This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateAsia Digital on June 22, 2021. Register today and save your spot.

Cirrus helps lenders double their production without adding staff, providing an improved experience for the borrower and banker alike. Built “by lenders, for lenders,” Cirrus saves 15 hours per loan.

Features

Turnkey solution to enable online loan applications

Transparent status updates for all parties involved

Ability to automate collection of documents for existing credits

Why it’s great Cirrus eliminates ‘document chaos’ using human-centered design and workflow automation.

Presenters

David Brooks, CEO With twenty-one years in the financial services industry, Brooks has deep experience in commercial banking. His mission is to save the banking industry ten million hours of wasted time per year. LinkedIn

John DeMoss, Chief Development Officer An innovative and strategic executive, DeMoss is a serial entrepreneur with extensive financial services experience and multiple successful exits to his credit. He leads corporate development at Cirrus. LinkedIn

Ahead of FinovateFall Digital next week, we hear from Chad Hamblin, Global Industry Director of Financial Services at Microsoft, one of Finovate’s Gold Sponsors. Hamblin exploreswhy success will come down to understanding and empathizing with your client. Dig a little deeper into this topic with Microsoft’s eBook on the topic: Reimagine the client experience in wealth management.

COVID-19 has put a strain on everyone. We’ve all navigated social isolation, uncertain investment projections, and remote work environments. Regardless of the experience, this time away has left a haze over individuals and organizations alike. We’re not just unsure what comes next, we’re questioning the very processes we’ve accepted to this point.

Investors are feeling a new tension that makes small pain points all the more obvious. Voice automation, fixed fees, commissions — what clients once accepted as the cost of doing business are suddenly under intense scrutiny. Clients aren’t obligated to trust a major firm with their financial future, and now they’re acting on the opportunity to move their money elsewhere.

So how can wealth management firms adapt their strategies (and identities) to regain that trust? It all starts with understanding the client.

A holistic experience

Over the years, many wealth firms operated under a one-size-fits-most model — if the client fell into a specific demographic, then the firm provided a specific portfolio. Empowered by the Digital Age and amplified by this pandemic, a growing number of modern clients are looking for a wealth management partner—someone willing to listen to their ambitions, dreams, and goals and recommend actions catered to their unique circumstances. These clients want to feel identified, seen, and valued; they want to feel like more than an account number. Organizations can deliver on that expectation by creating a holistic client experience — a strategic client approach that uses technology and relationship-building to create a more inclusive perspective on the client’s needs, interests, and ambitions.

Delivering a holistic client experience comes to life in three ways: portfolios, services, and communications.

Holistic portfolios understand the client’s dreams, goals, and life events and work to build the right mix of investments to meet that individual’s financial plan, risk preference, and goals. By moving away from cookie-cutter portfolios and embracing a consultative approach, advisors create a partnership built on trust.

Holistic services encourage firms to expand their capabilities to adapt to a changing world. In the last decade, clients have become jaded by fixed-fee models. At the same time, online resources have made wealth management more accessible. By shifting to a holistic client model, organizations expand their services beyond portfolio management and provide added-value services like financial advice and planning, risk mitigation, goal tracking, wealth building strategies, and even bring in experts for specialized areas like real estate, education planning, tax mitigation, and estate planning. By expanding into capabilities that they may not have focused on before, wealth management firms further align with the individual goals of their clients and can offer one-stop solutions.

Likewise, holistic communication leverages the client’s communication preference. Every company has multiple engagement channels—voice, text, email, chat, video, social media, etc.—but most organizations assume that every client wants to be contacted via every channel. Yet, modern tools can equip firms to democratize their client data to share information and insights. By consolidating data and communication streams into a single hub of truth and by providing that information via client-friendly channels, wealth management firms can ensure that clients are engaged in the mediums they prefer.

Adapting in real time

It won’t be enough to lag behind your clients, real time adaptations and analysis will count.

