This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

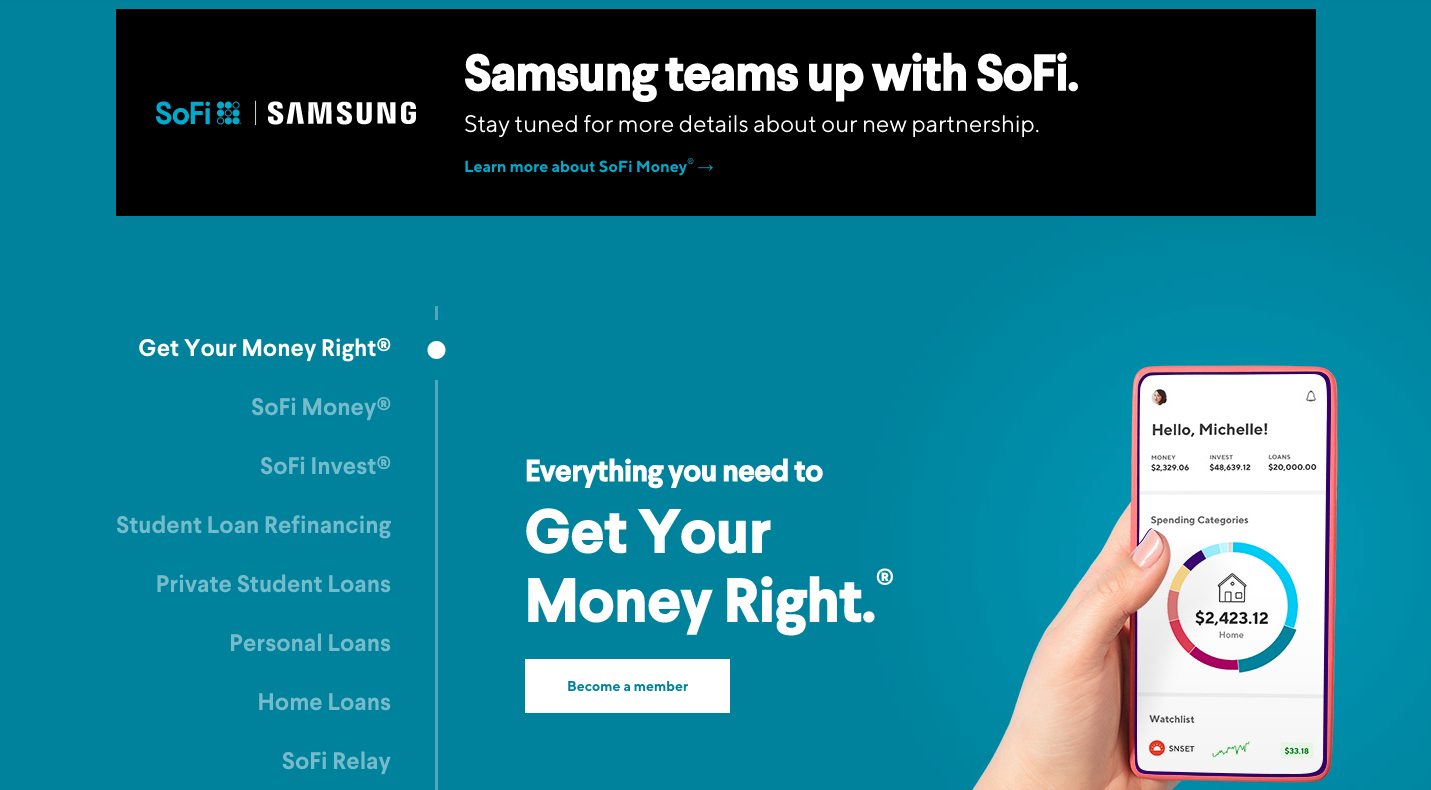

Alternative finance solutions provider SoFi and Samsung’s Samsung Pay joined forces this week to launch a debit card.

The two have spent the last year collaborating to make a mobile-first money management platform with its own debit card and cash management account.

