This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

FinovateSpring is just over a month away, on May 23 through May 25, and we’re already excited to watch the stage fill with fresh fintech demos and discussions about the hottest industry topics.

Just as fintech is a constantly changing industry, so are the conversations, advice, and relevant themes. So when we hit the networking floor next month in San Francisco, here are the top 10 topics we can’t wait to talk about with everyone:

Metaverse When it comes to the metaverse and Web 3, it seems like you’re either in or you’re out. While a handful of banks have already jumped in with two feet by purchasing real estate in the metaverse, others are dismissing it as a passing fad.

ESG ESG discussions are happening around the globe, and formal ESG reporting strategies are on the verge of becoming more than just nice to have. With proposed regulation in the U.S. and beyond, now is the time to begin paying attention to this space.

Generative AI The topic of generative AI transcends Open AI’s ChatGPT. While organizations are leveraging the technology to save costs, it still bears risk if used improperly. If you’re not a first-mover in this space, however, you certainly don’t want to be the last.

Partnerships Regardless of whether you call them bank-fintech partnerships or fintech-bank partnerships, these tie-ups matter, and they are trickier than they seem. In many cases, keeping good partners can be just as difficult as finding good partners in the first place.

Digital acceleration We may be three years past the golden age of digitization, but we’re not going back. Whether you’re a bank or a fintech, if you haven’t digitized your offerings and back-end processes, you may be left behind.

Economic outlook Last year we were worried about a pending recession. This year, we’re sweating about the impact of bank failures. Does anyone know what we’re in for next?

Decentralized finance The concept of decentralized finance (DeFi) was tarnished last year after the FTX scandal took place, and U.S. regulators have been on high alert ever since. There is more to DeFi than cryptocurrency, however, and much of the industry has yet to embrace– or even explore– the possibilities.

VC investing and fintech valuations Venture capitalists are being much more careful with their dollars these days, and many are focusing their investments on early-stage companies. But how can mid-to-late stage startups get much-needed liquidity? Many have advised focusing on unit economics, saying that companies should focus on customer lifetime value and customer acquisition cost.

Embedded finance Non-fintech and banking companies such as retailers and service providers are looking to make it as easy as possible to make a sale, and embedded finance may be the answer. Fintechs can not only help remove the friction from the checkout flow, they can remove the “checkout” all together by moving the processes into the background.

Customer experience We’ve been talking about ways to win when it comes to the customer experience for almost a decade now, so the topic can seem a bit hackneyed. There’s a reason for that, however. Customers have a broad range of needs, and because their preferences are always changing, it can be difficult for banks and fintechs to keep up with their expectations.

Don’t want to miss out on any of these discussions? Be sure to register before April 21 to save $300 on your ticket.

Canadian Crypto Combo: A trio of Canada-based cryptocurrency exchanges announced plans to merge into a single entity. Vancouver-based WonderFi, along with Toronto-based Coinsquare and Coin Smart Financial, are the firms involved. Together, they represent more than $600 million CAD in assets under custody and more than 1.65 million users. The merger will create what the companies are calling “Canada’s largest regulated crypto asset trading platform.”

The road to the three-way union had its complications. At one point, Coinsquare had been poised to acquire CoinSmart. At another point, a merger with WonderFi was allegedly on the table. CoinSmart had been both cold and hot to an acquisition by Coinsquare and reportedly was prepared to seek monetary damages in court when the acquisition deal did not work out. But those days are gone, and the three companies have decided they are better off serving cryptocurrency customers together than they are on their own.

UAE and ANZ Get Busy with CBDCs: There have been a few CBDC-oriented stories in fintech and crypto headlines in recent days. First up is news that the UAE has selected technology and legal partners ahead of the launch of its CBDC strategy. The country’s central bank has picked Clifford Chance to provide legal oversight. R3 and G42 Cloud will serve as technology and infrastructure providers. This will enable the central bank to begin Phase 1 of its CBDC project. This initial phase has three components: initiating real-value cross-border CBDC transactions for international trade settlement, proof-of-concept work for bilateral CBDC bridges with India, and proof-of-concept work for domestic CBDC issuance covering wholesale and retail use. Phase 1 is expected to take place over the next 12 to 15 months.

Meanwhile in Australia, ANZ bank reported that it had concluded one of its projects in the country’s CBDC trials. The project involved using the ANZ stablecoin to settle tokenized carbon credit transactions. ANZ Bank is involved in four of the 15 use cases and projects in the country’s CBDC pilot. With regard to this specific use case – applying tokenization to the carbon markets – ANZ Banking Services Lead Nigel Dobson expressed optimism. He highlighted the potential to improve both efficiency and transparency, as well as “preserve the unique characteristics of underlying projects to incentivize investment in climate solutions.”

Speaking of the relationship between crypto and the climate, SEB and Crédit Agricole announced this week that they are jointly launching so|bond, a sustainable and open platform for digital bonds built on blockchain technology. The platform enables issuers in capital markets to issue digital bonds onto a blockchain network in an effort to enhance efficiency and support real-time data synchronization between participants. Additionally, the network is using a validation protocol, Proof of Climate awaReness, that encourages participants to minimize their carbon footprint.

“Crédit Agricole CIB is proud to contribute to the emerging market of digital assets,” Crédit Agricole CIB Head of Innovation and Digital Transformation Romaric Rollet said. “The platform’s innovative approach, both to the blockchain infrastructure and to the securities market, is coupled with the strong commitment to green and sustainable finance that is at the center of our Societal Project.”

