This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Multi-rail payments infrastructure platform BVNK recently published a report on stablecoin utility that examines how consumers actually use stablecoins. The report found that consumers’ desire to obtain stablecoins is rising, and that stablecoins are becoming a fixture of consumers’ savings portfolios.

Published in partnership with YouGov, Coinbase, and Artemis, the report is the result of a survey of 4,658 crypto and stablecoin holders across 15 countries. Here are four major findings from the survey:

Stablecoin holdings increasing

Of the stablecoin holders surveyed, almost half (49%) increased their holdings within the past 12 months, while only 7% of people decreased their holdings. More than half (56%) of crypto or stablecoin holders expressed plans to acquire more stablecoins in the next 12 months. This shows that stablecoins are transitioning from a niche tool into a mainstream asset.

Crypto owners are diversifying

The report also surveyed crypto holders who do not yet own stablecoins. Among this subset of non-owners, 13% said that they intend to acquire stablecoins in the next 12 months. In low and middle income economies such as Africa, consumers showed a higher interest in acquiring stablecoins for the first time. In fact, in Africa in particular, 76% of respondents said that they plan to acquire stablecoins in the next 12 months. This is a reflection of the utility of stablecoins in lower income regions.

Stablecoins and crypto are becoming a core element of savings

The stablecoin and crypto holders surveyed reported allocating around one-third (34%) of their savings to crypto and stablecoins. Almost half (48%) of respondents allocate up to a quarter of their savings to stablecoins and crypto. This shows that many consumers are beginning to treat digital assets not as speculative, but as a meaningful component of their long-term savings strategies.

Stablecoin holders are relatively young

Not surprisingly, more than half (54%) of those surveyed who own stablecoins are aged 18 to 34 years old. Of the respondents in the older age bracket of 55+, only 8% said that they currently hold stablecoins, while 17% of people in that age range said that they plan to acquire crypto within the next 12 months. This shows that stablecoin adoption is being driven largely by younger consumers who are more comfortable incorporating new financial technologies into their everyday financial lives.

Overall, the findings suggest that stablecoins are evolving beyond their early role as a trading tool within crypto markets and are beginning to function as a practical financial instrument for everyday users. As access to digital wallets and crypto infrastructure improves, stablecoins are increasingly positioned to bridge traditional finance and digital assets by offering consumers a way to store value, move money globally, and participate in global markets with lower barriers than traditional finance.

What is the state of community banking in the US today? How are community banks evolving and transforming at a time of both potential opportunity and unprecedented challenge and competition?

Success stories about how community banks across the country are taking advantage of new technologies like generative AI and embedded finance will be a major part of the conversation later this year at FinovateSpring, May 5 through May 7, in San Diego.

With that in mind, today we’re taking a look at the findings from the 2025 CSBS Annual Survey of Community Banks that was unveiled at the Community Banking Research Conference last fall.

Rising competition from within and without the community

The competitive challenge from nonbanks remains a major concern for community banks throughout the US. Especially in areas such as payment services and wealth management, these fintech competitors have effectively leveraged enabling technologies like AI and embedded finance to create digital platforms able to attract customers, especially younger customers who are digitally native and have fewer ties to the traditional banking system. Nonbanks without a physical presence, for example, produced a 7% year-over-year change in competitiveness in payment services, according to the community bankers surveyed.

That said, nonbanks still trail other community banks as the biggest competition in seven out of nine product and service categories. Community banks identified local regional banks as their main competitors in payment services and nonbanks as their primary rivals in wealth management and retirement services.

The battle over deposits continues to be a significant challenge for most banks and financial institutions, and community banks are no different. While transaction deposit levels have stabilized in recent years, competition from nonbank institutions has grown, especially among those nonbanks that are out-of-market. This has compelled community bankers to adjust their pricing strategies based on local market rates; the survey noted that the number of community bankers that said that they “always” responded to rate changes increased by more than 38% to represent a quarter of all survey participants.

Fraud and financial crime remain paramount concerns

In terms of internal risks, community bankers cited cybercrime as a top issue by far all others. Both credit and debit card fraud are the most common types of fraud reported in terms of dollar losses, with check fraud, identity theft, and account takeover also among the chief challenges. The survey noted that these financial crimes—card fraud, check fraud, and identity theft with account takeover—represent the lion’s share of both total fraud cases and dollar losses.

To this point, the community bankers surveyed indicated that they were putting resources to work combatting fraud and financial crime. After safety and soundness practices, money laundering and consumer protection standards maintenance accounted for the second and third largest commitments of total compliance expenses.

“We continue to put more resources into cybersecurity and technology risk,” one respondent noted, “which has grown rapidly as part of our cost structure. We’ve invested heavily in systems and processes and added staff to review outputs to protect customers and prevent fraud. Fraud is not yet a large loss item for us, but it could be.”

E-signatures and remote deposit over AI and BaaS

For all the talk of AI and stablecoins, the technologies that are moving the needle for many community banks are more pedestrian and practical than one might imagine. Technologies viewed as “extremely” or “very” important included such solutions as e-signature, remote deposit capture (RDC), and integrated loan processing systems. At the bottom of the list of priorities? Interactive teller machines (ITMs) and fintech partnerships for Banking-as-Service were deemed “not at all important” by more than 50% and nearly 40% of respondents, respectively.

Asked to look forward over the next five years, the responses from the community bankers are similarly grounded. The top response by far, with more than 75% of respondents in agreement, was that the expansion of mobile banking services will be the most promising opportunity for their bank in the next half decade. Fully integrated loan processing systems came in second at just over 61% with cloud-based core systems at more than 53%. AI? As a tool for enhancing customer interactions, AI technology earned less than half the number of respondents. Partnerships with fintechs? For digital transformation, about a third. For BaaS, about a fifth.

What do community bankers want from fintechs?

The 2025 CSBS Annual Survey is a rich source of information and insight into the thinking of community bankers in the US right now. For fintechs looking to work with these institutions, either as partners or vendors, the survey offers a number of takeaways that can help make those connections fruitful for both fintechs and community banks.