The initiative is part of Samsung’s broader Samsung Pay mobile payments platform that the company launched in 2015. Samsung’s mobile payments platform uses built-in magnetic secure transmission technology (MST) and NFC functionality to enable users to make contactless payments.

“Our vision is to help consumers better manage their money so that they can achieve their dreams and goals,” said Sang Ahn, Vice President and GM of Samsung Pay, North America Service Business, Samsung Electronics in a blog post. “Now more than ever, mobile financial services and money management tools will play an even bigger role in our daily lives while also opening up new possibilities.”

Specific details about the card are still pending.

The new debit card offering will provide Samsung with a unique way to compete with Apple’s Apple credit card. Compared to Apple’s credit card, however, Samsung’s debit card product sounds more sticky. That’s because budgeting and cash management features built into the app will encourage users to spend more time in Samsung’s app and will keep the company’s debit card– along with its mobile payments service– top-of-mind for consumers.

Samsung’s announcement also comes shortly after news leaked that Google has its own debit card in the works. The debit card will work in conjunction with the Google Pay app.

Samsung’s timing on the launch is fairly ideal, despite the global economic crisis. The coronavirus has turned consumers’ attention toward their finances. Because of this, many banks are seeing record downloads of and engagement with their mobile banking tools. This shift to digital, combined with the new low-touch economy when it comes to everyday payments, provides an ideal environment to launch a contactless payment option.

Despite these conditions, the challenger banking space is becoming increasingly crowded in the U.S. However, Samsung’s choice to partner with an existing player instead of creating a product from scratch is a favorable one.

B2B cross-border solutions provider Currencycloud is teaming up with Canadian transaction processor Carta Worldwide to bring transparency, accuracy, and cost-competitiveness to international transactions.

“This is an exciting partnership and the first of its kind, combining our respective skills sets to drive innovation and give customers further transparency on their international card payments,” Currencycloud co-founder and Head of Strategic Partnerships Steve Lemon said. He noted that the partnership would put customers “at the center of the offer” and enable issuers to offer real-time foreign exchange rates at the point of sale to fintechs and challenger banks.

The two companies said in a statement that they are presently in the development phase of the collaboration. Their first joint offering is expected in the second half of 2020.

“We are very excited about this partnership,” Carta Worldwide Managing Director EMEA Richard Wray added. “Carta’s innovative processing capabilities collaborating with one of the most reputable platforms in the industry will enable us to deliver some real change to customers across the world.”

Named one of Canada’s top fintechs by the Digital Finance Institute, Carta Worldwide specializes in processing mobile and prepaid transactions. Founded in 2006 and headquartered in Ontario, Canada, and London, U.K., the company includes Vodafone, Westpac NZ, and Novum Bank among its customers.

Offering 85 APIs across four modules – Collect, Convert, Pay, and Manage – that support the full, B2B cross border payments workflow, Currencycloud provides enterprise-grade payments solutions to partners such as Visa and Starling Bank. Headquartered in London and founded in 2012, Currencycloud is regulated in the U.K., the E.U., the U.S., and Canada. The company began the year with an $80 million Series E fundraising round that featured participation of new backers such as Siam Commercial Bank, SBI Group, and Visa – whose SVP and Treasurer Colleen Ostrowski joined Currencycloud’s board of directors.

More recently, Currencycloud announced a partnership with Derivative Path to enable community and regional banks to offer more FX and interest rate derivative trading options to customers. The company has been a Finovate alum since 2012, and demonstrated its Global Collections solution at our west coast conference in 2018.

Fraud prevention solutions provider Emailage recently announced it has been acquired. LexisNexis Risk Solutions, owned by parent company RELX, closed the deal for $480 million.

Emailage was founded in 2012 by Rajesh Pandey and Rei Carvalho. The company offers an email risk score that uses email address metadata to help businesses assess transactional risk and validate digital identities. Access to this data enables companies to expedite approvals, prevent chargebacks, and automate workflows. Emailage also offers a Digital Identity score that layers in additional data to offer businesses a fuller picture of the user’s online reputation.