While holistic client experiences serve as the star of wealth management’s future, next-generation technologies will be the foundation of these efforts. Trending tools like AI, life event and goal tracking, market risk analysis, smart portfolio allocation, and project automation equip organizations with the tools they need to build more responsive, reliable offerings for clients.

Imagine how predictive analytic tools will help determine the stability of future investments or the time employees could save on data entry through automation. Today’s technologies grant employees the tools they need to deliver a holistic customer experience by making their day-to-day tasks more efficient and effective.

Investing in trust

By creating a holistic client experience, wealth management firms become a reliable asset during hardship and a celebrated ally in victories. Right now, clients around the world are reassessing their investments for fear of a future crisis. In many cases, COVID-19 has fundamentally upset the way many clients view wealth management and building. It’s up to firms to empathize with those concerns and shape their efforts to bring peace of mind.

With a multitude of wealth firms fighting for their dollars, today’s clients are increasingly taking their funds to firms that demonstrate a conscious effort to understand their ambitions beyond executing trades. Wealth management firms that position themselves as true advisors and champion the hopes and dreams of their clients can foster trusting and long-lasting relationships.

The alternative is a slow descent into transactional business, commoditization, and ultimately irrelevance. The holistic wealth management firm is prepared to advocate for the best interests of their clients.

For more insights into how today’s firms can steel themselves for tomorrow’s challenges, read Microsoft’s latest eBook.

We talked so much about the Buy Now Pay Later (BNPL) revolution in ecommerce that we are starting to sound like a broken record (someone please explain that reference to the younger millennials in the room). But the no-interest financing strategy is quickly becoming a must-offer feature for merchants, card issuers, and other players in the ecommerce ecosystem.

This week brings news that Zip Co, a digital retail financing and payments services company based in Australia, has agreed to acquire New York based Buy Now Pay Later company QuadPay in a deal valued at $269 million. One of the biggest BNPL companies in the U.S, QuadPay will enable Zip to expand its reach to five countries (Australia, New Zealand, South Africa, the U.S., and the U.K.), a combined annualized revenue of $182 million (AU$250 million) and 3.5 million customers.

Aside from the company’s co-founders, Adam Ezra and Brad Lindenberg, Zip was the largest shareholder in QuadPay. Ezra and Lindenberg will join Zip’s global leadership team post-acquistion with the responsibility of scaling business in the U.S.

Hungry for good news on the fintech funding front? Gaze no further than Latin America where a new report from KoreFusion highlights growth in smartphone ownership, ecommerce adoption, and dissatisfactioin with banks as just a few of the reasons why Latin America’s fintech boom is ust beginning.

The study, available for free from the San Francisco, California-based consultancy, is based on a study of more than 1,000 fintechs in Argentina, Brazil, Chile, Colombia, and Mexico. In addition to a survey of the fintech landscape – finding a concentration in the payments category with lending and B2B-based fintechs coming in second and third, respectively – the report underscores other areas – such as remittances and foreign exchange – where it believe major opportunities remain.

Read more in KoreFusion’s 2020 Latam Fintech Report.

Here is our look at fintech around the world.

Central and Eastern Europe

German regtech 4Stop partners with payment service provider emerchantpay.

ACI Worldwide announces that its technology helps power 75% of real-time payments in Hungary.

German P2P lender auxmoney raises $177 million (150 million euros) in growth capital.

The following is a guest post from Scott Raspa, Head of Marketing, Hydrogen.

The European fintech scene has experienced tremendous growth over the last few years. One of the key drivers of this growth is open banking. This is causing financial institutions and fintechs to partner together to provide more innovative, user-friendly solutions for consumers throughout Europe.

European consumers are receptive to the idea of non-financial players offering financial products, according to EY’s Global FinTech Adoption Index 2019. The survey finds that fintech adoption throughout Europe, especially in countries such as the Netherlands, U.K., Germany, Sweden, and Switzerland, are well above the global average of 64%, and aren’t showing signs of slowing down any time soon.

