This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

The collaboration, announced late last month, will provide access to Rize’s banking infrastructure and compliance program. Both current and new clients also will be able to securely link bank accounts from 16,000+ financial institutions and fintechs by way of MX’s data connectivity network, which leverages machine learning to clean and enrich transaction data.

“Our partnership with Rize is all about developing new financial products and services through one API,” MX EVP of Partnerships Don Parker said. “By cutting the associated time and costs of development, we’ll open up MX functionality to a wider range of fintech companies and organizations already working to improve financial strength and access to quality financial tools.”

Powering 85% of digital banking providers and thousands of banks, credit unions, and fintechs, MX most recently demonstrated its technology on the Finovate stage last fall in New York for FinovateFall. At the conference, the multiple-time Best of Show winner showed its Open Finance portal that improves the data sharing experience between providers and recipients for the benefit of the customer. The technology relies on modern, token-based connectivity to give financial institutions the ability to monitor and manage how customer data is shared.

In the months since its appearance at FinovateFall, MX has forged partnerships with Deposits.com to promote financial inclusion in underbanked communities, and with H&R Block, where the Lehi, Utah-based fintech will help the tax preparer provide customers of its Spruce mobile banking platform with greater transparency. In February, MX teamed up with Cadence Bank, a regional financial institution based in Tupelo, Mississippi with more than $50 billion in assets and 400+ branches in the American South, Midwest and in Texas. MX began the year with the appointment of Shane Evans as Interim Chief Executive Officer. Evans took over the top spot from MX founder Ryan Caldwell, who transitioned to the role of Executive Chair.

Open banking platform Tink partnered with Irish postal services provider An Post.

Tink will provide data and analytics that fuel An Post’s Money Manager app.

The new partnership serves as an inroad for Tink into the Irish market.

Visa-owned open banking platform Tink formed a new partnership this week that will bring its open banking capabilities to users of Irish postal services provider An Post.

An Post, which offers not only parcel and mail logistics but also financial services, operates a network of 920 post offices for its 1.5 million weekly customers. An Post offers many of the major services typical of high street banks, including current accounts, savings accounts, credit cards, loans, and a currency card that allows users to purchase and top up 16 currencies.

Leveraging Tink for data and analytics, An Post now delivers a Money Manager app that helps users track their income and spending, set budgets, and receive insights about how they can better manage their funds.

“The partnership with Tink is the next step in our transformation journey, to firmly position ourselves as a challenger to the banks in Ireland, and to give customers access to simple money management tools that will enable them to build their financial confidence,” said An Post Financial Services Director John Rice. “As the leading open banking platform in Europe, Tink was a clear choice of partner for us to provide the data and analytics that sit at the core of our Money Manager app.”

For Sweden-based Tink, the partnership with An Post serves as an important inroad into the Irish market. “An Post is in the perfect position to help simplify money management for its customers through the power of open banking technology,” said Tink UK & IE Banking Lead Tasha Chouhan.

More than 10,000 developers use Tink’s tools to help financial services firms leverage the power of open banking via a suite of open banking tools including income verification, payment tools, risk insights, and more. Tink currently serves 18 markets from its 13 offices and integrates with more than 3,400 banks and financial institutions reaching over 250 million end customers across Europe.

Founded in 2012, Tink is a two-time Finovate Best of Show Award winner, and most recently demoed at FinovateEurope 2019. The company acquired FinTecSystems earlier this year, a move that expanded Tink’s reach into the DACH region with a range of new customers including N26, DKB, Santander, Solarisbank, and Check24.

Michigan-based banking solutions provider Bankjoy announced 16 new credit union partners.

Combined, credit unions represent more than 350,000 members and more than $3.3 billion in assets

The partnership news follows the company’s launch of a new small business banking platform.

Digital banking solutions provider Bankjoy has added 16 credit unions to its digital service ecosystem. The new partners combined represent more than 350,000 members and more than $3.3 billion in assets. Additionally, they serve members in states ranging from New Mexico, Texas, and Nevada, to Ohio, Illinois, and Alaska.

