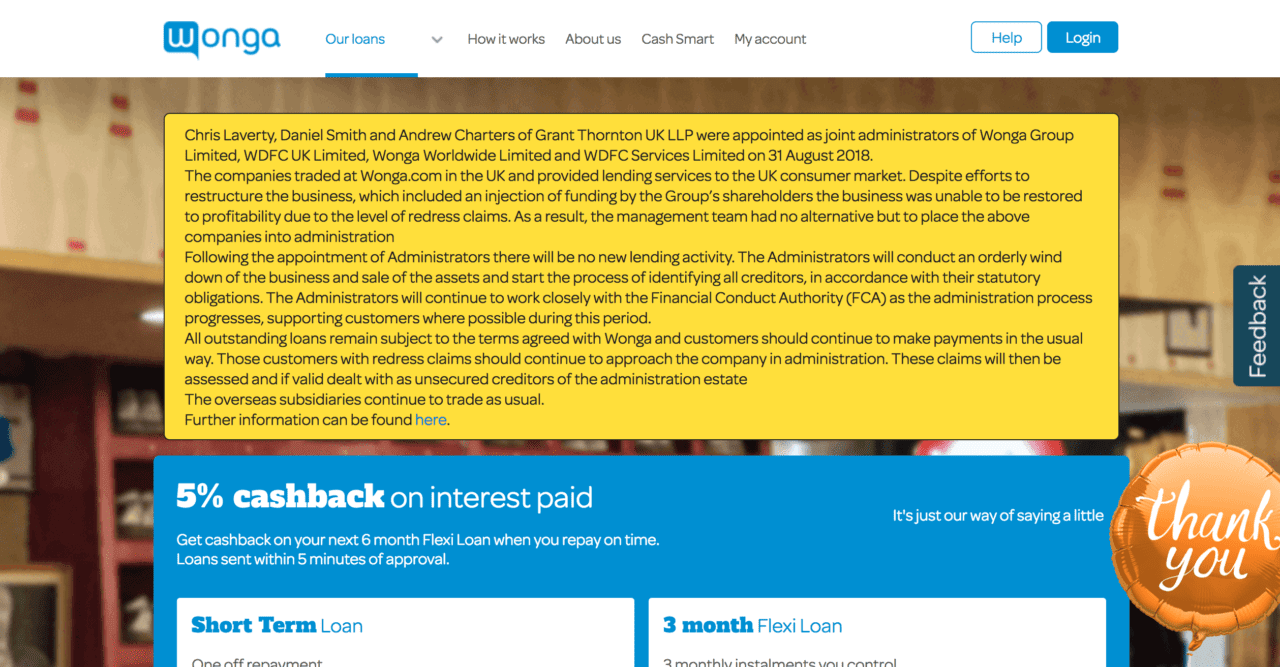

You’ve heard by now that short-term lending platform Wonga has shut down after launching in 2007. All drama aside, the scenario offers a real-life look at what would happen if a large payday lender closed its doors.

Wonga has received an increase in complaints over the past few years that it did not sufficiently verify that borrowers were able to repay their loans. These complaints, which were generally regarding loans made before new rules were introduced in 2014, lead to a large rise in compensation payouts. According to Wonga’s website, more than 24,800 complaints have been opened, 22,000 have been closed, 31% of which have been upheld.

This unexpected expense lead to financial trouble that prompted an injection of $13 million in capital earlier this year. Despite the funds and efforts from investors, Wonga’s financial situation remains untenable. Notably, two other U.K. startups, Cash Genie and Cheque Centre, both closed due to similar pressure.

At this point, three appointees from Grant Thornton U.K., Chris Laverty, Daniel Smith, and Andrew Charters, have been appointed as joint administrators of Wonga. Here’s what will follow:

- The platform is closed to new lending activity.

- Borrowers must still repay loans.

- Unless Wonga has already agreed to pay a claim, complaint claims are not likely to be paid out, since the recipient is seen as an unsecured creditor.

- The administrators will wind down the business, sell the assets, and begin identifying all creditors in accordance with their obligations.

This may end up having a small negative effect on peer-to-peer lenders, such as U.K.-based Zopa and U.S. based Lending Club, as they rely on balancing investor funds with borrower demand. If too many investors fear a shutdown, they may be more hesitant to lend, making it more difficult for the platforms to meet borrower demand.

Founded by Errol Damelin, Jonty Hurwitz, Wonga demonstrated at FinovateFall 2010. The company had raised a total of $159 million. Sky News reported earlier this year that the company “once had ambitions of a New York listing that could have valued it at well over $1 billion (£769m).”

A look at the companies demoing live at FinovateFall on September 24 through 26, 2018 in New York. Register today and save your spot.

Presenters

Presenters Tom Stinton, Head of Product and Design

Tom Stinton, Head of Product and Design

Presenter

Presenter

Presenters

Presenters

Presenters

Presenters Steve Frook, VP Sales

Steve Frook, VP Sales

Presenters

Presenters Siddhesh Yawalkar, Senior Software Engineer

Siddhesh Yawalkar, Senior Software Engineer