This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Embedded finance and digital banking solutions provider Finotta has announced a strategic partnership with Constellation Digital Partners (Constellation).

Constellation will integrate Finotta’s Personified platform into its own solution to help credit unions offer personalized financial guidance to their members.

Finotta made its Finovate debut at FinovateFall 2022 in New York.

Embedded finance and digital banking solutions provider Finottaforged a strategic partnership with Constellation Digital Partners (Constellation). A cloud-native digital banking services provider, Constellation will integrate Finotta’s Personified platform into its own solution to give credit unions new resources to boost member engagement and satisfaction, as well as drive digital growth.

“More than 90% of consumers expect their financial institution to offer a modern digital banking platform, but this is table stakes,” Finotta Founder and CEO Parker Graham said. “The key is differentiating the experience based on what members need and want, which is financial guidance. Unfortunately, this is also where massive missteps are made. Many traditional PFMs inadvertently shame consumers for poor financial habits rather than encourage positive behavior, killing the overall experience. As a result engagement is down considerably.”

Founded in 2018 and headquartered in Overland Park, Kansas, Finotta made its Finovate debut at FinovateFall 2022 in New York. At the conference, the company demoed Personified, a suite of products that enable FIs to provide personalized financial guidance via their mobile banking apps. Personified helps financial institutions anticipate member and customer needs, increase product conversions, and deliver actionable financial guidance – all in a single solution. The platform helps banks and credit unions leverage the digital channel to generate more revenue, improve financial performance, and boost profitability for members and customers.

Last year, Finotta noted that its Personified platform had increased user engagement compared to other mobile banking apps, with an average use of 13 minutes per month per user. According to Graham, this compares favorably to the “less than one minute per month” that users spend on the average mobile banking app. Not only does this reflect a significant lack of engagement from users, it also limits the FIs ability to cross-sell other products and services. Finotta also pointed to a study from Oracle that suggested as much as 40% of customers believe that independent PFM apps are superior to the offerings provided by most financial institutions.

“Embedded (Finotta’s) technology into our platform will equip credit unions with the tools they need to thrive in the digital age while delivering personalized, seamless, and exceptional service to their members every step of the way,” Constellation SVP and Head of Product Aaron Oplinger said. “We look forward to the value this will bring our industry.”

Founded in 2017 and headquartered in Raleigh, North Carolina, Constellation Digital Partners is a leading provider of mobile and digital banking solutions for community-based financial institutions. The company is dedicated to empowering both credit unions and community banks with innovative solutions for mobile banking, online account management, personalized financial insights, and more. The company has raised $17 million in funding via a Series A round completed in 2020. Kris Kovacs is President and CEO.

Business banking platform Rho has partnered with Navan to launch a jointly branded tool that will allow Rho’s business clients to add and manage their Rho Corporate Cards directly within Navan.

The partnership is leveraging Navan Connect, a card-link technology that extends Navan’s No Expense Reports experience to authorized expense partners.

The new, joint tool offers business clients a unified interface that saves them from having to coordinate multiple applications across separate vendors, or having to manage different costs and workflows.

Rho has teamed up with Navan to launch a new, jointly branded tool that will help simplify the way businesses manage their finances.

Leveraging Navan Connect, the new co-branded solution will allow businesses to add and manage their Rho Corporate Cards directly within Navan after configuring the cards using the Rho platform. Businesses can use the new finance suite to manage corporate travel and expenses, enforce expense policy compliance, send payments, and close their books. The unified interface saves businesses from having to coordinate multiple applications across separate vendors, or having to manage different costs and workflows.

Launched in 2023, Navan Connect is a card-link technology that extends Navan’s No Expense Reports experience to authorized expense partners. Using this technology, businesses can embed travel and other spending policies with Rho, which will offer finance departments control of and visibility into employee expenditures.