The credit unions newly partnering with Bankjoy include:

Cooperative Teachers Credit Union

Directions Credit Union

Elko FCU

Estacado FCU

Firelands FCU

Fremont FCU

Glass City FCU

Impact Credit Union

Las Colinas FCU

Lone Star Credit Union

Midwest Community FCU

OU FCU

Streator Onized Credit Union

Trius FCU

True North FCU

Pyramid FCU

“Credit unions like Estacado, Cooperative Teachers Credit Union and others are partnering with fintechs like Bankjoy to provide modern digital banking platforms that keep pace with members’ needs,” Bankjoy CEO Michael Duncan said. He highlighted growth in deposits in credit unions across the country, adding “as these trends continue, we’re adding more credit unions to our platform and look forward to helping them deliver a superior experience.”

Bankjoy’s partnership news comes in the wake of the company’s addition of a modern business banking platform to its offering. The platform, introduced in December, gives banks the tools its small business customers need and include solutions for invoicing, payroll, company formation, wire transfers, and entitlements.

Headquartered in Detroit, Michigan, and founded in 2015, Bankjoy also reported late last year that it had been chosen as the first official Corelation Certified Partner. The partnership enables credit unions who use Corelation’s Keystone core to efficiently integrate with Bankjoy. It also makes it easy for Bankjoy’s credit union partners to migrate their core to Corelation without disrupting the member experience.

“To support the credit union movement, it is critical for fintechs to partner with likeminded organizations who are committed to a member-centric approach,” Duncan said. “Our collaboration with Corelation has been incredibly successful, delivering tremendous value to credit unions.”

A Finovate alum since 2016, Bankjoy has raised $1.8 million in funding from investors including SixThirty and CheckAlt.

Consolidation in the Buy now, pay later (BNPL) industry continues as Zip agrees to acquire competitor Sezzle.

The deal values Sezzle at $355 million.

After the acquisition is finalized, Sezzle will rebrand to Zip and the company’s CEO Charlie Youakim will lead Zip’s U.S. business.

Buy now, pay later (BNPL) player Zip (formerly known as Quadpay) is acquiringSezzle in a deal that values Sezzle at $355 million.

Zip CEO and co-founder Larry Diamond expects the deal will help Zip scale up its operations. “Combining with Sezzle positions us as a leading global BNPL provider and prioritizes our ability to win in the important U.S. market.”

Following the deal, Zip’s customer base will increase from 9.9 million to 13.3 million and the number of merchant partners will grow from 82,000 to 129,000. Additionally, The Financial Review estimates that Zip’s total transaction volume will rise from $8 billion to $10.4 billion, and that almost $6.5 billion of this will be from U.S. users.

After the deal closes, Sezzle will rebrand as Zip and the company’s CEO Charlie Youakim will lead Zip’s U.S. business. “I believe the transaction will position us to win in the U.S. and globally,” Youakim said.

Today’s announcement is yet another indication of consolidation in the increasingly-crowded BNPL space. Industry giant Afterpay sold to Block (formerly Square) on February 2nd. And on February 17th, digital payments firm Latitude agreed to acquire Humm’s BNPL operations.

Australia-based Zip was founded in 2013, seven years before BNPL took off as an alternative payment method. Zip is publicly traded on the Australian Stock Exchange (ASK) under the ticker ZIP. The company allows users to split their purchase into four installments over the course of six weeks. With Zip’s app, shoppers use their Zip Virtual Card to pay for their purchase in installments anywhere that Visa is accepted, both online and in-store.

Similarly, Sezzle allows shoppers to use their Sezzle Virtual Card to pay for purchases in four installments over the course of six weeks. The company also offers a long-term financing tool in partnership with Ally and Sezzle Up, an alternative credit solution that helps shoppers build their credit.

Minnesota-based Sezzle was founded in 2016 and went public on the ASK in 2019 under the ticker SZL. At the time, Sezzle said it opted to list on the ASX instead of in U.S. markets because, prior to 2020, the BNPL model was more commonplace in Australia, given that Afterpay, a major player in the BNPL arena, is headquartered in Melbourne.

TransUnion launched Point-of-Sale Suite of Capabilities to provide lenders insight into consumer borrowing habits with point of sale lending and buy now, pay later products.

The new data reporting helps lenders underwrite credit risk.

The reporting methods also benefit the consumer by not penalizing them for using these alternative credit products on a regular basis.