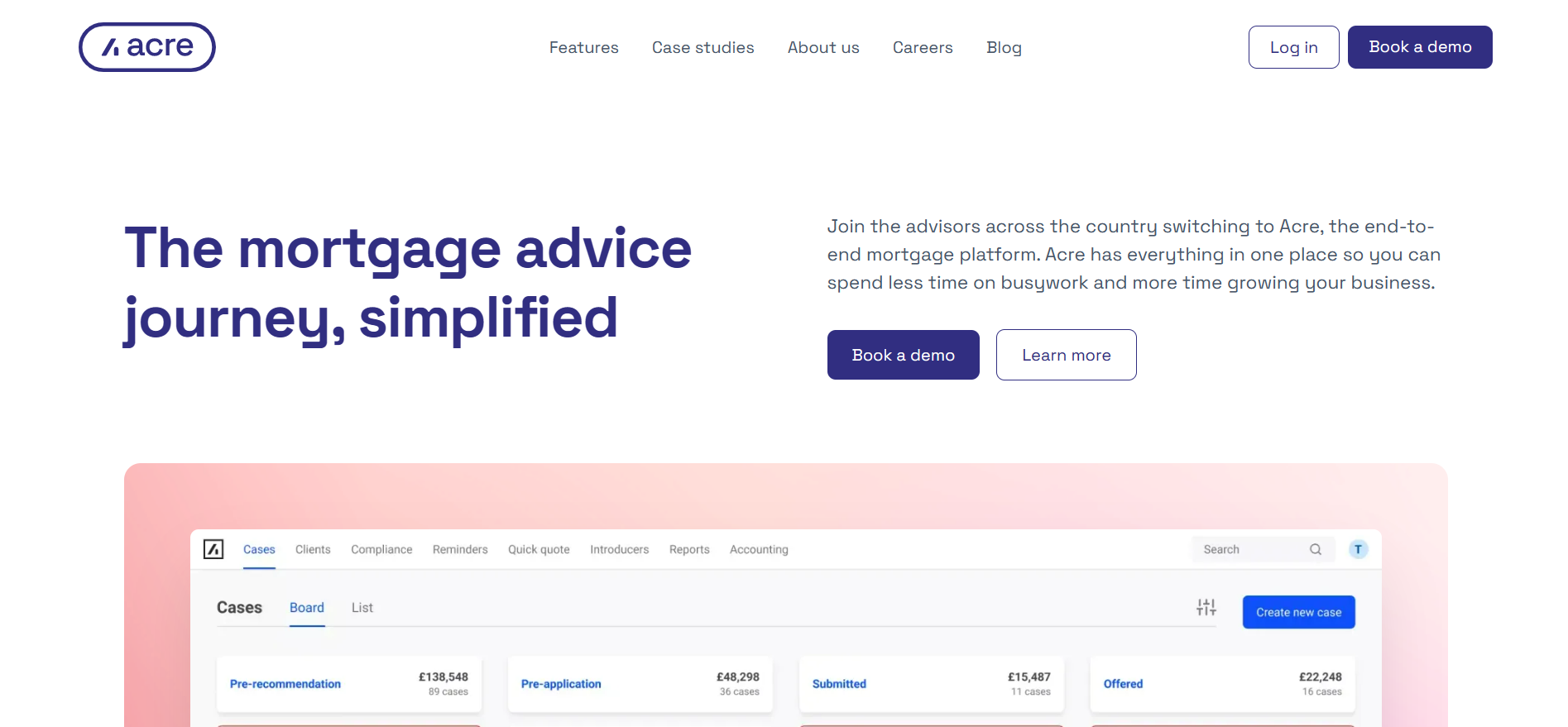

And while on the topic of the blockchain use cases, we report that Acre, a blockchain-based mortgage platform, has raised $8.1 million (£6.5 million). The fundraising is the second major capital infusion for the London-based company and brings the firm’s total equity funding to $14.3 million (£14.3 million). The round was led by McPike, an investor in Starling Bank, as well as Aviva and Founders Factory.

Acre helps traditional brokers compete with their digital counterparts by using blockchain technology to enhance the mortgage and insurance application process for advisers. The company’s technology brings together all aspects of the process into a single “record of the transaction.” This, according to Acre founder and CEO Justus Brown, helps brokers deliver “speedy, efficient advice that meets the individual requirements of each case in a dynamic market.”

Acre was founded in 2017. Brown reports that the company grew by 10x in 2022, and processes £10 billion in annual mortgage volume. In the wake of the latest investment, Acre will focus on forging new partnerships with lenders and insurers to enable brokers to recommend the most competitive financial products and services for their clients.

Coinbase Announces Derivatives Exchange Upgrade: Last up for this edition of 5 Tales from the Crypto is news from one of the industry’s banner companies, Coinbase. The firm announced this week that it had partnered with Transaction Network Services (TNS). The partnership is designed to enable faster, more efficient transactions on its derivatives exchange (CDE).

“Crypto has witnessed both volatile and liquid markets, and with institutional adoption remaining strong, we believe the time is right for the offering that TNS brings to the table,” Coinbase Derivatives Exchange CEO Boris Ilyevsky said. “Dedicated cloud infrastructure connectivity coupled with our derivatives exchange represents a mission-critical step toward supporting and maintaining a vibrant and reliable crypto derivatives market.”

Coinbase launched its Derivatives Exchange in June of last year with the goal of attracting more retail traders to its platform. This week’s news shows that the company recognizes the potential attraction its exchange could have for institutional investors, as well. Regulated by the Commodity Futures Trading Commission (CFTC), the CDE will leverage its new TNS-provided financial trading infrastructure to enable institutional investors to grow their storage capabilities and process large data sets with less delay.

If you need a break from bank failure news, here’s something refreshing. OpenAI’s GPT-4 was released yesterday. The new model is the successor to GPT-3.5-turbo and promises to produce “safer” and “more useful” responses. But what does that mean exactly? And how do the two models compare?

We’ve broken down six things to know about GPT-4.

Processes both image and text input

GPT-4 accepts images as inputs and can analyze the contents of an image alongside text. As an example, users can upload a picture of a group of ingredients and ask the model what recipe they can make using the ingredients in the picture. Additionally, visually impaired users can screenshot a cluttered website and ask GPT-4 to decipher and summarize the text. Unlike DALL-E 2, however GPT-4 cannot generate images.

For banks and fintechs, GPT-4’s image processing could prove useful for helping customers who get stuck during the onboarding process. The bot could help decipher screenshots of the user experience and provide a walk-through for confused customers.