LexisNexis Risk Solutions purchased Emailage to integrate the company’s email assessment capabilities into its Digital Identity Network offerings. The integration should be somewhat smooth since the two had an existing commercial partnership prior to the acquisition.

“This acquisition is a natural fit as LexisNexis Risk Solutions and Emailage are both committed to continuously evolving our solutions to combat fraud,” said LexisNexis Risk Solutions Business Services CEO Rick Trainor. “This acquisition will enhance and expand our email data intelligence to provide our customers a more comprehensive view of risk with minimal friction for their customers.”

This isn’t the first fintech RELX has snapped up to boost its fraud and risk management services. The firm has been making a steady stream of purchases in the sector, including ID Analytics, ThreatMetrix, Accuity, and ChoicePoint. RELX has also formed numerous partnerships in the space, including with BioCatch and Blockbid.

LexisNexis Risk Solutions initiated its purchase of Emailage before COVID-19 had overtaken the globe. However, the increased interest in security players is something we can expect to see more of as the virus steers us toward the low-touch economy and drives traditionally brick-and-mortar services into the digital realm.

Credit reporting agency TransUnionunveiled a new division this week that will unite the company’s fraud and risk offerings.

The new unit, Global Fraud & Identity Solutions Group, will tie together TransUnion’s identity verification and authentication tools that help businesses do everything from fight originations fraud to target consumers in their risk profile. The Global Fraud & Identity Solutions Group will also contain the company’s fraud detection and prevention solutions that range from detecting synthetic identities to providing background checks.

The initiative will also accelerate TransUnion’s go-to-market strategy for CallValidate and TransUnion IDVision with iovation. The CallValidate solution was formed in 2018 as the result of TransUnion’s acquisition of Callcredit Information Group. TransUnion’s IDVision solution is also the result of an acquisition the company completed in 2018.

TransUnion has brought on Shai Cohen, former general manager of RSA’s Fraud and Risk Intelligence business, to lead the effort. “We’re excited to bring in a proven leader from some of the world’s most respected cybersecurity and technology companies to unite these efforts and take our fraud prevention solutions to the next level,” said Tim Martin, executive vice president and chief global solutions officer at TransUnion.

The acceleration of a formalized fraud and risk division speaks to the global need for such solutions. The move comes at a time when demand for digital solutions has risen exponentially as consumers seek to conduct many aspects of their daily lives online during social distancing and stay-at-home orders.

TransUnion’s announcement comes on the same day its competitor Experian unveiledPrecise ID Model Suite, a new fraud fighting solution. The tools are specifically aimed to help organizations distinguish between first party fraud and third party fraud to determine their best course of action.

The Securities and Exchange Commission (SEC) announced today that it is temporarily easing up on reporting requirements for small businesses that use crowdfunding as a means for fundraising.

Small businesses looking to raise between $107,000 and $250,000 via crowdfunding are not subject to financial statement review requirements. The SEC also said it will fast-track the approval of crowdfunding listings.

The move is in response to small business’ need for funding to stay afloat while stay-at-home orders have diminished consumer demand– and therefore, revenue. While some were aided by the government’s stimulus package, the Paycheck Protection Plan, many small businesses either did not qualify for the funds or were not able to submit their application.

These small businesses may now more easily solicit the American people to help. “In the current environment, many established small businesses are facing challenges accessing urgently needed capital in a timely and cost-effective manner,” said SEC Chairman Jay Clayton. “Today’s action responds to feedback we have received from our Small Business Capital Formation Advisory Committee and others about the difficulties these companies may face in conducting an offering within a time frame that meets pressing capital needs, while continuing to provide appropriate protections for investors.”

To benefit, companies must disclose to investors that they are relying on the money because of COVID-19. Fundraisers must also meet eligibility requirements, including:

Must have been organized and operating for longer than six months prior to the start of the offering

Must be a U.S. business

Must not be a blank check or an investment company

Must have complied with Securities Act requirements in previous crowdfunding campaigns

The relaxed requirements will be in place until the end of August, so small businesses have just under four months to initiate their campaigns.