“We’re excited to partner with Navan to help businesses simplify the finance stack and save time and money,” said Rho Co-founder and CEO Everett Cook. “The years we’ve spent building the world’s best business banking platform infrastructure opens up ample opportunities for Rho to explore compelling partnerships with world-class organizations like Navan.”

New York-based Rho was founded in 2018 to serve as an all-in-one financial platform for businesses and organizations. In addition to checking and savings accounts and credit cards, the company offers expense management, AP automation, treasury management, and now business travel expense tracking and management.

Formerly known as TripActions, California-based Navan was founded in 2015 and leverages AI to create an enhanced user experience around booking corporate travel. Navan has made four acquisitions and now counts 2,900+ employees across 40 markets.

“Small- and medium-sized businesses need a complete suite of financial tools to get them up and running quickly,” said Navan Expense CEO Michael Sindicich. “With Rho, Navan customers now have an out-of-box set of financial tools from a trusted financial partner to help them proactively control spend as they scale while increasing operational efficiencies so companies can focus on the objectives that matter most.”

Ireland-based digital banking and payment solutions provider CR2 has agreed to be acquired by Morocco-based Hightech Payment Systems (HPS).

The transaction will strengthen HPS’s value proposition in French-speaking markets in Africa and help the company expand into English-speaking Africa and Australia.

CR2 made its Finovate debut at FinovateFall 2014 in New York.

Irish digital banking and payment solutions provider CR2 has agreed to be acquired by Morocco’s Hightech Payment Systems (HPS). The move will bolster HPS’s digital banking and payment capabilities and consolidate the company’s status as a leader in the African market, especially in its Francophone regions. The acquisition also will help HPS expand in English-speaking Africa and Australia due to CR2’s strength in these markets. Terms of the acquisition were not immediately available.

“We are pleased to be joining Abdeslam and the team at HPS,” CR2 CEO Fintan Byrne said in a statement. “Together, we share a wealth of experience, a passion for innovation, and a relentless focus on customer success.” Byrne added that the acquisition aligns with CR2’s global expansion goals. “With additional scale comes even more opportunity to invest and innovate. This is an exciting time to be in the digital banking and payments technology sector,” Byrne said.

A Finovate alum for more than a decade, CR2 offers digital banking and payment solutions via its flagship platform, BankWorld. The platform gives more than 90 banks in 50+ countries a comprehensive suite of digital banking, digital wallet, and payment functionalities. HPS will combine CR2’s technology with its PowerCARD suite of payment solutions which is used by 500+ institutions in more than 95 countries. HPS further noted that CR2 will “contribute materially” to its financial bottom line, post-acquisition. CR2 generated revenues of €23.8 million in the 12 months leading up to June 2023.

“Today marks a significant milestone in the continued growth of HPS,” HPS Co-Founder and CEO Abdeslam Alaoui Smaili said. “CR2 has a differentiated and exciting capability set, which is a strong fit for HPS and adds significant depth and breadth to our platform.”

Founded in 1995, HPS is a multinational corporation that provides payment software and solutions for issuers, acquirers, card processors, independent sales organizations (ISOs), retailers, mobile network operators (MNOs), and more. HPS is headquartered in Casablanca, Morocco, and has been a member of the Casablanca Stock Exchange since 2006.

Headquartered in Dublin, Ireland, with offices in Dubai, Jordan, India, and Australia, CR2 most recently demonstrated its technology at FinovateFall 2014 in New York. Earlier this year, the company announced a strategic partnership with U.K.-based core banking and financial solutions provider Fimple.

This is a sponsored article by LiveBank by Ailleron

In this digital age, the banking sector is not just undergoing change; it is at the cusp of a revolutionary transformation that is poised to redefine the very fabric of financial services. This transformative wave is powered by the synergistic relationship between human intelligence and artificial intelligence (AI). Far from merely mechanizing existing processes, this collaboration aims to completely reimagine how banking services are delivered, making them more intuitive, efficient, and customer-centric.

