bad actors seeking to take advantage of distracted individuals working from home or dispersed companies whose technologists are scattered in remote locations,” Edelstein said. “In such times, technologies like behavioral biometrics become more important than ever.”

In a post published at the company blog, BioCatch Product Leader Ayelet Biger-Levin noted that since the pandemic began and more people began social distancing and working remotely, “phishing and malware have been the primary source of scams and cyberattacks.” Biger-Levin added that financial institutions are especially vulnerable to social engineering schemes in which unwitting victims are tricked into making authorized but fraudulent transactions.

BioCatch leverages more than 2,000 bio-behavioral, cognitive, and physiological parameters to create real-time risk scores that enable institutions to defend themselves against both human and non-human cyber threats. The company’s technology provides identity proofing to fight new account and account takeover fraud, as well as continuous authentication to verify identity from login to logout.

“BioCatch has quickly established itself as the pioneer in the digital identity space by developing next-generation behavioral biometrics technology that integrates fraud detection and authentication capabilities to protect end-users and their most sensitive transactions,” Bain Capital Tech Opportunities Managing Director Dewey Awad said.

BioCatch demonstrated its Passive Biometrics/Invisible Challenges feature of its platform at FinovateFall. The company has secured more than 50 patents, has 90+ million users, and has provided more than 10x ROI based on testimonials from customers such as NatWest, American Express, and Itau Unibanco.

Earlier this year, the company acquired fraud and anomaly detection specialist AimBrain. Founded in 2011, BioCatch is headquartered in Tel Aviv, Israel.