This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Paystand is acquiring Teampay. Financial terms of the agreement were not disclosed.

Following the acquisition, Paystand will serve more than one million business customers.

Teampay will continue to serve its existing customers under the same brand, and things will be business as usual “in the near term.”

Cloud-based billing and payment platform Paystandannounced this week it has agreed to acquire expense management platform Teampay. Financial terms of the agreement were not disclosed.

The strategic move marks the California-based company’s second acquisition. Paystand purchased procurement platform Yaydoo in 2022. Now, the company services more than one million companies.

Teampay was founded in 2016 to offer spend management, accounts payable automation, purchasing assistant, spend approval tools, accounting automation, and more to help small-to-mid-market businesses and enterprises automate their spending without sacrificing control.

Paystand, which leverages the blockchain and cloud technology to digitize and automate businesses’ cash lifecycle, will use Teampay to scale its services. “With the fusion of Paystand and Teampay we significantly expanded our network, which now touches over one million businesses,” Paystand said in a blog post announcement.

Logistically, Teampay will continue to serve its existing customers under the same brand, and things will be business as usual “in the near term.” The companies did not specify whether Paystand planned to dissolve the Teampay brand and bring the customers under its own platform.

Paystand was founded in 2013 to help businesses digitize receivables, automate processing, reduce time-to-cash, eliminate transaction fees, and enable new revenue. In addition to its B2B payments and billing capabilities, the company also helps businesses leverage the blockchain to securely record their payment history by certifying and notarizing payments on the blockchain. Paystand has raised a total of $98 million. Jeremy Almond is Co-Founder and CEO.

In the U.S., the tax deadline kicks off the week, but don’t let that get you down! Sit back, relax, and catch up on some of the latest fintech news headlines. Check back for real-time updates on how the fintech landscape evolves this week.

To celebrate National Hispanic Heritage Month, we wanted to recognize some of the contributions Hispanic entrepreneurs have made in the fintech industry. From the start, Hispanic professionals have played a pivotal role in shaping fintech by using their creativity and unique perspective to build and improve solutions that truly make a difference for both retail and commercial users.

Below is a selection of Hispanic-founded fintech companies that continue to make a transformative impact in the worlds of banking and fintech. Join us in celebrating diversity, inclusion, and the achievements from these individuals during this month of recognition and reflection. Please note that this is simply a conversation starter and is not an all-inclusive list of Hispanic-founded fintechs.

Securitize

Securitize enables digital securities, which are easier to own, simpler to manage, and faster to trade. Founders: Carlos Domingo, Jamie H. Finn, Shay Finkelstein, and Tal Elyashiv

Payjoy

PayJoy is a consumer financing company that allows consumers to buy a smartphone on credit and pay it off in installments. Founders: Doug Ricket, Gib Lopez, Mark Heynen, and Tom Ricket

Finix

Finix develops a payment processing platform for businesses. Founders: Richie Serna and Sean Donovan

Petal

Petal offers three Visa credit card products for underserved consumers. Founders: Andrew Endicott, David Ehrich, Jack Arenas, and Jason Rosen

Flywire

Flywire is a global payments enablement and software company that simplifies complex payments for its clients and their customers. Founder: Iker Marcaide

Octane

Octane offers access to instant financing to fuel their customers lifestyles. Founders: Andre Gregori, Jason Guss, Mark Davidson, Mark Garro, and Michael Fanfant

Origin

Origin is a financial planning platform that manages compensation, benefits, and personal finances for employees. Founders: João de Paula and Matt Watson

Oportun

Oportun is a digital banking platform that puts its 1.9 million members’ financial goals within reach. Founders: Gabriel Manjarrez and James Gutierrez

Brex

Brex is a global spend platform with corporate cards, expense management, reimbursements, and billpay. Founders: Henrique Dubugras and Pedro Franceschi

Camino Financial

Camino Financial is an online finance company that offers business loans and wealth-building solutions to help small businesses grow. Founders: Kenneth Salas and Sean Salas

Ontop

Ontop offers streamlined payroll, onboarding, and smooth payments for international teams. Founders: Julian Torres and Santiago Aparicio

Papaya

Papaya develops technology designed to simplify bill payment for consumers. Founders: Jason Meltzer and Patrick Kann