Transforming Human-to-Human Interaction through Technology

At the heart of this transformation is the role of Generative AI. This advanced form of AI is transforming modern banking by enhancing the human element rather than replacing it, particularly in complex sales processes. For example, while simpler banking products have become largely automated and can be easily accessed online by customers independently, more intricate products – like those involving mortgages or business financing – still benefit significantly from human insight. However, AI tools in banking is not replacing the need for human interaction; instead, it enhances the advisory services provided by banking professionals, making these interactions more productive and customer-friendly.

Entirely Digital Mortgage Application Process

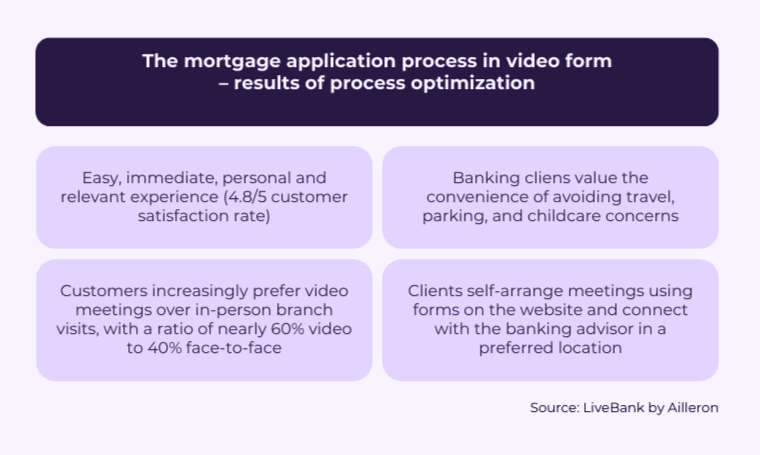

A vivid demonstration of this innovative approach was showcased by LiveBank in collaboration with ING Bank on the London stage. They illustrated how digitization could reinvent the mortgage process, which has traditionally relied heavily on face-to-face interactions and extensive paperwork. By integrating AI with digital technologies, LiveBank has transformed this process to better align with contemporary customer expectations, which include a seamless digital experience, personalized service, and simplified procedures that significantly cut down on processing times.

As a leader of Retail Banking in ING emphasized during a joint speech, “Customers seek the convenience of applying for a mortgage online, uploading required documents electronically, and monitoring their application’s progress in real-time. They also prioritize transparency, clear communication, competitive interest rates, and personalized guidance throughout the mortgage journey. Ultimately, they desire a smoother and more efficient experience compared to traditional paper-based methods.”

With 45% of consumers favoring digital channels for banking product purchases, LiveBank aligns perfectly with the modern client’s preferences. It streamlines banking operations and enhances customer service by offering real-time human-to-human assistance through the customer’s first-choice communication channel.

The entire presentation and more insights are available here.

How to Redefine an Online Mortgage Experience?

ING Bank has been expanding its remote customer service capabilities, particularly for clients interested in mortgage offerings. The journey began with the option to submit applications via phone through the Contract Center, which was later extended to include customers using the services of specialists in ING’s branches.

Recognizing the evolving landscape of customer expectations, ING took the initiative to introduce video call options, marking a significant advancement in providing clients with a seamless remote banking experience. This decision entailed evaluating both customer needs and advisor perspectives.

Success Story of ING Bank & LiveBank by Ailleron

To ensure alignment with customer expectations, ING conducted comprehensive research, actively seeking feedback and insights. Valuable suggestions emerged from this process, including the need for video meetings with specialists in local branches, especially in emergency situations.

In response to these insights, ING embarked on a journey to integrate customer expectations with the capabilities offered by video support tools. This strategic alignment not only enhances the remote banking experience but also underscores ING’s commitment to innovation and customer-centricity.

This transformation is crucial in today’s banking landscape, where customer expectations are increasingly geared towards digital solutions. The transition involves not only adopting new technologies but also rethinking the customer journey to make it as frictionless as possible. By reducing the need for in-person meetings and streamlining documentation, banks can address significant pain points, making the process quicker and more pleasant for customers while also optimizing operational efficiency.