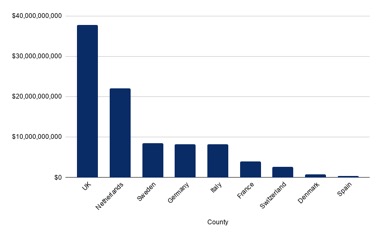

Below is a list of the top 50 fintech companies in Europe, based on their valuations.

These companies have raised over $16.8B (€14.3B) in venture capital funding and are valued, collectively, at over $92B (€78B).

The U.K. fintechs are valued at nearly $40B (€34B). The Netherlands are second, all thanks to Ayden, the most valuable fintech in Europe.

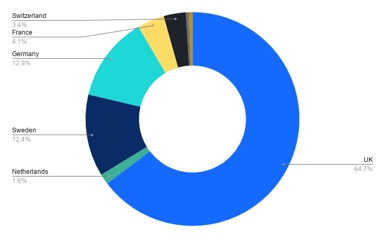

The U.K. has also invested the most money, nearly $11B (€9.4B), almost 65% of the funding of these top 50 fintech companies. After the U.K., Germany and Sweden have invested the most with 12.9% ($2.1B / €1.78B) and 12.4% ($2.0B / €1.7B) of the overall funding, respectively.

Fintech Enablement in Europe

Here at Hydrogen we work with companies all over the world. Our award-winning fintech enablement platform enables organizations to quickly and easily build fintech products and components. Whether you want to offer a PFM app in France, a challenger bank in the U.K., or issue cards in Germany, Hydrogen is here to help. Hydrogen has pre-built integrations, workflows, business logic, and UI already built in and available in white labeled/no-code modules or through our robust API.

It’s free to get started, so start building with Hydrogen today!

*Note: Funding information was provided by Crunchbase.com and the Euro, Pound, and US Dollar conversions were based off of today’s conversion rate. Also, total funding amounts didn’t include public companies or companies where we couldn’t identify the funding received.

In less than two weeks our all-digital, fintech conference, FinovateFall Digital will begin. If you haven’t registered yet for our week-long live and On Demand event – September 14 through September 18 – then there’s no better time than the present to visit our registration page and save your spot.

To whet your appetite for the latest in fintech thought leadership and technical innovation, we wanted to introduce you to ten of the industry experts who will be presenting keynote addresses during the week.

Pablos Holman – Futurist, Innovation Speaker, Inventor at the Intellectual Ventures Lab, Founder, Turing AI. LinkedIn.

There is no try but do: Raising the bar, passing the test, and innovating in a post-COVID landscape. Preview

Scott Gnau – Vice President, Data Platforms, InterSystems. LinkedIn.

“There’s a growing opportunity to lay the foundation for game-changing business data transformation that leverages both automation and analytics for sustainable success in any business climate.”

Digital Transformation’s Journey Toward Automation and Analytics.Preview

Jeremy Balkin – Head of Innovation, HSBC. LinkedIn.

“From robotics to wearables, how is technology being used to make us more human, to further financial inclusion and to allow for greater wealth creation?”

Technology and partnerships to bring people together, and the impact of COVID-19 on partnerships. Preview

Adam Dell – Head of Product, Marcus by Goldman Sachs. LinkedIn.

“What fintech trends will emerge as a result of the pandemic and how will consumer banking be changed forever?”

The Future of Finance: Predictions for a Post-Pandemic World. Preview

Sarika Sangwan – Global Head of Strategy & Marketing – Financial Services, Pinterest. LinkedIn.

“As one of the most trusted platforms, Pinterest allows FinServ partners to reach their target audience when and where it matters most.”

Rebuilding, capitalizing and maintaining customer trust in financial services. Preview

Tom Feher – Banking industry executive, U.S. financial services, Microsoft. LinkedIn.

