This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Envestnet | Yodlee, Quovo, and Morningstar Unite on Secure Open Data Access Framework.

Around the web

nCinoextends its Bank Operating System with its new Retail Sales and Service Solution.

Fenergo to bring client lifestyle management services to business and technology consultancy, Delta Capita.

ProfitStars division of Jack Henry & Associates goes live with its ImageCenter Express image capture solution.

Flywireadds international invoicing to its global payment and receivables platform.

Infosys Finaclepartners with seven major Indian banks to form blockchain-based trade network, India Trade Connect.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

FinovateSpring was a hotbed of future-looking technology. We spoke to Theo Lau, Innovator Technologist and Connector, Unconventional Ventures about why she thinks voice is the next UI.

Although voice may not a solution for all situations, there is no denying that the momentum and interest for voice technology is growing. In the Q3 2017 earnings report, Amazon disclosed that it has sold “tens of millions of Echo units” since the first release in 2015. According to “The Rise of Voice” report by Invoca, the voice opportunity is predicted to be worth more than $18 billion by 2023. Consumers have been using voice assistants from seeking information to playing music and shopping. Accessibility, convenience, and simplicity are some of the main reasons behind the user adoption. For those who cannot read or who may have trouble navigating the menu options on an app or website, ability to speak to a device offers a more intuitive option to obtain real-time information. Voice technology is also life-impacting for those suffering from isolation/loneliness. In all, it has the potential to become a more inclusive technology that can appeal to a board audience and serve a wide purpose.

Recognizing the potential and appeal, financial institutions such as Capital One, USAA, Bank of America, U.S. Bank, and Ally Financial have begun experimenting with various use cases. Applications thus far are still fairly rudimentary and focused on basic interactions such as checking balance, paying bill, and tracking spending.

Though voice banking is still at its infancy, the industry is quite bullish on its future. Capgemini predicts that 3 years from now, 40 percent of consumers will use voice assistants rather than website or app, and 31 percent will use a voice device instead of visiting a store or branch. Separately, Medici forecasts that approximately 1.83 billion customers will be using voice assistants by 2021. Financial institutions should leverage insights harnessed from these interactions to adapt the conversation to reflect their brand identity and user’s profile. As suggested by Mark Taylor from Capgemini: “A brand today is an image, a set of colors, something you see on TV, on a website or in a store. With a voice channel, you see nothing, so a brand needs to have an audible image.”

While we might not be at the “promise land” yet where the virtual assistants become truly conversational, we have made great strides. As with any technology, empathy is key. AI and voice technology has the potential to make businesses more human, allowing banks to truly focus on their customers and become their true partners.