The successful digital transformation of complex banking products like mortgages requires thorough organizational preparation. It entails understanding and integrating the needs and expectations of all stakeholders involved – both customers and bank employees. This preparation is critical to ensure that the new digital channels are not just new tools but are part of a holistic strategy to improve both customer and employee experiences.

Bank Branches and Their Role in Building Customer Relations

The recent pandemic has accelerated the shift away from traditional branch-based banking towards more dynamic, digital models. This shift has prompted banks to rethink the role of physical branches. Despite their reduced footfall, branches continue to play a critical role, particularly in fostering stronger customer relationships. Recognizing this, LiveBank has innovated a new approach where loan specialists are made available to clients through convenient video calls, allowing for digital collaboration throughout the loan application process. This approach not only maintains the personal touch that is often crucial in banking but also enhances convenience and efficiency.

Furthermore, LiveBank’s method allows clients to choose how they wish to engage with the bank, emphasizing the flexibility and client autonomy that modern customers desire. This model has proved successful, leading to a majority of remote interactions with over 400 branch mortgage specialists (60% of new meetings were on video) while maintaining high levels of customer satisfaction 4.9/5 – a testament to the effectiveness of integrating personalization with digital efficiency.

How to Increase Sales in Banking Using AI & GenAI Capabilities?

The expansive capabilities of Generative AI were further highlighted at FinovateEurope in London, where banking experts showcased how AI could elevate the credit process. AI assists bank advisors by managing vast amounts of data and providing insights, thereby enhancing their ability to offer tailored advice. Additionally, the use of advanced AI-driven avatars can pre-qualify customer needs, ensuring that when a client is handed over to a human advisor, the groundwork is already laid for productive interaction.

This blend of human empathy and machine precision is crucial. It leverages the strengths of both to optimize banking operations and tailor services to individual needs, thereby not only elevating the efficiency and effectiveness of banking services but also enriching the customer experience with a personal touch that technology alone cannot provide.

Human Empathy Meets Machine Precision to Optimize Banking Operations

LiveBank exemplifies this future, standing at the forefront of the transformative journey in banking. Its platform is meticulously designed to integrate the capabilities of humans and machines seamlessly, ensuring that every customer interaction is a blend of efficiency, personalization, and security. The key to their success lies in finding the optimal balance between human and artificial intelligence, using the unique attributes of both to deliver high-quality service in real time.

In conclusion, as the banking sector moves forward, the integration of human and machine intelligence holds incredible potential. Innovations like those pioneered by LiveBank are not just enhancing operational efficiencies; they are fundamentally enriching how customers experience banking. This is a visionary journey, one that promises to transform the landscape of financial services and set new standards for the banking industry worldwide.

Mateusz Grys, LiveBank by Ailleron speaker said, “Generative AI is a major trend reshaping our industry, but the human aspect remains critical, especially in sales and advisory roles. It’s crucial for dealing with complex banking products that customers may encounter only once in their lifetime. By integrating AI, we enhance these interactions, but the empathy and understanding of human advisors are irreplaceable when navigating such significant financial decisions.”

With neobank Monzo’s big investment and multi-billion dollar valuation on one side and the continued woes of BaaS provider Synapse on the other, “interesting times” continue to characterize the fintech landscape as we slide into the summer months.

Be sure to check our Fintech Rundown all week long for the latest updates and fintech headlines.

Insurtech

Indian insurtech CoverSureraises $4 million in pre-Series A funding in a round led by Enam Holdings.

The demos are done. The votes have been counted. And the people have spoken. After two days of live fintech demos here at FinovateSpring 2024, we are proud to introduce the winners of Best of Show.

Bloom Credit for its technology that helps banks and credit unions offer a deposit retention and credit building tool to their client base.

Cascading AI for its platform that improves efficiency in banks by 30x by automating rote tasks, enabling banks to leverage that step-change in efficiency to grow their top and bottom lines.