Snowball Wealth

Snowball Wealth offers a mobile app designed to help users tackle debt and build generational wealth. Founders: Pamela Martinez, Pearl Chan, and Tanya Menendez

Paystand

Paystand is a cloud-based billing and payment platform for B2B companies. Founders: Jeremy Almond and Scott Campbell

Listo

Listo offers insurance and loans via retail and mobile experiences. Founders: Alan Chiu and Sam Ulloa

Ripio

Ripio is a bitcoin and digital payments company that provides electronic payment solutions for businesses in Latin America. Founders: Luciana Gruszeczka, Mugur Marculescu, and Sebastian Serrano

InvestCloud

InvestCloud is a global company specializing in digital platforms that enable the development of financial solutions. Founders: Colin Close, John Wise, Julian Bowden, Michael A. Smith, Vincent Sos, and Yaela Shamberg

Novel Capital

Novel Capital provides revenue-based financing to B2B companies. Founders: Carlos Antequera and Keith Harrington

Flow

Flow offers an open architecture that connects investment managers with their limited partners and service providers. Founders: Adrian Ortiz, Brendan Marshall

Milo

Milo is reimagining the way crypto and global consumers access credit and financial solutions. Founder: Josip Rupena

Traive

Traive is a lending platform that connects lenders to farmers to provide financial products and services for the agricultural supply chain. Founders: Aline Pezente and Fabricio Pezente

Finally

Finally helps small and medium-sized businesses automate their accounting and finances. Founders: Edwin Mejia, Felix Rodriguez, and Glennys Rodriguez

Alvva

Alvva offers credit-building loans to pay for immigration expenses. Founders: Jorge Gonzalez and Sergio Torres

Portabl

Portabl offers identity-powered user experiences via a single API. Founder: Nate Soffio

Onyx Private

Onyx offers a modern private bank for the new generation. Founders: Douglas Lopes, Tiago Passinato, and Victor Santos

SMBX

SMBX is a funding portal and public marketplace for issuing and buying U.S. small business bonds. Founders: Benjamin James Lozano, Bhavish Balhotra, Gabrielle Katsnelson, and Jackie Chan

Zoe Financial

Zoe Financial helps its clients find and hire their ideal financial advisor. Founder: Andres Garcia Amaya

OKY

OKY is building technologies that help immigrants to improve their lives by connecting families and sending value home efficiently. Founders: Alejandro Miron, Estuardo Figueroa, Santiago Rossi, and Victor Unda

Caplight

Caplight is a platform that enables institutional investors to buy and sell derivatives of private equity. Founders: Javier Avalos, Justin Moore

Aeropay

Aeropay enables businesses to accept compliant, digital payments. Founder: Daniel Muller

Flourish FI

Flourish FI is a financial wellness and engagement platform for financial institutions. Founders: Jessica Eting, Pedro Moura

Capchase

Capchase provides financial solutions to startups by allowing access to funds as they grow. Founders: Ignacio Moreno Pubul, Luis Basagoiti Marqués, Miguel Fernandez, and Przemek Gotfryd

Chargezoom

Chargezoom is a B2B integrated payments platform. Founders: Matt Dubois and Miguel Avellan

Chipper

Chipper is a student loan app that helps users lower payments, qualify for forgiveness, and chip away debt faster. Founder: Tony Aguilar

Ease

Ease is a corporate card and practice operations software for private practices. Founders: Mario Amaro and Miles Montes

Active in 15 countries in Latin America, payments infrastructure provider Geopagos has secured an investment of $35 million. The equity funding round was led by Riverwood Capital and featured participation from Endeavor Catalyst. The sum represents the company’s first institutional financing and will be used to fuel the development of new embedded payments solutions and help the firm expand throughout Latin America.

Geopagos provides financial institutions, fintechs, retailers, software companies and other organizations with end-to-end digital solutions to help them launch or grow their payment acceptance businesses in the area. These solutions include terminals that enable mobile phones to operate as point of sale devices as well as technology that turns websites into e-commerce platforms.

With clients including Santander, BBVA, Banco Estado de Chile, and Finovate alum Fiserv, Geopagos processes more than 150 million transactions and more than $5 billion in volume a year. The Buenos Aires-based company was founded in 2013 by Sebastián Núñez Castro, Julián Lisenberg, Fernando Tauscher, Raúl Oyarzun and Damián Harburguer.

