This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In a round led by Qatar Investment Authority (QIA), personal finance solution provider SoFi has raised more than $500 million in equity funding. The new capital gives the San Francisco, California-based company a valuation of $4.3 billion, and will drive investment, the company said in its press release, in continued innovation and growth. SoFi’s total capital now stands at $2.3 billion.

QIA CEO Mansoor Al-Mahmoud highlighted SoFi’s long-term vision, which has enabled the company to evolve into a major personal finance platform for both lending and wealth management. “We strongly believe in SoFi’s approach, and their dedication to build a transformational financial platform that is rapidly disrupting consumer finance,” he said.

In his statement, SoFi CEO Anthony Noto underscored the company’s transformation, as well. “Over the last year, we’ve worked aggressively to grow SoFi from a desktop lending business to a broad-based, mobile-first financial platform enabling members to borrow, save, spend, invest, and protect their money,” Noto said.

With more than 700,000 members and 7.5+ million registered users, SoFi offers a variety of personal finance solutions in lending and wealth management. These include the company’s student loan refinancing and mortgages offerings, as well as newer products like SoFi Invest and SofiMoney.

SoFi Invest, launched at the beginning of the year, is a stock and ETF trading and investing platform that also allows for automated investing. SoFi Money combines the best of checking and savings accounts into a single account with a 2.25% APY and an app to facilitate mobile spending, saving, and payment.

Earlier this month, SoFi announced that it was introducing an exchange-traded fund based on the gig economy, GIGE. The actively managed fund – run by Toroso Investments – enables investors to participate in the stock market gains of companies like eBay, Lyft, Square, and Twitter. In April, the company teamed up with Lemonade and Root to add to its insurance offerings.

SoFi, in partnership with Quovo, participated in our developers conference, FinDEVr New York 2017. At the event, the two companies led a presentation, How Quovo and SoFi Perfected Bank Authentication, which won the duo a Favorite FinDEVr Alum award. SoFi was founded in 2011.

Plaid, a provider of APIs for financial infrastructure, announced its expansion into the U.K. this week. The move makes a lot of sense– an open banking fintech is launching in the motherland of open banking.

“We’re building a financial network that will deliver on the promise of open banking with the best in both local expertise and global opportunity,” Keith Grose, International Lead at Plaid said in a blog post.

The U.K. is Plaid’s second international market after launching in Canada last year. The expansion overseas initiates the San Francisco-based company’s more comprehensive launch into Europe as a whole.

Plaid elected to launch in the U.K. because, as some have argued, the region is the fintech capital of the globe. More than 1,600 fintech companies have come out of the U.K. and that number is projected to double in the next ten years.

Today’s news is as much about Plaid launching in the U.K. as it is about opening up the possibility for its client applications to do business in the region, as well. Venmo, Robinhood, Coinbase and Acorns all use Plaid to connect to their customers’ U.S. bank accounts, and can now more easily expand into Europe using existing integrations.

Plaid, which was granted its AISP license from the U.K.’s Financial Conduct Authority last October, currently offers five of its products in the U.K.:

Auth, an account authentication tool

Balance, which pulls account balance information in real-time

Identity, which leverages bank data to verify consumer identity

Transactions, which pulls bank statement data across banks

Assets, a verification of assets tool

Missing from this list is Plaid’s Income product, a tool that validates a consumer’s income and verifies direct deposit data.

At FinDEVr San Fransisco 2014, the company’s founder, Zach Perret gave a presentation about leveraging the Plaid API for financial infrastructure. Plaid has raised $310 million since it was founded in 2013. After the company’s most recent investment last year, TechCrunch estimated Plaid to be valued at $2.65 billion.

Plaid began 2019 by acquiring its competitor Quovo in a $200 million deal. At FinovateSpring earlier this month bill payment platform doxoannounced it is leveraging Plaid to bring customers overdraft protection when paying their bills online. And last week, Plaid unveiled Plaid Direct, a lightweight integration that makes banks and fintechs a data source in the Plaid network, allowing end customers to enjoy open banking connectivity across financial service providers.

From banking chatbots to speculations on superintelligence, the impact of artificial intelligence (AI) on financial services is one of the hottest topics in fintech. Our Summit Day sessions on AI at FinovateSpring earlier this year were consistently among our best attended sessions.

To continue this conversation, we exchanged emails with Alenka Grealish, Senior Analyst, Corporate Banking, Celent. Grealish’s recent report, AI in the UI: Adoption, Use Cases, and Business Cases, represents Celent’s latest investigation into the issues surrounding the rise and role of AI in financial services.

