Online insurance marketplace CoverHound announced a partnership with Intellirent, a rental marketing and tenant screening platform.

The partnership will enable renters whose landlords use the Intellirent software suite to access instant quotes on renter’s insurance leveraging CoverHound’s insurance marketplace. CoverHound offers renters transparency across policies while Intellirent benefits from the simplicity of a single partnership.

“The majority of real estate professionals using our service require their renters to maintain an insurance policy,” said Corey Eckert, founder of Intellirent. “By partnering with CoverHound, we can eliminate the hassle of insurance shopping for renters while providing these agents with a streamlined process they can share with their new tenants.”

CoverHound VP of Product and Personal Lines, Kelli Broin, explained that the partnership will help renters get insurance to protect what matters to them. She added, “Our streamlined process enables renters to compare quotes online and easily purchase the coverage that’s right for them.”

CoverHound was founded in 2010 to offer an insurance marketplace where consumers can shop around for auto, homeowners, renters, and life insurance. In 2016, the company expanded to offer insurance for small businesses, providing a range of insurance options including worker’s compensation, liability, cyber insurance, and more.

At FinovateFall 2013, CoverHound CEO and founder Basil Enan and CMO Keith Moore demoed the company’s mobile app. Last fall, CoverHound expanded its network of partners and insurance carriers. The company works with top carriers including Chubb, Liberty Mutual, Hiscox, Progressive, biBerk, Safeco, Nationwide, Mercury, and Hartford Steam Boiler.

Headquartered in California, CoverHound has raised a total of $56 million.

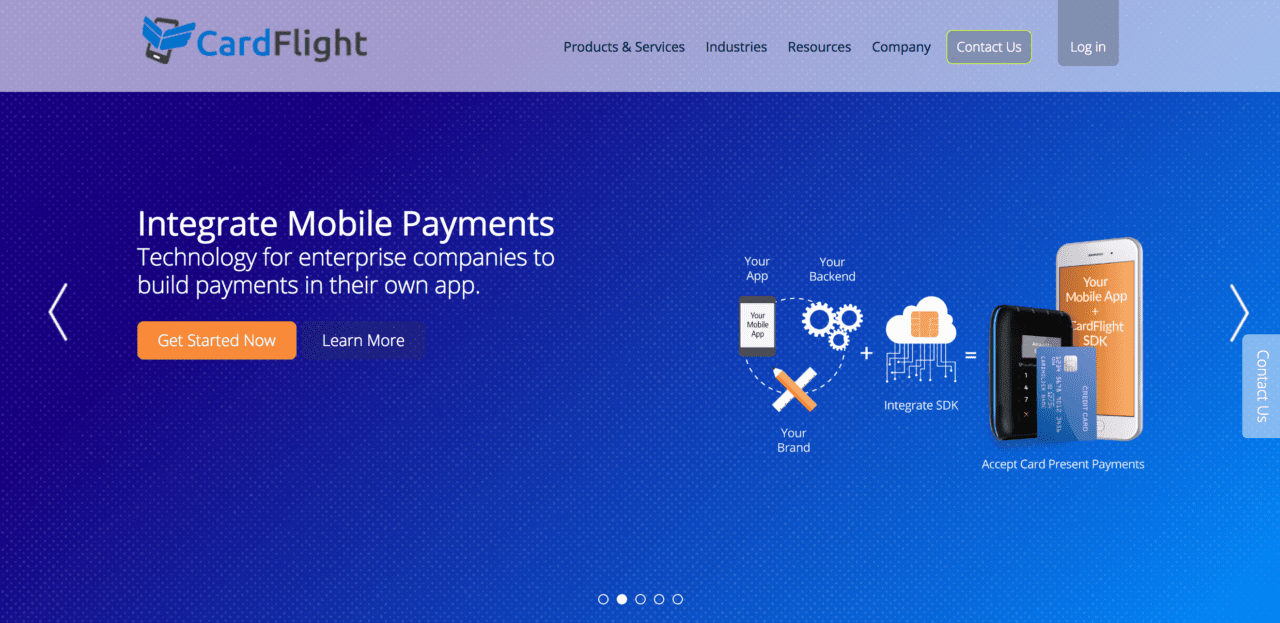

The partnership will enable Boomtown’s U.S.-based merchant acquirer and independent sales organization clients to offer CardFlight’s SwipeSimple payment acceptance solution to merchants. An EMV capable POS system, SwipeSimple is available as both a mobile or countertop register version and comes with back office reporting software to help businesses manage their inventory and operations. The SwipeSimple Register version (pictured right) was

The partnership will enable Boomtown’s U.S.-based merchant acquirer and independent sales organization clients to offer CardFlight’s SwipeSimple payment acceptance solution to merchants. An EMV capable POS system, SwipeSimple is available as both a mobile or countertop register version and comes with back office reporting software to help businesses manage their inventory and operations. The SwipeSimple Register version (pictured right) was