For the first time, FinovateFall 2024 (September 9-11) will showcase innovations in wealthtech. From AI-powered analysis and decision-making to embedded technologies that are democratizing the world of investing, now is a great time for asset managers, RIAs, and others looking to leverage technology to boost their wealth management businesses.

“Finovate spotlights cutting-edge technology and finserv themes dominating industry news,” Finovate VP and Demo Director Heather Stowell said. “The Great Wealth Transfer has been at the forefront of conversations, and we’re excited to showcase several startups innovating within wealth management and investing.”

Indeed. In its annual survey of wealth managers, Acuity Knowledge Partners noted that the intergenerational wealth transfer was a major opportunity and challenge facing asset managers. Additionally, survey respondents also expressed a desire for comprehensive solutions for estate, tax, and retirement planning. Growing revenues via customized research offerings was also mentioned as a goal, along with managing costs while embracing digitalization and new, enabling technologies like AI.

Below are six companies offering wealthtech solutions this year at FinovateFall 2024 in New York. For more on our wealthtech offering at FinovateFall next month, check out Wealthtech at FinovateFall: Client Centricity and the Rise of Alternative Assets.

Eko Investments

Offers investments to all clients starting from $10, and not just the top 1% via a financial advisor. Headquartered in New York. Founded in 2021. LinkedIn.

GPTadvisor

Empowers financial institutions with AI tools for optimized decision-making, streamlined workflows, and improved client advisory, driving business growth and operational excellence. Headquartered in Madrid, Spain. Founded in 2023. LinkedIn.

illuminote

Enables financial institutions and advisors to authenticate registered client legal estate records with confidence, providing access to authenticated data without expensive tech integrations. Headquartered in Santa Rosa, California. Founded in 2022. LinkedIn.

QuAIL Technologies

Automates processes and increases productivity so organizations can spend less time managing and more time growing. Headquartered in Pittsburgh, Pennsylvania. Founded in 2022. LinkedIn.

TIFIN AG

Uses AI and ML to deliver actionable insights, helping financial advisors make data-driven decisions that boost client acquisition, expansion, and retention, achieving organic growth. Headquartered in Charlotte, N.C. Founded in 2023. LinkedIn.

TradingValley

Empowers companies that adopt its AI investing model that reduces the investing research time for both individual and institutional investors. Headquartered in Taiwan. Founded in 2015. LinkedIn.

Are you an innovative fintech with new technology that’s ready for prime time? Join us in New York next month for FinovateFall and take advantage of the opportunity to showcase your solution before an audience of 2,000+ decision-makers.