“Latin America is a market with very low card penetration and Geopagos is well positioned as a software enabler and infrastructure provider to boost card acceptance and digital payments across the region,” Riverwood Capital co-founder and managing partner Francisco Álvarez-Demalde said.

Speaking of payments in Latin America, blockchain-enabled accounts receivable and B2B payments company PayStand has acquired Yaydoo, an accounts payable, cash flow management, and liquidity solution provider based in Mexico. Yaydoo is one of the fastest-growing startups in Mexico, with more than 150 employees working in more than six different countries. Founded in 2017 and operating throughout Latin America Yaydoo raised $20.4 million in Series A funding last year and this year was named a “Súper Empresa 2022” and a “Súper Empresas para Mujeres 2022” by Expansión Top Companies México.

“Together, PayStand and Yaydoo will redefine the boundaries of B2B fintech across the continent,” PayStand CEO Jeremy Almond said. “The combined company will be one of the first global B2B blockchain platforms at a significant scale. The resulting company will have processed over $5 billion in payments, added 300 additional employees, and built a network of over 500,000 connected businesses, the largest of any commercial B2B blockchain in the world.”

Founded in 2013, PayStand made its Finovate debut at our developers conference, FinDEVr Silicon Valley, one year later in 2014. The company leverages blockchain and cloud technology to digitize receivables, automate processing, lower time-to-cash, remove transaction fees, and drive new revenue. A member of the 2021 CB Insights Fintech 250 and named to the Inc. 5000 for a second year in a row in 2021, PayStand has secured $86 million in funding, most recently raising $50 million in a Series C investment led by NewView Capital and featuring participation from SoftBank’s SB Opportunity Fund and King River Capital.

Here is our look at fintech innovation around the world.

In a round led by new investor NewView Capital, blockchain-based commercial payments innovator Paystand has raised $50 million in funding. The company leverages the cloud and the Ethereum blockchain to power its Paystand Bank Network, a no-fee, digital B2B payment system used by more than 250,000 companies to make payments.

“With this new funding, Paystand is uniquely positioned to bring the benefits of blockchain to commercial payments so businesses can be more agile and competitive in the post-pandemic landscape,” Paystand CEO Jeremy Almond said. “Our vision is to create an open financial infrastructure that delivers a self-driving money experience for businesses and provides radically better economics for the industry itself.”

The investment takes Paystand’s total capital to more than $78 million. Also participating in this week’s financing were SoftBank’s Opportunity Fund, King River Capital, Industrious Ventures, and Transform Capital. As part of the investment, NewView Capital’s Jazmin Medina will join Paystand’s board of directors.

Paystand’s innovation is to automate the entire cash lifecycle to enable businesses to enhance the overall customer experience with seamless, B2B payment options. The company’s technology helps businesses accelerate time-to-cash, lower DSO (daily sales outstanding) by 60% or more, as well as reduce fraud and chargebacks thanks to real-time fund verification. And instead of charging businesses a percentage on each transaction, Paystand’s business model relies on subscriptions which the company says allows businesses to scale their payments operations without having to worry about dramatically increased fee-per-transaction expenses.

An alum of our developers conference, FinDEVr, Paystand was among the many fintechs who was able to turn the crisis of the global pandemic into an opportunity to support businesses that suddenly found themselves sprinting toward digital transformation. In a blog post discussing the challenges facing businesses during this time, Almond noted that while many companies had already migrated to the cloud for their “systems of record” (i.e., CRM, ERP, etc.), the “critical component” and “last mile” of digital transformation – revenue – was left underaddressed.

“Finance teams found themselves forced to return to the office at the height of COVID-19 outbreaks just to pick up checks and deal with cash flow,” Almond wrote, “something that clearly exposed the backwards nature of the legacy payment system.”

In May, Paystand inked a partnership with cloud business management solution provider Sage to enable a “Venmo for Businesses” like service via Paystand’s B2B payment network. The following month, the Scotts Valley, California-based fintech launched its Smart Lockbox, a digital-first alternative to traditional lockbox services. Smart Lockbox enhances the ability of businesses to transition away from paper-based payments to faster, less expensive, digital options, and makes migration easy with a seamless, one-click process.