Finovate: In setting up this conversation, I noted that Celent referred to this as part of an inaugural initiative. Why is now the time to turn the spotlight on this technology and its impact on financial services?

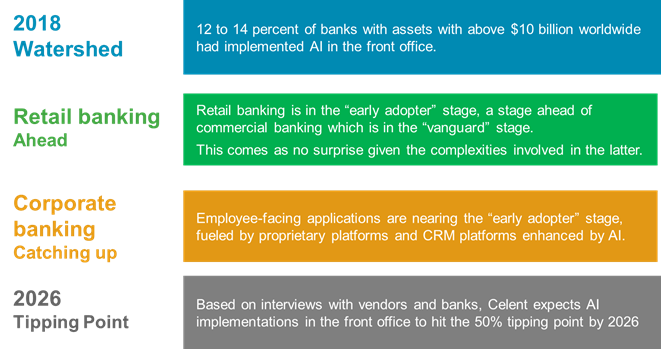

Alenka Grealish: We observed the beginning of a shift from all experimentation to gradual implementation amongst vanguard banks. It was common to have nine proofs of concept to one pilot at the vanguard banks. We’re now seeing more pilots and a few moving into production.

Finovate: What are we talking about when we talk about AI? How broad is this technology?

Grealish: Broad. What defines AI has expanded in the commercial world. The narrow Turing Test no longer applies. The current goal of AI developers is not to replicate humans, but rather complement them and build applications that team with them. A great example is found in anti-money laundering.

The broad definition includes rules-based and learning-based models. A useful way to categorize AI capabilities is: natural language processing and understanding, natural language generation (data-to-text), speech (speech-to-text and vice versa), vision, and data insights (machine learning driven analytics that generate, for example, cash flow forecasts for customers and next best action for bankers).

Finovate: Has AI become a catch-all for a variety of technologies, some of which are AI and some of which are not? And is that an issue for AI adoption going forward?

Grealish: AI has certainly become a buzz word and its definition stretched by tech vendors. Semantics aside…Critical to successful AI adoption is not to seek a problem for AI to solve but rather the reverse: determine the key problems you’re trying to solve (e.g., high false positives in AML) and/or goals you’re trying to achieve (e.g., personalize customer-banker interactions). Then, (the next step is to) examine the potential means to solve/achieve. The means could be a combination of rules-based and learning-based AI or established tech (e.g., OCR) combined with AI.

Finovate: What were the top two or three high-level takeaways from your research?

Grealish: I was struck by the percentage of banks $10+ billion in size which had implemented front-office AI. I had expected less than 10%.

Finovate: Your report notes a difference in AI adoption between retail and commercial banks, calling the former an “early adopter” and the latter “vanguard.” What distinguishes the two?

Grealish: The vanguard phase is when a small number of entities, less than 5%, moves into production. The technology is not mature but works sufficiently well for low risk use cases. These entities tend to have nimble organizations and little to no legacy baggage. The early adopter phase typically occurs when the vanguard banks are successful and appear to be gaining a competitive edge and inspire the next wave of adopters to take action. The early adopters are innovators but are likely juggling multiple priorities and hence cannot always be in the vanguard.

Finovate: One of the areas you highlight is the use of AI-enabled technologies for employees and workers. What sort of use cases – especially those relevant to financial services – are you seeing here?

Grealish: In terms of employee enablement, I’m excited by what I see. AI is proving helpful in basic “tell me” support, such as, “do we offer this type of product?” and “where is this feature located in our online portal?” It is also progressing in higher level support, such as data insights on sales trends and next best action suggestions.

Finovate: You note “relative complexity” as a main hurdle to broader adoption of AI. How are financial services companies navigating this challenge (hiring talent, partnerships, etc.)?

Grealish: AI is not a standalone technology but rather is woven into current processes and platforms and/or drives new processes and platforms. Hence, success begins at the top of the house, banks with a transformation, data-driven leadership team view AI as one component of a broader digital strategy.

Next, successful banks have a business model comprising four key elements: a collaborative multidisciplinary organizational dynamic, an enterprise-wide AI initiatives team, strong data and model governance, and regulatory engagement and compliance playbook. At the operating model level, these banks have basic automation expertise and are incorporating AI to solve the hard stuff, such as analysis of unstructured data.

At the foundation, these banks are migrating to a modern data and tech infrastructure that supports a digital-first strategy.

Finovate: You note that the primary business goal for most businesses using AI-enabled technologies is cost savings, but that customer engagement “is increasingly a goal.” What are some of the more interesting use cases for AI-enabled technologies in customer engagement?