Boosting deposit growth—Fintechs can support community banks in boosting deposit growth by offering tools such as personalized savings plans and competitive interest rate management solutions. Enhanced customer engagement platforms that heavily incentivize deposit loyalty can also be valuable. Fintechs can also provide community banks with analytics to help them identify and respond to deposit trends.

Scalable loan management technology—Making the process of loan origination, underwriting, and servicing easier for community banks is key to helping them win against competition in key financing areas such as small business, agriculture, and commercial real estate. This is also where AI-powered solutions can have a dramatically positive impact. Streamlining processes, improving applicant review, and enhancing the customer experience in lending overall are areas where fintechs have a significant track record of success and can greatly benefit community banks.

Operational efficiency and compliance—It is true for most businesses and community banks are no exception. Enabling technologies are making manual tasks increasingly unnecessary, as automation and agentic AI transform legacy workflows into smooth operational processes free of human error. These technologies are also making it easier for institutions—including community banks—to be more aware of their regulatory responsibilities and to be better able to act quickly and completely to ensure compliance. Fintechs specializing in compliance management tools and services can be key allies for community banks at a time of significant regulatory change and uncertainty.

The International Organization of Securities Commissions (IOSCO) is out with a new report that highlights both the promise and the potential hazards of the tokenization of financial assets.

In a world in which stablecoins have increasingly defined innovation in the cryptocurrency/blockchain space, tokenization of financial assets is seen by some as the Next Big Thing in decentralized finance. Tokenization of financial assets refers to the process of representing ownership of a traditional financial asset, such as a share of stock or a bond, as a digital token on a distributed ledger or blockchain. Importantly, although tokenized assets can be transferred, traded, or exchanged between parties electronically, these assets are not cryptocurrencies—they are digital representations of regulated financial assets.

Valued for their ability to bring greater efficiency to the payments process—as well as their transparency, programmability, and potential to support financial inclusion via fractionalization—tokenized financial assets remain a new feature on the financial services scene. As such, there are myriad questions about how they can and should be used, as well as how they should be regulated. In their recent report, IOSCO, via its Fintech Task Force (FTF) and Financial Asset Tokenization Working Group (TWG) raised a number of these questions.

“The analysis shows that the majority of risks arising from the current commercial application of tokenization fall into existing risk taxonomies,” the report reads in its Executive Summary. “Market participants are not unfamiliar with managing such risk types. However, the manifestation of vulnerabilities and risks that are unique to the technology itself may require the introduction of new or additional controls to manage them.”

Here are three top takeaways from the IOSCO report on the tokenization of financial assets.

Legal Uncertainty and Ownership Rights

The biggest concern expressed in the report is the idea that there remains significant legal ambiguity about the tokenization of financial assets. This includes questions about the rights of ownership, transferability, and enforceability of claims.

“While there are currently well-established legal frameworks and structures for the treatment of financial assets created in paper certificate or book-entry form,” the report observes. “It can be unclear whether the existing legal treatment … applies to those created or represented in the form of tokens.”

In the absence of greater clarity on these legal framework issues, investors may find themselves unable to price or trade tokenized financial assets with confidence. This, at a minimum, can create asymmetry between investor expectations and outcomes and, at a maximum, contribute to more systemic uncertainty and challenges.

Infrastructure Risks and Operational Vulnerabilities

The second major risk discussed in the IOSCO report has to do with infrastructure risk, and the concerns range from the operational to the malicious. In either case, however, a major event that exposes these technical vulnerabilities could result in assets becoming permanently lost or cause an even wider market disruption.

Much of this concern is related to the relative newness of distributed ledger technology, as well as to some unique aspects of the technology compared to what is found in traditional financial markets. One example is the potential loss of a private key in a token structure, a phenomenon that does not exist in the world of traditional finance. The loss of a private key, which represents a sort of digital signature or ownership credential, would effectively result in the loss of access to the asset. To that end, a stolen private key would enable a criminal to steal the victim’s tokens.

“These assets face operational vulnerabilities and risks unique to this infrastructure, including cyber-attacks on blockchain nodes, congestion in transaction processing, data leakage, market fragmentation, smart contract bugs, and loss of private keys,” the report explains. “As tokenization scales up, regulators should also be cognizant of possible changes in market activities and market structure.”

Market Interconnectedness and Systemic Risk

A third concern is the creation of new dependencies and greater interconnectedness between market participants that is likely to happen as tokenization of financial assets scales. There are two versions of this. As an example of the first version, the report notes that a critical failure of a shared infrastructure, with multiple financial institutions tokenizing assets on the same blockchain network, could impact all tokenized assets on the network, rendering them temporarily or even permanently inaccessible.

Another example of the potential interconnectedness challenge arises as tokenized financial assets are increasingly used as collateral in cryptocurrency markets or as part of a stablecoin reserve. Here, the concern is that a crisis in the cryptocurrency markets such as a major or sustained stablecoin depeg could affect tokenized money market funds or government bonds being used as backing assets. The impact could readily spread to institutional investors with tokenized holdings, who would become involuntarily exposed to the heightened volatility of the crypto market.

Innovating for Known Unknowns

The quote from the report’s executive summary helps keep these and other concerns raised in the report in the proper context. While some challenges are more daunting, others more likely represent the kind of technological gauntlet that any product, service, or network must overcome as it scales. “Such risks and controls have been acknowledged by issuers and operators,” the report itself notes. That said, clear legal frameworks will be essential for addressing the broader challenges facing tokenized financial assets and unlocking their potential benefits.

CB Insights is out with its State of Insurtech Q3’25 report. The top takeaway? With the total number of deals down and merger and acquisition activity at record highs, the insurtech industry appears to be reorganizing to maximize the opportunities of scale, digital modernization, and market reach.

Deals Down

According to CB Insights’ research, the number of insurtech deals dropped to its lowest level since the second quarter of 2016. Q3’25 featured 76 insurtech deals, 65% less than the industry’s peak of 219 deals in the first quarter of 2021.

