This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

What is AI and how can financial services companies leverage it to their advantage? Simply put, AI – or artificial intelligence – is the development of computer systems able to perform tasks that normally require human intelligence.

What does AI do better than humans?

First, analysis. AI thinks faster, processing far more information at a much more rapid rate than a human mind.

Next, learning. AI designs better and more efficiently by leveraging faster thinking and data aggregation to build and select appropriate models.

Finally, creating. AI can build stronger solutions capable of self-improvement and optimization beyond original instruction.

The top three ways financial services companies can leverage the AI advantage are:

One: Predicting risk. This includes optimizing investment and tax strategies as well as proactively preventing fraud and bolstering security.

Two: Examining data: In addition to marketing, banks rely on data analytics for regulatory compliance and underwriting

Three: Emulating human behavior. Financial services companies can use natural language reporting capabilities, bolster the user interface with speech recognition, and enhance customer engagement using chatbots.

For more ideas on AI and a look at how other companies are leveraging the enabling technology, check out the Finovate blog and search AI.

FinovateSpring was a hotbed of future-looking technology. We spoke to Theo Lau, Innovator Technologist and Connector, Unconventional Ventures about why she thinks voice is the next UI.

Although voice may not a solution for all situations, there is no denying that the momentum and interest for voice technology is growing. In the Q3 2017 earnings report, Amazon disclosed that it has sold “tens of millions of Echo units” since the first release in 2015. According to “The Rise of Voice” report by Invoca, the voice opportunity is predicted to be worth more than $18 billion by 2023. Consumers have been using voice assistants from seeking information to playing music and shopping. Accessibility, convenience, and simplicity are some of the main reasons behind the user adoption. For those who cannot read or who may have trouble navigating the menu options on an app or website, ability to speak to a device offers a more intuitive option to obtain real-time information. Voice technology is also life-impacting for those suffering from isolation/loneliness. In all, it has the potential to become a more inclusive technology that can appeal to a board audience and serve a wide purpose.

Recognizing the potential and appeal, financial institutions such as Capital One, USAA, Bank of America, U.S. Bank, and Ally Financial have begun experimenting with various use cases. Applications thus far are still fairly rudimentary and focused on basic interactions such as checking balance, paying bill, and tracking spending.

Though voice banking is still at its infancy, the industry is quite bullish on its future. Capgemini predicts that 3 years from now, 40 percent of consumers will use voice assistants rather than website or app, and 31 percent will use a voice device instead of visiting a store or branch. Separately, Medici forecasts that approximately 1.83 billion customers will be using voice assistants by 2021. Financial institutions should leverage insights harnessed from these interactions to adapt the conversation to reflect their brand identity and user’s profile. As suggested by Mark Taylor from Capgemini: “A brand today is an image, a set of colors, something you see on TV, on a website or in a store. With a voice channel, you see nothing, so a brand needs to have an audible image.”

While we might not be at the “promise land” yet where the virtual assistants become truly conversational, we have made great strides. As with any technology, empathy is key. AI and voice technology has the potential to make businesses more human, allowing banks to truly focus on their customers and become their true partners.

Today’s customers demand that every experience provide immediate value on multiple levels. They require a competitive, friendly, quick and personalized user experience. They swear allegiance to no brand and are ready to jump ship to the first competitor that can offer them what they want, when they need it, and at the level of service they feel they deserve. Grant Thorton discuss the what this means in practical terms.

Tech giants, such as Amazon or Netflix, have set the bar high for intuitive personalized user experiences. Many industries, including financial services, are rethinking their own customer service approach to match this new standard and meet the expectations of modern consumers.

It is increasingly evident that the future success or failure of financial services institutions will hinge on their ability to provide personalized user experiences. Institutions must seize the rich customer data that they already possess in order to optimize customer experience and differentiate from their competition. To achieve this outcome, they must shift their mindset, from one focused on what they want to offer to the customer to one that prioritizes what creates immediate value for the customer. In addition, they must be willing to allocate the necessary resources to drive this goal. To this purpose, they can use artificial intelligence (AI) to achieve brand differentiation.

We recently explored issues and opportunities related to customer experience in a joint webinar with Finovate – Data overload? The impact of AI on the customer experience – moderated by David Head, managing director, Grant Thornton, with panelists Carrie Russell, executive strategic advisor, Finn.ai; Tariq Bakhari, CEO, Aggresant, Inc.; Dave Brodsky, VP digital innovation, Wells Fargo; and Katy Gibson, vice president of product applications, Envestnet | Yodlee.

Webinar panelists discussed various ways in which AI can help financial institutions solve their differentiation-through-customer-experience challenge. While currently AI is still in its infancy, the technology has the potential to transform customer experience by enhancing the interaction with the customer, rather than replacing humans with bots.

Paving the way for AI, many banks have implemented machine learning (ML) and natural language processing (NLP), primarily in their back office, to reduce labor costs and increase productivity. In the near future, AI can revolutionize retail banking and other financial service offerings by becoming an omnipotent artificial brain behind the scenes to improve customer interaction and increase personalization.

Here are several insights from the webinar, regarding applications of AI (and of other related technologies) that can create immediate value for the customer:

Simplify processes.

Allow customers to execute simple transactions through user-friendly tools that leverage their data. In this way, they will see how access to their data creates direct, personal value.

Offer customers personalization and optimization of their experience based on live data.