Grealish: We’re in the very early days of customer engagement, that is, brief, basic “tell me” conversations. These “tell me” conversations are taking off thanks to Siri, Alexa, Google Assistant, which are driving consumers’ comfort level engaging with machines. The outlook over the next 5 years is promising. “Do it for me” type interactions will become common. For example, a small business will simply ask the online virtual assistant to choose the optimal payment type based on its criteria. Further on the horizon are “Alert and advise me” type interactions. For example, a mid-market company has an FX exposure and is alerted with action options to hedge the exposure.

SoFiAnnounces $500 Million Investment Led by Qatar.

Around the web

Trustlylaunches automated invoice payment solution, Pay Your Invoice.

PayPalreaches $10 billion in small business loans issued via its business financing offerings.

Mastercard and UOB partner to introduce the UOB Retail Business Metal Card designed for APAC SMEs.

Kofaxlaunches its Intelligent Automation software platform.

Brazilian exchange brokerage, Frente Corretora de Cambio, goes live with cross-border remittance solution powered by Ripple technology.

Fenergounveils a new suite of CLM tools, Digital Client Orchestration.

Trulioonamed best identity verification and authentication solution at 2019 CNP Expo.

KyckGlobal partners with InComm to provide same-day pay to gig workers.

Sam Kilmer offers 3 takeaways of FinovateSpring 2019 in 3 minutes.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