In addition to the number of deals being down, the median insurtech deal size has also decreased on a year-to-date basis from $3.8 million in 2024 to $2.9 million in 2025. The report indicates that a diminished early-stage pipeline is to blame. Year-to-date, 60% of all deals have gone to early-stage startups, the lowest deal-share percentage since 2011.

Lastly, the number of active investors in insurtech in Q3’25 shrank to the fewest since the first quarter of 2017. Especially notable was the quarter-over-quarter decline in investors making multiple investments, from 13 in Q2’25 to 4 in Q3’25.

Mergers and Acquisitions Up

At the same time, M&A activity in insurtech was on a tear, reaching its highest levels in three years. There were 21 insurtech M&A deals in Q3’25—the most since Q3’22 when there were 23 deals. This compares favorably to 16 deals in Q2’25. The report notes that the gains in the third quarter of this year helped reverse a trend of decreasing M&A activity between 2022 and 2024.

The reasons for the uptick in M&A activity are varied and interesting. Some analysts have suggested that business leaders are becoming increasingly confident in dealing with uncertainty and have embraced a “move through uncertainty” mentality, in the words of WTW analyst Jana Mercereau. Other factors include high stock market valuations, which can facilitate acquisitions; relatively stable interest rates; and the relatively weak M&A period from 2022 to 2024. The drive for digital modernization also plays a role. For its part, CB Insights offers an intriguing idea that the relative lack of attention from investors gave established insurance companies the opportunity to “engage more closely with emerging insurtechs.”

Insurtech in Q4 and Beyond

Heading into the final quarter of the year, there are a number of questions for insurtechs and many of them mirror concerns and issues in fintech more broadly. Which companies are actually putting AI to work in interesting use cases, and which are still in a pilot phase purgatory? How well are investors and establishment insurance companies recognizing where the value lies? How will evolving regulatory requirements incentivize regtechs to develop innovative compliance solutions for insurers? These are some of the questions that come to mind when reading CB Insights latest insurtech report. It will be interesting to see how the events of the fourth quarter and beyond help us answer them.

This year marks the year of the stablecoin, especially in the US. From the start of the year, we have watched as stablecoins evolved from a concept in trials overseas to a market force attracting billions in daily transaction volume, partnerships with major payment networks, active pilots among US banks, and a central focus of US financial regulation in the form of the GENIUS Act.

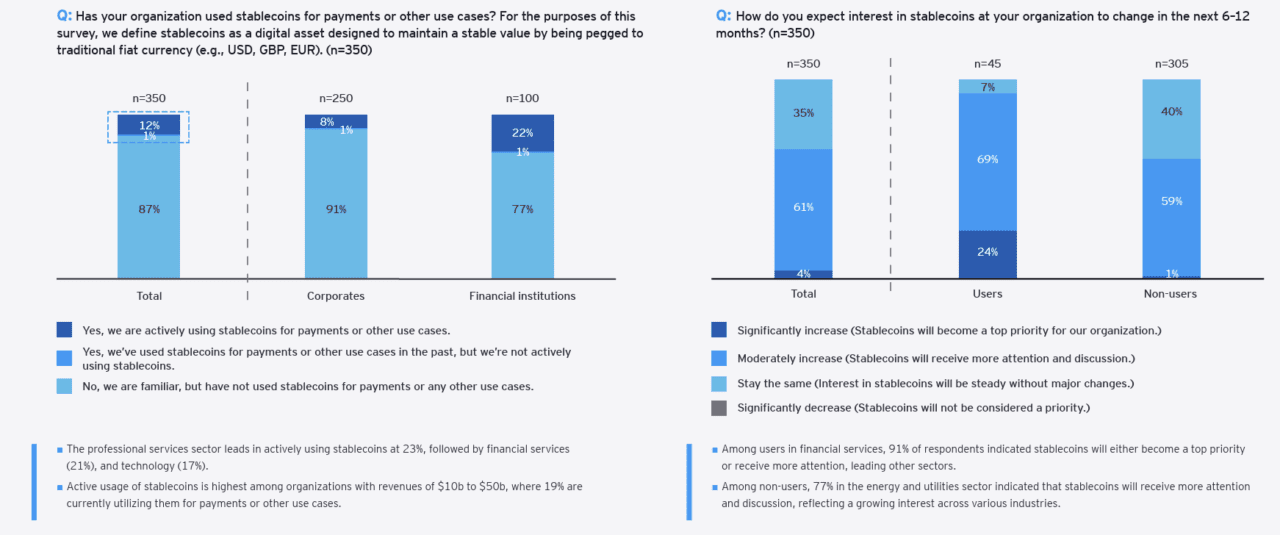

After the passage of the GENIUS Act in July, Ernst & Young’s (EY) strategy consulting services group EY-Parthenon surveyed more than 350 executives from financial and nonfinancial sectors about their views on stablecoins. Based on its findings, the firm generated a 31-page report that highlights adoption, usage, benefits, challenges, regulatory implications, and more. We’ve highlighted the report’s five major takeaways below.

Stablecoins are no longer fringe

All of the 350 executives surveyed are aware of stablecoins. Of those, 13% have already used stablecoins and 65% expect interest in stablecoins to rise in the next 6 to 12 months.

The fact that 100% of executives surveyed are aware of stablecoins demonstrates how quickly stablecoins have moved into the mainstream. For banks and corporates, the conversation around stablecoins is no longer a question of “if,” but rather “how fast” adoption spreads and what role the organization should play. This shift from niche to norm shows that institutions that wait to make a move may miss out on shaping standards and capturing early market share.