Less likely to respond to inappropriate requests

According to OpenAI, GPT-4 is 82% less likely than GPT-3.5 to respond to disallowed content. It is also 40% more likely to produce factual responses than GPT-3.5.

For the financial services industry, it means using GPT-4 to power a chatbot is less risky than before. The new model is less susceptible to ethical and security risks.

Handles around 25,000 words per query

OpenAI doesn’t measure its inputs and outputs in word count or character count. Rather, it measures text based on units called tokens. While the word-to-token ratio is not straightforward, OpenAI estimates that GPT-4 can handle around 25,000 words per query, compared to GPT-3.5-turbo’s capacity of 3,000 words per query.

This increase enables users to carry on extended conversations, create long form content, search text, and analyze documents. For banks and fintechs, the increased character limit could prove useful when searching and analyzing documents for underwriting purposes. It could also be used to flag compliance errors and fraud.

Performs higher on academic tests

While ChatGPT scored in the 10th percentile on the Uniform BAR Exam, GPT-4 scored in the 90th percentile. Additionally, GPT-4 did well on other standardized tests, including the LSAT, GRE, and some of the AP tests.

While this specific capability won’t come in handy for banks, it signifies something important. It highlights the AI’s ability to retain and reproduce structured knowledge.

Already in-use

While GPT-4 was just released yesterday, it is already being employed by a handful of organizations. Be My Eyes, a technology platform that helps users who are blind or have low vision, is using the new model to analyze images.

The model is also being used in the financial services sector. Stripe is currently using GPT-4 to streamline its user experience and combat fraud. And J.P. Morgan is leveraging GPT-4 to organize its knowledge base. “You essentially have the knowledge of the most knowledgeable person in Wealth Management—instantly. We believe that is a transformative capability for our company,” said Morgan Stanley Wealth Management Head of Analytics, Data & Innovation Jeff McMillan.

Still messes up

One very human-like aspect of OpenAI’s GPT-4 is that it makes mistakes. In fact, OpenAI’s technical report about GPT-4 says that the model is sometimes “confidently wrong in its predictions.”

The New York Times provides a good example of this in its recent piece, 10 Ways GPT-4 Is Impressive but Still Flawed. The article describes a user who asked GPT-4 to help him learn the basics of the Spanish language. In its response, GPT-4 offered a handful of inaccuracies, including telling the user that “gracias” was pronounced like “grassy ass.”

Last week, to kick off Women’s History Month, we highlighted the women who will be representing their companies on Day One at FinovateEurope on March 14 next week in London.

Today, on International Women’s Day, we would like to introduce you to the women who will be taking center stage with keynote addresses, fireside chats, and more on Day Two of FinovateEurope.

Suraya Randawa

Head of Omnichannel Experience at Curinos, Panelist. Meet at the Cafe.

It’s the first day of March, which means FinovateEurope is officially taking place this month on March 14 through 15 at the Intercontinental O2 in London (there’s still time to register). As you preview the agenda and prepare your notes on must-see company demos, you’re probably also filling your schedule with meetings and after parties. Because, let’s face it– sometimes the networking is just as good as the on-stage content.

After 12 years of attending Finovate events, I’ve seen some unique attendees on the networking floor– including a dog and a baby. But who can you expect to see this year? Our audience is generally comprised of financial institution executives, startup representatives, industry analysts, and venture capitalists. However, everyone has a unique “conference personality.” Below, I’ve broken down these personalities into five categories.

The Front Row Fiend

This is the person that arrives extra early to secure their seat in the front row. They’re usually analysts or journalists in search of taking quality, up-close pictures of the on-stage discussions. As an added bonus, because they have their choice of auditorium seat, they usually secure a spot next to a much-coveted power outlet.

The Standing Room Only

Opposite in personality to the Front Row Fiend, the Standing Room Only person prefers the back row. They like being in the back so much that they forgo the luxury of sitting, even during the longest sessions. Whether they stand in the back because they are hoping to run into a colleague or because they enjoy watching the people in the audience, it is possible that the handful of people that stand in the back of the auditorium know something that the rest of us don’t.

The Demo Obsessed

Finovate was a pioneer of the tech demo model back in 2007, and many veteran attendees return each year just to watch the demos. This is where the Demo Obsessed personality comes from. These are the people that pay attention to every detail of every demo. They are both quick to applaud and quick to critique. This brings me to the next personality…

The Tweeter

This person is the perfect combination of someone who thinks quickly on their feet and who knows how to work a social platform. During every session, the Tweeter always has their two thumbs ready to type a comment, reply, critique, or a recently stated statistic into Twitter– and they always do so using the correct hashtags while tagging the proper username.

The Hallway Conference Caller

If you go to enough conferences, there’s no doubt you’ve been the Hallway Conference Caller at some point. This is the person huddled in a corner wearing ear pods and holding their computer so they can jump on a weekly scheduled call and quickly have their input before returning to the auditorium or networking floor.

There are plenty of reasons why FinovateEurope 2023 next month will be one of the year’s biggest fintech events. With just over a week left to take advantage of early-bird savings on your FinovateEurope ticket, we thought we’d share a handful of our favorite reasons why we hope to see you in London, March 14 and 15.

New Keynote Speakers!

FinovateEurope 2023 will feature the return of many of our favorite keynote speakers. But this year’s event will also showcase a number of newcomers. At the top of the list is Leda Glyptis, veteran banking professional and author of the book Bankers Like Us. With a mainstage keynote on Day One of FinovateEurope titled “The Problem with Digital Transformation Is You,” Glyptis will examine the key role that financial services professionals play in helping – or hindering – the process of digital transformation in their own businesses and institutions.

Also making their Finovate debuts as keynote speakers at FinovateEurope are John C. Hulsman, President and Managing Partner, John C. Hulsman Enterprises, who will speak on the global economy; and Adam Lowe, Chief Product & Innovation Officer, Arculus by CompoSecure, who will discuss securing digital platforms and optimizing the customer experience.