Financial insights firm TransUnionlaunched a new set of tools today that will help shoppers using point-of-sale (POS) loans, including buy now, pay later (BNPL), improve their credit scores while offering lenders a more holistic view of prospective borrowers’ risk.

TransUnion’s Point-of-Sale Suite of Capabilities offers lenders insight into the payment behaviors of consumers using alternative credit tools such as POS lending and BNPL products.

This increased data reporting and visibility helps lenders underwrite credit risk, but also benefits the consumer by not penalizing them for using these alternative credit products on a regular basis. That’s because POS and BNPL loans are underwritten as unsecured installment loans. When these installment products are used frequently, typical credit models could view the borrowing behavior as risky.

“The inclusion of point-of-sale loans including BNPL into credit reports and other risk management tools can help tens of millions of consumers gain access to more credit opportunities and potentially secure better loan terms,” said Liz Pagel, senior vice president and consumer lending business leader at TransUnion. “TransUnion has taken a measured approach in developing our solution suite, working with the top BNPL lenders over the past three years to craft solutions that benefit consumers and do not penalize them for using these products frequently.”

TransUnion’s new toolset aims to offer lenders a single standard to report this alternative borrowing data. In order to minimize unnecessarily negative impact on the consumer credit score while still communicating valuable borrowing and repayment data, POS and BNPL borrowing information will be tagged and filtered into a new section in TransUnion’s core credit file.

“Maximizing the financial inclusion impact requires broad usage of this valuable data in more credit decisions. Ultimately, given the prominence of FICO and VantageScore in the market, the biggest impact from the data will not be realized until the data migrates to the core file and these scores take into account consumers’ good behavior,” added Pagel.

The use of BNPL is becoming more commonplace as more retailers and payment companies adopt varying versions of the technology to encourage higher consumer spending. In fact, according to a recent TransUnion study, up to 100 million U.S. adults have used BNPL loans at least once in the past 12 months. As this growth continues, lenders will need to adjust their underwriting models to account for use of alternative lending technologies.

New York-based Signal Intent has rebranded as Chimney.

The company won Best of Show in its Finovate debut at FinovateSpring last year.

The rebrand announcement accompanied news that Chimney had raised seed funding that “exceeded its investment goals.”

Signal Intent, which won Best of Show in its Finovate debut at FinovateSpring 2021, has rebranded as Chimney. The company develops financial calculators for banks, credit unions, insurers, and mortgage companies that are “built for the digital age.” The New York-based fintech’s rebrand, announced last month, was accompanied by a seed investing round with participation from individual investor Anil Aggarwal, as well as investment firms Fin VC, and Converge.

“Banking is fundamentally changing as consumer behaviors shift,” Chimney CEO Matthew Covi said. “To compete, banks must change their digital strategy. It is no longer about providing outstanding products and services. It’s about the value they provide through digital experiences. As consumers increasingly make financial decisions online, they expect experiences that are embedded in their everyday life. Chimney is committed to delivering not just the products consumers want, but the experiences they expect.”

More than 60 financial institutions in 30 states use Chimney’s financial tools and technology to better engage their customers and fund more loans. The company said that its financial institution clients have experienced a 15% boost in conversions since deploying Chimney’s technology that helps connect customers to the right solution at the right time. Chimney also helps FIs reduce acquisition costs while growing their loan portfolios.

Selected for the 2022 ICBA ThinkTECH Accelerator program, Chimney plans to add to its team, including multiple “key positions” over the next several months. The company’s co-founders include Chief Technology Officer Ryan F. Salerno, former Technical Co-founder of equity management platform Finta (previously Equity Token); and Chief Revenue Officer Chase Neinken, former VP of Global Sales at B2B media company Industry Dive.

“We created Chimney to build the future of financial guidance,” Neinken said. “We believe in a world where people are empowered to make better financial decisions through technology – it’s about confidence and understanding. The demand so far has exceeded expectations and we’re thankful to our clients, partners and investors. Big things are coming ahead.”

FinovateEurope 2022 is less than a month away, and innovative fintechs from all around the world are gearing up to demonstrate their latest technologies live on the Finovate stage. Find out more about our annual European fintech conference, including how to register and save your spot as Finovate returns to live events in Europe for the first time since 2020 next month on March 22 and 23.