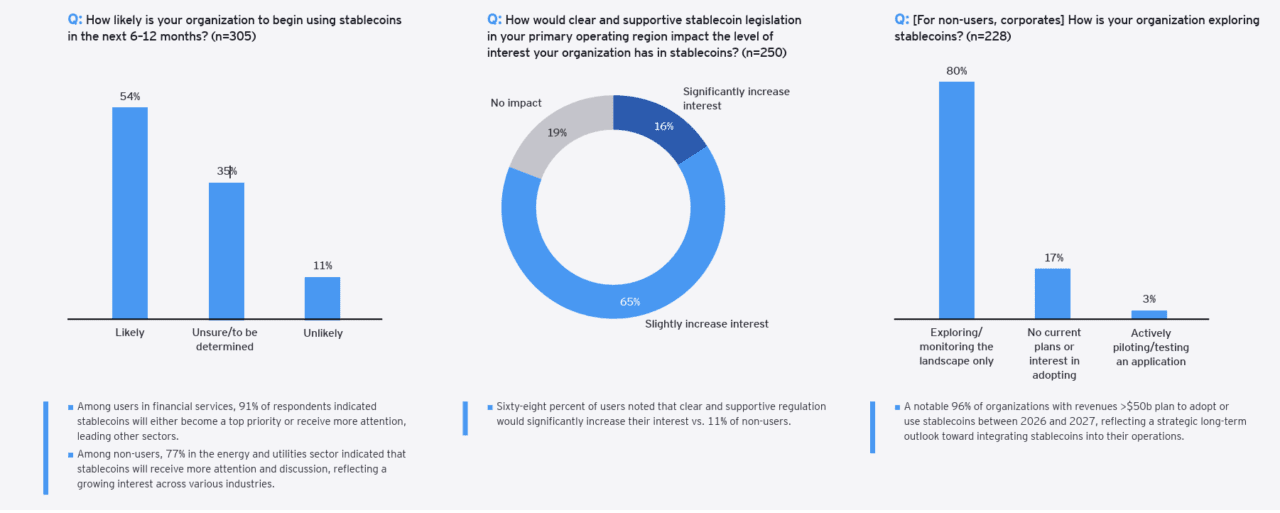

More than half, 54%, of financial institutions and corporates that are not using stablecoins expect to begin using them in the next 6 to 12 months. For 81% of participants surveyed, clear and supportive legislation increases their interest in stablecoins, either significantly or slightly.

With more than half of firms signaling plans to adopt stablecoins within a year, the market will likely see an acceleration in usage. For policymakers, this highlights the importance of regulatory clarity, given that it would directly boost adoption. For banks, it shows an opportunity to deepen their relevance by offering compliant, stablecoin-enabled services before competitors get there first.

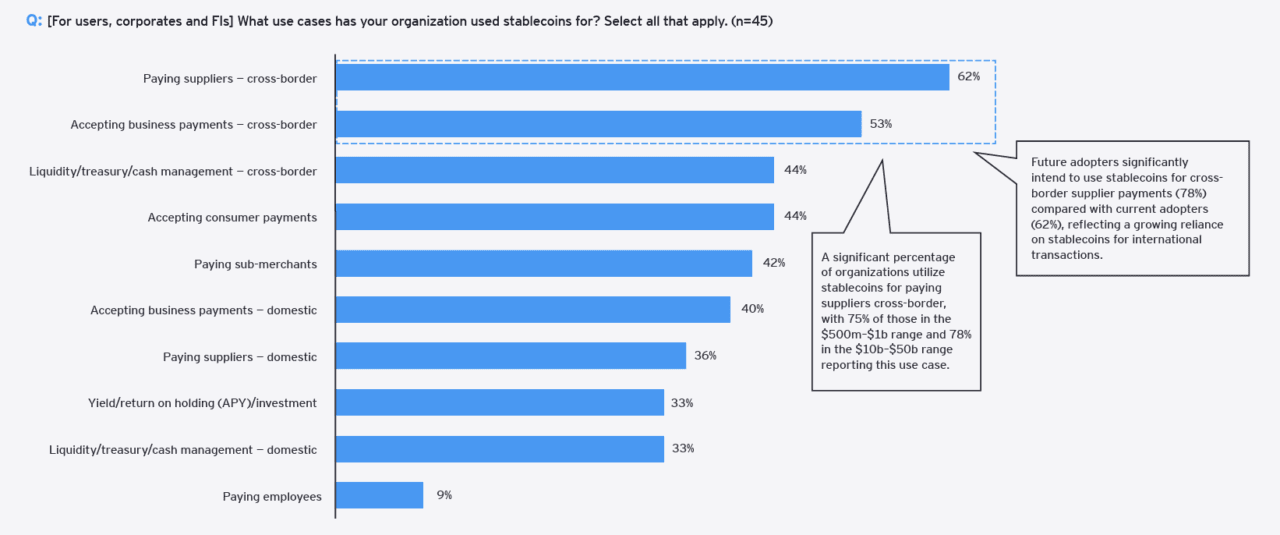

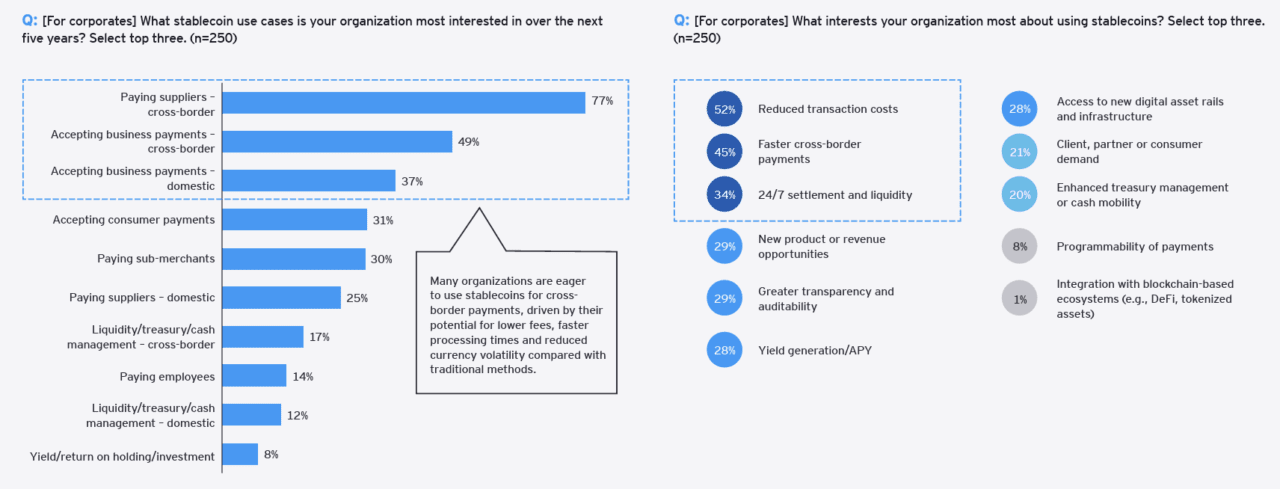

The survey asked about 10 different use cases. Of those ten, the top three use cases centered around cross-border payments.