FinovateEurope will also present a series of Quick Fire Keynotes. Leading these 10-minute presentations are Matt Bullivant, Director of ESG Strategy, OakNorth, who will speak about climate change, ESG, and financial services; Martin Hyde, EMEA Payment Partnerships Lead, J.P. Morgan Payments, who will talk about the power of embedded payments in financial services; and Dhaksha Vivekanandan, founder of Daylight Robbery, who will discuss bitcoin and the relationship between traditional and decentralized finance.

New Demoing Companies!

Of the 30 fintech innovators demoing their latest solutions live on stage next month, nearly half will be making their Finovate debuts. Representing countries as diverse as Scotland, Austria, Estonia, India, Switzerland, Israel, Sweden, and Bulgaria – as well as the U.S. and U.K. – these newcomers include:

The official name of the session is “Pre-Event Briefing for Financial Institutions.” But we know a pre-funk when we see one! On March 13 – “FinovateEurope Eve” if you will – we are hosting a special, invite-only occasion featuring expert insights into top fintech trends, a special address, and a fireside chat with keynote speaker, Steven Van Belleghem. We’ll top off the evening with drinks and networking to allow attendees to spend quality time with fellow professionals from banks and other financial institutions.

Alumni Alley: How the Best Have Won

Alumni Alley is our opportunity to showcase some of the biggest brands in fintech that have demoed their innovations live on the Finovate stage. For our upcoming conference next month, the focus will be on FinovateEurope alums. Check out our coverage of some of FinovateEurope’s most storied alums.

If you’re working with a bank, an established fintech innovator, or a bold, new startup, Alumni Alley is a unique chance to gain insights and ideas that can help you grow your organization, improve partner relationships, and take your business to the next level.

“If You Start Me Up”: Finovate’s Startup Booster Program

Our Startup Booster program is designed to enable early-stage startups to take advantage of the full Finovate experience – at a price point appropriate for their early-stage status. Held on March 15, participants in our Startup Booster Program will hear from successful founders about partnership strategies, insights into the investment process, tips on how to land your first bank customer, and more.

Following the presentations, startups will have two hours of networking time with investors from across the U.K. and Europe.

What’s Hot? What’s Not? The GameShow!

Think you know what’s hot and what’s not among fintech’s competing trends and passions? Join us for our special event – What’s Hot? What’s Not? The Gameshow! – where we’ll pit veteran fintech analysts and insiders against the wisdom of the crowd to find out who really knows where fintech is headed!

Our unique gameshow format – in which you the audience get to play judge and jury – will bring a little lighthearted fun to the discussion of fintech trends, and add a little healthy competition to the endless debate: HOT? Or NOT!

Early-bird savings for FinovateEurope end on March 3rd. Visit our FinovateEurope hub today and save your spot!

It’s the first day of Black History Month, and this year’s theme is Resistance. We’ll be serving up related coverage all month, and today’s piece sets the scene.

In an effort to highlight Black founders in our industry, we gathered a list of 70 fintechs with Black founders. This is far from an exhaustive list of fintechs with African American founders, but it is a good representation of diverse, relevant* companies.

Helps reduce delinquencies and increase revenue while helping people pay off debt sooner and with fewer penalties Founders: Diana Frappier, Phaedra Ellis-Lamkins

Empowers general partners and limited partners to focus on building enduring relationships and investment opportunities Founders: Adam Ginsburg, Alex Robinson, Yonas Fisseha

Enables secure and seamless data transmission using the ultrasonic data technology Founders: Chris Ostoich, Chris Ridenour, Josh Glick, Nikki Ridenour, Rodney Williams

Provides a financial advice platform that powers SmartAdvisor, a marketplace connecting consumers to financial advisors Founders: Michael Carvin, Philip Camilleri

Offers a social investing platform where you can talk about investments with friends and make trades on the market. Founders: Darian Bhathena, Jack Phifer, Michael Liu, Roger Cawdette

An all-in-one platform that offers financial tools to help creators grow their business Founders: Arabian Prince, Chris Mendez, Chris Schwartz, James Jones Jr.

Provides a community finance platform where members request and fund emergency needs Founders: Jarrel Carter, Rodney Williams, Taylor Bruno, Travis Holoway

Offers a lending platform that provides short-term financing to qualified TV and Film productions Founders: Janelle Alexander, Jon Gosier, Josh Harris, Mickey Vetter

Helps essential professionals buy homes and build financial security near the communities they serve Founded: Alex Lofton, Jesse Vaughan, Jonathan Asmis

Offers a relationship-based lending application that simplifies and automates loans between friends, family, and trusted relationships. Founders: Dennis Cail, Michael Seay

Provides a rewards and loyalty infrastructure for banks and businesses in Africa Founders: Harshal Gandole, Madonna Ononobi, Simeon Ononobi, Suraj Supekar

Offers an Automated Mortgage Advisor that simulates buying a home with multiple lenders to determine mortgage approval odds and affordability impact based on lifestyle Founders: Bryan Young, Steven Better, Tim Roberson

Provides an operating system for active investment management, powering investment products, and experiences for retail investors Founders: Clayton Gardner, Joe Percoco, Max Bernardy

Offers a global split payment platform built for co-creators on any project, anywhere Founders: Adam Clabaugh, Mangesh Bhamkar, Marcus Cobb, Rachel Knepp

Enables lenders to open more accounts by showing users the actions necessary to meet eligibility for their financial goals Founders: Abb Kapoor, David Potter

Provides an AI-powered 401K alternative stock investing platform helping everyday investors retire early Founders: Ben Malena, Johnathon Albercrombie, Lakeisha Turner, Ronnie Green

Partners with mortgage lenders to offer a seamless digital homebuying experience for their clients Founders: Frederick Townes, Marcos Carvalho, Mauro Repacci

If you’re not familiar with OpenAI’s newest technology, ChatGPT, now is the time to spend a few minutes to sign up and play with the chatbot that has captured the world’s attention. ChatGPT leverages Generative Pre-trained Transformer 3 (GPT-3), OpenAI’s language generation model, and it is poised to disrupt a lot more than the customer service.