“Smart Lockbox is the key tool that helps companies seamlessly bring their mission-critical revenue into the digital age,” Almond said when the solution was announced. “In a post-pandemic world, everything looks very different. COVID supercharged the push for digital transformation across the board for businesses, and there’s no question that this shift is here to stay. Now, with Smart Lockbox, finance teams can turn their biggest headaches into a newfound source of power.”

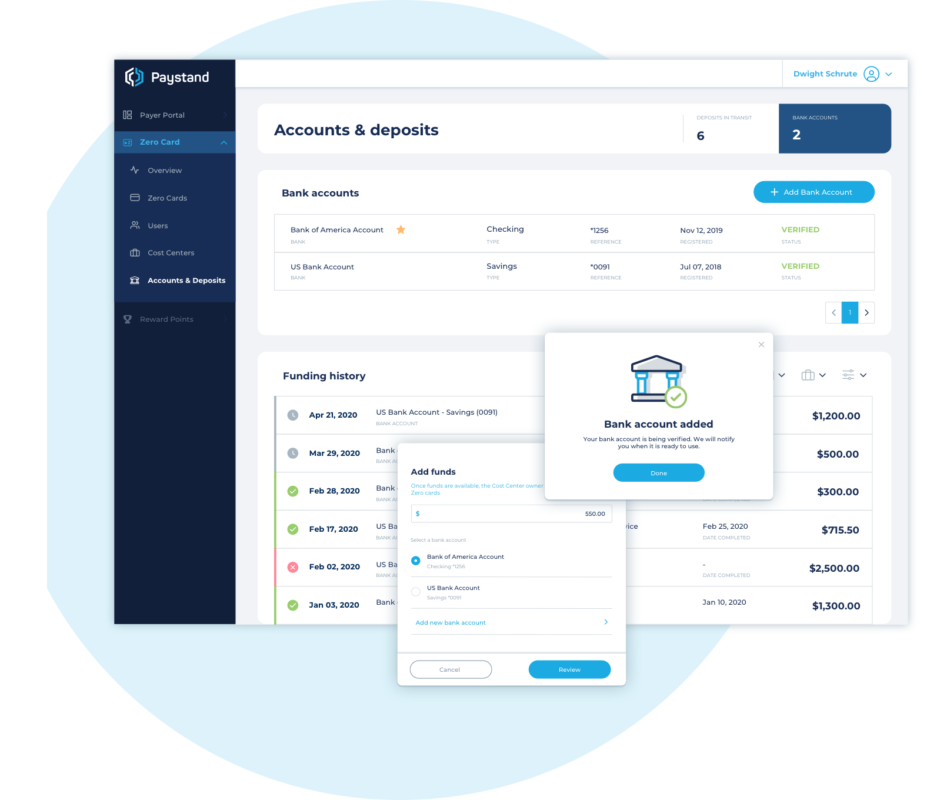

Paystand’sZero Card, launched today, offers businesses a touchless, prepaid corporate expense ePayable solution that leverages Paystand’s zero-fee payment network to eliminate the cost of transaction fees.

Geared to help mid-market businesses in particular, which often require a high degree of flexibility and control over their budgets, the Zero Card streamlines expense management operations such as invoice processing, expense reporting, and payment execution. The prepaid virtual expense card also enables businesses to manage, track, and control spending in real-time. The offering includes fraud prevention controls and the ability to capture and add critical remittance data to transactions to make expense reporting and reconciliation easier.

“The Paystand Zero Card combines the consumer-like experience of peer-to-peer payments with the speed and security of Paystand’s no-fee payment network,” Paystand CEO Jeremy Almond said. “We completely re-engineered the corporate card so businesses can move away from reactive spend management tactics to a place where they have visibility of spend before it happens.”

One of the aspects of the Zero Card the company is touting is the way it brings a common payment infrastructure to accounts payable and accounts receivable operations. In its statement, the company referred to this disconnect as “one of the biggest challenges in B2B payments today,” which pits payers and receivers against one another as “technology and process improvements for one group often lead to inefficiency and friction for the other.”

In contrast, the Zero Card is designed for both accounts payable and accounts receivable, natively connecting both AP and AR to keep costs low, ensure swift and secure payments, and effectively bridge what the company calls “the payables gap for B2B payments”

Challenges like the payables gap, according to Paystand VP of Marketing Mark Fisher, are why he believes B2B payments have “a long way to go before it achieves the ease and speed of consumer payments.” Fisher credited the Zero Card for helping B2B payments catch up. “When money moves over our network,” he said, “it’s instant, automated, and comes at no cost. That’s good for businesses and that’s good for the economy overall.”