AI can replace annoying surveys through real-time data mining and by interacting with customers in real time, eliminating the need for the survey feedback loop. As a transformative technology, AI empowers automated financial assistants that provide updated, real-time customer interactions.

Offer recommendations to motivate financial customer behavior.

Savvy financial services institutions can partner with fintech companies to establish trusted relationships and create a financial wellness experience for their customers. This includes using customer data to help them achieve their short- and long-term goals. Institutions can create tools to help customers: 1) keep on top of day-to-day finances to answer immediate questions quickly (e.g. a financial calendar that can keep track of a customer’s account balance until payday and send bill payment reminders, etc.); and 2) think through long-term financial planning.

Use AI or related technologies (e.g. ML, NLP) to enhance rather than replace human interaction.

AI can enhance the customer experience even when it is not customer facing. For example, call centers can follow 2 paths for interaction with customers: 1) they can be fully automated and chatbots can simply answer calls; or 2) they can use a mix of human and artificial intelligence, where chatbots can aid human call center representatives interact with customers effectively. So far, the second has proved more effective than the first.Turnover and training are well known challenges for call centers. Customers can feel dissatisfied with a call center representative that does not have an answer to their query; the representative can feel that, despite his best effort, he does not have access to the right information to answer the query. AI can help with this issue, not necessarily by replacing representatives and human interaction, but rather by facilitating speed and access to information to help representatives create an outstanding customer experience. This can be particularly effective with new hires that have to get up to speed fast.

Get the right channel. Go where the customer is likely to be.

Customers expect personal experiences that make their lives easier. For example, customers spend most of their time on their cell phones and have started using virtual voice-enable assistance more and more. Financial institutions need to meet the customers where they are to offer convenience and ease of use. This insight should guide investment in new tools. Conversational assistants/virtual assistants can be used for day-to-day transactions and allow customers to explore additional products and services, policies and other information.

Think through infrastructure challenges that limit the customer experience.

When planning investments in AI tools, financial institutions need to think proactively about current infrastructure challenges and future infrastructure advances. Delivering differentiation through technology depends on the capacity of the technological infrastructure to support the tool. At the high end of the technology infrastructure spectrum, 5G capabilities may enable the Internet of things (IoT) new data sources. Are banks/financial institutions prepared to collect and leverage this new data? At the low end, many US citizens barely connect to broadband because of the areas in which they live. Are they untapped customers? What tools/channels work for them, as they are dependent on the limited availability of infrastructure now and in the future?

Financial services institutions are in an excellent position to build a solid technological foundation that will make use of new customer data in meaningful ways. At this critical point, the question remains how to evaluate and select the appropriate tools and how to find a manageable pace of adoption.

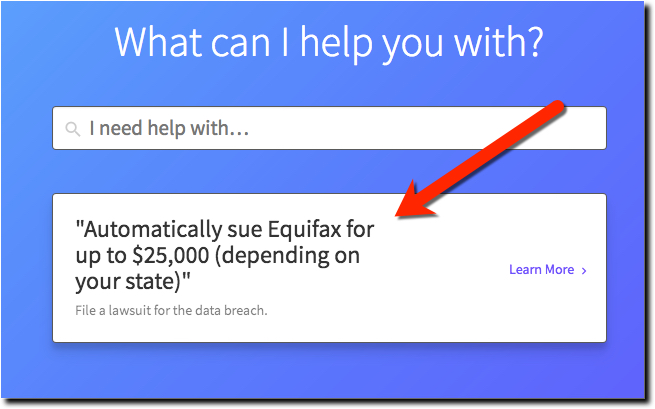

There’s an interesting article in today’s WSJ about DoNotPay, a free AI-powered chat-based service that was built to help London residents automatically fight parking tickets. That service has now assisted 400,000 consumers fight off $11 million in fines (more background at TechCrunch).

It’s the brainchild of then 17-year old Joshua Browder (who is now 19, and of course, studying CS at Stanford). But Browder is not content beating the meter reader. He is now gearing up to equip everyone with free AI-powered law tools to take on bigger injustices and issues (see DoNotPay overview video above). His latest work, a tool to make it easy to process a no-fault divorce, something that typically can cost $10,000.

The article mentioned a few more areas ripe for this type of tool: airline restitution for delays and lost luggage and battling telemarketers and landlords.

But one area that’s sure to attract multiple consumer AI startups: bank fees, penalties, credit decisions, and more. What are you going to do when you start receiving hundreds, if not thousands, of cease & desist letters challenging NSF charges, late payment fees, and so on? Or worse, suing you in small claims court or threatening arbitration (see the current default “problem” at DoNotPay, how to sue Equifax for $25,000, inset).

You are not going to be able to afford the legal expense to fight for a $35 NSF fee. Eventually, you’ll have your own AI to fight their AI, but that’s a ways away (though if you saw Tim Huber’s AI talk at FF, it may be closer than we think).

An even bigger issue are all those sketchy charges on bank credit and debit card. It’s not a stretch to imaging the consumer’s AI routinely filing disputes and following up over and over again until you and/or the merchant capitulate.

Bottom line: Make sure your penalty fees are appropriate, well communicated, and understood by customers. And you might want to pay a bit more attention to new technologies available to answer customer queries, and even legal threats, in a semi-automated fashion.

Author: Jim Bruene (@netbanker) is Founder & Senior Advisor to Finovate as well as Principal of BUX Advisors, a financial services user-experience consultancy.