One of the goals of every company demoing their solutions at Finovate is to win a coveted Best of Show award. This honor is granted exclusively by our Finovate attendees who evaluate every company on stage and select only those innovators whose technology is most impressive and, potentially, impactful. To give you a sense of the kind of companies to win this award, here’s a look at the FinovateEurope Best of Show winners from the previous two years – as well as an update on what they’ve accomplished since winning their award.

2021

Dbilia earned a Best of Show in its Finovate debut at FinovateEurope 2021 for its platform that enables creatives and influencers to sell digital memorabilia. The New York-based company was featured in the July edition of MarTech in a look at the rising NFT trend.

Property investment platform Proptee, also a Best of Show winner in its Finovate debut last year at FinovateEurope, raised more than $57,000 in seed funding in December from Lebenheim Capital and Steep VC.

Continuous product design innovator Quantum Metric was among the Finovate newcomers to earn a Best of Show award at FinovateEurope 2021 last March. Since then, the Colorado Springs, Colorado-based company has announced the availability of its solution on Salesforce AppExchange, and forged partnerships with Korea Air, iGaming operator BetVictor, luxury fashion brand La Perla, experience management software company Qualtrics, and video-based human insight innovator UserTesting.

2020

If 2021 was the year Finovate audiences showed their appreciation for conference newcomers, 2020 marked the year when veteran Finovate alums earned their place in the spotlight. Four of the companies that won Best of Show at FinovateEurope in that pre-pandemic year – Dorsum, Glia, iProov, and W.UP – picked up their second awards in a row (or more) having taken home Best of Show honors at the previous year’s conference in 2019.

Digital customer service innovator Glia has been one of Finovate’s most popular demoing companies in recent years, with multiple Best of Show wins in Europe and in the U.S. Earlier this month, the company announced a partnership with insurtech leader Sureify, integrating its capabilities into Sureify’s Lifetime platform. In 2021, Glia reeled in $78 million in funding, and earned recognition from Deloitte with a spot on the firm’s Technology Fast 500 for the second consecutive year. Among the company’s new partnerships forged in 2021 were collaborations with Kasisto, Posh, Apiture, Liberty Bank, fellow Finovate alum Clinc, and Zensar.

Horizn, which specializes in helping financial institutions and their employees maximize and accelerate their digital transformation efforts, earned the first of its Best of Show awards at FinovateEurope in Berlin in 2020. The company announced a partnership with Pacific Western Bank at the beginning of this month, powering the Los Angeles, California-based financial institution’s newly launched digital learning platform.

Biometric authentication company and FinovateEurope veteran iProov earned its third Best of Show award at our European fintech conference in 2020. The company secured $70 million in funding from Sumeru Equity Partners to start this year and, earlier this month, was granted a patent to extend its Genuine Presence technology to include driver’s license and government ID verification. Named to the Deloitte Fast 50 of the fastest growing technology firms in the U.K. last year, iProov reported a record 2021 in which the company achieved revenues that were 3x the previous year’s results.

Sonect demonstrated its global platform for cash transactions during its Finovate debut in Berlin in 2020, winning a Best of Show award. The company, headquartered in Zurich, Switzerland, enables users of its technology to withdraw cash via smartphone at any one of its 2,500 partnering retailers. Last summer, the company announced that its service would be available to customers in the U.K., following its participation in the U.K. Finance Community Access to Cash Pilots Initiative. In October, Sonect announced that it had raised more than $5 million (EUR 4.65 million) in funding from Italian Angels for Growth to bring its cash access solution to Italy.

Budapest, Hungary-based digital banking solution provider W.UP is another FinovateEurope favorite, having been awarded Best of Show in each of the last three FinovateEurope events. The company offers a personalization platform which leverages data to help institutions offer better banking services. In October of 2021, the company merged with BSC of Czechia to form a new company Finshape that is dedicated to driving digital transformation in banking in Europe.

OCR Labs, an identity verification company founded in Australia and headquartered in London, announced a $30 million Series B round.

The funding takes the company’s total capital to $46 million and will be used to help OCR Labs expand further in North America and EMEA.

Making its Finovate debut in 2016, the company won Best of Show at FinovateAsia a year later.

In a round led by Equable Capital, a New York-based family office, identity verification specialist OCR Labs has raised $30 million in a Series B round. The investment will be used to help the London, U.K.-based company grow its team in North America and EMEA, and gives the firm $46 million in total capital.