“As the world continues to respond to COVID-19, we’re equipping our customers with the tools they need to respond, recover, and reimagine the future.”

Coming together to respond, recover, and reimagine during COVID-19. Preview

Paul Rohan – Head of Business Strategy – Finance, Google Cloud. LinkedIn.

“In the digital 21st century, customers expect their favorite brands to collaborate to provide extended and connected digital experiences.”

Open Banking is 21st Century Branch Banking. Preview

George Anderson – Founder and CEO, Ninth Wave. LinkedIn.

“Learn how leading banks are staying ahead of the surge in demand for transparent, secure, and scalable data connectivity from business, consumer, and wealth management customers.”

Mike Burr – Lead Android Enterprise Security Evangelist, Google. LinkedIn.

“Discover how to debunk security myths, and learn how the latest, multi-layered security protections, encompassing software, hardware, and application levels, now leverage the power of machine learning to protect your device fleet.”

Redefining the approach to mobile security in fintech (and why it works). Preview

Oliver Hughes – CEO, Tinkoff.

“Learn about achieving profitability as a digital bank, launching new products in the time of COVID-19, and what you need to be thinking about in terms of current and future trends in fintech.”

Digital banking in a post-COVID-19 landscape: The bright future of fintech. Preview

Fiserv announced the release of its AllData Connect solution today. The technology provides a single, authorized portal to facilitate third party access to consumer financial account data. AllData Connect makes third-party data aggregation simpler and makes screen scraping unnecessary.

“Consumers want to share their financial data with third parties in a model that’s both secure and convenient,” VP of Digital Payments and Data Aggregation at Fiserv Paul Diegelman said. “This process can be difficult for financial institutions to support if screen scraping impairs online banking performance, or when login credentials are stored at unaffiliated third parties. AllData Connect gives financial institutions the ability and insight they need to confidently empower consumers to share their financial account information.”

AllData Connect works by sending consumers to a Fiserv-hosted portal to verify their identity and provide consent for data-sharing. Once the consumer is validated by Fiserv and information access granted, AllData Connect delivers the permissioned data to third party apps for the specific activity. The solution provides confirmation and capture of consumer’s consent to share their data, managed access to online banking, secure storage of account holder usernames and passwords, and insights into where consumer information is being used. AllData Connect can also help FIs reduce the volume of unidentified bulk traffic that can inhibit website performance.

The new offering is the latest data aggregation solution within Fiserv’s AllData product suite. The suite also includes solutions for data integration by API, planning and financial management, and wealth management: AllData Aggregation, AllData PFM, and AllData Advisor, respectively.

The fintech industry has long fantasized about automating finances. The earliest example of this is automatic billpay, which is so common today it is considered table stakes.

Wealthtech player Wealthfront is taking personal finance automation to a new level today with the launch of Autopilot, the first service under the company’s Self-Driving Money umbrella. Autopilot takes Wealthfront Cash clients’ savings and automatically monitors their balances and moves money around on their behalf to maximize their savings and returns.

Wealthfront Cash is a challenger banking service the company launched last year. The account, which is key to the company’s Self-Driving Money concept, is fee-free and pays accountholders 0.35% APY on their savings. When an accountholder’s paycheck is deposited into their account, Wealthfront optimizes the allocation of the funds by automatically paying bills and routing the remaining funds to investments, savings accounts, debt payoff, etc.

“Our clients are diligent savers and follow best practices to grow their savings, but they struggle to prioritize managing their finances among a long list of competing priorities,” said Chris Hutchins, Wealthfront’s Head of Autonomous Financial Planning. “This can lead to missed days in the market or missed days of compounding interest, which has a huge negative impact on your long term net worth. Autopilot is your free financial assistant, automating your financial tasks to ensure your savings are put to work immediately in the best account for your goals.”

Wealthfront’s next development will improve upon the speed of money movement within its ecosystem by implementing services such as same-day investing. The company already offers clients the option to receive their paychecks up to two days early when they use direct deposit with their Wealthfront Cash account.