Kobalt Labs for its solution that helps fintechs and financial institutions accelerate and strengthen their third-party diligence, leading to faster and safer paths to revenue-generating partnerships and operational efficiency that doesn’t increase headcount.

QuickFi for its technology that enables banks and manufacturers to give their business customers a fully digital, self-service finance experience that’s fast, intuitive, and consistent with how modern business borrowers prefer to do business.

Remynt for its platform that helps creditors achieve higher recoveries and recapture defaulted consumers as customers when their financial position improves.

SAVVI AI for its solution that helps financial services companies step into the age of AI, with faster, more accurate forecasting, without changing their workflow or processes and using their existing teams.

A heartfelt thanks to all of our demoing companies for sharing their latest fintech innovations with our FinovateSpring audience. Be sure to check out the Finovate Podcast featuring Greg Palmer in the weeks to come as he interviews FinovateSpring 2024’s Best of Show winners.

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The six companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2024 conferences are below:

Today’s customers want personalized experiences, but how can companies drive meaningful one-on-one connections at scale?

Data wins!

Handled correctly, well-orchestrated data reaches customers the way they want to be reached: fast and seamless while facilitating loyalty and trust.

The next generation customer experience is made easier with LeanData, the leading Revenue Orchestration platform. LeanData connects the dots for over 1,000 companies, increasing speed-to-response and aligning go-to-market motions with efficiency.

90% reduction in data duplication

78% decrease in time needed to research records

5 hours per week saved by eliminating manual processes

Time-to-response decreased from 1 to 2 days to less than 1 hour

This week, Finovate Global looks at recent fintech developments in France.

French start-up Lydiaannounced the launch of a new digital banking brand this week. Named Sumeria, Lydia plans to invest more than €100 million in the new initiative, as well as hire 400 people over the next three years. Sumeria, according to a post on LinkedIn, offers 4% interest and is designed to be a “simple and accessible banking super app.

“We are convinced that technology (cloud, mobile) is not an end in itself, but a way to simplify life, through everyday details,” the company noted in a statement on its website. Arguing that current accounts should be neither “trendy gadgets” nor make users captive to a given app, system, or institution, the company explained: “It should solve a real problem. This is why Lydia’s choices, with Sumeria, are motivated by common sense and its ambition to be universal: for everyone, for everything.”

Lydia’s brand announcement follows a decision by the company to split its digital banking app into two components. Originally launched in 2013 as a P2P payments app, Lydia’s solution scaled, adding more and more financial services features over the years. It was the launch of its Lydia Accounts offering convinced the company that a change was necessary to keep its early adopters – who relied heavily on the P2P service – onboard. The result was to offer the P2P services separately from Lydia’s digital banking proposition through the Lydia Accounts app. The original Lydia app will become Sumeria, with the new features mentioned above – such as stock trading, savings accounts and loans – to be ported to the new banking brand.

Headquartered in Paris, Lydia has raised more than $259 million in funding. The company’s investors include Accel and Echo Street Capital. In addition to the launch of Sumeria, Lydia is also seeking a credit institution license from the French Prudential Supervision and Resolution Authority.

Paris, France-based private wealth management startup RockFiraised €3 million in funding this week. The round was led by Varsity I and featured the participation of numerous business angels in technology and private management. The company plans to use the capital to grow its workforce by 3x by the end of 2024 so as to provide private banking and wealth management expertise to clients throughout France.

“Since the beginning of the year, we have seen strong client traction eager for a new model to manage their wealth,” RockFi Co-Founder and CEO Pierre Marin said. “With a market of €4.8 trillionin assets ahead of us and no tech leader yet in France and Europe, our ambition is very high for the coming years.”

RockFi’s model combines human expertise and technology to offer services including banking, wealth management, life insurance, and pension savings. The firm has a targetable clientele with assets of more than €100,000, representing six million households in France.