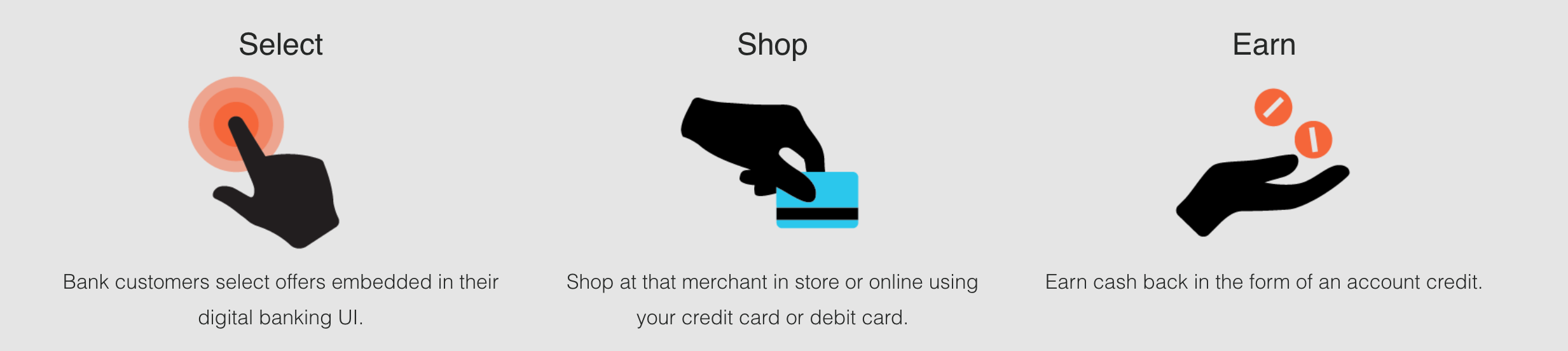

“We are pleased to announce the signing of an agreement for a national launch with JPMorgan Chase,” said Lynne Laube, COO and co-founder of Cardlytics. “The addition of Chase to the Cardlytics Purchase Intelligence platform will further strengthen our ability to provide powerful, actionable insights for our marketer clients and then act on these insights at scale.”

Cardlytics’ Purchase Intelligence platform is a loyalty program that banks implement with their existing debit or credit cards. Customers receive personalized offers and cash-back savings based on their transactions. This increases average consumer spend, boosts merchant loyalty, and drives more engagement within the bank’s online and mobile banking.

Chase joins a host of other banks and financial services companies already leveraging Purchase Intelligence, including PNC, Regions, SunTrust, Bank of America, Fiserv, FIS, and Digital Insight. David Evans, CFO of Cardlytics, said, “With the announcement that Chase will be coming onto our platform, we are very excited about the longer-term prospects for the business.”

Cardlytics’ primary offering is Cardlytics Direct, a native bank advertising channel that enables marketers to reach consumers through online and mobile banking channels. The service has more than 2,000 bank clients in the U.S. and appeals to bank customers by offering cash back on select purchases. In fact, Cardlytics has paid more than $230 million in consumer rewards to date.

At FinovateFall 2013, Cardlytics demoed its geolocation application, a solution that sends bank customers ads and offers based on their location. Making its public debut on the NASDAQ in February, the company has put forth strong growth for shareholders. In the first quarter of this year, Cardlytics’ total revenue was $32.7 million, an 22% YoY increase, and its direct revenue was $32.1 million, a 31% YoY increase.

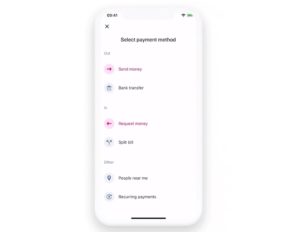

Thanks to Revolut’s latest solution, Near Me, Revolut users will be able to send and request money from more than just the people they know well. The company’s latest feature leverages geolocation technology to enable users to split bills and send money to any other active Revolut user in the area.

“Until now, you would need to have the person you want to split the bill with added as a contact in your phone,” Revolut’s Chief Blogging Officer Rob Braileanu explained in a blog post today. “And while this is great for your close friends and family, what if you don’t know the person that well?”

To use the new feature, users with the latest version of the Revolut app select the People Near Me option from the Payments tab. Enable Near Me and choose your location sharing preferences. When the list of Revolut users appears, make your selection, choose “send” or “receive” and confirm the amount. Note that the person or persons on the other end of the transfer will need to have their Near Me screen open and select their location sharing preferences, as well.

Supporting 25 currencies and three cryptocurrencies, Near Me is the latest solution from a company that has been prominent in the fintech headlines of late. Last month, the company introduced a new savings solution, Vaults, that enables users to turn their spare change into savings in cash or crypto. In March, Revolut launched disposable virtual cards for online payments and, in January, the company added travel insurance to its offerings, leveraging geolocation to automatically turn coverage on and off when users leave and return to their home countries.

But the big splash for Revolut was the $250 million in funding the company picked up less than a month ago. The DST Global-led round sent Revolut’s valuation soaring to $1.7 billion, making the firm the first digital bank in the U.K. to earn unicorn status (valuation above $1 billion).

Founded in 2015 and headquartered in London, U.K., Revolut demonstrated its Personal Money Cloud at FinovateEurope 2015. Nikolay Stronosky is CEO.

RevolutIntroduces New Payment Sharing Feature, Near Me.

Around the web

FinTech Breakthrough namesCloud Lending SolutionsBest Business Lending Platform.