“We’ve set out to build a new system that makes money with our clients, not off of them as traditional banks do,” said Wealthfront Co-founder Dan Carroll. “The system we’re building has the potential to be one of the biggest wealth creation engines of our generation, automatically optimizing your money in the background while saving you time and stress.”

The following is a sponsored post from Michael Hom, Head of Financial Solutions at InterSystems, Gold Sponsors of FinovateFall Digital 2020, September 14 through 18, 2020.

Currently, external factors like the COVID-19 pandemic mean that the global economy has become increasingly volatile and capital markets firms are having to work harder than ever to make sure users, both retail and institutional, can continue to trade without interruption.

As these financial organizations look to mitigate risk in this period of uncertainty, gaining operational resilience, implementing risk mitigation strategies, and having the right technology in place will be crucial to continue to deliver value to customers, comply with regulations, get ahead of the competition – and, most importantly, maintain trust.

Given this, the pressure for incumbents to upgrade infrastructure is only increasing, but challenges remain in doing so. While the pandemic may have been the linchpin for organizations to start embracing new technologies there are still barriers to overcome and best practices to be put into play to not only mitigate risk, but also prepare capital markets for what’s to come in the future:

Replacing legacy technology

Critical to mitigating risk is ensuring data is available quickly and easily accessible. For many capital markets firms this is an area where they struggle due to a significant amount of legacy technology in their infrastructure and, consequently, data siloes.

Connecting these disparate systems will be vital to not only help them with performance issues they have today, adapting to situations such as mass remote working, for example, but also so they are capable of growing with them into the future.

This requires them to adopt solutions that can seamlessly run, scale, and expand into the cloud. By replacing legacy infrastructure, they will have the benefit of providing new technologies and innovations access to their wealth of valuable data.

These solutions should also be location agnostic to allow capital markets firms to be agile and take advantage of new technology and services and bring that into their existing infrastructure.

Investment in the future

As these institutions look to replace their legacy technology, they should focus their investments on two key areas.

First, they should invest in platform scalability as being able to scale up as the market spikes is crucial and can be a major differentiator. This scalability can even give firms a competitive edge with some firms having recently gained market share solely due their ability to scale up.

The second area of investment should be in analytics and automation that can support and, in some cases, reduce the manual-intensive workload. We’ve already seen increases in algorithmic trading and customer chatbot technologies, while many organizations within the financial services industry use AI to automate processes, such as fraud checks and compliance.

With less time spent on time-intensive manual tasks, capital markets firms will be able to direct their attention to more value-adding services for their clients. The use of AI will help to spot patterns and anomalies in those patterns much faster for fraud prevention, while also reducing the risk of human error.

Gaining access to real-time data

Is your data strategy keeping up in real-time?

Within capital markets firms, there is a growing requirement to be able to access real-time data so these organizations can simplify their stack and get access to transactions that are happening in the moment. This will allow them to produce more time-sensitive reporting so they can make appropriate business decisions and better comply with regulatory requirements.

Data fabric

Data fabrics are fast becoming a key trend within data management across the board, helping to reduce friction. Improving the accuracy, availability and accessibility of data and should also be a consideration as capital markets weather this period of uncertainty and beyond.

A data fabric that uses the latest technology will help organizations to better grasp data governance, ensure that their data is clean and accurate, to harmonize that data where appropriate, and make it more accessible. All of these will help them derive more value and better insights from their data to help drive their enterprises and those of their customers forward.

How can capital markets firms not only survive, but also thrive?

As capital markets firms look beyond this period of volatility to thriving long term, it’s vital they embrace agility by implementing modern technology with a focus on analytics and automation. This will allow them to quickly adapt to changing and new business needs by helping them to make use of their data, analyze it, monetize it, and turn it into actionable intelligence.