“Three months after our official launch this is an important step that anchors a strong momentum and allows us to further accelerate the construction of the new private management,” the company wrote on its LinkedIn page this week. “The ambition remains: to surround ourselves with the best talent and partners in each field and to deploy a tech ecosystem to unleash the potential of independent wealth managers at the service of their clients.”

Meet Finovate’s French Alums!

Over the years, Finovate has been proud to showcase a number of fintech innovators based in France. Here’s a look at some of French fintechs that have demoed their technology on the Finovate stage in recent years.

Aeropay raised $20 million in new funding for its pay-by-bank technology.

The round, which boosts Aeropay’s total funding to $25 million, was led by Group 11.

Aeropay also announced the launch of Aerosync, the company’s internally developed bank aggregator.

Chicago-based payments company Aeropayannounced today it has landed $20 million in new funding. The Series B round, which boosts the company’s total funds to $25 million, was led by venture capital firm Group 11 and saw participation from Chicago Ventures and Continental Investment Partners.

Aeropay was founded in 2017 to help businesses move money in a faster, less expensive way using Aerosync, the company’s internally developed pay-by-bank technology. Launching today, Aerosync is Aeropay’s bank aggregator that enables customizable integrations via open APIs.

“Payments in most verticals operate on archaic systems filled with excessive fees and risks,” said Aeropay Founder and CEO Daniel Muller. “We’ve built a bank-driven payments network that protects businesses against fraud, saves them money, and gives their customers an easy way to pay. Put simply, we are building the next-generation payments network.”

Aeropay will use the funds to expand into new markets, including financial services, wellness, utilities, QSR, and property management. The investment will also help fuel new product offerings, build on strategic partnerships, and explore new opportunities.

“For years, we’ve searched for a company advanced enough to solve the pains and inefficiencies of the card payment market, arguably the last bastion of the traditional financial services industry,” said Group 11 Founding Partner Dovi Frances. “Aeropay has tackled the most complex technological and compliance challenges, making them the most likely player to seize upon this massive addressable market.”

Pay-by-bank has seen rising popularity across the globe in the past few years, as open banking fuels new possibilities. The technology holds the promise of reducing transaction fees for retailers. End consumers, however, may remain skeptical of pay-by-bank’s security and user friendliness.

VantageScore launched its newest credit scoring model, the VantageScore 4plus.

The score combines consumer-permissioned open banking data with data from Experian, Equifax, or TransUnion to improve lenders’ underwriting efforts.

The new credit scoring model is available as a pilot for banks, fintechs, and government lenders.

Consumer credit score software company VantageScore unveiled VantageScore 4plus, its newest credit scoring model, today.

VantageScore 4plus leverages alternative data sourced through open banking that can be accessed via all major aggregator APIs. When consumers offer lenders access to their bank data, the lender can combine the data with traditional credit scoring information from Experian, Equifax, or TransUnion to make more informed underwriting decisions and potentially lend to more consumers who have thin credit files but demonstrate positive cash management.

“The use of consumer-permissioned bank account data is a huge step forward in creating a credit score that is more predictive and reflective of a consumer’s full financial profile, helping them build their credit and gain access to mainstream financial products,” said Credit Builders Alliance CEO Dara Duguay.

This new credit scoring model is available as a pilot for banks, fintechs, and government lenders. Because it uses the same 300 to 850 scoring range with aligned score-to-odds ratios as VantageScore 4.0, most lenders won’t need to adjust their credit or lending policies to use the new VantageScore 4plus credit score. And because the new score leverages real-time data, lenders will be able to view a consumer’s credit score adjustment within seconds, facilitating faster lending decisions.

The additional data from VantageScore 4plus not only helps lenders make informed decisions about new borrowers, but it also helps lenders identify existing borrowers whose habits have changed. The new score provides visibility into signs of financial distress months before the trouble is detected by traditional credit bureaus. which is critical in the current economic uncertainty.