While ChatGPT has a multitude of use cases in the fintech industry– from automating copywriting to crafting a job description– GPT-3 is even more powerful. Accessed through OpenAI’s API, it can be tailored to suit a range of natural language processing tasks and runs on 175 billion parameters. ChatGPT has only 20 billion parameters. More importantly, firms can use GPT-3 via an API in a compliant environment.

The applications for GPT-3 across fintech and banking are seemingly endless, but I’ve outlined a handful of ways banks and fintechs can use the technology without requiring additional resources to save costs and create a better user experience.

Automate customer service interactions

Banks and fintechs can integrate GPT-3 into a chatbot or virtual assistant to lessen the volume of phone inquiries into their customer service department. GPT-3 can handle common customer inquiries, such as account balance inquiries or loan application status updates.

Enhance fraud detection

Organizations can use historical transaction data to train GPT-3 to identify patterns and flag anomalies that may indicate fraudulent activity.

Streamline document processing

GPT-3 can prove useful to firms that process a large number of documents and need to extract specific information from the paperwork. The technology can automatically extract information from financial documents, such as invoices or loan applications, which ultimately saves time by reducing manual data entry.

Create more personalized financial advice

Advisors can use GPT-3 to generate financial advice, such as investment recommendations, for their clients. In order to tailor the advice to the individual, GPT-3 will take into account customer demographics, risk tolerance, and investment goals.

Create sentiment analysis

From a marketing perspective, GPT-3 can be used to determine brand awareness and overall sentiment toward a company or brand. By analyzing customer feedback and social media interactions, companies can gain insight on new product deployments and measure customer satisfaction over time.

While many of these tools and capabilities have been available in the fintech and banking industry for over a decade, they are now even more powerful. What’s more, using GPT-3 may be more cost effective in the long run because of the range of use cases the technology presents.

Our first Five Tales from the Crypto column of 2023 takes a look at cryptocurrency firms receiving funding, launching new payments solutions, and teaming up with e-commerce innovators to help bring cryptocurrencies and digital asset technology into the mainstream.

Tap Global Secures $3.7 Million in Funding

Cryptocurrency firm Tap Globalwent public this week in an IPO that raised $3.7 million (£3.1 million) for the Gibraltar-licensed firm. But don’t go looking on the NASDAQ for shares; the company is trading on a London-based alternative trading platform called the Aquis Stock Exchange. Aquis was founded in 2001 as a primary and secondary market for both equity and debt securities. Approximately 90 primary market securities are listed, with more than 600 names on Aquis’ secondary market.

Tap Global CEO David Carr addressed the controversy surrounding the company’s decision to go public at a time when cryptocurrency-related businesses are under additional scrutiny. “Our decision to list now raised some eyebrows, particularly in the wake of the FTX fallout,” Carr said. “But it is our focus on regulation and customer protection that sets us apart from less responsible operators.”

Tap Global shares were priced at $0.05 (4.5 pence). Nearly 69 million shares were listed. The listing was accomplished via a reverse takeover by Quetzal Capital and the company will trade under the ticker “TAP.”

With more than 100,000 registered users in more than 46 countries, Tap Global offers fiat banking and crypto settlement services. Users can purchase up to 26 different crypto assets on the Tap Global app and store them directly in the customer’s wallet. Fiat currencies such as the British pound, the Euro, and the U.S. dollar can also be stored. Tap Global leverages proprietary AI middleware to help users secure the best execution and pricing in real time.

Africa-based crypto exchange Yellow Cardintroduced a new payment feature this week called Yellow Pay. The new offering enables Yellow Card customers to send and receive money instantly via the Yellow Card crypto exchange platform with only a few taps on their phone. There are no additional charges for the service.

“This is more than just a money transfer service – it’s a powerful tool that will unlock new opportunities for people across Africa,” Yellow Card co-founder and CEO Chris Maurice said. “By enabling instant, low-cost transactions across borders, we are helping to create a more connected and dynamic Africa.”

Yellow Card enables users to buy and sell Bitcoin, Ethereum, USDT via bank transfer, mobile money, cards, or cash. In order to send funds, users simply require the recipient’s phone number. Fund recipients, as well as those looking to withdraw sent funds, must enroll in Yellow Pay.

“This new product feature not only makes it easier for family members to support each other across Africa with ease,” Maurice said, “but it also opens up the continent to more investment, access to credit, business grants, and generally will improve the ease of doing business.”

Yellow Card was founded in Nigeria in 2019. The company is currently active in 16 countries and, in September, announced that it had surpassed the one million user mark earlier in the year. Also in September, Yellow Card reported that it had received $40 million in Series B investment. The round was led by Polychain Capital, and featured participation from a number of investors including Valar Ventures, Third Prime, Sozo Ventures, Castle Island Ventures, and more. The funding took Yellow Card’s total funding to $57 million. Polychain Capital Partner Will Wolf praised the company as having “the best executing team on the continent.”

Nebeus Launches Visa-backed Debit Card

Back in Europe, cryptocurrency app Nebeuswent live with its Visa-backed Nebeus debit card. The Nebeus Card will enable users to spend directly from their Nebeus accounts, and will be available in markets throughout Europe.

“With this, Nebeus reaches another level of integration and offers a solid connection of everyday payments with superior crypto services,” Nebeus COO and Head of Product Michael Stroev said. “It is a significant accomplishment for us and the most recent illustration of the enormous complementarity between the current banking system and digital assets.” Stroev also noted that the company plans to add Apple Pay and Google Pay functionality as part of “upcoming development phases” of the card. Nebeus also plans to launch a line of credit to enable customers to make transactions without having to sell their cryptocurrency holdings. Stroev said the developments are part of the company’s determination to “contribute towards global financial inclusion.”

Headquartered in Barcelona, Nebeus is registered as a cryptocurrency custodian and a Virtual Assets Service Provider by the Bank of Spain. The company was founded in 2014.

Revelator Partners with Stripe on NFT Payments

Does anyone still care about NFTs? Digital IP infrastructure provider to music companies Revelator announced this week that it was teaming up with Stripe to help it launch a new NFT payment infrastructure. The new functionality would reside on top of Revelator’s digital music supply chain management services.