In an increasingly competitive landscape, where new market entrants aren’t weighed down by legacy technology and architectures, this will be a key differentiator and enable capital markets firms to take advantage of new opportunities within the market faster.

If you want to hear more about this subject, listen to this webinar in which InterSystems takes a deep dive into the challenges facing capital markets firms and how they can mitigate risk, alongside a panel of other industry experts from Northern Trust, Westwood Group, and SIX Securities & Exchanges. Or read InterSystems‘ latest blog posts on Data Excellence.

Buy Now Pay Later (BNPL) is having a moment in fintech. And one of the leading players in the space is expanding its innovations into the offline realm.

Minnesota-based Sezzle unveiled its virtual payments card this week, helping users benefit from its BNPL technology during their in-store shopping trips. The company has partnered with card issuing platform Marqeta to power its new virtual card.

Sezzle virtual cardholders will be able to use Sezzle’s installment payments technology in-store at retailers that already accept Apple Pay and Google Pay, as well as online. The purchases are interest-free and can be split into four installments, paid out over six weeks.

Sezzle Virtual Card

“As traditional, in-store retail re-emerges, it’s critical that we support our merchant partners by giving them new tools to jump-start sales, both online and in-store,” said Sezzle Co-founder and Chief Technology Officer Killian Brackey. “As a proven solution for driving incremental sales and new customer growth, we are thrilled to publicly announce an easy way for U.S. retailers to offer Buy Now, Pay Later in store.”

The in-store user experience is simple. At checkout, consumers authenticate themselves and tap their phone at the point-of-sale terminal, which will activate their Sezzle card.

Sezzle’s news comes on the heels of PayPal’s announcement that it plans to add a BNPL competitor. The payments giant revealed on Monday the launch of Pay in 4, a short-term payments installment product for U.S. customers.

Four-year-old Sezzle, which listed on the Australian Stock Exchange (ASX) last summer, has seen a recent uptick in adoption, spurred by the economic effects of the coronavirus. The company added 325,000 new users in the second quarter of this year, up 326% from the same period last year. Sezzle has a market capitalization of $848 million.

I was pretty excited for my first ride in my nephew’s brand new Tesla. The car was a major upgrade from his previous vehicle: a Jeep with “character” that had both broken down and been broken into a few times too many. His visit – and the Tesla’s – also marked the first time my wife and I would have company over for dinner since the COVID-19 pandemic struck, so there was more than a little to look forward to.

And while the Greek burgers were good and the tzatziki and baklava even better, my ride in the brand new Tesla was … kinda underwhelming.

Admittedly the experience as a rider in a Tesla is not identical to the experience as a driver. But as I slowly emerged from my initial shock at the lack of ornamentation, the absence of anything even resembling a full service dashboard and began to appreciate the machine’s unnaturally silent acceleration, its “It’s-All-on-the-Tablet” functionality, and “front trunk,” it dawned on me just how dramatically Tesla had reduced the driving experience to its most essential features and then turned them up to eleven.

What does this have to do with banking?

My Tesla experience reminded me of the challenge of distilling customer experience into its most necessary aspects. This is what drives innovation in everything from PFM apps that provide account balances without requiring login to mobile brokerages that cut out the stock market’s most hated middle man – commissions. Yet what is a trifle to one customer can be a can’t-do-without attraction to another. In the same way that I found myself in my nephew’s Tesla actually missing the dials, buttons, and other dashboard gizmos that had once defined automotive technological sophistication, so will many consumers find the leanness of new digital banks, for example, and perhaps even the trend away from what might be called “the human touch” in financial services to be a less appealing customer experience rather than a more fulfilling one.

In this way, I wonder if it is helpful to think of two innovation tracks for banks and financial services. One track is the one we spend most of our time reading and thinking about in fintech circles: the digital-first if not digital-only mobile bank that caters to the young, the mobile and, ironically, to both the hyper social connected individual and the asocial consumer who believes that automated checkouts at the grocery store are the best thing since sliced bread. Here the innovations are mostly technological, leveraging AI, machine learning, Big Data, and other leading technologies to provide more data, more services, faster, with a premium on seamless, frictionless, no frills interactivity.