This shows that stablecoins are tackling real, persistent pain points, especially in cross-border payments. Despite previous disruption by alternative players such as Wise, Remitly, and Revolut, international transfers remain slow and expensive. Stablecoins are a credible alternative that resonates with businesses and consumers. This focus could disrupt entrenched correspondent banking networks and give stablecoin adopters an edge in the lucrative field of cross-border payments.

Firms most interested in reducing cost and increasing payment speed

The most interesting use case is cross-border payments (77%), with interest largely driven by reduction in transaction costs and faster payments.

The overwhelming interest in cost savings and speed is a reminder that stablecoins will succeed or fail based on tangible value, not hype. For businesses, even modest reductions in cross-border fees can translate into significant savings at scale. Banks face the challenge of turning this efficiency into a competitive advantage, offering better pricing and faster settlement while managing risks.

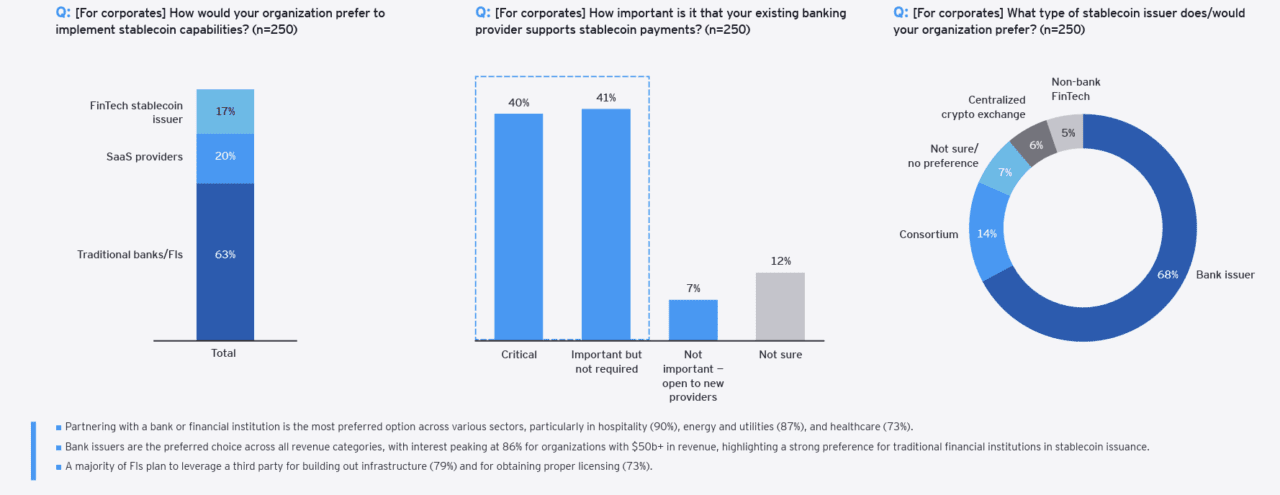

The survey found that organizations are looking to their traditional banking partners for access to stablecoins, and that most financial institutions, 79%, plan to leverage a third party for stablecoin infrastructure.

The finding that most organizations plan to access stablecoins through existing banking partners is significant. It suggests that businesses want access to stablecoins without having to deal with the complexity that comes with the new payment rail. Instead of investing in-house to leverage the new technology, they’re looking to trusted intermediaries like banks to handle the heavy lifting of facilitating the infrastructure. For banks, this is both an opportunity and a warning. Institutions that move quickly to build reliable, third-party-powered stablecoin services can strengthen client relationships, while laggards risk being bypassed entirely.

A new partnership between WealthAI and AI-driven investment solutions provider MDOTM will bring new portfolio construction, rebalancing, and automated reporting capabilities to financial advisors and wealth managers.

Courtesy of the partnership, MDOTM’s AI platform Sphere will be offered via the WealthAI Marketplace as a seamless integration into the WealthAI platform. This will enable wealth managers and financial advisors to access Sphere’s advanced AI tools for both portfolio construction and optimization from directly within their current WealthAI workflows.

“This partnership with WealthAI is a natural step in our mission to empower investment professionals with the most advanced technology available,” MDOTM Ltd. Chief Operating Officer Federico Invernizzi said. “By integrating Sphere into the WealthAI ecosystem, we are expanding access to our AI-driven investment platform, enabling a broader range of advisors and wealth managers to benefit from its capabilities. This collaboration reinforces our commitment to helping institutional clients make impactful, data-driven investment decisions at scale.”

Sphere enhances the investment process for wealth managers and financial advisors with three primary solutions. First, the platform delivers unbiased, AI-driven investment insights that transform complex market inputs into actionable ideas for portfolio and risk alignment. Second, Sphere’s Portfolio Studio offers mass customization and scalable portfolio rebalancing. Based on the manager’s or advisor’s strategies and objectives, Portfolio Studio enables users to scale the creation, personalization, and rebalancing of thousands of portfolios with controlled tracking error. Third, the platform’s StoryFolio capability allows managers and advisors to generate automated, portfolio-specific commentaries and reports that leverage Gen AI in order to turn complex information into customized investment narratives.

“We are thrilled to partner with MDOTM Ltd to bring Sphere’s powerful AI capabilities to our clients,” WealthAI Chief Executive Officer Jason Nabi said. “This partnership reinforces our commitment to providing wealth managers with the most advanced AI tools to deliver personalized, compliant, and efficient investment solutions.”

WealthAI offers an AI operating system for wealth managers, family offices, private banks, and asset managers. The company’s WealthAI Assistant is an agentic front-end that works like an intelligent co-pilot, using reasoning skills and the ability to adapt and take initiative to help relationship managers, portfolio managers, operations managers, and compliance officers become more productive and perform better. Founded in 2023, WealthAI is headquartered in London.