Revelator CEO and founder Bruno Guez said that the partnership between Stripe and Revelator would play a key role in encouraging those in the music industry who are “non-crypto natives” to learn about the opportunities in Web3. “This is a major step toward Revelator’s vision of onboarding more labels, artists, and fans onto Web3, to bring these promising digital assets to the mainstream of music fans,” Guez said.

Guez said that integrations like this are critical in lowering the technical barriers that currently exist between musicians, music fans, and music companies on one side and what Guez called “a thrilling new medium” on the other. The new NFT functionality will give Revelator Pro platform users the ability to create, sell, distribute, and manage NFTs from a single location. The Stripe integration will enable NFT buyers to set up an account and purchase NFTs with a single click.

Coinbase’s Armstrong: “Dark Times Weed Out Bad Companies”

If it’s always darkest before the dawn, then hopefully a new day is indeed ahead for Coinbase. The company struggled with challenging headlines this week as the sentiment around cryptocurrencies continues to be mixed, at best. On Tuesday, the brother of a former Coinbase product manager was sentenced to 10 months in prison for what is believed to be the first case of cryptocurrency-based insider trading. The same day, the company announced that it would reduce operating expenses by 25%, which included laying off approximately 20% of its workforce, representing some 950 employees.

In a blog post addressed to Coinbase employees, company co-founder and CEO Brian Armstrong expressed optimism toward the future of cryptocurrencies. Despite the falling prices of Bitcoin, Ethereum and other cryptocurrencies – as well as the “fallout from unscrupulous actors in the industry” – Armstrong wrote that he believed “recent events will ultimately end up benefiting Coinbase greatly.” He compared the current challenges faced by the cryptocurrency industry to the early days of the Internet and suggested that “the most important companies not only survive but thrive” in what he called “dark times.”

Coinbase made its Finovate debut in 2014 at FinovateSpring.

It can be difficult to pin down a birth year for fintech, but no matter how you look at it, our industry has come a long way. I was recently reminiscing and found a post published in 2003 by Finovate Founder Jim Bruene titled, The 10 Most Significant Innovations & Developments of 2003. These developments, Bruene said, “provide the best glimpse at the future of online financial services delivery.”

2003 was officially 20 years ago, which makes it a perfect benchmark. I’ve taken a look at the 10 developments and innovations that Bruene deemed “most significant” in 2003, and outlined some of fintech’s most recent updates and persistent struggles.

Phishing undermines trust (for now)

One of the original enemies to widespread adoption of online banking was phishing. In the last two weeks of December of 2003, one (now-defunct) organization had recorded 60 unique phishing attacks, sending an estimated 60 million fraudulent messages.

Those numbers don’t look so bad compared to today’s figures. The Anti-Phishing Working Group (APWG) recorded more than 14,000 phishing attacks per day in the third quarter of 2022, marking the worst quarter for phishing the organization has ever observed. However, while phishing persists, it hasn’t deterred the majority of users from adopting digital banking.

Banks move to boost security perceptions

In this section, Bruene referenced an increase in keylogging incidents, along with one bank’s efforts to circumvent keylogging attacks by adding a keypad on the screen to allow users to click the buttons to enter their PIN instead of typing on their keyboard. The bank also implemented a secondary password requirement.

While these workarounds likely mitigated some of the fraud, they simultaneously introduced more friction for end users. Today, many firms have implemented biometrics to eliminate keylogging. However, while biometrics may have gotten rid of keylogging attacks, the authentication method has not put an end to fraud.

Citibank launches interbank transfers (A2A)

Citibank added online interbank transfers in the fall of 2003, making it the first major U.S. bank to offer such a service. At the time, Citi tapped CashEdge (acquired byFiserv in 2011 for $465 million) to power the transfers.

Today, of course, the industry doesn’t consider account-to-account transfers an innovation. Rather, the service is now considered table stakes for all banking service providers. What has changed are the rails. A handful of banks have started piloting using the blockchain to transfer funds, especially in the case of cross-border payments.

Press turns positive toward online banking and other online financial activities

Twenty years ago, the dot-com crash was still fresh in the minds of both investors and everyday consumers. According to Bruene, 2003 was a turning point as consumers began to embrace the conveniences and efficiencies of online banking.

Today, while we’re not recovering from a dot-com crash, we are still reeling from the FTX scandal that took place late last year. It is estimated that around $1 billion to $2 billion in consumer funds were lost after the digital crypto exchange failed. And while the event will not result in negative press about fintech in general, it has already soured the press and industry analysts on crypto.

Bank of America hits seven million users

As you may imagine, adoption of Bank of America’s digital banking looked vastly different in 2003. “Bank of America had as many online banking customers as all U.S. banks combined had five years ago (at year-end 1998),” said Bruene. “The bank’s 7 million active users account for 43% of its checking account base, and 22% of all households. Year-over-year growth was an impressive 50%, with 2.3 million new active users.”

Today, Bank of America serves 67 million retail and small business clients. Of those, 55 million use Bank of America’s digital banking services. In July of last year, those customers logged into their Bank of America accounts one billion times– a record number for the bank.

The decline of paper statements begins

While 2003 may have marked a decline in paper statements, it didn’t mark the beginning of the end. According to a 2017 Javelin Strategy & Research report, only 61% of checking account customers have committed to paperless statements. In the report, Javelin suggests that much of this is unintentional. “Consumers now reflexively reach for their smartphones in all aspects of their lives and banking is not an exception,” said Mark Schwanhausser, Director, Digital Banking at Javelin Strategy & Research. “The intent is not to take statements away from customers; it is to provide an alternative that convinces them that paper statements are as unnecessary and obsolete as a checkbook register.”

Banks redesign websites for Yahoo-like clarity

Of the ten developments on this list, this one is my favorite, and not only because of the use of Yahoo! as an example. Optimizing online user interfaces is a science, and by 2003, developers didn’t know as much as they do today about creating user-friendly services.