Payoneerannounces new investment and support for cross-border U.S. SMEs.

eToro to launch cryptocurrency offering in the U.S., initially enabling investors to buy and sell 10 cryptocurrencies.

UnikenearnsCool Vendor in Identity and Access Management recognition from Gartner.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Coming into effect on May 25th, GDPR represents a significant sea change in terms of data privacy and data protection and designed to harmonize data privacy laws across Europe, to protect and empower all EU citizens data privacy and to reshape the way organizations across the region approach data privacy. This webinar provides actionable guidance on how to determine if your selected data processors are, in fact, fully compliant, how processes have been vetted and guiding you to ask the right questions in order to provide you a little peace of mind. Hearfrom Jumio, Fintrail and leading banks discuss the challenges – and opportunities – of GDPR within the digital identity sector.

Today’s customers demand that every experience provide immediate value on multiple levels. They require a competitive, friendly, quick and personalized user experience. They swear allegiance to no brand and are ready to jump ship to the first competitor that can offer them what they want, when they need it, and at the level of service they feel they deserve. Grant Thorton discuss the what this means in practical terms.

Tech giants, such as Amazon or Netflix, have set the bar high for intuitive personalized user experiences. Many industries, including financial services, are rethinking their own customer service approach to match this new standard and meet the expectations of modern consumers.

It is increasingly evident that the future success or failure of financial services institutions will hinge on their ability to provide personalized user experiences. Institutions must seize the rich customer data that they already possess in order to optimize customer experience and differentiate from their competition. To achieve this outcome, they must shift their mindset, from one focused on what they want to offer to the customer to one that prioritizes what creates immediate value for the customer. In addition, they must be willing to allocate the necessary resources to drive this goal. To this purpose, they can use artificial intelligence (AI) to achieve brand differentiation.

We recently explored issues and opportunities related to customer experience in a joint webinar with Finovate – Data overload? The impact of AI on the customer experience – moderated by David Head, managing director, Grant Thornton, with panelists Carrie Russell, executive strategic advisor, Finn.ai; Tariq Bakhari, CEO, Aggresant, Inc.; Dave Brodsky, VP digital innovation, Wells Fargo; and Katy Gibson, vice president of product applications, Envestnet | Yodlee.

Webinar panelists discussed various ways in which AI can help financial institutions solve their differentiation-through-customer-experience challenge. While currently AI is still in its infancy, the technology has the potential to transform customer experience by enhancing the interaction with the customer, rather than replacing humans with bots.

Paving the way for AI, many banks have implemented machine learning (ML) and natural language processing (NLP), primarily in their back office, to reduce labor costs and increase productivity. In the near future, AI can revolutionize retail banking and other financial service offerings by becoming an omnipotent artificial brain behind the scenes to improve customer interaction and increase personalization.

Here are several insights from the webinar, regarding applications of AI (and of other related technologies) that can create immediate value for the customer:

Simplify processes.

Allow customers to execute simple transactions through user-friendly tools that leverage their data. In this way, they will see how access to their data creates direct, personal value.

Offer customers personalization and optimization of their experience based on live data.

AI can replace annoying surveys through real-time data mining and by interacting with customers in real time, eliminating the need for the survey feedback loop. As a transformative technology, AI empowers automated financial assistants that provide updated, real-time customer interactions.

Offer recommendations to motivate financial customer behavior.

Savvy financial services institutions can partner with fintech companies to establish trusted relationships and create a financial wellness experience for their customers. This includes using customer data to help them achieve their short- and long-term goals. Institutions can create tools to help customers: 1) keep on top of day-to-day finances to answer immediate questions quickly (e.g. a financial calendar that can keep track of a customer’s account balance until payday and send bill payment reminders, etc.); and 2) think through long-term financial planning.

Use AI or related technologies (e.g. ML, NLP) to enhance rather than replace human interaction.