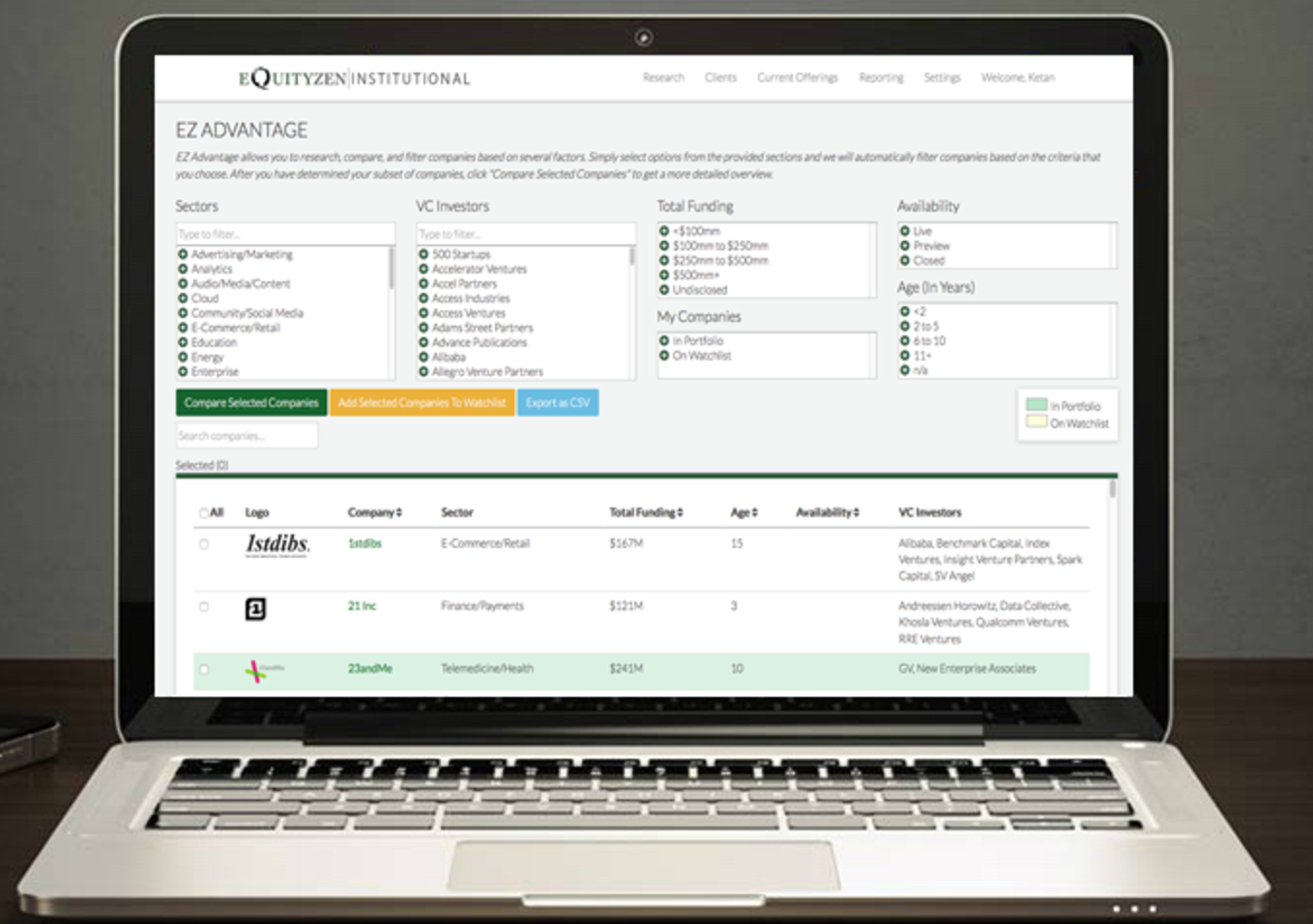

EquityZen’s EZ Institutional lets advisors give clients access to a diverse asset class

EquityZen’s EZ Institutional lets advisors give clients access to a diverse asset class