Small business expense management platform Bento for Business has a new man at the top. The company announced today that Guido Schulz will join the company as its new CEO. Schulz will team up with co-founder Farhan Ahmad who will remain as chairman of the company’s board of directors.

“Bento for Business has built an incredibly intuitive product that directly addresses the core cash flow and operational problems faced by the businesses that drive much of our economy, create jobs, and help build our communities,” Shulz explained. He called expense management “the single largest area of opportunity” for small businesses.

Founded in 2014, Bento for Business provides expense management solutions that are designed specifically for small businesses and nonprofits. Bento offers business debit cards with spending controls – including virtual cards that can be issued and used instantly – as well as Bento Pay, a B2B digital payments service that only requires the fund recipient’s email address in order to send money. Bento made its Finovate debut at our west coast conference in 2015.

“As we’ve reached a new phase of growth ourselves, bringing on Guido is an important step for delivering the same exceptional experience to businesses as Bento’s footprint continues to expand,” Ahmad said. He praised Schulz’s record in scaling companies and said he looked forward to working together to “deliver a healthy bottom line for businesses through unprecedented visibility and control over monthly expenses.”

Schulz comes to Bento from global hospitality payment gateway provider Merchant Link, where he was Chief Commercial and Strategy Officer. The company was acquired by Shift4 last August. Previously, Schulz worked for Bluefin Payment Systems, where he was also Chief Commercial Officer and, before that, at AFEX as Global EVP and Chief Strategy Officer. He was educated at the University of Erlangen-Nuremberg and was a visiting scholar at the University of Notre Dame.

Bento’s C-suite addition comes almost a year after the company bolstered its executive ranks with the addition of Paula Bachman as Chief Financial Officer. The news also arrives as the company announces a partnership with San Francisco Achievers, a youth development program that is using the Bento for Business app to manage scholarship funds and learn responsible budgeting habits.

“We have an orientation for our scholarship students,” Duane Wilson, the program’s Executive Director explained. “For some of them, this is their very first card. It allows them to have the experience.”

Headquartered in San Francisco, California, Bento for Business has raised $18.5 million in funding. The company includes Edison Partners, Anthemis Group, and Comcast Ventures among its investors.

The millennial-focused social trading and investing app, which drew criticism during the market meltdown in March for repeated outages, is now sitting with $280 million in additional funding. The new capital comes courtesy of a just-completed Series F round led by Sequoia Capital, and gives the company a valuation of $8.3 billion. NEA, Ribbit Capital, 9Yards Capital, and Unusual Ventures also participated in the round.

“Amid challenging times and market volatility, we’re humbled that people are turning to Robinhood to participate in the markets and build their financial future,” the company’s blog read this week. The announcement included data points such as the three million funded accounts the company has added in 2020, as well as Robinhood’s effective outreach to new investors. The company also noted that the funding would be used to scale the Robinhood platform, develop new solutions, and add to its workforce.

Fortune’s coverage of Robinhood’s fundraising features observations on the company’s rumored IPO, the diversification of its revenue and profitability, as well as a potential launch in the U.K.

Founded in 2013 by Baiju Bhatt and Vladimir Tenev, Robinhood offers users the ability to trade and invest, commission-free, in a variety of assets including stocks and ETFs, options, gold, and cryptocurrencies. The app-based platform supports fractional share purchasing, enabling investors to buy equity in thousands of companies with as little as $1, and provides 0.30% APY on uninvested cash. The company began the year with news that its financial newsletter and podcast, Robinhood Snacks, had surpassed 10 million downloads. More recently, to help customers understand recent turbulence in the financial markets, Robinhood unveiled a new Market Volatility page with information on the various steps exchanges take to help mitigate market extremes.

Robinhood became notorious in some circles for the “race to zero” movement last fall in which major brokerages including E-Trade, Charles Schwab, and TD Ameritrade announced plans to eliminate trading fees in stocks and ETFs. Competition with Robinhood was cited as the reason.