AI can enhance the customer experience even when it is not customer facing. For example, call centers can follow 2 paths for interaction with customers: 1) they can be fully automated and chatbots can simply answer calls; or 2) they can use a mix of human and artificial intelligence, where chatbots can aid human call center representatives interact with customers effectively. So far, the second has proved more effective than the first.Turnover and training are well known challenges for call centers. Customers can feel dissatisfied with a call center representative that does not have an answer to their query; the representative can feel that, despite his best effort, he does not have access to the right information to answer the query. AI can help with this issue, not necessarily by replacing representatives and human interaction, but rather by facilitating speed and access to information to help representatives create an outstanding customer experience. This can be particularly effective with new hires that have to get up to speed fast.

Get the right channel. Go where the customer is likely to be.

Customers expect personal experiences that make their lives easier. For example, customers spend most of their time on their cell phones and have started using virtual voice-enable assistance more and more. Financial institutions need to meet the customers where they are to offer convenience and ease of use. This insight should guide investment in new tools. Conversational assistants/virtual assistants can be used for day-to-day transactions and allow customers to explore additional products and services, policies and other information.

Think through infrastructure challenges that limit the customer experience.

When planning investments in AI tools, financial institutions need to think proactively about current infrastructure challenges and future infrastructure advances. Delivering differentiation through technology depends on the capacity of the technological infrastructure to support the tool. At the high end of the technology infrastructure spectrum, 5G capabilities may enable the Internet of things (IoT) new data sources. Are banks/financial institutions prepared to collect and leverage this new data? At the low end, many US citizens barely connect to broadband because of the areas in which they live. Are they untapped customers? What tools/channels work for them, as they are dependent on the limited availability of infrastructure now and in the future?

Financial services institutions are in an excellent position to build a solid technological foundation that will make use of new customer data in meaningful ways. At this critical point, the question remains how to evaluate and select the appropriate tools and how to find a manageable pace of adoption.

In crypto, when the going gets good, the good go institutional.

Digital asset platform Coinbase has launched a set of new tools and resources designed to help institutional investors take advantage of the boom in cryptocurrencies. The solutions, as Coinbase General Manager Adam White described them in a blog post earlier today, represent the sort of “institutional grade products and services” that will enable FIs to participate in the cryptocurrency markets.

First up is Coinbase Custody. Designed in partnership with an SEC-regulated broker-dealer, Coinbase Custody provides secure crypto storage and third-party auditing and financial reporting validation. We first reported on Coinbase Custody last fall when the company announced that access to an early version of the technology would be available in 2018.

Second, Coinbase announced further development of its electronic marketplace, Coinbase Markets, with the launch of a new engineering office in Chicago. The company plans to leverage the area’s “large talent pool of engineers with deep exchange infrastructure experience” to add new features to Coinbase Markets, such as low latency performance, on-premise data center colocation services, institutional connectivity and access, and settlement and clearing services. The goal, White wrote, was “tighter markets, deeper liquidity, and increased certainty of execution.”

Third, Coinbase Prime will give institutional investors the specialized resources they need in order to effectively trade cryptocurrencies. This includes lending and margin financing for qualified customers, high touch and low touch execution services, as well as new market data and research products. Coinbase Prime will also feature multi-user permissions and whitelisted withdrawal addresses.

Last in the company’s suite of solutions launched today was the Coinbase Institutional Coverage Group. These sales, research, operations, and client services support professionals work exclusively with institutional clients and bring years of experience from companies like the New York Stock Exchange and Morgan Stanley, and agencies like the SEC and CFTC.

“The cryptocurrency market is maturing rapidly as more sophisticated institutional participants enter the space,” White wrote. He noted that 100 hedge funds have been created to speculate and invest in cryptocurrencies in recent months and that “some of the world’s largest financial institutions” have gone on record with plans to develop crypto trading desks.

Founded in 2012 and based in San Francisco, California, Coinbase demonstrated its Instant Exchange platform at FinovateSpring 2014. The company added its first Chief Technology Officer last month, appointing Balaji Srinivasan to the post as part of the its acquisition of digital currency startup, Earn.com. Also in April, Coinbase launched a new fund, Coinbase Ventures, to support early-stage crypto startups. With a valuation of $1.6 billion, Coinbase is one of fintech’s more recent unicorns (startups with more than $1 billion valuation) and the first bitcoin company to achieve unicorn status.