“By harnessing the power of alternative open banking data, VantageScore 4plus is ushering in a new era of consumer credit scoring that is transformational for lenders,” said VantageScore President and CEO Silvio Tavares. “As the fastest growing credit scoring company in the U.S., with over 42% growth in 2023 and 27 billion credit scores used per year, lenders are recognizing the innovation and predictive power of VantageScore credit scores.”

The news comes shortly after Experian launchedCashflow Attributes, a tool also powered by open banking and consumer-permissioned data, that aims to offer lenders more data about underserved consumers.

Connecticut-based VantageScore was founded in 2006 as an independently managed joint venture of the U.S.’ three Nationwide Consumer Reporting Agencies (NCRAs) – Equifax, Experian and TransUnion. The company, which is committed to financial inclusion, saw the usage of its VantageScore increase by 42% in 2023, when it reported more than 27 billion credit scores. VantageScore helps 3,400+ institutions, including eight of the top 10 banks, to use the VantageScore credit score to underwrite credit cards, auto loans, personal loans, and mortgages.

Finovate’s David Penn interviewed Rikard Bandebo, VantageScore Executive Vice President and Chief Product Officer on the company’s approach to credit scoring in 2022.

With just a few days until FinovateSpring takes the stage at the Marriott Marquis in San Francisco, it is a good time to set your schedule in the event app. As usual, we have curated a lineup of keynote speakers who will be offering their expertise on some of the most pressing topics in fintech and banking.

Here’s a look at some of the keynote speakers taking the stage during the general session.

Brian Solis, Author at Mindshift: Ignite Change, Inspire Action, And Innovate For A Better Tomorrow

On Tuesday at 10:30 am, Solis’ keynote, The Cycle For Emerging Technologies: Which Will Really Matter To Financial Services Providers And Why? If You’re Waiting For Someone To Tell You What To Do, You’re On The Wrong Side Of Change will help financial services providers dig into the newest technologies and determine how to prioritize new, and rapidly approaching changes in banking and fintech.

Shirin Oreizy, Founder and CEO of NextStep

Oreizy’s keynote address is taking place on Tuesday at 12:45 pm. During her presentation, How Companies Can Leverage The Psychology Of Human Decision Making To Design And Scale Financial Products, Oreizy will consider how your consumers are really making their decisions, what motivates them, and how to design your UX to drive desired behavior.

Manas Chawla, CEO at London Politica

Chawla will take a look at the current geopolitical outlook in his keynote, The Global Economic & Geo-Political Outlook – What Are The Five Things You Need To Know? He takes the stage at 1 pm on Tuesday and will be looking at topics such as the interest rate environment, bank failures, wars, and political tensions.

Karl Alomar, Managing Partner at M13

In his quick fire keynote session at 3:35 pm on Tuesday titled, Major Banks Are Making Serious Plays In The Crypto & Digital Currencies Space – Why?, Alomar will consider the shortcomings of traditional currencies and will take a look at the rise of digital currencies, including CBDCs. He will also address the impact digital currencies will have on banks and how they should prioritize discussions.

Gary Rudman, Founder and CEO of GTR Consulting

Rudman will take the stage at 11:40 am on Wednesday to offer his keynote, ALT, SHIFT & CTRL: The 3 Keystrokes That Define the Gen Z Worldview – What Banks & Fintechs Need to Know. During his presentation, Rudman will describe how Gen Z differs from their predecessors and will discuss how banks can connect with the new generation.

Sam Kilmer, Managing Director, Fintech Advisory at Cornerstone Advisors

Kilmer’s quick fire keynote, which takes place at 9 am on Thursday, is titled, Focusing On The Three Pillars Of Banking: Deposits, Loans, and Money Movement – How Can Banks Innovate To Drive Revenue In A Challenging Economic Environment? The presentation will cover what Kilmer has determined are the three pillars of banking: deposits, loans, and money movement operations. Kilmer will also consider KYC, fraud detection, and authentication, and will discuss what banks should prioritize to add value.