Today, the shining examples in tech have shifted from Yahoo! to the likes of Uber, Stripe, and Airbnb. And by now, most large firms’ digital experiences exhibit “Yahoo-like” clarity. Still, there will always be room for improving the user experience, especially as consumers become aware of new enabling technologies like open finance.

Real-time credit for remote deposits

In this section, Bruene applauded two FIs for offering consumers instant credit for mailed remote deposits. It baffles me to think about mailing in a paper check to deposit it. However, in a pre-smartphone era such as 2003, there weren’t many other options that didn’t require additional hardware or infrastructure.

Today, while consumers can deposit most checks via smartphone, the deposits still generally take two-to-three days to post in consumer accounts. As a bonus, most firms have discovered a way to turn remote deposits into a revenue generating opportunity by charging consumers for instant deposits into their accounts.

Identity Theft 911 provides a credible source to fight ID theft

Identity Theft 911 has a storied history. The company rebranded to CyberScout in 2017, was acquired by Sontiq in 2021, which was bought by TransUnion in late 2021. Regardless of the multiple transitions, all companies shared a similar mission. Today, TransUnion helps consumers build and grow their credit scores, offers credit alerts, fraud alerts, credit monitoring, and more.

What’s different about this industry today, however, is the number of competitors in the space. Many organizations offer free credit monitoring. Other, paid services offer monitoring and reporting from all three bureaus, identity theft insurance, and more.

If you plan on binge watching holiday movies in the next few weeks (or if you have been since October), here’s something to think about. Did you know that many of these films come with lessons for the fintech industry?

Here are some films you may want to watch over your winter break, along with some of the wisdom they hold.

Home Alone (1990)

In this movie, Kevin McCallister finds himself left at home without any adults to help him carry out daily tasks and defend himself against burglars. In the same way, many customers are conducting their banking activities from home on their own devices. The only tools they have to successfully conduct banking activities are a strong password and your bank’s user-friendly design.

Lesson: Don’t make your customers feel at home alone. Provide them with tools they need to successfully conduct everyday banking tasks from your app.

It’s a Wonderful Life (1946)

After George Bailey contemplates suicide during a time of financial instability, his guardian angel comes to show him all the ways in which he has made a difference in the lives of others. In the end, he begs his angel to give him his life back. After he does, his community rallies around him to help him regain financial stability. The current economy is impacting firms across banking and fintech differently. Every organization has a storm to weather.

Lesson: Pay attention to what’s truly important in life and maintain a focus on community, especially in the midst of economic turmoil.

Family Stone (2005)

When a woman from the big city, Meredith, accompanies Everett, her boyfriend, to his childhood home for Christmas, they both discover that they aren’t right for one another. As the story progresses, it becomes apparent that Everett and Meredith’s sister Julie are falling for each other. Keep your bank or fintech partners in mind while watching this one.

Lesson: Finding the right bank or fintech partners can be a struggle. However, it is worth conducting proper due diligence to find the right partner before committing.

The Santa Clause (1994)

Toy salesman Scott Calvin is unexpectedly forced to become Santa Clause after the original Santa Clause falls off his roof. After spending much of the movie in denial and resisting his new role as Saint Nick, Scott Calvin ultimately accepts his new role, and everyone is better off because of it. Has your organization ever had to make a similarly drastic pivot?

Lesson: When the needs of the customer evolve, so should your business. Being able to pivot to meet customer expectation not only benefits end users, it will also be good for your bottom line.

Die Hard (1988)

When New York City Policeman John McClane visits his ex-wife at a holiday party on Christmas Eve, terrorists attempt to take over the building and John realizes that he is the only one who can save everyone. Whether you can see the fraudsters or not, everyone deals with them on a daily basis.

Lesson: You are responsible for creating the first line of defense between your customers and cybercriminals.

Jingle All the Way (1996)

In this holiday movie, Howard Langston tries to impress his son by giving him the season’s hottest toy, the Turbo-Man, for Christmas. The toy is almost sold out, however, and Howard goes to great lengths to compete with another father to get the toy. Ultimately– and only after proving himself a hero– Howard gets the Turbo-Man toy to give to his son in time for Christmas. While the customer acquisition race isn’t as competitive as a war over the Turbo-Man toy, it may seem like a battle at times.

Lesson: There will always be competition between and among banks and fintechs. And just like Howard’s fight for Turbo-Man, fighting to gain customers takes sacrifices and ultimately may require your organization to prove itself a hero to the customer before winning them over.

How the Grinch Stole Christmas (1966)

The Grinch, who hates Christmas, tries to take the joy away from the townspeople of Whoville by stealing their presents and other Christmas paraphernalia. Even after he does so, however, he hears the townsfolk joyfully celebrating Christmas, despite the lack of presents, food, and decorations. In the end, the Grinch realizes that Christmas is more than presents, tinsel, and bows. Just as the Grinch discovered there is more to Christmas than the money-making aspects of it, perhaps we can all look beyond our bottom lines this season to discover how we can better serve our target market.

Lesson: Perhaps there is more to fintech than just pandering to populations that seem the most profitable. Look for ways to benefit to others, even if they may be a net-zero opportunity.

Any Hallmark Christmas special

Many Hallmark holiday movies seem to share a similar premise. A big-city girl inherits a vineyard or a bed and breakfast in a small town. During her visit to the country, she meets a charming man and falls in love with both him and the small town lifestyle. You don’t have to watch a Hallmark movie to realize that expanding your horizons can be beneficial.

Lesson: It may profitable to serve the underserved populations found in rural locations. They could have more in common with your existing target audience than you think.

National Lampoon’s Christmas Vacation (1989)

Clark Griswold tries to create the perfect Christmas for his family, but when the Christmas bonus he expected for the year fails to come through, Clark’s cousin Eddie takes the issue up with Clark’s boss. Though Clark ends up receiving his bonus after all, the movie serves as a reminder not to financially overcommit before funds are guaranteed.

Lesson: Even when times are good, don’t count on extra cash to get your company through. Watch your burn rate.