A collaboration between fraud prevention and detection company Breach Clarity and digital consulting firm Xtensifi will bring additional machine learning technology to bear in the battle against cybercrime in financial services. The new integration will enable the company’s Breach Clarity Premium for Financial Services platform to empower banks, credit unions, brokerage firms and insurance companies to address the impact of data breaches – from financial losses to identity theft – after they happen.

“We sought out a company we knew would execute our vision and provide us with the knowledge and expertise to get these entirely new products to market,” Breach Clarity CEO Jim Van Dyke said. He credited Xtensifi not only for helping develop the new platform, but also for giving the company the ability to market its technology to a new client base: financial services companies. “Initially consumer focused, we are now able to provide financial institutions with hyper-personalized, customer-level breach risk intelligence, capable of making a measurable difference in a variety of areas – from customer engagement to fraud loss mitigation,” Van Dyke explained.

Founded in 2019 and based in Walnut Creek, California, Breach Clarity analyzes more than 1,000 elements to gauge and score the risk level of a data breach. The company’s proprietary, machine learning algorithm analyzes 50 data breaches a week on average, and Breach Clarity said that it has 4,000+ such incidents in its database. This resource is maintained by the Identity Theft Resource Center.

“Breach Clarity is working to revolutionize the fraud detection, prevention, and mitigation landscape by providing a greater degree of transparency into breaches and their effects,” Xtensifi CEO George Kelley said. “Providing the industry with more clarity, confidence, and direction around breaches will ultimately result in stronger consumer financial health and safety.”

Like a number of companies in the fintech space, Breach Clarity is making its services easier to access during the COVID-19 crisis. More than a month ago, the company announced that it was waiving per-user costs for financial institutions using its Breach Clarity Premium for Financial Services solution for six months.

Breach Clarity co-founder and COO Al Pascual underscored the value of these services at a time when shifting computer use patterns – from business offices to private homes – during the global pandemic have given rise to a shifting set of risks. “As cybercriminals experiment with new forms of cyber scams,” Pascual said, “newly remote workers and the systems to which they are attached will be a high value target.”

Breach Clarity demonstrated its consumer-facing solution last year at FinovateFall. A specialist in post-compromise fraud, Breach Clarity enables users to search any publicly-reported data breach and receive a fraud risk rating, a list of top identity-holder risks, and a set of action steps ranging from freezing credit to modifying alerts to limit exposure to potential identity theft and related cybercrimes.

Small business payments and accounting platform Autobooks unveiled a new initiative today that works directly with small businesses to help them receive credit card payments online.

The program, Get Paid with Autobooks, deposits transaction revenue directly into the business’ existing bank account. The tool was previously only available to small businesses via Autobooks’ existing bank partners. In fact, Autobooks partners with more than 50 banks and credit unions to help them compete with fintechs such as PayPal and Square by offering their small business clients an online payment acceptance tool.

Autobooks is waiving its $10 monthly fee for Get Paid through the end of this year. This offer comes at a time when many businesses have been pushed to accept payments online in order to provide a no-contact experience for their clients. Businesses will still be charged the standard 2.75% on each transaction.

Autobooks lowers the barrier of entry for businesses to accept payments by using a model called payment facilitation. “Non-bank providers such as PayPal, Square, and Stripe have long benefited from this model and it’s now time financial institutions can too,” said Autobooks CEO and Cofounder Steve Robert. “By providing a digital, self-service onboarding and automated underwriting process – a small business can now begin receiving payments directly into their existing checking account within a few minutes.”

Autobooks was founded in 2015 and has since raised $17.5 million in funding. The company offers banks a range of tools, including invoicing, accounting, and billpay, to help them support their small business customers.

China-based internet giant Tencent laid out $300 million to acquire a 5% stake in buy-now-pay-later firm Afterpay.

The move is part of a strategic partnership that will offer Afterpay easy access and collaboration opportunities with Tencent, a Hong Kong-based fintech giant with a $500 billion market capitalization. In comparison, Afterpay’s market capitalization on the Australian Stock Exchange tops just over $8 billion.