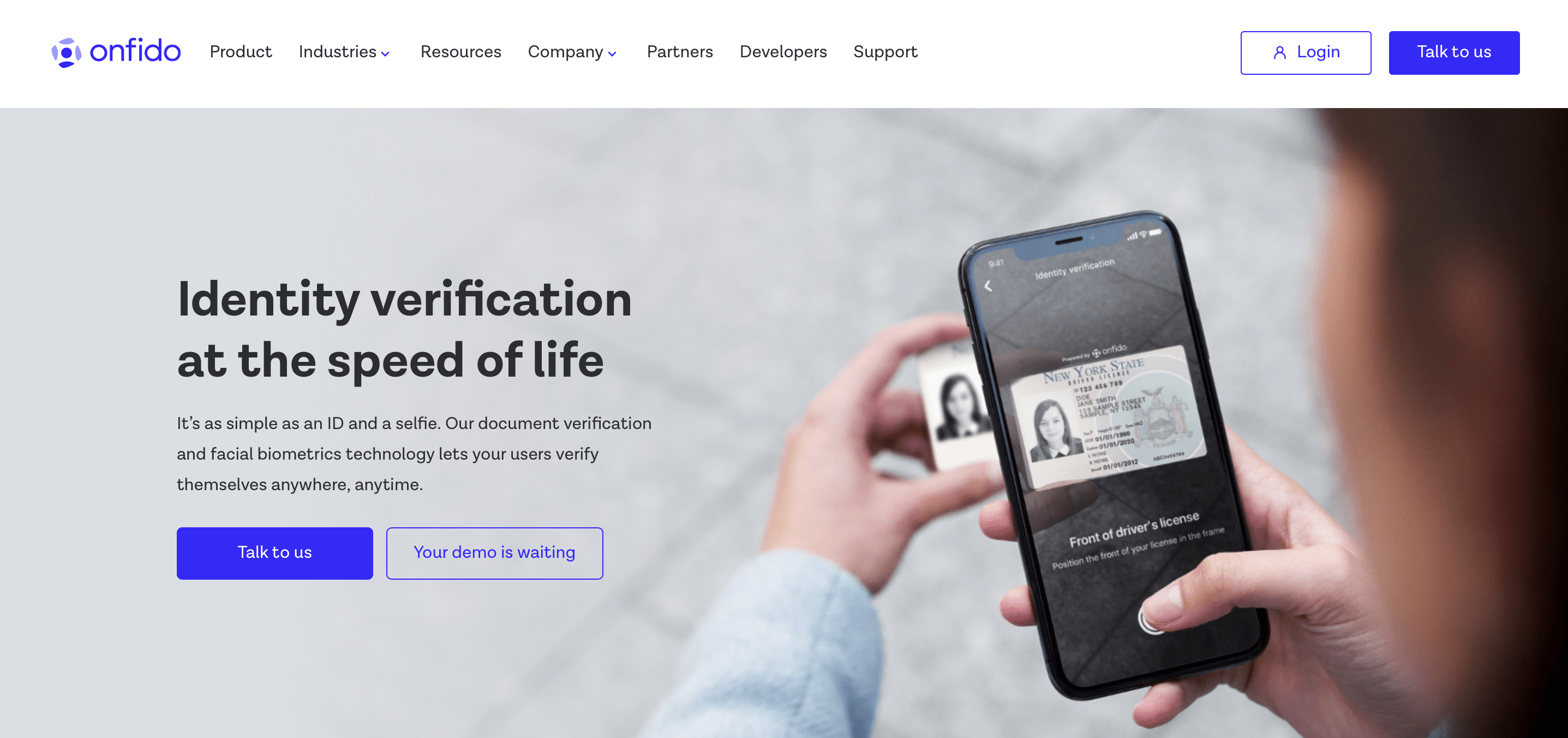

Courtesy of a partnership with ID document verification specialist Onfido, Checkr has launched a new solution that will enable businesses to add identity verification to their trust and safety programs. The new solution, Checkr Connect IDV, leverages Onfido’s technology to verify the user’s ID and conduct a biometric check comparing the image on the ID to a selfie taken by the user.

Combined with Checkr’s AI-powered background check technology, the new offering gives businesses a unified identity verification and background check solution. Available in the fall, Connect IDV will help businesses avoid some of the hurdles – from complex integrations to a dependance on multiple manual processes – that have discouraged businesses from using identity verification solutions more completely.

“Identity verification and background checks are becoming increasingly important in our digital society and (are) an essential step for every company that wants to grow its customer base or workforce,” CEO and co-founder of Onfido Husayn Kassai explained. “By embedding our identity verification technology within Checkr’s platform we can now offer customers what they have been asking for: a strong, seamless solution for their end-users.” Kassai called this a “shared priority” between the two companies.

“Every business today faces increased risk from identity fraud, and traditional anti-fraud methods are falling behind the capabilities of sophisticated bad actors,” VP of Product at Checkr Lydia Varmazis said. “We designed Checkr Connect IDV to make it simple for our customers to add identity verification into their hiring workflows, allowing them to elevate their trust and safety programs.”

San Francisco, California-based Checkr was founded in 2014 by Daniel Yanisse (CEO) and Jonathan Perichon (CTO). The company offers solutions for continuous background checking, quality screening, and well as security resources, and includes Uber, Instacart, and GrubHub among its 10,000+ customers. Checkr has raised $149 million in funding. T. Rowe Price, Y Combinator, and Accel are among the firm’s investors.

Founded in 2012 and based in London, U.K., Onfido demonstrated its Facial Check with Video technology at FinovateEurope 2018. More recently, the company announced a partnership with mobility-as-a-service firm Drover, and earned a spot in the inaugural cohort of cross-border regulatory sandbox, Global Financial Innovation Network (GFIN).

Onfido picked up a major investment this spring, adding $50 million in new capital and taking the company’s total funding to more than $100 million. Onfido added C-level talent this year, as well, hiring Kevin Goldsmith as Chief Technology Officer and Thomas Ammirati as Chief Revenue Officer.

Merchant acquirer Global Payments has agreed to buy issuer processor firm Total System Services (TSYS) in a $21.5 billion deal, reports Jane Connolly of Fintech Futures (Finovate’s sister publication).

The two companies confirmed the deal today (May 28) in what will be the payment industry’s third “mega-merger” of 2019. The all-stock deal values TSYS at $119.86 per share, a rise of 20% since before news of the talks started to emerge.

Global Payments shareholders will own 52% of the combined company, while TSYS investors own 48%. TSYS CEO Troy Woods will become the chairman.

The combined entity will provide payment technology and software to more than 3.5 million small to medium-sized merchants and over 1,300 financial institutions worldwide.

It is expected that the deal, anticipated to close in the fourth quarter, will generate around $8.6 billion in adjusted net revenue annually plus network fees and make cost savings of $300 million.

TSYS was founded in 1983 and is headquartered in Columbus, Georgia. The company demonstrated its Authorization Controls solution at FinovateAsia 2013, showing how the technology enabled users to set their own default account parameters and authorization rules.

As Finovate goes increasingly global, so does our coverage of financial technology. Finovate Global: Fintech News from Around the World is our weekly look at fintech innovation in developing economies in Asia, Africa, the Middle East, Latin America, and Central and Eastern Europe.

Central and Eastern Europe

FintechOS of Romania raises $1.23 million (€1.1 million) in post-seed funding.

Elvira Nabiullina, head of the Central Bank of Russia, talks about the state of Russian fintech.

Lithuania’s Evarest to launch a stock trading app in the second half of the year.