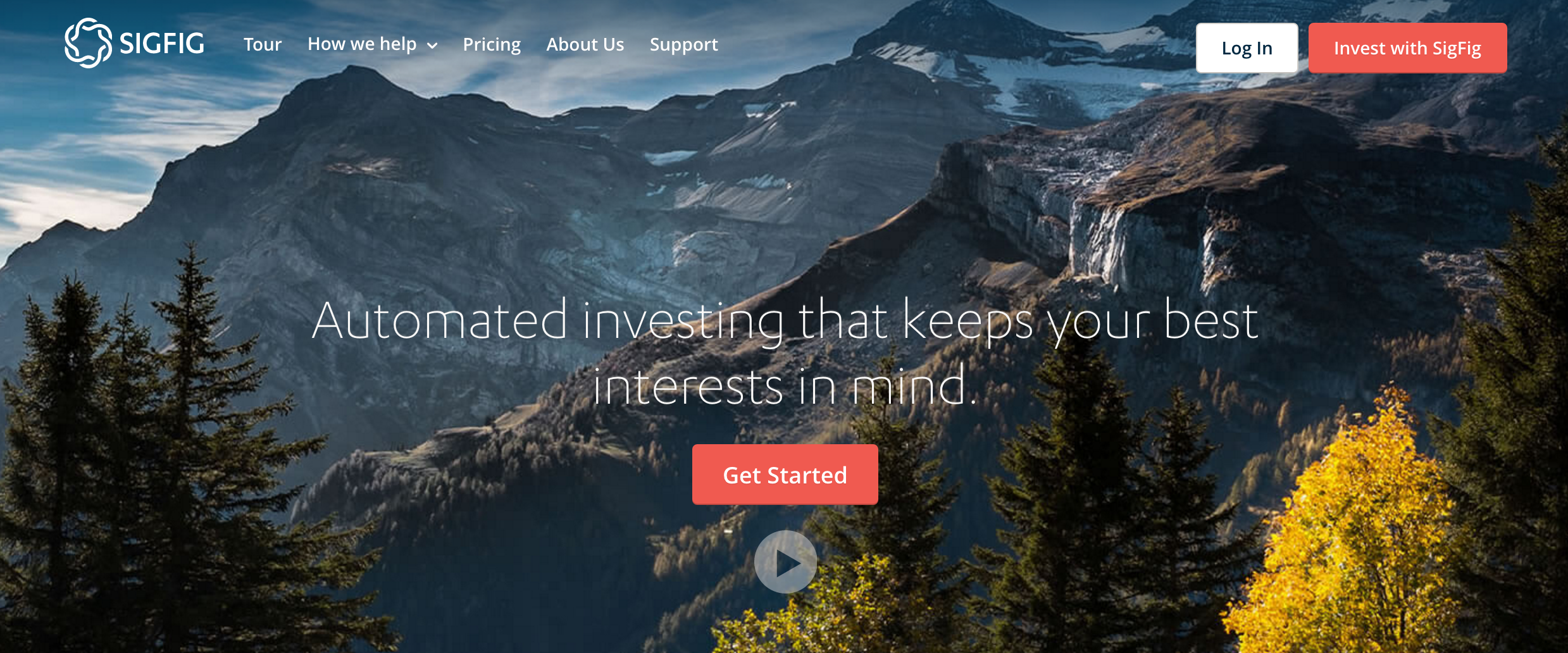

SigFig has partnered with multiple banks, including Wells Fargo, Pershing, and Citizens Bank

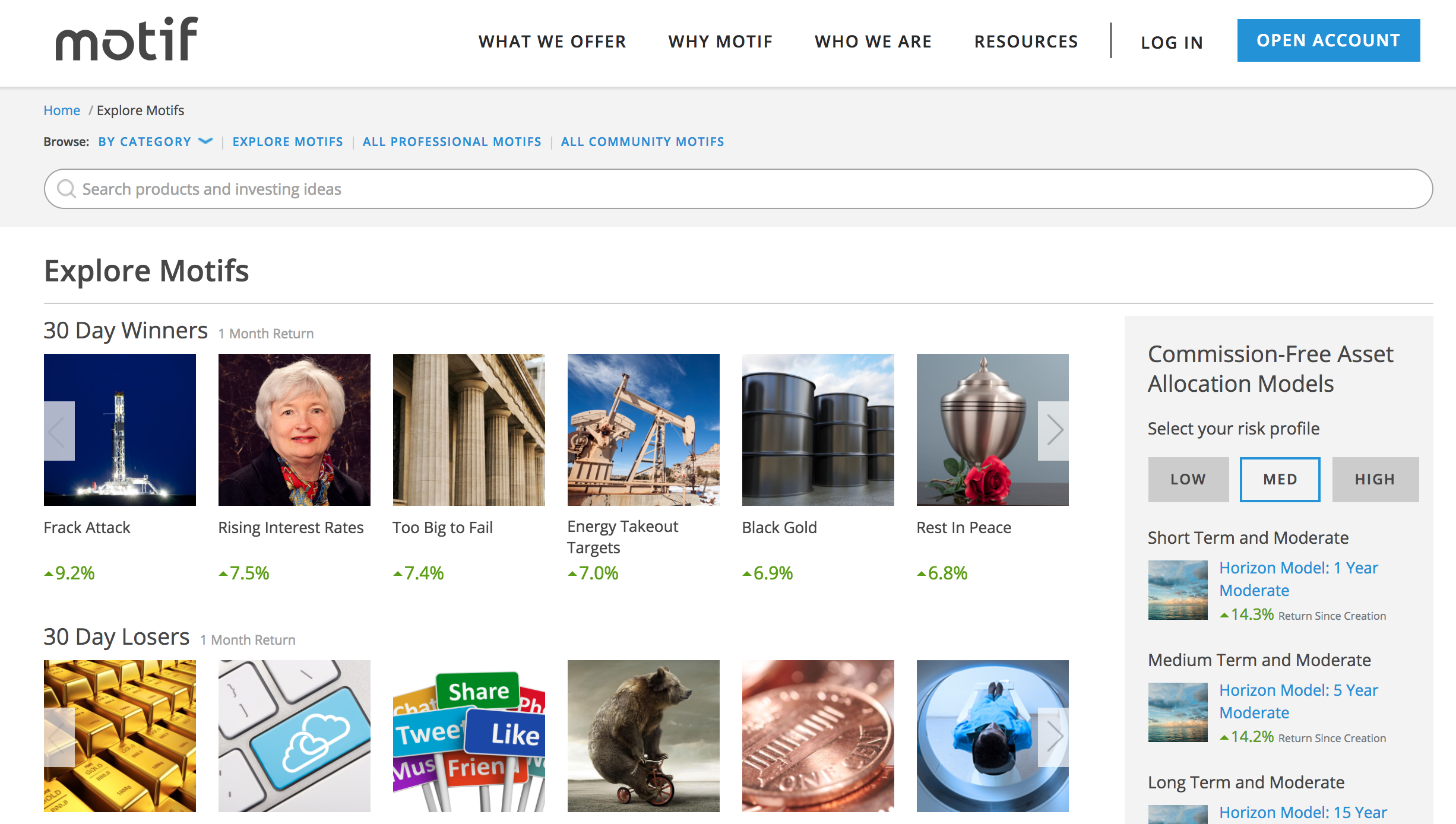

SigFig has partnered with multiple banks, including Wells Fargo, Pershing, and Citizens Bank With Motif, uses invest in grouped stocks and ETFs that revolve around a common theme