Afterpay was founded in 2014 by Nicholas Molnar and Anthony Eisen, who now serves as the company’s CEO. The Australia-based company has 4.6 million users and its revenues totaled over $160 million last year.

“Afterpay’s approach stands out to us not just for its attractive business model characteristics, but also because its service aligns so well with consumer trends we see developing globally in terms of Afterpay’s customer centric, interest free approach as well as its integrated retail presence and ability to add significant value for its merchant base,” said Tencent Chief Strategy Officer James Mitchell.

Tencent’s move comes shortly after its rival Ant Financial took a minority stake in Afterpay competitor Klarna. Afterpay has 3x the web traffic of Klarna and 1.5x the traffic of its other major competitor Affirm.

The buy-now-pay-later segment of fintech has been heating up this year, despite– or perhaps because of– the current economic and health crises. A few weeks back, Goldman Sachs launched MarcusPay, a tool to help borrowers make purchases ranging from $750 to $10,000 and pay for them over the course of 12 to 18 months.

Mambu, the cloud-based banking platform based in Germany, is partnering with U.K. business banking platform Tide to power the company’s revolving credit facilities and overdrafts for small businesses.

“There is a need to be flexible, agile, and customer-centric in the design of financial products,” Managing Director of Mambu EMEA Eelco-Jan Boonstra explained. “Legacy technology constraints can undermine even the best innovation strategy.”

The collaboration will enable Tide to overhaul its product suite in order to better serve customers in a number of locations around the world. This includes offering larger overdrafts, credit cards, and invoice financing, as well as enabling Tide members to lend to each other leveraging solutions managed by Mambu.

“When today’s customers evaluate financial institutions, they no longer compare different banks, they compare experiences,” Boonstra said. “We see this partnership approach as the future of banking technology.”

Regtech is all the rage in fintech these days. From helping businesses negotiate a wave of new regulation – from GDPR to PSD2 – to empowering firms to combat fraud, companies involved in developing technologies to ensure that businesses are getting and staying compliant are enjoying rare attention from the rest of the industry.

A recent review of top regtech startups in Europe in Fintech News was an example of the light increasingly shining on these companies and their vital role in supporting a fintech industry that a growing number of financial services customers – and other businesses – are relying on.

The review cited research from KPMG that anticipates regtech spending in 2022 climbing to $76 billion. Analysis from XAnge, a European VC firm, finds approximately 140 regtech startups in the E.U., divided fairly equally between compliance management, KYC/AML, and risk management solutions.

We were especially please to see that, of the ten regtech startups highlighted in the feature, four of the companies are Finovate alums. Apiax and NetGuardians, which most recently demoed at FinovateEurope and at FinovateAsia respectively, both hail from Switzerland. Apiax, recently profiled here on the Finovate blog, offers a comprehensive compliance solution that leverages APIs to integrate its compliance rules into digital processes. NetGuardians focuses on Big Data and uses it to help banks fight fraud and automate compliance.

Also earning recognition on the top European regtech list was Ireland’s Fenergo. The company, founded in 2009 and having made its Finovate debut back in 2012, specializes in client onboarding and account opening solutions for banks and financial services companies. Just this week, Fenergo announced that it was launching a new remote account opening solution in both the EMEA and APAC regions.

Half of the companies on Fintech News’ regtech roster are from the U.K. The Finovate alum among this group, Onfido, leverages automated machine learning, optical character recognition (OCR), and other technologies to provide identity verification to combat fraud. Demoing its technology at both FinovateEurope and FinovateFall in 2018, the company earlier this month announced a major $100 million fundraising that brought the company’s total capital to more than $182 million.

“We’ve naturally chosen the grow-fast path because we strongly feel that the time to solve the digital access problem is overdue, and urgently needs to be solved, for good,” Onfido CEO and co-founder Husayn Kassai said. “We didn’t fundraise to just get to the next milestone, we need the funding as we’re changing the world.”