“2021 was an incredible year for OCR Labs, with continued validation from customers who have chosen us as their provider for online digital identity verification,” OCR Labs CEO John Myers said in a statement. “This investment provides us with the capital to continue our growth while bringing a value-added investor on to our board.”

Boasting a 5x increase in new clients and 3x growth in the size of its team over the past 12 months, OCR Labs offers automated identity verification via ID document validation, facial biometrics and other techniques. OCR Labs’ approach removes the need for human intervention in the customer identification process, and gives companies the tools they need to meet AML and KYC requirements and reduce fraud.

The company made its Finovate debut at our developers conference FinDEVr Silicon Valley in 2016 and returned one year later to win Best of Show at FinovateAsia in Hong Kong. Securing Series A funding last year, OCR Labs also recently opened a new office in North America, added a direct sales force, and hired a global Chief Revenue Officer.

“Our vision remains unchanged,” Myers said, “we strive to be the leading technology provider of digital identity verification, globally. The market opportunity continues to grow, and with our expansion in the U.S., and investment in our global sales effort, we’re in a phenomenal position to grow our customer base.”

The first private company to earn accreditation as an identity provider under the Trusted Digital Identity Framework (TDIF) of the Australian government, OCR Labs serves customers in a wide variety of verticals including financial services companies, brokerages, insurers, telecoms, and gaming companies.

If making a great first impression is important, then Virgin Money’s decision to partner with customer onboarding and KYC technology specialist HooYu should make a pretty good impression of its own.

“Our smart digital tools put our customers in control and the HooYu journey helps our customers to successfully pass KYC where traditional name and address checks fail,” Virgin Money Head of Digital Customer Experience Linda Robertson said. “We chose to work with a regtech partner like HooYu because their platform enables us to easily build a range of digital onboarding journeys that are simple for our new customers to complete.”

A two-time FinovateEurope alum, HooYu combines a variety of KYC tools and technologies to ensure the success of the customer onboarding journey. This includes giving companies confidence that their customers are who they say they are. HooYu’s identity verification service leverages selfie capture, liveness detection, ID document capture and validation, facial biometrics, address proofing, and geolocation in a seamless process that reduces abandonment and increases conversions. Features such as dynamic customer prompts, white label customization, and flexible customer journeys help reduce friction and streamline the account opening experience.

Calling the emphasis on the digital customer experience an “obsession” with banks like Virgin Money,” HooYu Marketing Director David Pope said it was HooYu’s role to help these institutions “refine their new account journeys and achieve the origination goals.”

Virgin Money serves 6.5 million customers in the U.K. A full-service digital bank, the institution offers current, savings, and business accounts; credit cards and insurance; mortgages and personal loans; as well as pensions and investments. Originally launched as Virgin Direct in 1995, the company secured its banking license 2010 and rebranded as Virgin Money two years later.

“It’s our job to help banks like Virgin Money to orchestrate KYC services and easily configure and deploy with a great customer journey,” Pope said.

Founded in 2015 and headquartered in London, U.K., HooYu began the year by leveraging open banking to support identity and affordability checks. The new offering, Bank Connect, enables users to establish their identity or affordability by logging into their bank account during the KYC process. With the user’s consent, Bank Connect provides identity, account overview, transaction, and card data. This information is analyzed, scored, and presented in a HooYu report. HooYu deletes all the user’s Bank Connect data once the client has reviewed the results of the report.

The technology is currently being rolled out to gaming operators, who benefit from the insights into customer affordability and use the information to make more accurate customer risk assessments. In fact, one month after announcing Bank Connect, HooYu introduced new partner MrQ, one of the U.K.’s growing number of online casinos.

Want to meet companies like FinovateEurope alum HooYu? Check out our FinovateEurope 2022 Sneak Peek series and learn more about the companies demoing their latest technologies next month at FinovateEurope in London, March 22 and 23.

Savings app Plinqit has raised $5 million in Series A funding, bringing its total capital to nearly $10 million.

The technology helps users save safely and efficiently, and offers rewards for users who improve their financial literacy by engaging in educational content via the app.

Plinqit was founded in 2015 by CEO Kathleen Craig

Michigan-based savings app Plinqit has secured $5 million in funding this week. The company, which made its Finovate debut in 2019 at FinovateFall in New York, will use the new capital to help scale the business to meet growing demand. The Series A round brings Plinqit’s total capital to just under $10 million.