Relationship marketing hub Optimove has taken a step further in helping brands build an emotional relationship with their customers. The New York-based company announced today it acquired DynamicMail from PowerInbox.

DynamicMail specializes in real-time email personalization and dynamic subscriber engagement and is expected to boost Optimove’s growth. Here’s how Optimove described the acquisition in its announcement: “After being built and developed as a brain, the company is now at a position to acquire muscle and give our clients a more holistic solution to their relationship marketing needs.”

The 3,000 brands that use Optimove can now email their subscribers that can be updated in real-time to keep the contents relevant at the time the consumer opens it. Brands can also include dynamic content such as countdown timers, videos, and information, such as weather, that is based on a reader’s current location.

As a part of the transition, eight of DynamicMail’s employees will join Optimove’s team. The financial details of the deal were not disclosed.

Optimove was founded in 2009 with a mission to “empower marketers with the emotional intelligence required to communicate with their customers most effectively at all times, via all available channels.” At FinovateFall 2017, the company’s CEO & Founder, Pini Yakuel, showcased the Science-first Relationship Marketing Hub. That same year, the company’s clients sent more than 3 billion personalized emails to their customers.

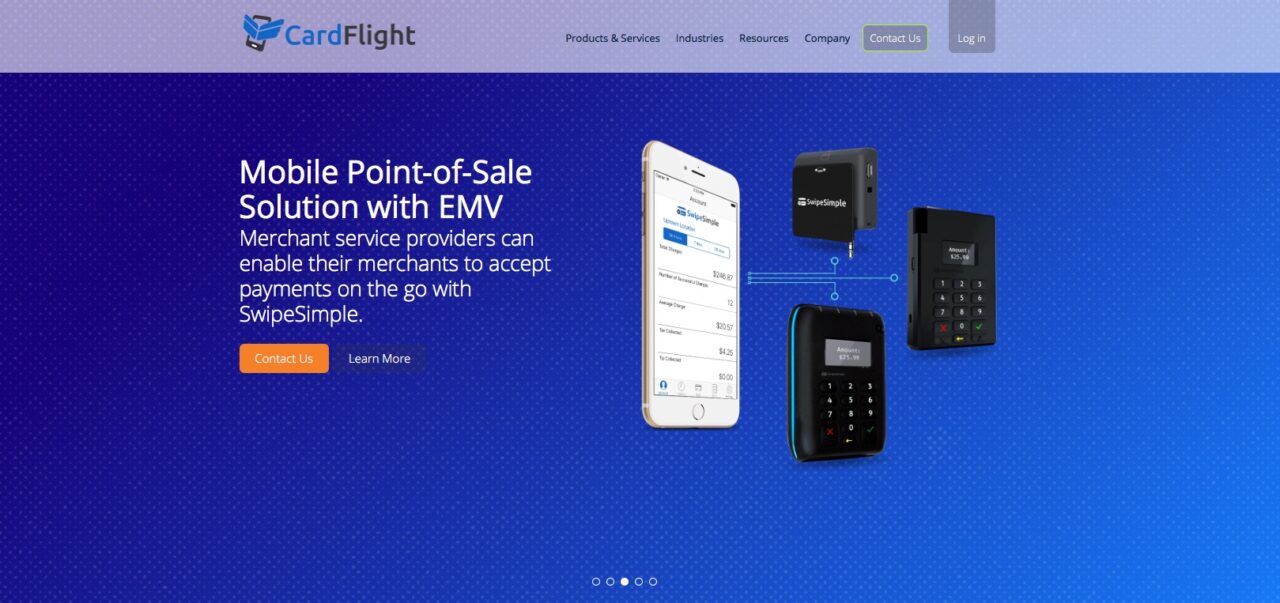

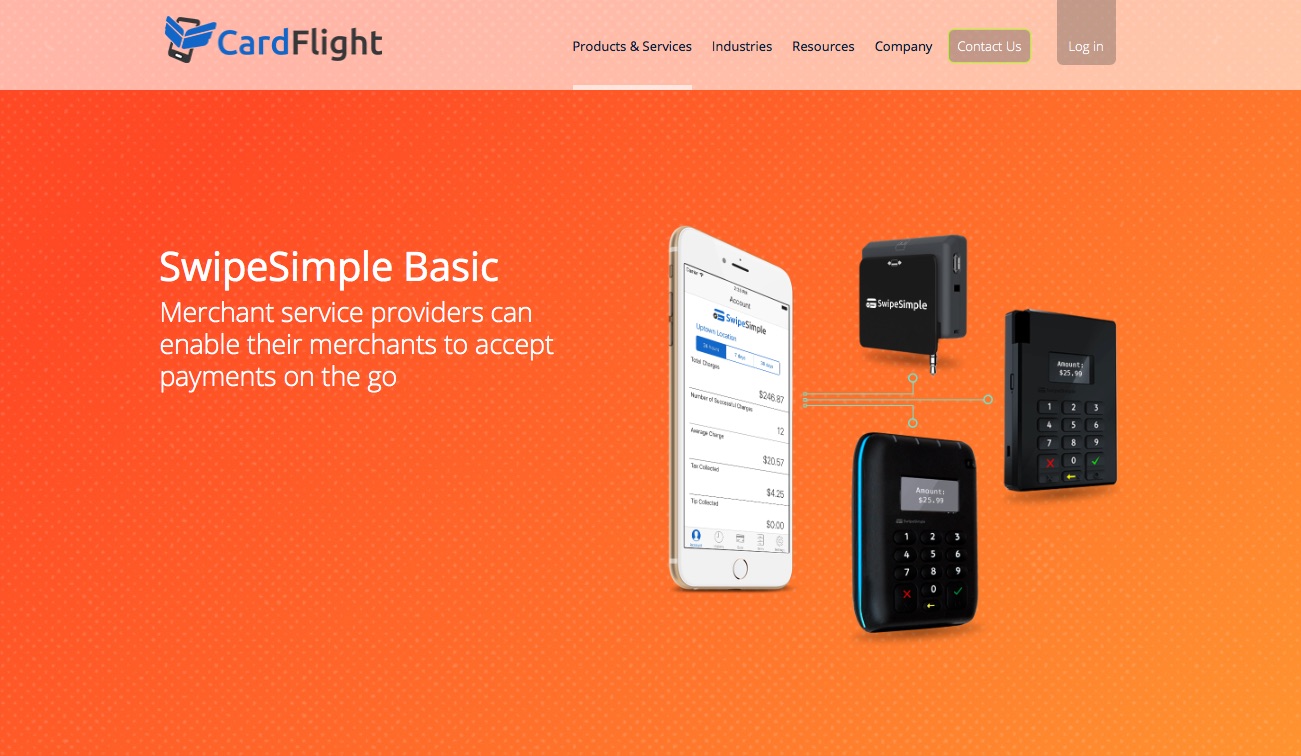