Based in London and maintaining offices in both New York and Milan, Italy, MDOTM made its Finovate debut at FinovateEurope 2025. At the conference, the company demonstrated how Sphere enables users to access AI-driven insights and build and manage portfolios at scale. Sphere also provides personalized, easy-to-understand portfolio commentaries and reports featuring both macro and market analysis on the current financial environment.

Speaking of reports, this spring MDOTM teamed up with EY to produce a report that examined the impact and value of AI in the wealth and asset management sector. The report Artificial Intelligence: The Value is in Scale, reviews the primary use cases for AI in wealth management and highlights deployment of the technology for document analysis, back-office automation, advanced search, personalized advisory, and market forecasting.

The report notes that wealth managers and financial advisors have been slow to embrace AI. A 2024 survey by EY European Financial Services indicated that more than 40% of investment managers believed they were “lagging behind” when it came to using AI, with only 5% referring to themselves as “at the forefront” in terms of AI use in their daily operations. In response to this, the report encourages firms to move from an “experimental” approach to AI and instead embrace a “continuous learning mindset.”

“Operators must build the infrastructural foundations, AI governance, and recognition of the value generated to base their transformation journey,” EY Wealth & Asset Management Leader, Italy, Giovanni Andrea Incarnato said. “Furthermore, it is of fundamental importance to recognize the value of external partners in creating these foundations in an ecosystem logic in order to accelerate adoption and leverage the economies of scale and experience already gained, proceeding with progressive internalization.”

Interestingly, the report reinforces findings from other European experts in AI implementation in financial services. This includes the “experimentation to execution” transition many see as key to successful and evolving use of AI in wealth management specifically and in financial services in general.

Global payments have been gaining popularity in fintech over the past few months. There is increasing demand for faster, safer, and cheaper payment opportunities as cross-border trade activity escalates.

As McKinsey points out, however, payments are becoming disconnected from users’ accounts as platform-as-a-service (PaaS) and embedded payments models rise in popularity. These models, which often provide a more seamless and tailored customer experience, may pose a challenge for banks. That’s because, in many cases, banks may need to build new businesses to keep their existing customers.

In its latest report, McKinsey offers data highlighting the growth of global payments revenues and details six trends that will define the next five years in the global payments landscape. While the report is full of valuable stats. Here are the points that I found most notable.

Historical unicorns prove promising

Over the past 10 years, the number of payments unicorns grew from 39 to 384, a group that boasts a combined valuation of $1 trillion. Though decreased funding and downrounds have slowed the growth of new payments unicorns, their track record has proven that, when the fintech sector begins to boom again, we will likely see a boost in high-value payments fintechs.

Growth of global payments revenue

Last year, the global payments industry processed 3.4 trillion transactions worth $1.8 quadrillion that generated $2.4 trillion in revenue. While this revenue figure has grown 7% each year since 2018, McKinsey estimates the growth will slow to 5% per year for the next five years.

Cash usage tanks

Since 2019, cash usage across the globe has dropped by 20%. The report notes that global cash usage continues to decline at 4% a year, but developing economies are experiencing a faster rate of decline than that of the U.S., where card usage has long been popular. While this report doesn’t mention it, countries with government-led payment schemes such as India (with UPI) and Brazil (with PIX) are also seeing a major decline in cash payments. In India, while cash payments still account for 60% of consumer expenditure, digital payments have doubled in the past three years.

CBDCs are more relevant than ever

According to the report, “More than 90% of central banks are pursuing or considering central bank digital currency (CBDC) projects, and more than 30 have rolled out pilots.” This figure was quite surprising, as I haven’t looked into CBDC projects since 2021, when only 43 countries were exploring the use of a CBDC. Despite U.S. hesitation to pilot a CBDC, I think we’ll see more discussion on the topic in 2025 as crypto grows and the environment becomes more crypto-friendly.

We know fraud is up, but by how much?

McKinsey’s report estimates that losses from global payment card fraud will reach $400 billion over the next ten years. Regulators have stepped up their efforts by increasing pressure on banks to comply, and as a result AML fines reached an all-time high, soaring past $6 billion last year.

Check out the entire McKinsey report for a better picture of today’s global payments landscape. With trends like embedded payments, declining cash usage, the increasing relevance of CBDCs, and the ever-present threat of fraud, players in the payments industry will need to not only innovate, but also to collaborate to remain competitive.

We all know that the VC investment scene is nothing like it was in 2021 and early 2022. With Q3 of 2024 behind us, we now know that fintech is still experiencing a funding downturn. In fact, both deal numbers and funding totals are down from Q2 of this year, with 179 fewer deals and $2.4 billion less in funding volume.

While the drop is sobering, however, there are a few bright lights in recent funding data that may signal the potential start of a positive turnaround. I took a look at CB Insights’ recent State of Venture Q3 ’24 Report, and here are my major takeaways.

Areas of micro growth

As mentioned previously, there are a few aspects of CB Insights’ recent data that offer signs of potential recovery:

Deal size The drop in the average size is leveling off. So far in 2024, the average deal size is currently $12.7 million, and compared the 2023 average size of $13.2 million, deal size falls around $500,000 short. This is much smaller than the $3.2 million drop that took place from 2022 to 2023, and looks quite favorable when compared to the $11.6 million drop from 2021 to 2022.

Even better news is that the median deal size has increased for the first time since 2020. Thus far in 2024, the median deal size has increased by $1 million. This comes after the median deal size dropped by $700,000 from 2022 to 2023 and decreased by the same amount from 2021 to 2022.

Resilience in early-stage investment The data regarding deal stage distribution shows that 71% of deals are still going to early-stage companies. This suggests that investors remain optimistic about long-term innovation in fintech, even if they are currently more conservative with growth-stage investments. Investors’ focus on early-stage companies could signal that they are planting the seeds for future growth, and may be anticipating a recovery in the fintech sector.