Frozen (2013)

The main characters, sisters Anna and Elsa, illustrate the ups and downs of the crypto market. After Elsa freezes the town, the damage seems permanent, and residents wonder if they will have to live in wintertime conditions forever. At the end of the film, Elsa figures out how to control her magic and returns the town to its regular climate.

Lesson: Crypto will one day exit the crypto winter and will once again level out. The key to achieving this stasis may be the arrival of regulation in the cryptocurrency space, which is already be on its way. Today, U.S. Senator Elizabeth Warren unveiled a bill to enforce against crypto money laundering.

The fallout over the collapse of cryptocurrency exchange FTX continues. On Friday, the embattled company filed for Chapter 11 bankruptcy protection, noting that it had in excess of 100,000 creditors – before amending its filing days later to report that the number of creditors might be more than one million.

While 2022 has been a dark year for a number of cryptocurrency companies, none have suffered as FTX has. With a valuation of $32 billion and more than one million users, FTX was the third largest cryptocurrency exchange by volume last year. But all of this came crashing down earlier this month. When rival Binance learned that FTX partner Alameda Research had much of its assets in FTX’s token FTT, Binance began selling its holdings of FTT. This resulted in more selling, in what some observers have called the equivalent of a bank run, which demolished the value of FTT and created a serious liquidity crisis for FTX. An aborted plan by Binance to buy FTX gave the company few alternatives to the bankruptcy declaration it made late last week.

What’s next? The FTX crisis has reached the recrimination stage, with even the company’s performance coach weighing in. (You can read Dr. Lerner’s response to rather lurid allegations about the behavior of the company’s senior executives. Spoiler: he refers to the company’s Bahamas headquarters as a “pretty tame place”). A sizeable swathe of celebrities – from NFL star quarterback Tom Brady to supermodel Gisele Bundchen- who served as brand ambassadors for FTX are also finding themselves under scrutiny – and worse.

And speaking of scrutiny, it appears as if the FBI is in discussions with the Bahamian authorities on extraditing FTX founder Sam Bankman-Fried to the United States for questioning.

Et tu, BlockFi?

Is cryptocurrency lender BlockFi now endangered due to the crisis at FTX? Media reports from The Wall Street Journal indicate that the company, launched in 2017 and headquartered in Jersey City, New Jersey, may be considering bankruptcy.

Why? According to reports, BlockFi admitted that while it did not keep the majority of its assets at FTX, the firm did have deposits on the company’s platform, as well as an undrawn line of credit from FTX “and obligations that FTX owed it.” BlockFi has suspended customer withdrawals in the wake of the FTX collapse, is limiting platform activity, and also is reportedly planning to layoff an unspecified number of workers.

BlockFi has not responded to the reporting from The Wall Street Journal at this time. A message at the company’s website reads: “BlockFi is not able to operate business as usual. We have limited platform activity, including pausing client withdrawals as allowed under our Terms. We request that clients not deposit to BlockFi Wallet or Interest Accounts at this time.”

Anthony Pompliano Makes Crypto’s Case

Entrepreneur and investor Anthony Pompliano was interviewed on CNBC’s Overtime program Tuesday afternoon. Asked about the FTX situation, Pompliano made an impassioned case for the future of cryptocurrencies. Pompliano also argued that the American market-based system is the only place where this kind of innovation – and accountability – is possible.

Pompliano runs investment firm Pomp Investments. He was formerly co-founder and partner with Morgan Creek Digital Assets, and Managing Partner with Full Tilt Capital. Pompliano also was a Product Manager at Facebook where he led the growth team for Facebook Pages, and helped launch solutions including AMBER Alerts and Voter Registration. He is the author of a daily email newsletter of business, finance, and Bitcoin called “Pomp Letter.”

Plug and Play Launches Crypto Program

At a time when so many are down on cryptocurrencies, it may be reassuring to hear news that innovation platform Plug and Play is keeping the faith.

In collaboration with founding partners Visa, AllianceBlock, The INX Digital Company, IGT, and Franklin Templeton, Plug and Play has launched its new Crypto and Digital Assets program in Silicon Valley. The goal of the program is to help startups around the world that are innovating in the crypto and digital asset spaces to connect with the program’s aforementioned founding partners to help them pilot their solutions. The program has four main focus areas: stablecoin adoption, decentralized finance, crypto economics, and enterprise blockchain.

“Not only will this unique partnership offer deeper connections on the West Coast and Silicon Valley, but it will also allow us to put our leadership and expertise to work as we advise companies on the benefits of participating in the rapidly growing ecosystem of blockchain, tokenization, and cryptocurrency,” INX Chief Business Officer Douglas Borthwick said.

Companies interested in participating in the Plug and Play Crypto and Digital Assets program are being encouraged to apply.

Binance Battles On

With its decision to acquire FTX now a thing of the past, blockchain company Binance is back to focusing on its own organic growth.

The company announced at midweek that it has secured a license from the Financial Services Regulatory Authority (FSRA) of Abu Dhabi Global Market (ADGM). This license — a Financial Services Permission (FSP) — will enable Binance to offer digital and virtual asset custody services to professional clients that meet the FSRA’s conditions for FSP.

“Obtaining this license is a pivotal step in the growth of Binance in Abu Dhabi, and a reflection of the city’s progressive stance on virtual assets,” Binance (AD) Senior Executive Officer Dominic Longman said. “We are excited to continue to strengthen our symbiotic relationship with ADGM and the city of Abu Dhabi and look forward to providing institutional investors with a secure and reliable platform for their virtual asset activities.”

ADGM’s FSRA issued its virtual asset regulatory framework in 2018. ADGM Chairman Ahmed Jasim Al Zaabi said that the framework is a core part of ADGM’s goal of supporting fintech innovation in the financial sector and “reinforcing the UAE’s status as a rapidly accelerating global crypto marketplace, with Abu Dhabi and the ADGM as the engine room powering this growth.”

Finovate has held two fintech conferences in the UAE in recent years: an inaugural event in 2018 and a second conference the following year in 2019. Read more about fintech in developing economies in our weekly Finovate Global column, published on Fridays.