“Financial wellness is crucial for all of us in financial services,” Plinqit founder and CEO Kathleen Craig said. “We created Plinqit to help builders create solutions that truly help people in a way that is engaging and rewarding. It was critical for us that it was technology that they would want to use – and they are.”

The round was led by Nashville, Tennessee-based Fintop Capital and New York’s JAM FINTOP. Also participating in the investment were Invest Detroit, Michigan Rise, and Michigan’s 4Front Credit Union.

Plinqit is a brandable, mobile-first savings app – built by Millennials for Millennials. The platform empowers users to create up to five savings goals, and begin setting aside funds for each goal while earning rewards. The app’s Build Skills feature not only helps users develop financial literacy, it also pays them for doing so, rewarding users for engaging with content which boosts user engagement for financial institutions that offer the technology. Plinqit also offers a virtual account management system – Vi.Ledger – which enables financial institutions to build their own custom savings programs using virtual accounts within the app.

Launched in 2015, Plinqit is one of the leading solutions offered by app development company, HT Mobile Apps (HTMA). The technology has been adopted in recent years by a number of community financial institutions including The Milford Bank ($482 million in assets), ChoiceOne Bank ($244 million in assets), and First Arkansas Bank & Trust ($760 million in assets). “We created Plinqit as a tool to not only help customers safely and securely meet their savings goals, but to also help financial institutions compete for deposits and develop deeper relationships with their customers,” Craig said when the partnership with First Arkansas Bank & Trust was announced in the summer of 2020.

Last fall, Plinqit announced an integration with the digital banking platform of fellow Finovate alum Q2. Funds saved on the Plinqit app are FDIC- or NCUA-insured, and the service is free to users.

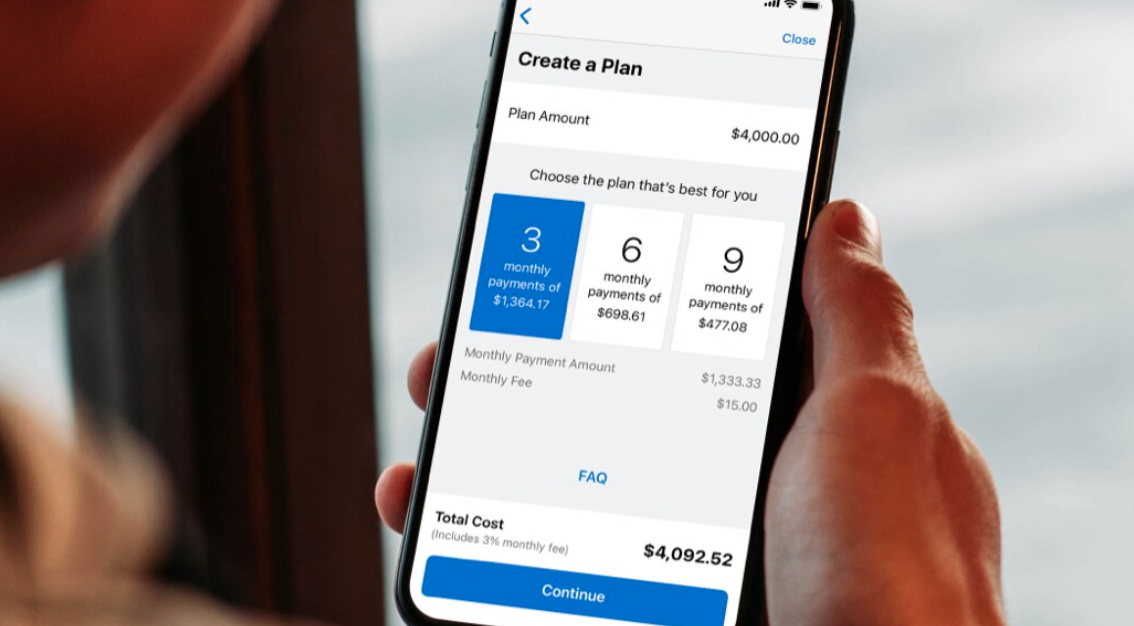

American Express partnered with Delta Air Lines to offer American Express’ buy now, pay later tool, Plan It, as a payment option at checkout.