Areas of concern

There are, of course, still some less positive aspects of the Q3 investment data, notably, M&A activity and unicorn valuations.

M&A environment

The data indicates that interest in acquisitions is dropping. In the third quarter of this year, we saw 146 exits made via M&A. While this is an increase of six acquisitions when compared to the same quarter last year, it is down from both the first and second quarters of 2024, which were 161 and 159, respectively.

Increased M&A activity often suggests that the market is stabilizing, so the decrease suggests that investors are either still concerned about market conditions or are holding out for lower interest rates.

New unicorns

The number of new unicorns has dropped. In the third quarter of 2024, there were just two newly minted unicorns. This level is equal to what we saw in the first quarter of last year. The number of new unicorns has dropped from three in the second quarter of last year and from seven in the first quarter of this year.

Is this the bottom?

Looking at the data, it would appear that we are pretty close to the bottom of the fintech funding slump. And while I said that last year at about this time, this year, we have small signals to back it up. Specifically, the first increase in the median deal size since 2020 is quite encouraging and may indicate the potential for increased investor appetites.

It is no secret that banks are under pressure from a variety of sources: fintech upstarts, the rise of embedded finance, an increasingly dynamic regulatory environment, the pace of technological innovation–to say nothing of competition with one another.

For community banks, the pressure can be all the more intense. While many community banks enjoy a special relationship with local customers and businesses, this relationship does not prevent their patrons from wondering from time to time if the grass might be greener with a banking or fintech solution offered by another provider.

BNY recently surveyed community bankers to find out what they see as their top challenges–and opportunities–in the current environment. Conducted in partnership with the Harris Poll, BNY’s 2024 Voice of Community Banks Survey provides some interesting insights into where community banking is today, and what it needs in order to be successful in the years to come.

Wealth management and treasury services in demand

The growing interest in wealth management and treasury services was one of the more exciting insights from the BNY survey of community bankers. With the aging of the Baby Boomers and Millennials entering prime family formation years, it is little surprise to see a growing demand for everything from investment to estate planning. Relative to their larger rivals, community banks have not been as active in wealth management. But some have argued that community banks could change this by better leveraging their more personal relationships with their customer base to entice them away from faceless, corporate asset managers and large institutions. In fact, 100% of the community banks surveyed indicated that they want to add wealth management services to their offering.

At the same time, the interest in treasury services is perhaps even more eye-catching. The advent of real-time payments has made treasury services an increasingly attractive offering for financial institutions. In the same way that more personal relationships with individual customers can make wealth management services worthwhile for community banks to offer, so can the personal relationships these institutions have their local businesses encourage them to consider seeking treasury services where they are already doing much, if not all, of their banking business. According to BNY’s survey, fully 95% of community banks surveyed are inclined to agree that they would like to see treasury services added to their portfolio.

AI, tech, and digital transformation

While nearly half the community banks surveyed indicated that they saw themselves as “innovative within their communities,” that has not stopped most of them from wanting to enhance their products and services–as well as offer new ones– via digital transformation and enabling technologies. Interestingly, the survey did not just ask about technology per se, but instead queried them to find out specifically what they hoped these enabling technologies would do. To this point, nearly 30% pointed to efficiency and security as two major needs and indicated offerings like instant payments and automated loan processing both responded to these needs and helped community banks maintain “a competitive edge.”

Yet, while more than 90% of community banks said they were ready to embark upon digital transformations, significant uncertainty about the actual readiness remains. Approximately half of the respondents considered their data analytics capabilities–key for maximizing technologies like AI–to be “advanced,” and less than 20% believed that they had any real expertise when it comes to data analytics.

Non-fintech partnerships

Partnerships with technology companies and fintechs is one way for community banks to improve their ability to take advantage of enabling technologies like AI. However, one interesting reveal from the BNY survey was the interest that many community bankers have in non-fintech partnerships.

Almost 30% of respondents indicated that they saw non-fintech partnerships–collaborations with institutions in retail and education–as opportunities that would be as important as fintech partnerships over the next five years. This, arguably, should serve as a wake-up call for those fintechs that are innovating in adjacent areas–from e-commerce and consumer lending to financial education and even college prep.

AI may be one of the most misunderstood concepts in financial services at the moment. Not only is the technology complex, it also suffers from hype, bias, lack of transparency, lack of standardization, regulatory ambiguity, and it is constantly evolving. Accenture’s AI report helps demystify a bit of the AI enigma.

The firm spent multiple years surveying executives in a range of industries to compile a report detailing how to harness the power of AI. The firm surveyed more than 3,000 executives across 19 industries and 10 countries from November 2022 to November 2023 to compare how organizations leveraged AI.

Reinventing the enterprise

The main emphasis of Accenture’s AI report centered around reinvention. Accenture highlighted that reinvention is the key to unlocking the potential of AI for firms. Companies need to embrace reinvention as a deliberate strategy to fully leverage the powers of both AI and generative AI.

What it means to reinvent

Reinvention is more than just a buzz word. It involves firms transforming their entire organization by involving the whole C-suite in a collective decision-making process. Instead of simply adopting new technologies that fit into a bank’s existing approach, the entire firm must adopt a holistic approach that takes on four main attributes:

Encompass talent strategy Organizations must invest in training their entire workforce to understand and effectively use AI technologies. They must also attract new AI-skilled talent into their workforce by creating an attractive working environment and offering opportunities for growth and development. Additionally, firms must develop their leaders to understand AI’s potential and how to strategically implement it.

Break down organizational silos Because AI initiatives often require collaboration among different departments, breaking down silos ensures that all teams work together effectively. This also means that each silo needs to offer transparent access to its data (in a secure way, of course). By making data accessible across the entire organization, AI systems can leverage more comprehensive datasets for more accurate and helpful outputs. And, perhaps most importantly, aligning AI projects with broader business objectives helps ensure that the entire organization is working towards that same goal.

Embrace new ways of working To reinvent their current way of working, organizations need to embrace new ways of working and be open to change. Specifically, firms must adopt agile practices that allow them to iterate quickly, respond to changing markets, and continuously improve their AI systems. They also must create a culture of innovation that encourages experimentation, and offer flexible working arrangements that can improve employees’ productivity as well as their job satisfaction.