But there is – or at least could be – another bank. And while it is digital, as well, and provides many if not most of the same basic financial services as any other bank, this bank focuses more on responding to the personal and social worlds of its customers. This bank puts financial inclusion and wellness at the center of its mission, sponsoring and providing educational opportunities for members of the local community – including their children who are likely getting precious little financial education in school. In-person credit counseling and financial planning would also be a good fit for an institution like this, which would play a role in the private sphere of a community that is similar to the role a local library or post office plays in the public sphere. At more advanced levels, coursework and training for individuals looking for careers in financial services could be offered, as well.

Not necessarily 100% or exclusively brick and mortar, this truly community-based financial institution would provide a customer experience that would be very different from its all-digital cousin, but one that could be just as innovative by using technology to make finance and financial services easier to understand and easier to incorporate constructively in the average working and middle class person’s life.

A new partnership between device identity and authentication innovator Entersekt and fellow Finovate alum NuData Security will integrate the latter’s NuDetect behavioral analytics solution into Entersekt’s Secure Platform (ESP) to provide real-time, seamless identity verification.

“By combining our leading techniques, we unlock new ways to remove friction for users interacting online, on web or mobile,” Entersekt Chief Strategy Office Dewald Nolte said. “The combination is like none other on the market, in usability and security, and is another exciting leap forward in our mission to make the digital world safer and more user-friendly.”

NuDetect leverages both device-based and behavioral data to identify and distinguish legitimate users from potential fraudsters in real-time. The technology features an additional level of protection, a step-up authentication process, involving an in-app push prompt, FIDO-certified security key, or other option, which can be triggered in higher-risk circumstances. The result is a fast, secure, digital identity authentication experience that verifies legitimate users whether logging in, creating an account, or completing a transaction seamlessly.

“By adding behavioral analytics to the Entersekt Secure Platform,” NuData Security SVP Michelle Hafner said, “we provide an additional layer of protection while simultaneously reducing friction and improving the customer experience.”

The Entersekt Secure Platform helps businesses ensure rapid deployment and integration of Entersekt services such as Transakt for digital security and authentication, Connekt for digital payments enablement, and Interakt for non-app-based authentication. The platform enables banks and other large companies to better identify their customers’ specific needs, engage them effectively with smart messaging (and accurately with robust authentication), and empower them to get more done with less effort.

Headquartered in Cape Town, South Africa, and founded in 2008, Entersekt began this year working with Netcetera to help the company provide enhanced authentication technology to card issuers in Germany, Austria, and Switzerland. This summer, Entersekt announced a successful technical integration with Huawei Mobile Services, and released its updated security guidance for financial institutions in light of new digital security threats with the onset of the public health crisis.

Current, a challenger bank focused on underbanked consumers, locked in a partnership with InComm, a prepaid solutions company.

By teaming up with InComm, Current will allow its 1.4 million accountholders to deposit cash to their Current account at select physical retail locations.

The new solution is powered by InComm’s Vanilla Direct platform, which will leverage a barcode on the Current app. While visiting one of 60,000 participating retail chains, including 7-Eleven, Dollar General, and Family Dollar, accountholders can give the cashier their cash deposits. The cashier, in turn, scans the barcode on the customer’s Current app, and the cash is delivered to their account.

“Our VanillaDirect mobile barcode solution is perfectly aligned with Current’s vision of bringing financial services to its customers, and in this instance providing their customers with a simple and convenient experience for making cash deposits in an extensive network of retail locations across the United States,” said Tim Richardson, Senior Vice President at InComm.

Traditionally, users at online-only banks deposit cash via ATMs. This solution, however, may not be appealing to underbanked users. Additionally, it would require Current to form ATM network partnerships.