Vents Magazine highlightsTrustly’sPay’N Play technology.

The 2019 Aspire Leaderboard recognizes Quadient as overall leader for CCM for the second year in a row.

Star Tribute profilesSezzle and its plans to go public in Australia later this year.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.

Biometric authentication specialist Fortress Identity has partnered with Visa this week. Under the agreement, Visa cardholders in Latin America and the Caribbean will have their transactions protected by means of Fortress Identity’s biometric technologies.

Fortress Identity will use voice prints, phone codes, as well as active and passive biometrics to authenticate users. “We want Visa cardholders to feel absolutely confident that their funds and personal data are safe whenever and wherever they use their Visa cards,” said Fortress Identity CEO Alessandro Chiarini.

“Multi-factor user authentication is critical in today’s interconnected commerce space, and verifying the identity of people attempting to access the network is key to reducing many types of fraud, including chargebacks,” said Eduardo Perez, SVP and Risk Officer for Visa Latin America and the Caribbean.

Fortress Identity will also collaborate with Visa technology partners including YellowPepper, a payment platform provider; NovoPayment, a banking as a service platform; and HST, an EMV vendor.

Founded in 2015, Fortress Identity leverages a suite of biometrics technologies to protect users in mobile iOS and Android applications, Microsoft Active Directory environments, and Citrix applications. The Miami, Florida-based company demoed its active and passive biometrics technology earlier this month at FinovateSpring. Fortress Identity has eight employees and has raised $3 million.

Global Treasure Bank (GTB) in Myanmar has implemented Infosys Finacle’score banking solution to power its retail and corporate operations, reports Jane Connolly of Fintech Futures, Finovate’s sister publication.

Finacle is understood to have replaced the Kastle core banking system from another India-based vendor, 3i Infotech.

Since the implementation, the bank says it has signed up nearly 75,000 new accounts of various types, with each onboarding process taking just minutes. It has also seen improved control and productivity in its 163 branches, thanks to built-in workflow engines.

GTB is now processing an average 300,000 mixed transactions per day and is benefiting from the “360-degree view of customer relationships and transactions” that Finacle provides.

“For over two decades, GTB has stayed true to our mission of comprehensive economic development of Myanmar through reliable, inclusive and convenient banking services,” said U KoKo Aung, CEO of GTB. “Today, to continue to abide by this commitment in an increasingly complex regulatory and competitive environment, we felt the need for a modern platform to power our banking strategy.”

Venkatramana Gosavi, senior vice-president and global head of sales at Infosys Finacle stated that the Myanmar banking industry is undergoing a transformation.

He added, “With Finacle, GTB has gained a strong foundation to boost agility and efficiency of operations, and significantly improve customer experience across channels.”

The implementation process was aided by ACE Data Systems, Finacle’s business partner in Myanmar.

Finacle, part of EdgeVerve Systems, a subsidiary of Infosys, showcased EdgeVerve Blockchain Framework for Financial Services at FinovateEurope 2017. At the start of 2018 Infosys teamed up with Tradeshift to help clients digitize supply chain management. At the start of this year, the company partnered with Qatar National Bank.

Banking technology vendor Temenos is partnering with UBX to deliver digital banking to millions of unbanked and underserved customers in the Philippines, reports Jane Connolly of Fintech Futures, Finovate’s sister publication.

The fintech subsidiary of UnionBank of the Philippines, UBX has developed a range of plug-and-play services to help rural banks reach customers in remote communities.

These include the blockchain-based i2i turnkey solution, which connects rural banks to each other and to the Philippines’ main financial networks.

Having partnered with Temenos, UBX can now offer core banking software to its partner financial institutions, through Temenos T24 Transact.

Temenos says its cloud-native, cloud-agnostic, API-first banking software will provide greater levels of agility and scalability for rural banks, cooperatives and microfinance institutions.

“At UBX, our mission is to build platforms that bring businesses and people together,” says John Januszczak, CEO of UBX. “As part of that, we provide access to needed technology and services while connecting communities.

“The rural banking community in the Philippines has been championing financial inclusion for decades. Temenos will help us provide the most tailored, innovative and advanced core banking solution to our rural banking customers.”

The partnership aims to deliver digital banking to millions of people over the next five years.

Founded in 1993, Temenos debuted its Connect Mobile Banking application at FinovateEurope 2015 in London. With clients in 145+ countries, Temenos employs more than 4,600 people in 63 offices. The company has a market capitalization of $12.5 billion.

This post will be updated throughout the day as news and developments emerge. You can also follow all the alumni news headlines on the Finovate Twitter account.