The Buy Now Pay Later Revolution is sweeping the world. Check out Finovate Senior Research Analyst Julie Muhn’s coverage of Tencent’s $300 million investment in Australia-based Afterpay this week:

Tencent’s move comes shortly after its rival Ant Financial took a minority stake in Afterpay competitor Klarna. Afterpay has 3x the web traffic of Klarna and 1.5x the traffic of its other major competitor Affirm.

The buy-now-pay-later segment of fintech has been heating up this year, despite– or perhaps because of– the current economic and health crises.

Here is our weekly look at fintech around the world.

Asia-Pacific

V Capital, and advisory firm based in Malaysia, and U.S.-based Cross River Bank partner to apply for a digital banking license in the country.

Hong Kong-based Oriente, a fintech that provides digital infrastructure for financial services, secures $50 million in its still-open Series B round.

South Korean cryptocurrency startup Childly teams up with blockchain analysis company Chainalysis.

Sub-Saharan Africa

Nigerian fintech startup Okra, which facilitates the exchange of real-time financial between banks, customers, and apps, locks in $1 million in pre-seed funding in a round led by TLcom Capital.

Flutterwave, based in San Francisco, California and Lagos, Nigeria, introduces new portal for African e-commerce merchants.

Visa and Kenya’s Pesapal team up to support connected digital payments.

Central and Eastern Europe

Resistant AI, a cybersecurity startup based in the Czech Republic, raises $2.75 million in funding.

Azer Turk Bank (ATB), based in Azerbaijan, deploys technology from Lithuania’s Ashburn to manage EFTPOS networks.

Germany’s Celonis leverages its process mining platform to develop new AI-powered accounts payable solution.

Middle East and Northern Africa

Egypt’s Commercial International Bank acquires 51% stake in Kenya’s Mayfair Bank.

BenefitPay, Bahrain’s national electronic wallet, announces 1257% increase in remittance volume in March.

Tata Consultancy Services to launch a digital only bank in Israel.

Central and Southern Asia

Indian cryptocurrency exchange CoinDCX announces trading availability of two native tokens from Crypto.com, MCO and CRO, on its platform.

Amazon launches new credit service, AmazonPay Later, in India.

India-based ecommerce firm Paytm unveils contactless dining solution for restaurants in the coronavirus era.

Latin America and the Caribbean

paysafecard brings its payments platform, Paysafe, to Paraguay.

Latin Post looks at the use of fintech apps in Mexico.

After ten years in the investment space, online brokerage platform Motif will be shutting down operations on May 20.

The company notified users via email on April 17 in a message saying, “At this time, we’ve made the decision to cease operations and transfer your account to Folio Investments.”

Motif was founded in 2010 by Tariq Hilaly and former Microsoft executive Hardeep Walia, who debuted the company’s build-your-own motif concept at FinovateSpring 2013. Since its launch, the company amassed $127 million in funding from investors including Y Combinator, TechStars, and 500 Startups. In March, Motif reported $604 million in assets under management between individual accounts and institutional clients. The company also reported around $264 million in assets held in the ETFs it launched in conjunction with Goldman Sachs.

Last month, Motif deepened its ties with Goldman Sachs, ringing the opening bell of the New York Stock Exchange in celebration of launching five new ETFs in partnership with the bank.

As mentioned in Motif’s statement to its users, the company is transferring users’ accounts to Folio Investing. “We appreciate the opportunity we’ve had to work with you, and we are confident that your investment needs will be well-served by Folio,” the email said. Folio was founded in 2010 and offers 2,000 commission-free, window trades per month, most of the ETFs listed on the U.S. national securities exchange, 1,100 no-load mutual funds, and almost 125 pre-made portfolios.

While some Motif users have publicly complained about the company’s choice in the new provider, some fintech firms, including M1 Finance, have taken the opportunity to bring Motif’s users over to their platforms.

As ThinkAdvisor noted in a piece published last week, Motif’s news is a signal of what’s to come for smaller players in fintech. In fact, many analysts have noted that the recent pandemic and economic crisis will drive consolidation in the industry.