Continuously seek reinvention The final piece of the puzzle is that organizations must not stand still. Even after taking initial steps, firms must regularly evaluate and refine their AI strategy to keep pace with advancements in technology as well as changing business needs and shifting consumer demand. Additionally, organizations must continuously invest in research and development to explore not only new AI technologies, but also new applications of existing technology.

Benefits of reinventing

Those willing to reinvent their enterprise stand to reap multiple benefits. In addition to driving growth, productivity, and outperforming their competitors, firms that reinvent their enterprise to unlock the key to leveraging AI will enhance the user experience for their end customers, tap into data-driven decision making, accelerate innovation, manage risk, scale their business, empower their employees, and optimize resources.

By integrating these benefits into their reinvention strategy, firms can fully exploit the transformative potential of AI and generative AI, ensuring long-term success and resilience.

To learn more about what it means to reinvent your enterprise, including the seven components of the digital core outlined in Accenture’s AI findings, check out the free report.

The week begins with a few research-related announcements in the fintech and financial services space. CB Insights announced the availability of its State of Insurtech report for the first quarter of 2024, and the Federal Reserve Board issued a summary of climate risk resiliences exercises conducted recently by a handful of big banks. While the focus on this column in on the former, the publication of the latter shines some light on potential answers to the problems raised in CB Insights’ report.

With regards to the state of insurtech, there is still a great deal of hesitation among investors. CB Insights noted that quarterly funding for Q1 of this year was only $0.9 billion, the lowest level since 2018. Property & casualty insurtech suffered the most, with a quarter-over-quarter decline of 25%. Q1 2024 was also the first time since 2018 that there were no “mega-round deals” – investments of $100 million or more. There was some good news in Europe, as the number of deals increased slightly, as did the median insurtech deal size. But the overall message continues to be caution when it comes to investor attitudes about investech.

What Ails Insurtech?

Digital disruption: The challenge of digital disruption is one that the insurtechs share with the broader fintech community. The rise of enabling technologies such as AI will both steepen customer expectations as well as accelerate competition between companies to effectively deploy new, innovative solutions.

The insurance business is ripe for innovation. From the massive volume of manual processes and the document-intensive nature of the business to the challenges of underwriting and refining statistical models, the idea that AI will be a powerful ally in the insurance business is a no-brainer. One firm, Zippia, has predicted that as much as 25% of the insurance industry could be automated via AI by 2025.

There are obstacles. The disposition of regulators toward change in the industry is a major concern as new technologies are introduced to enhance operations like underwriting and statistical modeling. A regulatory authority that is indifferent, or hostile, to new technologies or their application in certain use cases can send a powerful signal that innovators are better off deploying their solutions in other industries or other geographies. Looking at the U.S., if the behavior of regulators toward innovators in the crypto space and the Banking-as-a-Service space is any indication, then we can expect to see insurtech and their investors to tread cautiously.

There are also challenges with regard to talent. Now that almost every company in every industry is looking to up their AI game, the fight over top talent in AI and automation has become all the more competitive.

Nevertheless, there is no doubt that AI promises to revolutionize many key processes that insurers rely on. And as those processes become more efficient – and as those companies best exploiting those AI-enhanced processes take greater market share – it is easy to see investment dollars returning to insurtech as investors begin making their bets on winners and losers in the space.

Climate change: The impact of climate change is another instance in which challenge and opportunity go hand-in-hand for insurtechs. The growing incidents of extreme weather – from temperature extremes to increasingly powerful hurricanes, floods, and other phenomena – have put a major strain on both property and casualty (P&C) insurers as well as those homeowners and individuals who rely on their protection. Note that CB Insights reported the biggest quarterly drop in funding this year was among P&C insurtechs. And of the top 10 P&C insurtech deals of Q1 2024, only three were U.S. based companies.

While many fintechs involved in climate change and sustainability have focused on helping businesses and institutions measure and better manage their carbon footprints, there is a need for technology companies in the insurance space that can help these firms build the models they need to better anticipate climate change-related risk. I mentioned the Federal Reserve report on climate resiliency earlier. The Fed’s report was a summary of an exploratory pilot Climate Scenario Analysis (CSA) exercise held by six U.S. banks: Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo. Among the conclusions that are especially relevant to this conversation were these two:

The role of insurance in mitigating climate change risks for consumers, businesses, and banks was emphasized, with a call to monitor changes in insurance costs and their impacts on specific markets and segments.

and

Participants expressed the high uncertainty and difficulty in measuring climate-related risks, making it challenging to incorporate them into risk management frameworks on a routine basis.

Insurtechs – and fintechs, for that matter – who are able to help financial institutions resolve these two issues, will find their services in demand as companies seek ways to quantify their own exposure to climate change risk. It is easy to envision other enabling technologies, such as quantum computing, also playing a part. Together, they could provide the kind of powerful modeling that would accurately gauge the risks of climate change and its potential impact on markets, communities, businesses, and families alike.

Moneyhub recently commissioned research into building societies and consumers, which involved interviews with building society leaders from the likes of Nationwide, Skipton, Yorkshire, Coventry, and The Building Societies Association. Additionally, 2,000 British adults were surveyed to find out about the sector’s digital readiness and the opportunities a more data-led proposition might offer.

Here’s what Moneyhub found:

Nearly 1 in 2 building society members report difficulties in engaging with their services.

80% of consumers believe that a good online platform is important when choosing a new financial provider.

66% of 18-34 year olds would like more convenient access to products and services without the need to visit physical bank branches.

Building societies are at a pivotal juncture. Traditionally known for their community focus and customer-centricity, they now face the urgent need to digitize to meet evolving consumer demands.

“Digitize or die”, a senior sector stakeholder said.

Moneyhub’s research highlights a stark reality: there is a gap between consumer expectations and the digital offerings of building societies. The company’s report – Digitize or Die: A Call to Arms for Building Societies – serves as a roadmap for building societies ready to embrace this essential transformation, ensuring they meet the needs of today’s and tomorrow’s consumers.