Founded in 2013 and headquartered in San Francisco, California, Paystand secured $20 million in funding in February in a round led by DNX Ventures. Mitch Kitamura, Managing Director at the firm put the company’s latest offering in the broader context of the “cashless transformation” led by fintech innovators like Paystand. In a statement, he referred to the Zero Card as “a critical step … in driving more seamless interaction between businesses to help realize the true economic value of digital infrastructure.”

Zenus Bank to deploy onboarding authentication technology from Fortress Identity.

Paystand to provide an end-to-end payments platform for customers of Japanese payment card issuer and acquirer, JCB.

Blackhawk Networkintroduces new SVP of Global Commerce, Brett Narlinger.

Ovum highlightsQuadient and its leadership role in providing customer journey mapping in its report, Customer Journey Management’s Path to Optimization.

Forbes Senior Contributor Ron Shevlin givesTransferWise an “Honorable Mention” among the Winners in his review of the Winners and Losers in Fintech this year.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

SumUppartners with donation software company to help charities to go contactless for Christmas.

TransferWisepartners with Visa to enable real-time transfers to debit cards.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Paystand CEO Jeremy Almond knows a thing or two about business payments. Since co-founding the company in 2013, Almond has implemented numerous improvements to the company’s payments engine, taking full advantage of the blockchain.

Among Paystand’s most recent debuts are the company’s 2018 launch of a blockchain that ensures payment, storing an immutable record of every transaction the company processes. Earlier this year, Paystand launched the Assurety-as-a-Service API that leverages the company’s blockchain to prevent fraud. Paystand also unveiledAutomated Receivables, atool that leverages the blockchain to automate invoice collection.

Almond is a 15-year veteran of the tech industry, having served as a serial entrepreneur, startup advisor, and occasional investor. Almond helped co-found Paystand in 2013 and has since been at the helm of the company as CEO. We caught up with him in an interview earlier this month.

Finovate: What is Paystand and how does it differ from other online payment gateways?

Jeremy Almond: Paystand is a commercial payments platform that automates the entire cash cycle, from invoicing to reconciliation, to make payments an easy, effortless experience.

Today’s financial system is plagued by costly fees, inefficiencies, and paper-driven processes. We believe this broken system is holding businesses back, so we created Paystand to eliminate fees and build the payment framework for the digital era.

Much the same way that Netflix came along and completely re-thought consumption of media or how Tesla has come to market with not just a new vehicle but a business model and mission focused on energy independence, Paystand differentiates itself with its Payments-as-a-Service model. The outdated, inefficient, fee-based approach to commercial payments and money movement no longer makes sense. Instead of taking a cut from every customer sale, our customers pay a flat monthly rate to use our payment software. Essentially, it is unlimited “consumption” for payments with predictable costs. This means that as our customers’ businesses grow, their profits increase instead of their fees.

We’ve also built the most complete digital payment network available to businesses. Using the Paystand Bank Network, customers can move money electronically without paying any fees. It’s the industry’s first zero-cost rail, and the easiest way for businesses to get paid today. It’s also the only blockchain-based payments infrastructure that has been tested at scale with millions of transactions and enterprise volume.

Finovate: You’re a startup investor yourself. How does that influence how you’ve built Paystand?

Almond: Most venture-backed startups fail, especially the high-potential ones. Everyone is hungry to find the next Uber or Facebook, so it’s easier than ever to start a company and get funded. But building a startup that lasts isn’t easy. I think many founders underestimate that and end up spending their time and resources chasing quick exits and unicorn status.

That’s why we do things completely different at Paystand. We’re focused on building a sustainable business that solves real, meaningful problems. There’s a certain business pacing you have to keep up to attract the right investors and gather momentum around your vision. So driving that kind of sustainable growth is our top priority.

Over time, I believe we’re going to see a shift away from companies constantly raising equity to this sustainable growth approach. If you look at the market today, especially after Zoom’s IPO, there’s a real appetite for businesses with a clear path to profitability.

In many ways, being an investor has been an advantage to building Paystand.

Finovate: Tell us about Paystand’s new Fintech Advisory Council launched earlier this year. What was the impetus for this?