James Robert Lay, Author of Banking on Digital Growth

In his keynote, Banking On Change – The Exponential Growth Journey, Lay considers how firms can maximize their digital growth using a future mindset. He also looks at how legacy systems limit digital growth potential. Lay’s presentation begins at 9:50 am on Thursday.

Sarah Welch, Managing Director at Curinos

In her quick fire keynote, How AI Is A Force Multiplier On Customer Loyalty, Welch will offer her take on AI in financial services and will consider how organizations can use the enabling technology to improve customer service and ultimately improve loyalty. Welch’s presentation begins at 10:05 am on Thursday.

Sam Maule, Head of Business Development at Moov

Maule’s presentation, The Next Chapter For Embedded Finance & The Digitisation Of Commerce. In An Age Of Re-Bundling Financial Product Experiences, How And Where Should Banks Play To Win? Why Retailers & Banks Need To Be Actively Partnering On Embedded Finance, takes place at 11:25 am on Thursday. Maule will consider how embedded finance is transforming the industry and will offer advice on where to steer.

Digital identity verification innovator Socure announced a partnership with identity-secured transactions company Proof.

The partnership will combine Proof’s Defend solution with Socure’s Sigma Fraud suite to help companies fight fraud and forgery in authorizations, agreements, contracts, and forms.

Founded in 2012, Socure made its Finovate debut the following year at FinovateFall in New York.

A new partnership between digital identity verification innovator Socure and identity-secured transactions company Proof will bring new tools to the fight against fraud and forgery in authorizations, contracts, and forms.

“With the explosion of new fraud vectors, our mission at Socure remains steadfast: use AI to deliver the most accurate anti-fraud and identity verification solutions in the industry,” Socure Founder and CEO Johnny Ayers said. “Partnering with Proof allows us to uniquely ensure identity-assured transactions for contracts, authorizations, forms, and high-risk financial events across various sectors.”

While there is widespread understanding about threats like money laundering that cost businesses $18 billion every year, the challenge from document fraud is significantly greater. A 2021 report from FINCEN revealed that false records and forgery are responsible for more than $45 billion in fraud activity annually. Fraudsters also have become more effective at leveraging AI to deploy deepfakes, synthetic identities, and – in the case of document fraud – falsified records.

The partnership will blend the strengths of Proof’s Defend solution with Socure’s Sigma Fraud suite. Defend leverages 100+ behavioral, fraud risk signals to detect fraud in online customer interactions. Businesses get a risk score for every transaction that highlights any fraud issues behind the authorization, signature, notarization, or identity verification.

Sigma Fraud analyzes historic behavioral patterns across channels to spot anomalies that may indicate fraudulent activity at the identity level. The suite also is backed by consortium data from the Socure Risk Insights Network, which draws from nearly 2,400 customers from the country’s largest banks, fintechs, payment platforms, and payroll providers.

“Adding Socure’s digital identity verification capabilities to Defend, our fraud detection and prevention product, allows customers to secure transactions at every stage, quickly and accurately,” Proof CEO Pat Kinsel said. “We can’t think of a better partner and are excited to introduce Socure to Defend clients.”

Founded in 2012, Socure made its Finovate debut at FinovateFall a year later. Most recently demoing its technology on the Finovate stage in 2017, Socure has since grown into a leader in digital identity verification with more than 2,300 customers. Last month, the company unveiled its new global watchlist screening and monitoring tool. The solution gives financial institutions the ability to screen, monitor, and assess new and existing customers against the Office of Foreign Assets Control (OFAC) sanction lists and politically exposed persons (PEP) databases, adverse media, and custom watchlists.

Socure began the year announcing a pair of new partnerships. In January, the company reported that auto finance company Exeter Finance would deploy the Socure ID+ platform to onboard new customers. In February, Socure teamed up with fellow Finovate alum Trustly to offer a Pay-by-Bank solution with streamlined onboarding.