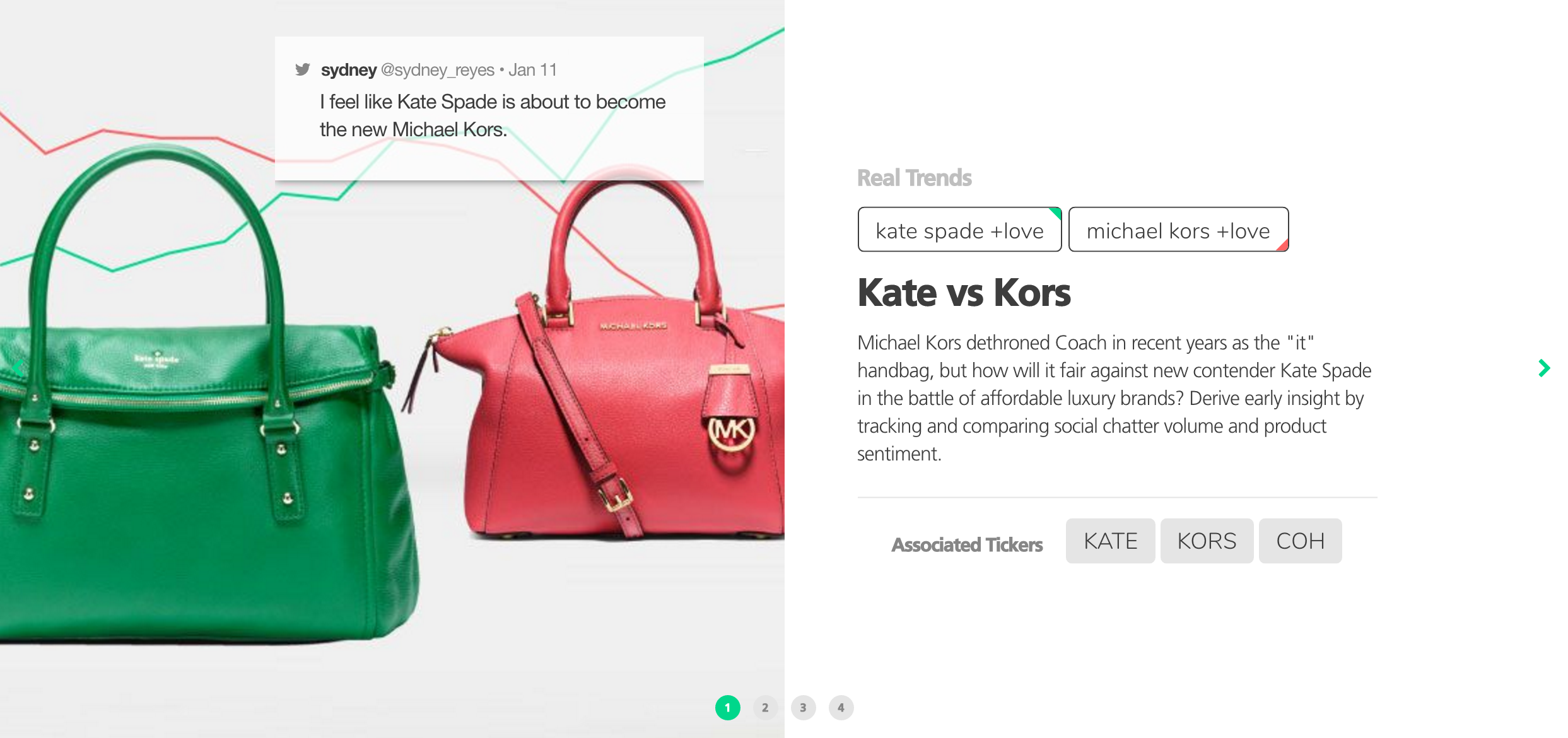

With Motif, uses invest in grouped stocks and ETFs that revolve around a common theme TickerTags helps users discover trends even before they become news

TickerTags helps users discover trends even before they become news