Almond: The need for the Fintech Advisory Council really came from our growth. We’ve nearly tripled our revenue this year, which is more than an 8x increase since raising our Series A round. So we built the advisory council to help us scale our product innovation and better meet this demand.

We didn’t make the appointments lightly. These are people who are literally the top of the top for financial services and B2B fintech. CheckFree founder Pete Kight, for example, made it possible to pay bills online with your bank account. Other advisors include the former president of Bill.com and the former president of PayPal. Having these pioneers on our side, guiding us, is going to be a massive value ad as we build the next chapter in commercial finance.

This is a huge mission we’re talking about — rebooting the financial system. Our Fintech Advisory Council is going to help us make that happen.

Finovate: Paystand recently surpassed 100,000 businesses using its platform. What new features does Paystand have in the works to garner its next 100,000 users?

Almond: Although we recently surpassed 100,000 businesses using the platform, we know we’re still just scratching the surface. There are over 6 million B2B companies in the United States alone. And 18 trillion dollars still moves between businesses via paper check every year in this country. That’s a staggering figure. Those businesses need a modern payment solution that doesn’t penalize growth via more and higher fees. So, we’re focused on continuing to deliver the best payment solutions to that market with our core payment platform. We plan on deepening our integrations and relationships with core systems of record like NetSuite to further provide seamless automation of accounts receivable workflows.

At the same time, we’re continuing to build innovative products to enable automation and reduce friction for the entire downstream network involved in payments. We recently launched Autopilot, our receivables automation product that helps companies reduce DSO, decrease late payments, and improve the customer payment experience. And our newly launched Payment Portal gives all of their downstream payers an intuitive interface to view their payments, payer history, and access our payment platform.

Every day, more businesses are making the shift to a more open, inclusive commercial payments infrastructure and are rejecting the outdated, fee-based model that no longer makes sense. We’re proud to help them on their journey.

Paystandsurpasses 100,000 businesses on its network.

Swaper celebrates its third birthday.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Business payments platform PayStand is launching what it’s calling Assurety-as-a-Service, which is exactly what it sounds like. The new API allows businesses with no prior blockchain experience to verify any event, action, or identity in real-time by creating a record that is notarized on the blockchain.

To picture what this looks like, imagine having a frictionless notary public that can scale; notarizing an unlimited number of documents. In a blog post detailing the API, PayStand illustrates a multitude of use cases across a variety of industries. In the insurance industry, for example, businesses can track the exchange of high-value assets and use an automated collections process to settle a claim more efficiently. And businesses in the real estate vertical can record, track, and transfer land titles, property deeds, and liens, and ensure all documents are accurate and verifiable.

The solution levels the blockchain playing field by not requiring businesses to have any prior experience with the enabling technology. “Assurety-as-a-Service lets businesses skip the steep learning curve and start using blockchain right now,” said PayStand CEO Jeremy Almond. “Any developer can use our API and spin up their own blockchain app in minutes,” added Omar Baqueiro, Director of Product and Engineering.

The Assurety-as-a-Service API helps businesses deploy applications that prevent fraud by leveraging PayStand’s hybrid blockchain to document proof-of-action without allowing anyone to edit the record. The tool offers the accountability of a public blockchain while providing data privacy of a private blockchain. As Baqueiro phrased it, Assurety-as-a-Service “combin[es] the advantages of a trustless, decentralized, immutable public chain with the privacy and security expected of enterprise-level solutions.”

Today’s development comes after the company’s 2018 launch of a blockchain that ensures payment, adding security to the PayStand Bank Network. On that blockchain is stored an immutable record of every transaction the company processes.

PayStand showcased at our developers conference, FinDEVr Silicon Valley 2014. Earlier this year the company launched a service that uses the blockchain to automate invoice collection. Businesses can integrate the tool, Automated Receivables, into their existing customer payments infrastructure.

PayStandLeverages the Blockchain to Document Proof-of-Action.

DriveWealthPowers Commission-Free Trading for Revolut Cardholders.

Around the web

Columbia Bank to leveragenCino’s Bank Operating System.

Fast Company highlightsLighter Capital as a competitor to Clearbanc.

Ezbobwins the Best Fintech Partnership category for its Smart Onboarding Engine in this year’s Banker’s Tech Projects Awards.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.