Mobile POS and SaaS payment solutions provider CardFlightannounced a new partnership with payment technology company Paya today. The agreement will enable Paya to offer CardFlight’s SwipeSimple payment acceptance solutions to its merchants.

Paya President Greg Cohen called SwipeSimple a “perfect fit” for its own payment services. “This collaboration allows us to offer our customers an advanced, secure mobile payment solution that helps answer many of their everyday business needs,” Cohen said. Paya has more than 100,000 clients who rely on the Reston, Virginia-based company’s adaptive solutions and two decades of experience in payments technology.

“Paya is one of the leading merchant service providers in the United States because of their commitment to arming their merchants with quality solutions and service,” CardFlight CEO Derek Webster added. “As the leader in EMV enabled card readers and payment acceptance solutions, CardFlight is happy to collaborate with Paya and provide SwipeSimple to their merchants.”

SwipeSimple enables merchant service providers, FIs, and independent sales organizations to offer their business customers a turnkey, EMV-ready mPOS solution. With CardFlight’s platform, Paya’s small business customers will get access to Bluetooth Low Energy or audio jack EMV Quick Chip, NFC contactless-enabled card readers; mobile and web apps to accept payments in-store or remotely; a back office merchant portal for business management and reporting; and a virtual terminal to enable merchants to accept CNP transactions using any device.