Plan It allows users to select from one to three repayment options and charges a fixed monthly fee.

Plan It will be added as a checkout option on Delta’s mobile app this spring.

American Express and Delta Air Linespartnered this week to offer their shared customers a buy now, pay later (BNPL) option when booking flights on Delta.com’s web interface.

The partnership, which leverages American Express’ Plan It tool, enables American Express U.S. consumer card members to split up purchases of over $100 into equal monthly installments with a fixed fee.

Launched in 2017, Plan It allows customers to select from one to three repayment options, depending on factors such as the purchase amount, the cardholder’s account history, and their creditworthiness. Plan It charges a fixed monthly fee that is disclosed before the transaction.

As an added advantage over other BNPL plans, Plan It is built into the American Express card and does not require users to enroll, plus cardholders earn rewards as they usually do with their card payment. Further, cardholders do not need to keep track of additional payments, since they are included in their monthly statement.

As Anthony Cirri, Executive Vice President for Global Consumer Lending and Cobrand at American Express highlighted, the timing of the partnership is ideal. “It’s the perfect time to bring these together as people are booking long-awaited trips, and our card members can book with confidence knowing they are backed by the strong partnership between Delta and American Express.”

Plan It has benefited from the rising popularity of BNPL and alternative payment options. The volume of new plans originated in the fourth quarter of 2021 was more than double the volume in the fourth quarter of 2020. And 65% of plans originated in the last year were from new users.

Travelers will see Plan It as a checkout option on Delta’s mobile app this spring.

Backbase has forged a new partnership with New England-area financial institution, Eastern Bank.

Eastern Bank will leverage Backbase-as-a-Service and Backbase Digital Sales technology to streamline its new account opening process, as well as create and release new financial products and services.

With $24 billion in assets and more than 120 locations, Eastern Bank serves customers in eastern Massachusetts, southern and coastal New Hampshire, and Rhode Island.

A new partnership between engagement banking innovator Backbase and Eastern Bank will bring a fully digital account opening experience to the Boston-based financial institution’s customers. Eastern Bank ($24 billion in assets) will deploy both Backbase-as-a-Service and Backbase’s Digital Sales solutions, which will give Eastern the technical infrastructure it needs to create and deliver new products and services faster.

The deployment of Backbase’s Digital Sales solution will enable Eastern Bank to combine Backbase’s out-of-the-box accelerators and integrations with solutions from third-party fintechs to offer their customers personalized digital banking services – as well as remove much of the complexity customers encounter when opening new accounts. Eastern Bank expects to offer Backbase’s Digital Sales capabilities in the first half of this year to new retail customers. The bank’s new commercial and business banking customers can expect a similar offering later in 2022.

“We are thrilled Eastern Bank chose to collaborate with us around this commitment to technology and innovation,” SVP of Americas at Backbase Vincent Bezemer said. “Like us, they are passionate about delivering the best digital experience possible for customers.” Bezemer complimented Eastern Bank’s team as “agile and digitally-focused” as well as having a “human-centered approach” to collecting and incorporating customer feedback to ensure high-quality customer experiences.

Founded in 1818, Eastern Bank offers banking, investment, and insurance products and services for retail consumers and businesses in parts of Massachusetts, New Hampshire, and Rhode Island. The bank earned the 2021 Impact Innovation Award for Artificial Intelligence and Advanced Analytics by Aite-Novarica Group and was a finalist in the Best Small Business Banking Solution category at the 2021 Finovate Awards.

A multiple-time Finovate Best of Show winner, Backbase is one of Finovate’s oldest alums, having made its debut on the Finovate stage in 2009. More recently, the company participated in Finovate’s return to live events last September as part of FinovateFall in New York. At the conference, Backbase demonstrated its complete customer onboarding technology that consolidates customer finances via direct deposit, billpay auto linking, and debit card account opening.

Founded in 2003 and headquartered in Atlanta, Georgia, Backbase was named “Best in Class” among digital banking platform vendors in Javelin’s 2021 Digital Banking Platform Scorecard. In addition to its partnership with Eastern Bank, Backbase has collaborated in recent months with Wyoming-based Blue Federal Credit Union and St. Louis, Missouri-based, family-owned First Bank.