Founded in 2013 and headquartered in New York City, CardFlight demonstrated its mobile payment acceptance technology at FinovateSpring 2013. With 15 of the top 50 merchant acquirers in the U.S. among its partners, CardFlight has more than 40,000 small business end user customers, including merchants in all 50 states. This spring, the company introduced countertop payment terminals for small businesses, and announced that more than 80% of its SwipeSimple merchants had been upgraded to EMV quick chip payment acceptance.

CardFlight has raised $6.6 million in funding and includes MATH Venture Partners and ff Venture Capital among its investors.

Deutsche Börse and its post-trade services provider Clearstream will partner with Germany’s figo and Luxembourg-based regtech start-up Finologee to create a fintech acceleration platform, reports Antony Peyton of Fintech Futures, Finovate’s sister publication.

The new platform will enable established players and new digital firms to distribute and use each other’s services to ideally make more money.

It will allow access to Deutsche Börse’s market and reference data as well as functional services via APIs.

Marc Robert-Nicoud, CEO of Clearstream, said it brings together the “know-how and innovation capacity of an established market infrastructure with the innovative models and flexibility of strong fintech start-ups” and “can contribute immensely to developing new interaction, collaboration and monetization models”.

The first services offered by third parties will be an access to account gateway for banks for the second Payment Services Directive (PSD2).

Deutsche Börse has been cooperating with banking services provider figo since 2016.

The new partnership with Finologee is targeted to serve particularly the Luxembourg market with the “first end-to-end PSD2-compliant payment solution”. In addition, Finologee will contribute to the architecture and development of the platform software layers as well as further partnerships.

Clearstream contributes its IT infrastructure design and regulatory compliant operations, as well as several software components to run the API marketplace for Deutsche Börse.

First deployments on the platform are currently being evaluated. Among them are a number of offerings, including Budget Insight, IDnow, AriadNEXT, Governance.com, Jemmic, and KYCTech.

The platform is in the pilot phase and will be first offered as a development environment to allow testing and coding.

Further applications at this piloting stage will be Finologee’s identification and consent automation product.

Figo expands the portfolio with its PSD2-related RegShield for non-banks and PSD2 enabler for banks as well as several Clearstream and Deutsche Börse services.

The launch is targeted for the fourth quarter of 2018, subject to regulatory approval.

Founded in 2012 and headquartered in Munich, Germany, figo demonstrated its banking and payments API at FinovateEurope 2013. figo has raised more than $11 million (€10.1 million) in funding. Andre Bajorat is co-founder and CEO.

CardFlightTeams Up with Paya to Bring EMV-Ready Payment Solutions to Merchants.

CoinbaseUnveils Institutional Grade Solutions for Cryptocurrency Trading.

Around the web

Currencycloud and Cashplus partner to help SMEs save on international payments.

New risk screening feature from Thomson Reutersfilters unstructured data to help FIs fight financial crime.

IdentityMind Global to help decentralized private social media platform, ONe Network, meet KYC and AML compliance requirements.

Honor Credit Union ($850 million in assets) to launch member-owned, digital insurance agency courtesy of new partnership with Insuritas.

Consumers Credit Union ($968 million in assets) credits boost in deposit account openings to December deployment of digital sales platform from Gro Solutions.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

To use the new feature, users with the latest version of the Revolut app select the People Near Me option from the Payments tab. Enable Near Me and choose your location sharing preferences. When the list of Revolut users appears, make your selection, choose “send” or “receive” and confirm the amount. Note that the person or persons on the other end of the transfer will need to have their Near Me screen open and select their location sharing preferences, as well.

To use the new feature, users with the latest version of the Revolut app select the People Near Me option from the Payments tab. Enable Near Me and choose your location sharing preferences. When the list of Revolut users appears, make your selection, choose “send” or “receive” and confirm the amount. Note that the person or persons on the other end of the transfer will need to have their Near Me screen open and select their location sharing preferences, as well.

{kind=link}